2014 Series • No. 2014–7

Current Policy Perspectives

Student Loan Debt and Economic Outcomes

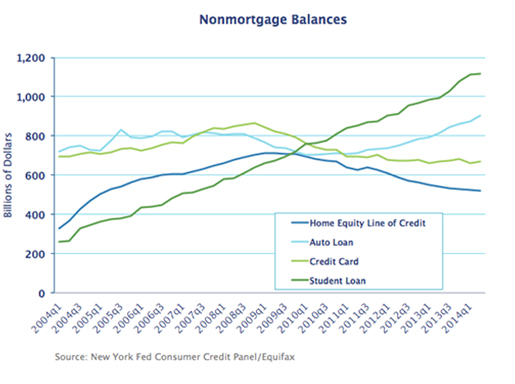

This policy brief examines the impact of student loan debt on individuals' homeownership status and wealth accumulation, employing a rich set of financial and demographic variables that are not available in many of the existing studies that use credit bureau data. It is important to understand whether and, if so, how student loan debt affects households' economic decisions because student loan debt has now surpassed credit card debt to become the second largest amount of household debt outstanding after mortgage debt.

Key Findings

Key Findings

- Overall, student loan debt lowers the likelihood of homeownership by age 30 or so for a group of individuals who attended college during the 1990s.

- There is a fairly strong negative correlation between student loan debt and wealth (especially if it is net of student loan debt) for a group of households with at least some college experience and the household head or spouse is 40 years old or younger.

- The negative effect of student loan debt on wealth holdings is more pronounced among homeowners than among renters.

Exhibits

Implications

Household balance sheet data suggest that the lower wealth accumulation among homeowners with outstanding student loan debt is likely due to greater expenses for these households rather than to lower income. However, we cannot yet conclude that student debt causes lower homeownership rates and wealth for relatively young households. A more structural approach and better data are needed to assess whether there is a causal link. More broadly, additional research is needed to better understand why student loan liabilities are associated with worse economic outcomes for individuals and households.

Abstract

This policy brief advances the growing literature on how student loan debt affects individuals' other economic decisions. Specifically, it examines the impact of student loan liabilities on individuals' homeownership status and wealth accumulation. The analysis employs a rich set of financial and demographic control variables that are not available in many of the existing studies that use credit bureau data. Overall, student debt lowers the likelihood of homeownership for a group of students who attended college during the 1990s. There is also a fairly strong negative correlation between student loan debt and wealth (excluding student loan debt) for a group of households with at least some college experience.