Business Opportunities In Community Development Lending : Manchester

This Event Has Ended

#1 reason people come to NH Small Business Development Center … is access to capital. “We’re not a lender,” says Mary Collins of the NH SBDC, “but we prepare people.” Small businesses need a foundation of knowledge and skills, which the SBDC can provide.

Banks, nonprofits, government and quasi-government lenders met to explore how collaboration makes affordable housing, small business, commercial real estate, economic development happen.

Panelists identified almost a dozen nontraditional sources of capital or credit.

They include Community Development Block Grants, Low Income Housing Tax Credits, Small Business Administration, Community Reinvestment Act funding from financial instiutitons, Capital Access Program (NH Business Finance Authority), Individual Deposit Account (IDA) Programs, Revolving Loan Funds, Equity Equivalents (EQ2).

To cosponsor a meeting on this topic, contact Claire.M.Greene@bos.frb.org.

Strategies for success

How to work effectively with cities and towns

Concord’s Deputy City Manager Carlos Baia says municipalities and development teams must build relationships with all parties involved. “The easy deals have all been done. We’re talking about deals that require funding sources from a half-dozen places at least.”

Even the most worthy projects have aspects that might make them less than attractive to politicians, city managers and neighbors.

Carlos Baia, deputy city manager for development of Concord, NH, suggests five prerequisites for developers seeking to create a successful project.

Baia’s advice to for-profit and nonprofit developers:

- Deploy your references. Local government wants to see that the organization has completed a successful project elsewhere.

- Do your homework. Understand how your project fits in with the community’s long-term planning and goals.

- Show how the project will benefit the community. As Baia put it, “you don’t want to have one building that kills everything else around.” Get the abutters on board and encourage them and business leaders to write letters to the editor.

- Develop relationships with the administrators of cities and towns. Elected officials often turn to staff for advice.

- Simplify. For complex deals, identify one key person who will shepherd the deal, stay on top of the details and communicate with officials.

- Have patience. “All the easy deals were done before 2008,” Baia said.

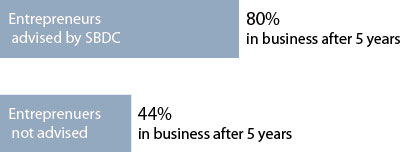

Which startups succeed?

SBDCs link small business to capital and help them get ready to access credit

Entrepreneurs who get advice from Small Business Development Centers have almost twice the five-year success rate of others (80% survive five years, compared to 44% of those who do not get advice).

Not bankable?

Credit enhancements for high visibility, high impact inner city sites in New Hampshire

- Capital Regional Development Council (CRDC) deploys credit enhancements from 5 different federal agencies.

- CRDC is certified by the Small Business Administration to provide 504 loans throughout New Hampshire.

- CRDC offers a variety of direct loan programs for growing NH companies.

- CRDC provides loans and grants to businesses, nonprofits and municipalities in Merrimack and Hillsborough counties to support clean-up of environmentally damaged sites that are suitable for redevelopment.

“Long term affordable money you can use”

FHLB Boston executive shows how member banks can use grants and loans

Kenneth Willis described three Federal Home Loan Bank (FHLB) programs provide grants and subsidized loans for affordable housing via member financial institutions.

- FHLB members receive a financial return on their investment and meet the credit needs in their communities

- Investments in the community have an economic ripple effect that benefits everyone.

- Every $1 million of FHLBB funding supports an additional $14 million in the project, with $26.6 million in additional economic impact. (Graphic shows results over 5 years.)

Community Development Financial Instiutions (CDFIs) are eligible to join the FHLB.

Hitting hot buttons of downtown rebirth

Getting to yes on affordable housing

Rosemary Heard of CATCH Neighborhood Housing says multiple sources of funding came together to support Menino Place because the project works on many levels: downtown revitalization, support for artists, green construction, job creation.

Mennino Place tapped in to broad community support because “it hits many hot buttons of downtown revitalization” according to the developer, CATCH Neighborhood Housing.

Those hot buttons, per CATCH’s Rosemary Heard:

- Preference for income qualified artists

- Green, gold LEED certified construction

- Housing in a walkable community

- One- and two-bedroom apartments for people at 50% and 60% of area median income

Credit enhancements save 50 jobs in NH

How credit enhancements kept 50 jobs in New Hampshire

Jack Donovan of the New Hampshire Business Finance Authority tells how the extra financing closed a gap when the factory’s appraised value fell short, saving 50 jobs for New Hampshire.

The back story: 2 employees use their retirement money to purchase a manufacturing company that must relocate.

The shortfall: To purchase, rehab and expand in a new location exceeds the building’s appraised value.

The solution: 3 additional sources of public funding—a city revolving loan fund, a local development corporation, the NH Business Finance Authority—come together to close the gap, save 50 jobs for New Hampshire and lay the foundation for success in a modern, efficient facility.

The takeaway: To help your clients, learn about all the economic development financing that is available.

Manufacturer Relocation/ Expansion

| Sources | |

| Bank | $1,026,000 |

| SBA 504 | 718,200 |

| Owner Equity | 307,800 |

| $2,052,000 | |

| Uses | |

| Purchase existing Building | $325,000 |

| Addition | 946,500 |

| Electrical/Mechanical | 330,000 |

| Renovation | 450,000 |

| $2,052,000 |

* Existing business is purchased but must be relocated

* Buy existing 15,000 sq.ft. building and add 18,300 sq.ft.

* Shortfall: Completed building appraised value of $1,400,000

Revised Sources and Uses

| Sources | |

| Bank | $1,026,000 |

| SBA 504 | 718,200 |

| City RLF | 70,000 |

| Local Dev. Corp. | 250,000 |

| BFA – SSBCI Collateral Shortfall | 250,000 |

| Owner Equity | 292,000 |

| $2,052,000 | |

| Uses | |

| Purchase existing Bldg | $352,000 |

| Addition | 946,500 |

| Electrical/Mechanical | 330,000 |

| Renovation | 450,000 |

| $2,052,000 |

* 50 jobs saved

* Manufacturer relocated to new, more efficient facility

Slides

Affordable Housing: Getting to Yes

- Rosemary Heard

CATCH Neighborhood Housing - Kathy Bogle Shields

NH Community Development Finance Authority - Carlos Baia

City of Concord - Christopher Miller

NH Housing Finance Authority - Craig Welch

NH Community Loan Fund - Glen Ohlund

TD Bank

Small Business: The Collaborative Path to the Deal

- Mary Collins

NH Small Business Development Center - Hollis McGuire

NH Small Business Development Center - Stephen Heavener

Capital Regional Development Council - Ed Caron

Merrimack County Savings Bank - Lou Guevin

Laconia Savings Bank - Jack Donovan

NH Business Finance Authority

Keynote

- Kenneth Willis

Federal Home Loan Bank of Boston

Presenting organizations

New Hampshire organizations share local knowledge

The Capital Regional Development Councilprovides real estate development and creative financing resources for small businesses including SBA 504 loans, Brownfields loans and grants, CDBG loans and grants, NH state tax credit project financing applications, direct loans and new markets tax credit project packaging throughout New Hampshire.CATCH Neighborhood Housing creates opportunities for affordable, quality housing for people otherwise not being served in Merrimack County, NH.

Concord is New Hampshire’s capital city, population 43,000. Its community development department aims to improve the quality of life for the taxpayers of Concord by preserving existing jobs, tax base, and the unique character of the city.

Federal Home Loan Bank provides wholesale funding for member banks to make community development loans and offers technical assistance to nonprofits.

Laconia Savings Bank, a SBA Express and SBA Preferred Lender, makes loans for purchasing, refinancing or expanding commercial real estate; purchasing or refinancing personal property; meeting short-term, seasonal or other work capital requirements; or acquiring or expanding an existing business.

Merrimack County Savings Bank, a Small Business Administration (SBA) Preferred, SBAExpress and Patriot Express lender, makes loans up to $4 million, including offer commercial mortgages, lines of credit, equipment and machinery loans, construction loans.

New Hampshire Business Finance Authority works with banking, business and economic development sectors to expand the availability of credit in the state and provides credit enhancement and bond financing.

New Hampshire Community Development Finance Authority supports affordable housing and economic development activities that benefit low and moderate income citizens in New Hampshire. CDFA administers nearly $40 million in funding resources.

New Hampshire Community Loan Fund, a community development financial institution, provides loans, capital and technical assistance to enable traditionally underserved people to participate more fully in New Hampshire’s economy.

New Hampshire Housing Finance Authority, a self-supporting public benefit corporation, administers programs to assist low- and moderate-income persons and families to obtain decent, safe and affordable housing.

New Hampshire Small Business Development Center offers one-on-one management advising and educational program for all sectors, from individuals seeking to start or acquire a business to established companies including innovative technology and manufacturing firms.

TD Bank is one of the 10 largest banks in the U.S., providing more than 7.8 million customers with a full range of retail, small business and commercial banking products and services at more than 1,280 convenient locations throughout the Northeast, Mid-Atlantic, Metro D.C., the Carolinas and Florida.

Sponsors

During 2011-12, the Federal Reserve Bank of Boston is organizing meetings about business opportunities in community development lending throughout New England as part of its commitment to promoting sound growth and economic development in the region.