2015 Series • No. 15–4

Research Department Working Papers

The Failure of Supervisory Stress Testing: Fannie Mae, Freddie Mac, and OFHEO

In the aftermath of the global financial crisis, policymakers in the United States and elsewhere have adopted stress testing as a central tool for supervising large, complex, financial institutions and promoting financial stability. Although supervisory stress testing may confer substantial benefits, such tests are vulnerable to model risk. This paper studies the risk-based capital stress test conducted by the Office of Federal Housing Enterprise Oversight (OFHEO) for Fannie Mae and Freddie Mac, the two government-sponsored enterprises (GSEs) that are central to the U.S. housing finance system. This research aims to identify the sources of the stress test's spectacular failure to detect the growing risk and ultimate financial distress at these GSEs as mortgage market conditions deteriorated in 2007 and 2008. The analysis focuses on a key element of OFHEO's stress test, the models used to predict default and prepayment of 30-year fixed-rate mortgages.

Key Findings

Key Findings

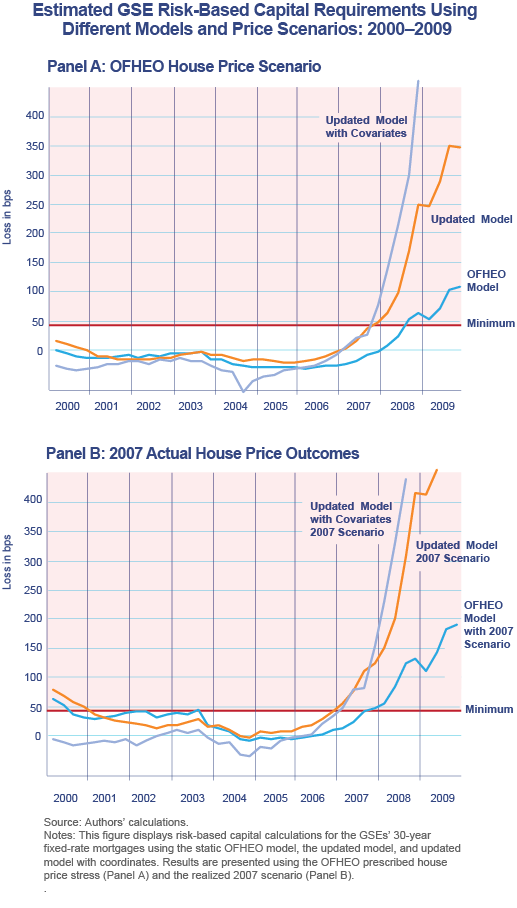

- One major problem is that the supervisor never re-estimated the model and hence left the parameters static for almost a decade. Also, certain new variables that were increasingly being used in modeling mortgage underwriting were omitted, negatively affecting model performance.

- The second major problem is that the house price stress scenario was insufficiently dire.

- The third major problem is that while the stress test was supposed to look 10 years into the future, it ignored the effect of future loans on future losses.

Exhibits

Implications

The results of this research imply that real efforts should be taken to mitigate model risk through continual development and model validation. With an improved model and a more adverse house price scenario, the stress test would have predicted that the GSEs were undercapitalized almost two years before the conservatorships took place. This could have forced OFHEO to face some unpalatable choices that could have worsened the financial crisis. But the highly nonlinear pattern of risk-based capital implies that the GSEs could have survived the housing bust had it taken place two years earlier—because the GSEs had enough capital to absorb 10 years' of losses on the loans outstanding in 2006. But more than half the GSE mortgages that defaulted in 2008 were made in 2006 and 2007. Since these loans were made at the peak of the bubble, their subsequent defaults generated much larger losses than those of earlier vintages. An obvious implication is that new loans originated when house prices are falling will underestimate the risk faced by the institutions. However, allowing for new business requires critical assumptions about the size, composition, and risk characteristics of the new loans. Indeed, the General Accounting Office concluded in 2002 that OFHEO should not incorporate new business assumptions into their stress test, because doing so is inherently speculative and would introduce additional complexity. The authors believe that understanding how to treat new business warrants future research attention, given the important role that stress testing has assumed in macro-prudential supervision, and that the highly nonlinear path of estimated credit losses, with its implication for required capital charges, is inherently problematic.

Abstract

Stress testing has recently become a critical risk management and capital planning tool for large financial institutions and their supervisors around the world. However, the one prior U.S. experience tying stress test results to capital requirements was a spectacular failure: The office of Federal Housing Enterprise Oversight's (OFHEO's) risk-based capital stress test for Fannie Mae and Freddie Mac. We study a key component of OFHEO's model—the performance of 30-year fixed-rate mortgages—and find two key problems. First, OFHEO left the model specification and associated parameters static for the entire time the rule was in force. Second, the house prices stress scenario was insufficiently dire. We show how each problem resulted in a significant underprediction of mortgage credit losses and associated capital needs at Fannie Mae and Freddie Mac during the housing bust.