Survey: Black small business owners’ credit concerns didn’t fade during pandemic

Fed expert says survey points to need for different lending options – like FinTech lenders

FG Trade/Getty Images

{kind=link}

The Federal Reserve’s annual credit survey of small business owners always seems full of compelling data and stats to Brian Clarke, a business strategy manager at the Federal Reserve Bank of Boston. But this year had added interest.

The Small Business Credit Survey results were released this spring, but the survey itself was taken between September and October 2020, smack in the middle of the pandemic. So, it offered a glimpse of the responses of business owners to the worst crisis any of them will hopefully ever face. And Clarke was struck with one finding in particular:

About half of all Black business owners who responded (48%) said “credit availability” was a challenge they expected to face through the end of 2021. That’s 8 percentage points more than the next closest racial group (Hispanics) and 18 percentage points higher than white business owners.

“I remember flagging that right away,” Clarke said. “This was a time when customers are disappearing, and that’s what other business owners are worried about. But you have one demographic that’s outside of that, that’s saying, ‘I’m still just as worried about access to credit.’”

Longstanding Black concerns about access to credit showed in PPP uptake

Of course, concerns about a relative lack of access to credit among Black Americans long predate the survey and the pandemic because of the historical impact on the Black community.

Consider mortgage lending. Disparities in credit access there – both in the number of loans approved and in the cost of those loans – are often cited as a major contributor to the racial wealth gap.

That’s because home equity is by far the largest component of a family’s “stock of wealth,” said Sara Chaganti, a researcher in the Boston Fed’s Community and Regional Outreach department. And Chaganti added that research, including a landmark 1992 Boston Fed study and more recent work from the Chicago Fed, shows Black families have long been wrongly denied the chance to accumulate this type of wealth.

“Black Americans have been systemically excluded from home ownership by unjust practices and policies that still persist today,” Chaganti said. “That’s certainly affected their ability to trust financial institutions to be there when they need them.”

She added traditional banks have historically had a limited presence in communities of color, and Black families tend to pay higher fees and interest for the same financial products that white families get for less. As a result, Blacks looking for loans may not interact much with banks at all.

Clarke said this was a problem during the pandemic because traditional lenders were originally the main conduits of Paycheck Protection Program loans nationwide. These PPP loans – many of which were later forgiven – were a lifeline to many businesses and ended up serving 970,000 of them.

But when the PPP loans became available, Clarke said he and his colleagues focused on informing communities of color after they quickly realized that people without strong banking relationships might have trouble accessing the money. The survey results ended up confirming that concern. For instance:

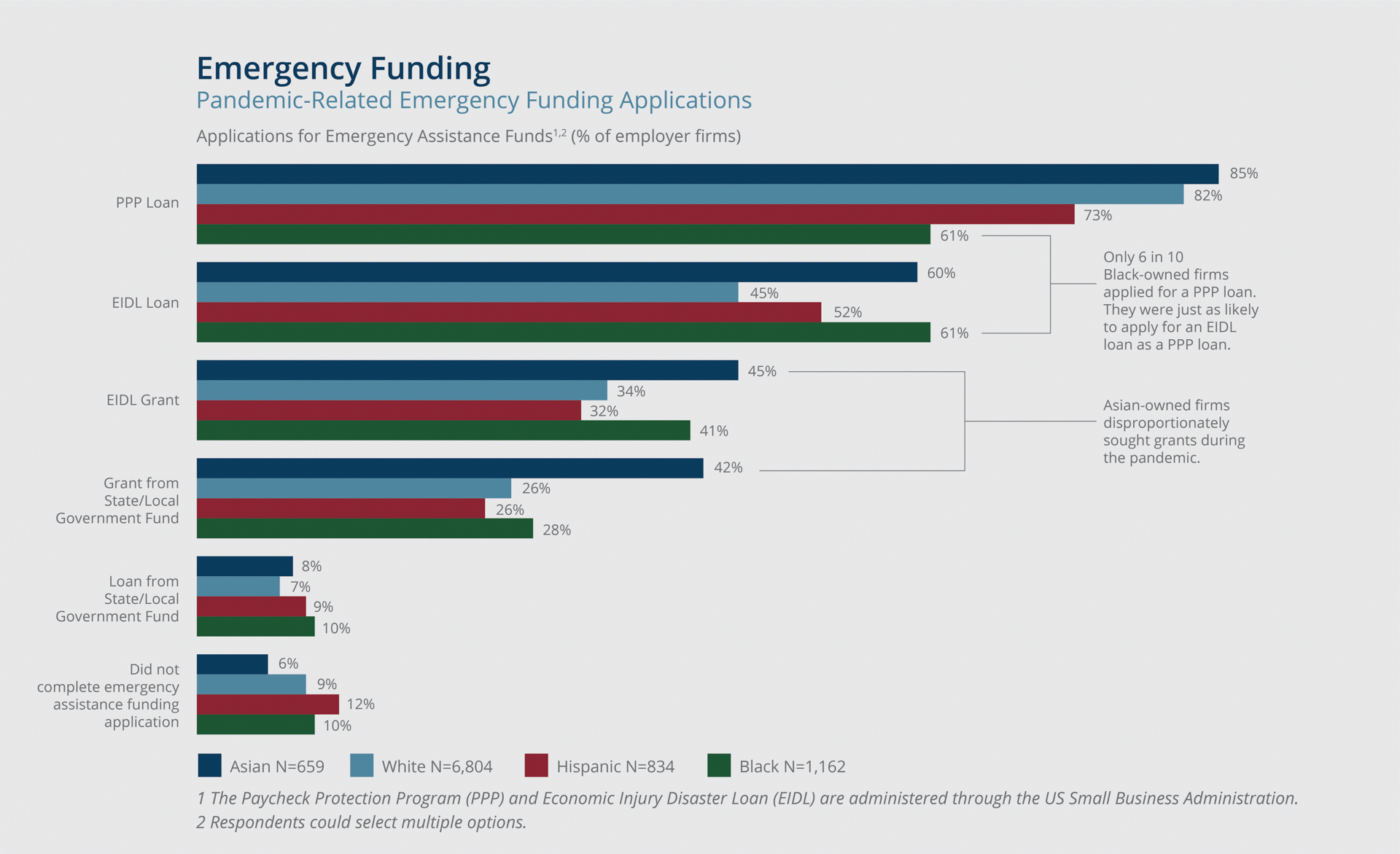

- Only 61% of Black-owned firms applied for a PPP loan. By comparison, 85% of Asian-owned firms applied, the largest share of any group.

- 1-in-5 Black-owned firms who did not apply for a PPP loan had never heard of the program, the most of any group.

{kind=link}

Small Business Credit Survey

To Clarke, the responses simply revealed the longstanding lack of communication, and sometimes lack of trust, between Black business owners and the financial services industry.

“I think it all points to structural and systemic issues that were exposed during the pandemic,” he said.

Clarke: FinTech lenders could offer some answers during next crisis

But the survey also indicated about 1 in 10 borrowers of all races use online lenders or FinTech companies as their financial services provider. Clarke said growth in this number could expand Black engagement with the financial services industry and generally increase lending options for small businesses.

FinTech stands for “financial technology,” and these companies either offer loans themselves or partner with a bank. These aren’t brick-and-mortar institutions, so there’s minimal overhead, and their virtual nature supports a greater agility and flexibility than a traditional bank, Clarke said. Perhaps the biggest difference is that they often use different data (known as “alternative data”) to determine creditworthiness – maybe rent payment history, cash flow data from a small business, or even if you pay your Netflix subscription every month, he said.

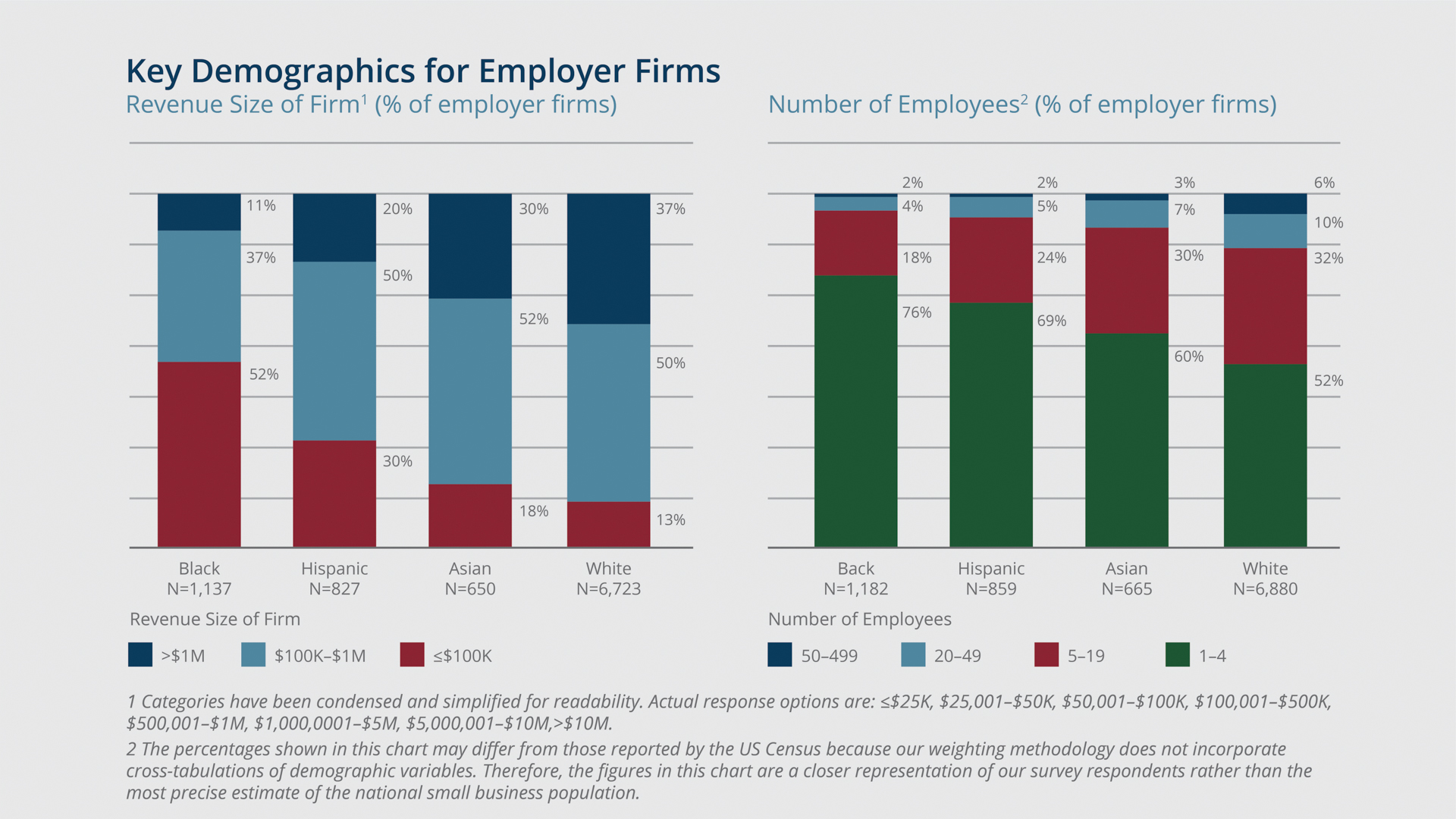

By using different data, FinTech lenders might, for instance, work with firms that otherwise don’t have enough revenues to get a business loan at a bank, he said. That matters among Black small business owners, because 52% of Black survey respondents said they operated on $100,000 or less in annual revenue, the highest percentage of any racial group (Hispanics were next at 30%).

{kind=link}

Small Business Credit Survey

Clarke said that more transparency from FinTech lenders is critical – otherwise, the formulas and alternative data used to determine creditworthiness could be used to support predatory lending schemes. But he added if it’s done right, a greater proliferation of these new kinds of lenders in the Black community may mean more access to credit for Black business owners, and less worry about credit during the next crisis.

“These FinTechs firms can go into different markets in ways a traditional bank can’t or won’t,” he said. “They move faster, they’re lending smaller amounts, and generally just make credit more available. It’s one of the most exciting things out there in this space.”

About the Authors

About the Authors

Jay Lindsay is a member of the communications team at the Federal Reserve Bank of Boston.

Email: jay.lindsay@bos.frb.org

Site Topics

Keywords

- Small Business ,

- credit availability ,

- credit ,

- credit constraints ,

- Black Americans