Is Small Business Lending Valuable to Banks?

New evidence suggests that small business lending is a profitable market niche for small and possibly midsize publicly traded banking organiza tions in the United States.

{kind=link}

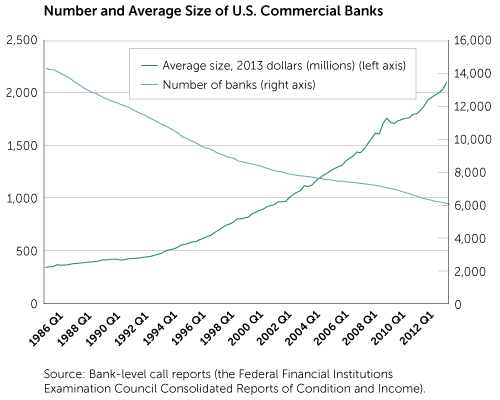

The consolidation of individual U.S. bank charters has resulted in both a shrinkage in the number of banks and an increase in their average size. (See "Number and Average Size of U.S. Commercial Banks." ) A well-known concern is the effect on the availability of credit to small and midsize enterprises (SMEs) that, being too small to efficiently access national credit markets directly, rely on financial intermediaries, especially banks. A less well-known concern is the potential adverse effect on the shareholders of the surviving banking organization.

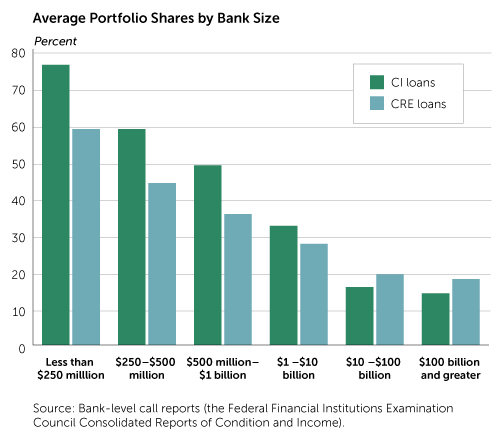

Given the inverse relationship between bank size and the portfolio share of small business loans, the ongoing consolidation in the banking industry will tend to shrink the share of small business loans in the portfolio of surviving entities. (See "Average Portfolio Shares by Bank Size." ) But in addition to possibly impairing credit availability to SMEs, consolidation may destroy value for shareholders because the relationship-lending expertise of the smaller banks may be deemphasized.

Benefits of Relationship Lending

Much of the literature on relationship lending focuses on the fact that smaller companies are opaque compared with large businesses that provide information in public filings and are often covered by securities analysts.

Small businesses may have little or no collateral and, in many cases, may be too young to have sufficient history from which to extrapolate future performance. Because of their size and the absence of substantial public information about their quality, such companies have virtually no access to funds from commercial paper, bonds, publicly traded equity, and the like. They tend to be dependent on banks. However, since banks are not well informed about the companies' credit risk, they must take the time to acquire and process information, and subsequently monitor the enterprises' activities.

Previous studies have established that long-term lending relationships between banks and businesses are valuable to small firms in terms of increased credit availability and protection against adverse credit shocks.[1] Relationship lenders, in turn, may extract benefits for themselves, not only covering the additional costs associated with establishing and maintaining the relationships, but adding value in three ways.

First, relationship lending, unlike transactional lending, lets a bank make use of the private information it acquires.[2] Second, it can give the bank opportunities to cross-sell products such as core deposit services and investment-banking services to its relationship borrowers. Finally, it can provide future business opportunities as the companies expand in size and scope.

A relationship bank has an opportunity to gain benefits from the businesses just by knowing more about them and exploiting the proprietary (and superior) information acquired through repeated interactions. The business has an incentive to remain with the relationship bank because, although the bank may charge an interest rate that is higher than justified by the level of credit risk, the rate will be lower than the interest rate that less well-informed lenders would charge.

In contrast, other bank lending is usually transactional in nature. Many banks lend to small businesses using credit-scoring models rather than private, qualitative information. Credit scoring applies statistical methods to quantifiable data, summarizing borrower characteristics to produce a score that can be used to evaluate the likelihood of repayment. Other transactions-based lending technologies, such as fixed-asset lending, are also unlikely to benefit from bank-firm relationships.

The costly information-collection and processing activities required for relationship lending partly offset the benefits. Given the expense associated with screening and monitoring small, opaque companies, the money earned by a relationship bank could simply be compensation for its information-gathering efforts and not represent a gain. However, it is also possible that what is earned from the bank's informational power will actually add value.[3] And the data do suggest that small business lending, at least by smaller banks, is value enhancing to the banks.

The increased competition among lenders in recent years of bank consolidation and technological advances, including the increased use of credit-scoring models, may be reducing the profitability of relationship lending. In fact, a number of studies have documented a rise in the use of credit scoring for small business lending even among small and midsize banks. Still, it can be argued that a focus on relationship lending by well-managed community banks remains an economically viable strategy.[4]

New Evidence

A recent Federal Reserve Bank of Boston working paper uses data from the small business loan survey contained in the June bank-level call reports(the Federal Financial Institutions Examination Council Consolidated Reports of Condition and Income) to estimate the relationship between the book value and market value of banks' small business loan portfolios.[5] The key hypothesis tested in the study is that relationship lending in the form of small business loans held by banking organizations is value enhancing to banks, both in absolute terms and relative to the large loans held by the same banking organizations. Because the analysis is based on market values, the sample is limited to publicly traded U.S. banking organizations.

To capture the effect of bank-firm relationships on bank value, the researchers focused on commercial and industrial loans (CI) to U.S. addresses in domestic offices and commercial real estate loans (CRE) secured by nonfarm, nonresidential properties in domestic offices. The Small Business Lending Survey provides information on loans with original balances of $1 million or less, further disaggregated into less than or equal to $100,000, $100,000 through $250,000, and $250,000 through $1 million. Unfortunately, the survey is based on loan size rather than company size and does not completely capture loans to small businesses.

The researchers found that small CI loans do add market value to small and midsize banking organizations. This suggests that at least for those banks, the added revenue associated with relationship lending exceeds the added costs of evaluating and monitoring small business loans. The estimated effect may also include the value emanating from the opportunity to profit from other lines of business with the borrowers. Furthermore, the value-enhancing effect for the smallest banks appears to arise primarily from the smallest size category of CI loans-those with original amounts of $100,000 or less. Such loans likely represent the loans made to small, opaque firms, which give banks the most ability to leverage the power of better information.

In contrast, small CRE loans do not appear to enhance the market value of banking organizations beyond that from CRE loans generally, even for the smallest banks. One explanation is that CRE loans represent transactional rather than relationship lending and, being based on collateral rather than superior private information about borrowers, make the advantages arising from information-intensive relationship lending less important.

§

The new evidence suggests that small business lending is a profitable market niche for small and possibly midsize publicly traded banking organizations in the United States. The evidence is consistent with the banks having a comparative advantage in originating and monitoring small business loans, compared with larger banking organizations. Consequently, consolidation of the banking industry-insofar as it takes the form of the acquisition of smaller banking organizations by larger banking organizations that are less focused on small business lending-may be value destroying and thus not in the interests of the shareholders of the acquiring banking organizations.

Joe Peek is a vice president and head of the financial group in the research department at the Federal Reserve Bank of Boston. Contact him at Joe.Peek@bos.frb.org.

Acknowledgments

The author wishes to acknowledge the excellent research support of Peggy Gilligan and Hannah Shaffer.

Endnotes

- See, for example, M. Petersen and R. Rajan, "The Benefits of Firm-Credit Relationships: Evidence from Small Business Data," Journal of Finance 49, no. 1 (1994); A.N. Berger and G.F. Udell, "Relationship Lending and Lines of Credit in Small Firm Finance," Journal of Business 68 (1995); and R.A. Cole, "The Importance of Relationships to the Availability of Credit," Journal of Banking and Finance 22 (1998).

- See, for example, S. Sharpe, "Asymmetric Information, Bank Lending, and Implicit Contracts," Journal of Finance 45, no. 4 (1990); R. Rajan, "Insiders and Outsiders: The Choice between Informed and Arm's Length Debt," Journal of Finance 47 (1992); and J.C. Stein, "Information Production and Capital Allocation: Decentralized versus Hierarchical Firms," Journal of Finance 57, no. 5 (October 2002).

- D.A. Carter, J.E. McNulty, and J.A. Verbrugge, "Do Small Banks Have an Advantage in Lending? An Examination of Risk-Adjusted Yields on Business Loans at Large and Small Banks," Journal of Financial Services Research 25 (April-June 2004).

- R. DeYoung, W.C. Hunter, and G.F. Udell, "The Past, Present, and Probable Future of Community Banks," Journal of Financial Services Research 25 (April-June 2004).

- D. Holod and J. Peek, "The Value to Banks of Small Business Lending" (Federal Reserve Bank of Boston Working Paper No. 13-7, 2013).

Articles may be reprinted if Communities & Banking and the author are credited and the following disclaimer is used: "The views expressed are not necessarily those of the Federal Reserve Bank of Boston or the Federal Reserve System. Information about organizations and upcoming events is strictly informational and not an endorsement."

About the Authors

About the Authors

Joe Peek,

Federal Reserve Bank of Boston

Email: Joe.Peek@bos.frb.org

Resources

Related Content

Bank Consolidation and Small Business Lending: It's Not Just Bank Size That Matters

The Value to Banks of Small Business Lending

Banks and the Availability of Small Business Loans

Small Business Credit Availability: How Important is Size of Lender?