Mapping New England

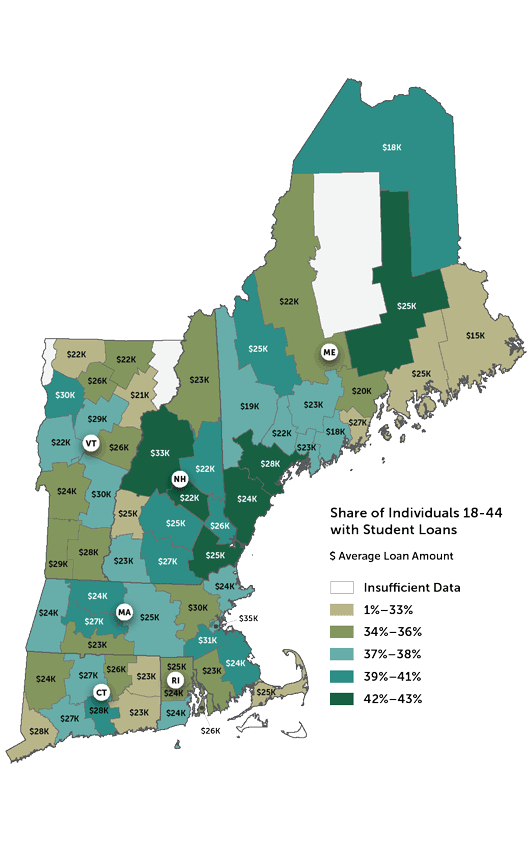

Individuals just entering adulthood make one of the biggest financial decisions of their lives-how much to borrow for postsecondary education. In New England, almost one in five residents is now saddled with a student loan that, on average, surpasses $26,000.[1] Nationwide, that adds up. In 2013, U.S. student loan debt totaled $1.08 trillion, and many debtors were struggling to repay.[2] Over 11 percent were more than 90 days overdue, a higher rate than for any other form of credit.

Using fourth-quarter 2014 data from the Federal Reserve Bank of New York's consumer credit panel (FRBNY CCP), we examine student loan conditions in New England, focusing on the population with a disproportionate share of student loans, individuals aged 18 to 44.[3]

Cumberland and Penobscot counties in Maine have the highest share of individuals with student loans. (Penobscot County hosts the University of Maine, and Portland, in Cumberland, is home to several higher-education institutions and a relatively young population.) The next-highest counties are Rockingham in New Hampshire, Bristol in Rhode Island, and York in Maine. Of those individuals aged 18 to 44 with credit scores, at least 40 percent in the top five counties have student loans.

The county averages range from under $20,000 in the bottom counties ($14,770 in Washington County, Maine) to over $30,000 in the top five. Suffolk County, Massachusetts, tops the list at an average of almost $35,000, followed by Grafton County, New Hampshire, Norfolk County, Massachusetts, and Windsor and Chittenden counties in Vermont.[4]

Endnotes

- Average loan amounts exclude individuals with no reported student loans.

- See http://www.newyorkfed.org/householdcredit/2013-Q4/HHDC_2013Q4.pdf.

- See Donghoon Lee and Wilbert van der Klaauw, "An Introduction to the FRBNY Consumer Credit Panel" (Staff Report No. 479, Federal Reserve Bank of New York, 2010), http://www.newyorkfed.org/research/staff_reports/sr479.html. As our estimates are derived from individuals who have had some contact with the formal credit market, the data ranges may slightly overestimate the proportion of individuals per county with a loan. Some individuals aged 18 to 44 will have no contact with the formal credit market. However, the average loan amounts would not be overestimated since student credit is part of the traditional credit market. Counties with fewer than an estimated 2,000 individuals with student loans were excluded.

- The map does not consider the relative ability to repay loans in different counties.

Articles may be reprinted if Communities , Banking and the author are credited and the following disclaimer is used: "The views expressed are not necessarily those of the Federal Reserve Bank of Boston or the Federal Reserve System. Information about organizations and upcoming events is strictly informational and not an endorsement."

About the Authors

About the Authors

Kaili Mauricio

Resources

Related Content

Mapping New England: Distance to Closest SNAP (Food Stamp) Outlet

Mapping New England: People Living in Lower-Income Areas, by County

Mapping New England: Income Distribution by County

Mapping New England: Coronary Heart Disease Death Rates