Statement of Eric S. Rosengren, Commenting on Dissenting Vote at the Meeting of the Federal Open Market Committee

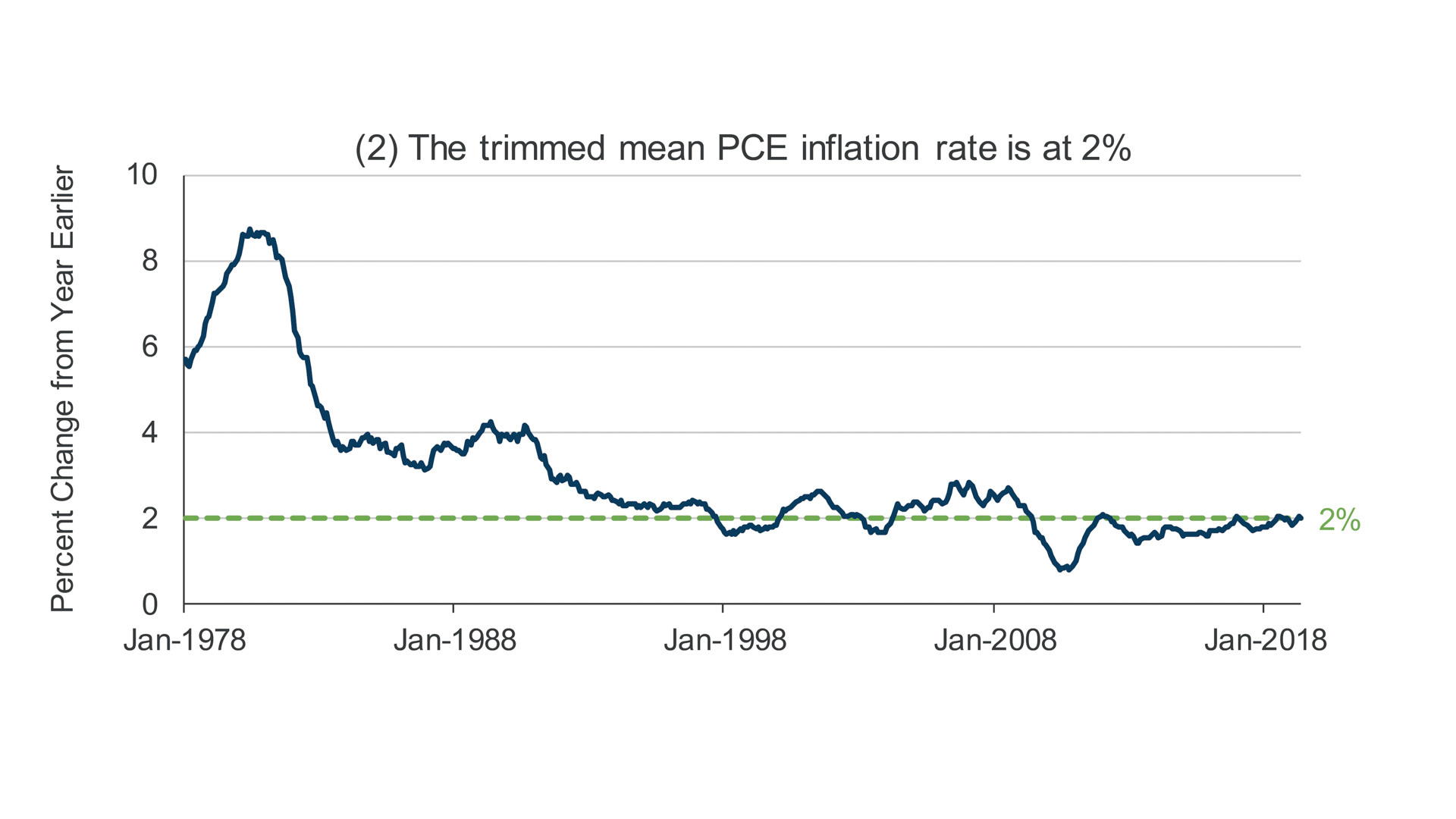

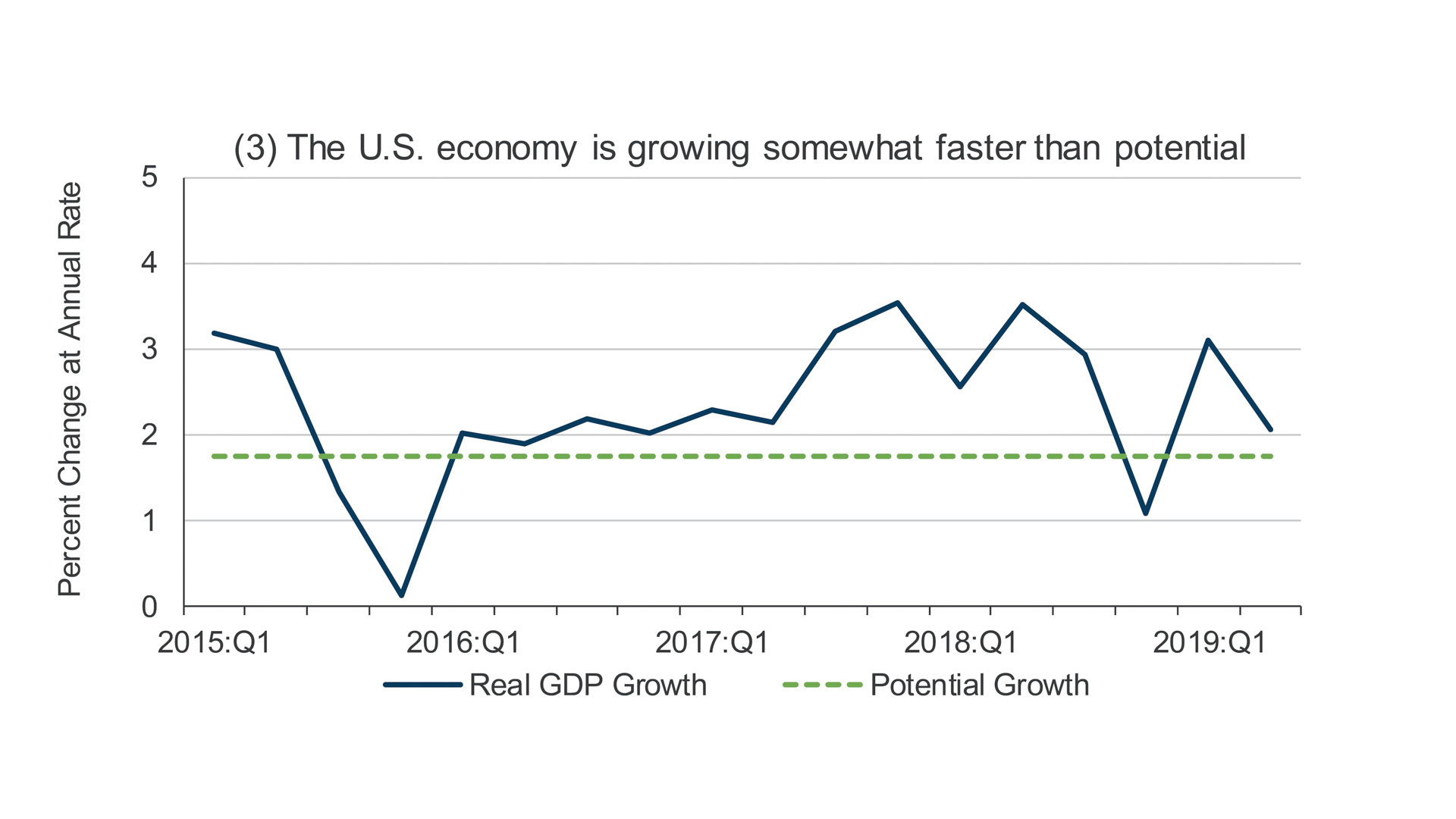

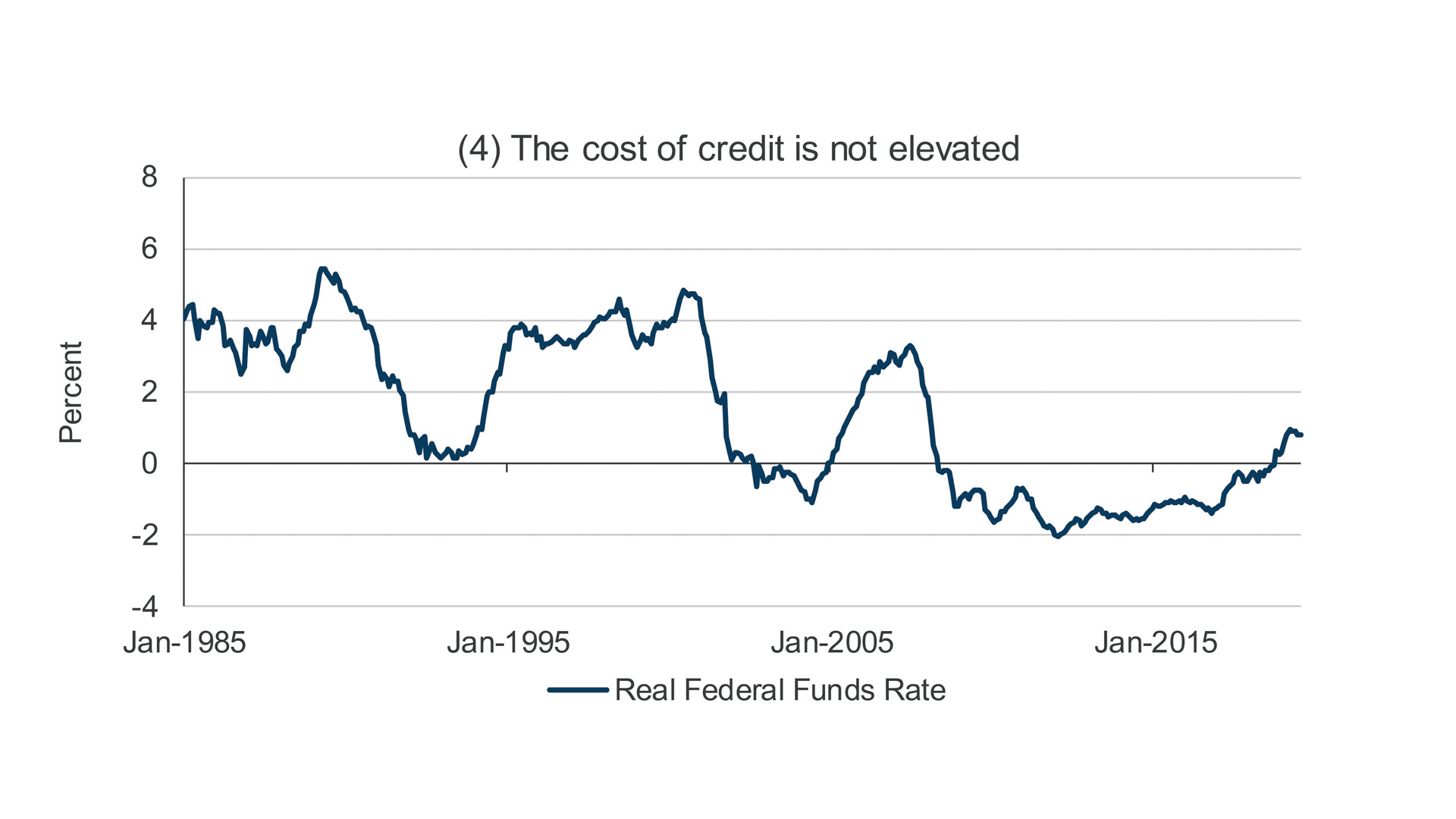

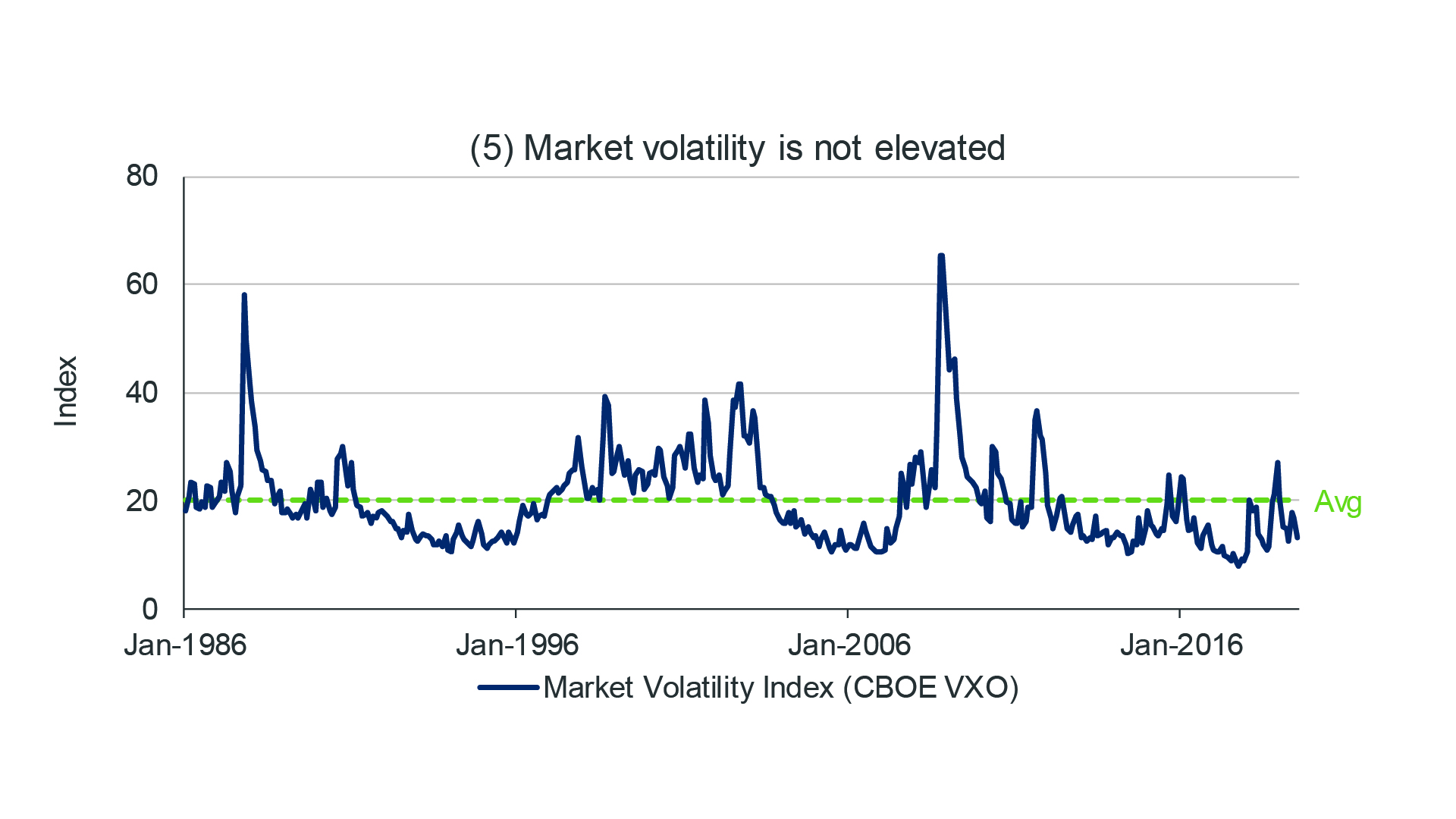

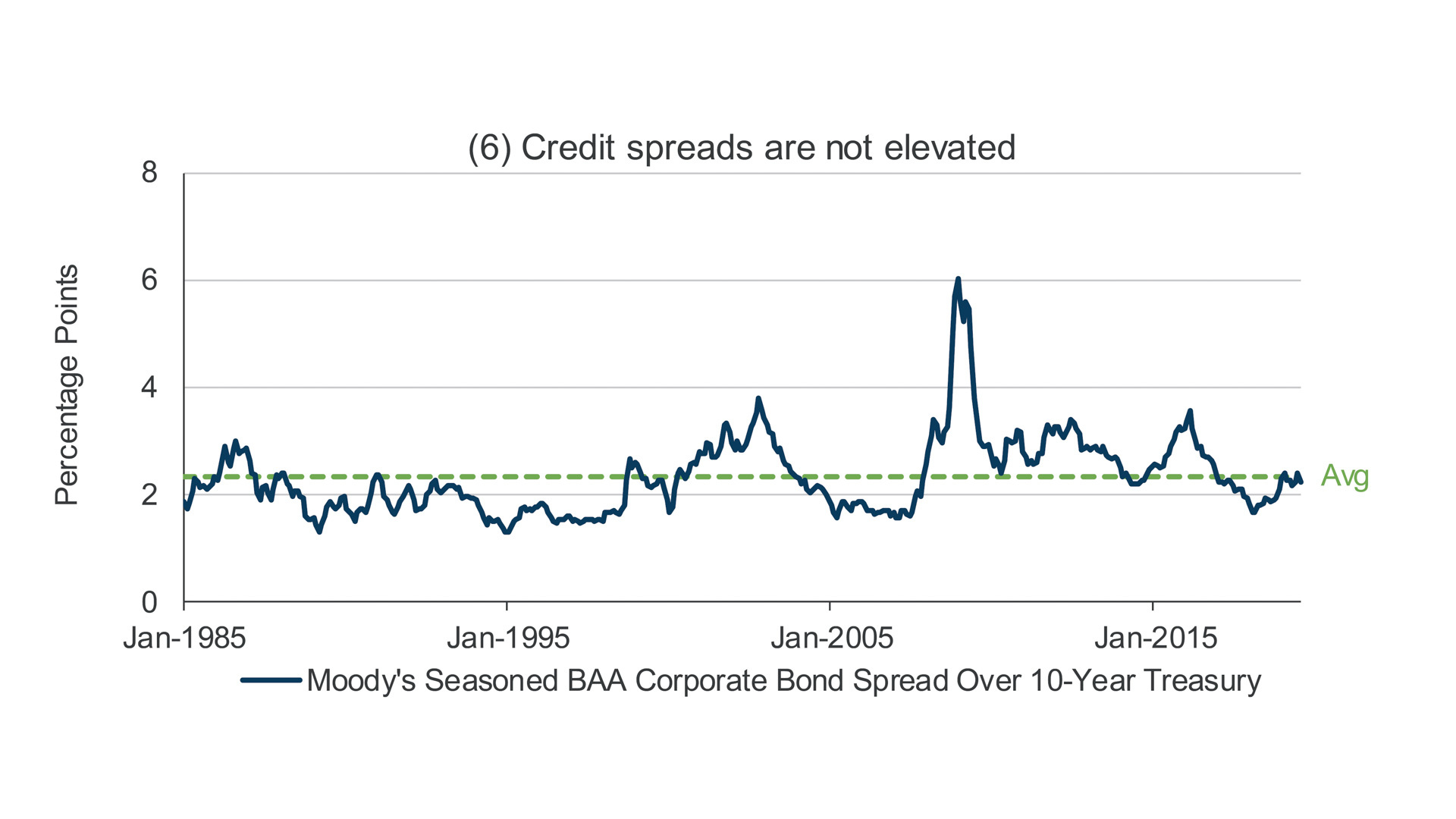

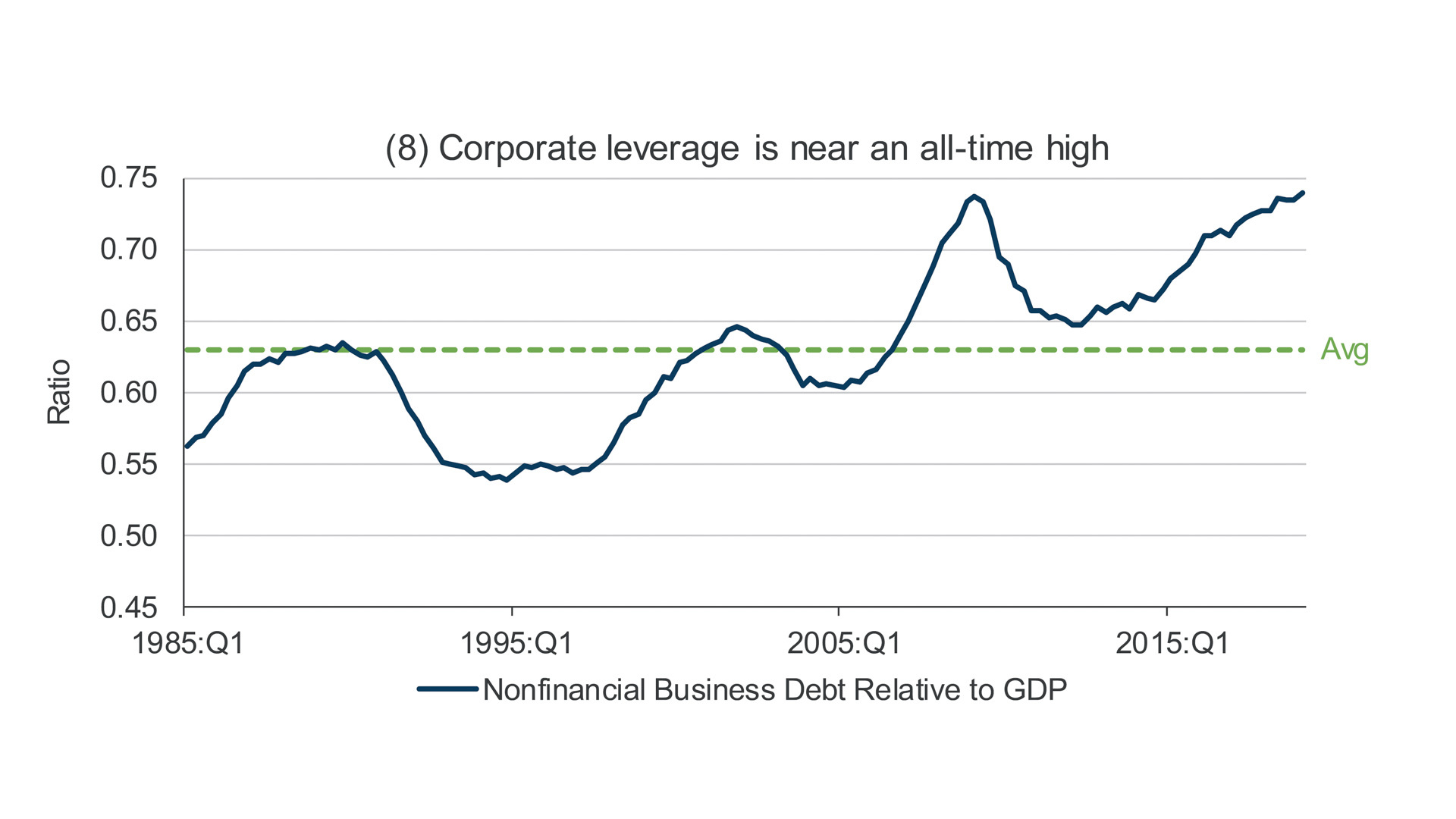

With the unemployment rate near 50-year lows and inflation likely to rise toward the 2 percent target, and with financial stability concerns being somewhat elevated given near-record equity prices and corporate leverage, I do not see a clear and compelling case for additional monetary accommodation at this time.

The following eight charts reflect the key data on which I base this view, with each chart’s title summarizing a key point:

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Note: The real federal funds rate is calculated as the federal funds rate minus core PCE. The June 2019 figure for core PCE is used as an estimate for July in calculating the real federal funds rate for July 2019.

Sources: (1) BLS, (2) Federal Reserve Bank of Dallas, (3) BEA, Federal Reserve Bank of Boston – estimate of potential, (4) BEA, Federal Reserve Board, (5) CBOE, (6) Federal Reserve Board, Moody’s, (7) S&P, (8) BEA, Federal Reserve Board, (1-8) Haver Analytics

Resources

Resources

Keywords

- Dissent Statement