The Scratch Ticket and the Numbers Game: Who Plays Which and Why?

BanksPhotos/iStock

Research in Maine shows that draw lotteries and instant-play lotteries attract different demographics, although they both affect the most economically vulnerable.

{kind=link}

Currently, 44 states offer consumers the opportunity to play the lottery.1 Lotteries are often touted as a simple way to raise funds without increasing taxes. In the most recent economic downturn, some states—notably Maryland—made the lottery an integral part of their plans to avoid budget cuts. Because those who play the lottery do so voluntarily with the hope of obtaining a big payout, at first blush it is hard to point to obvious losers in this revenue-generating scheme. Even those who do not win can claim some form of cheap entertainment that perhaps justifies the expense.

Lotteries have grown significantly since their introduction in 1964 by New Hampshire.2 More than $70 billion was spent on lottery tickets and games in the United States in 2014,3 which averages out to around $300 per year per adult. However, the growing literature on what drives lottery play indicates that much of the impetus appears to be financial desperation on the part of participants rather than entertainment seeking.4

The Maine State Lottery was enacted in 1974 in a statewide referendum.5 Neighboring states had already adopted some type of lottery, and the thought in Maine was that if the state introduced its own, it could capture some of the revenue leaving the state.6 Lotteries are often sold to the public by connecting the revenue with sympathetic causes, such as education. This is not the case in Maine, however, where state lottery revenue becomes part of the general budget. In recent years interstate competition in lottery sales has become less of an issue as most states offer lotteries. This has led to the introduction of multistate lotteries with larger jackpots and wider publicity. Maine joined the multistate Powerball in 2004, the Hot Lotto in 2009, the Mega Millions in 2010, and the Lucky for Life in 2012. All of these are multijurisdictional jackpot games controlled by the Multi-State Lottery Association (MUSL).7 MUSL is a nonprofit, government benefit association that is owned and operated by its member lotteries.

{kind=link}

Rachel Bissett/Federal Reserve Bank of Boston

Not All Lotteries Are Equal

There are two main types of lottery games: draw and instant. Draw lotteries involve the purchase of a ticket possessing a set of numbers (either random or selected by the participant) that provide an opportunity to win huge jackpots reaching into the hundreds of millions of dollars. For example, in January 2016, the Powerball jackpot reached a whopping $1.6 billion. These jackpots are widely advertised; their size depends on the number of winners from prior rounds and their take. Game structure and jackpot size are two of the biggest factors affecting lotteries' profitability. Researchers argue that the jackpot size has a bigger impact on lottery sales than likely expected winnings, suggesting an irrational "lotto mania" behavior on the part of consumers. The above-mentioned Powerball game, with the highest jackpot to date as of this writing, had a winning probability of one in 292.2 million (the overall odds of winning a prize in a Powerball game are one in 24.878), yet had a record number of participants.9

Instant lotteries provide an opportunity for an immediate payout at the time of purchase: having purchased a ticket, customers scratch an obscuring coating off boxes on the card to reveal whether or not they have won anything (winning requires all the revealed boxes to match). Instant games tend to offer much smaller winnings, although on rare occasions players can win close to $2 million.10

Who Plays the Lottery and Why It Matters

People with low socioeconomic status are more likely to play the lottery than those who are better off. Lower-income households and individuals spend a larger share of their income on purchases of lottery tickets than do those with higher incomes.11 This by itself is not particularly damning if it merely indicates that lotteries are a cheap form of entertainment. However, this does not appear to be the case. Some have found that simply feeling poor increases the likelihood of purchasing lottery tickets, regardless of actual income level.12 Moreover, lottery ticket sales do not appear to substitute for attendance at movie theaters or other cheap forms of entertainment.13 Behavioral theories of financial risk taking suggest that individuals are more prone to take risks when they have experienced recent negative financial shocks. As they fall below their reference income level, they are more willing to risk further losses—for example, by playing the lottery—in order to return to their former status. One such negative wealth shock is loss of employment, which leaves an individual without a constant source of income. Therefore we might expect that as the unemployment rate goes up, lottery sales will too.

The Case of Maine

Using comprehensive store-level data on lottery ticket sales from the state of Maine, we can shed light on the relationship between financial shocks and lottery play. Our data include five years of observations from all sellers in the state of Maine. This includes total sales of lottery tickets, both draw sales and instant lottery sales. Notably, the five-year period covers 2010 through 2014, a period of recovery from a major recession. The analysis is conducted at the zip code level.

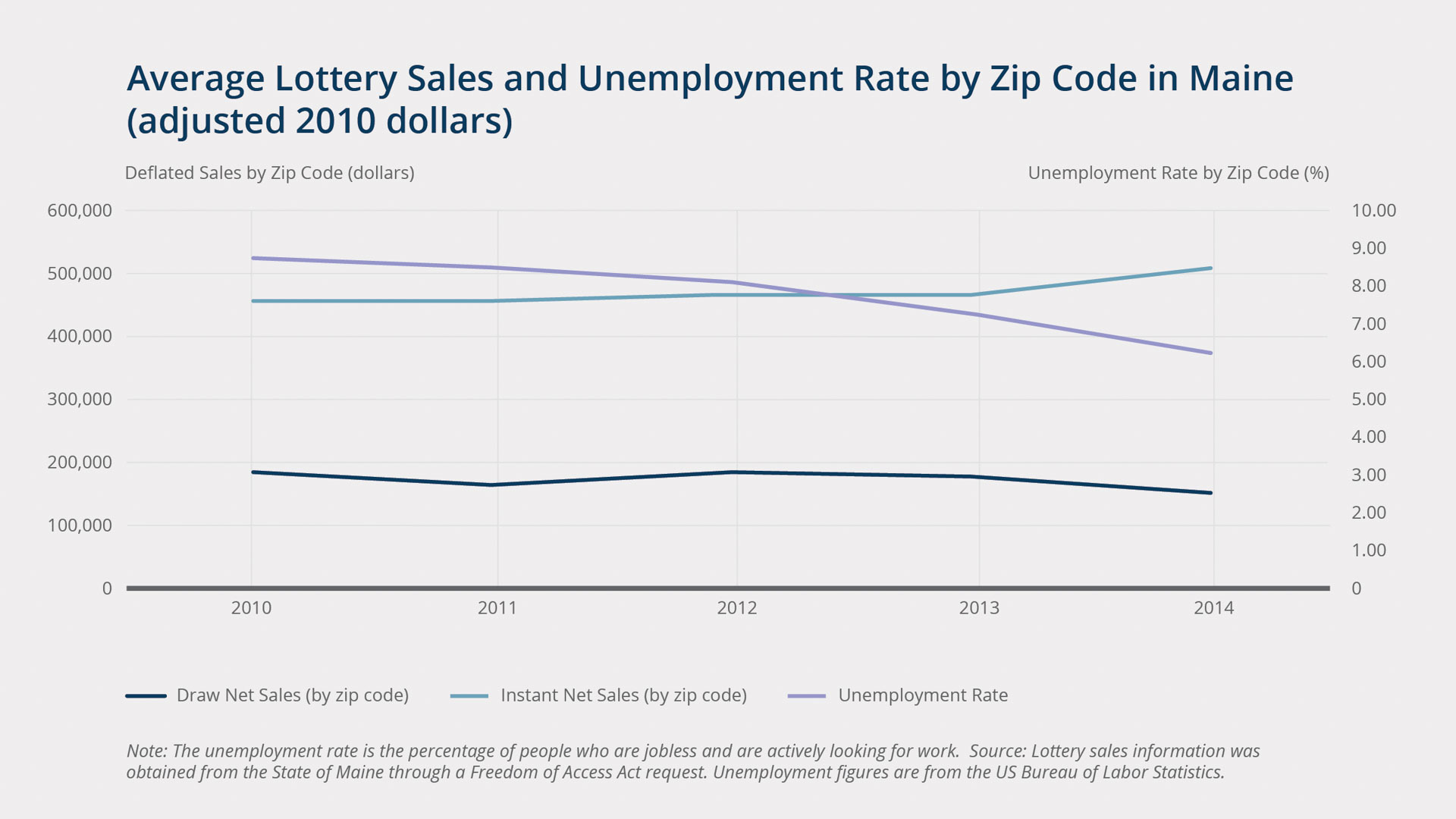

The analysis shows a large, positive, and significant relationship between unemployment rate and draw lottery sales. (See "Average Lottery Sales and Unemployment Rate by Zip Code in Maine.") A 1 percent increase in the unemployment rate tends to increase draw lottery sales in a zip code by 4.7 percent. There is no corresponding increase in instant lottery sales, suggesting that the recently unemployed are drawn to the larger jackpots of the draw game. When people become unemployed, lotteries seem to provide a risky opportunity to address the immediate problem. However, our analysis is somewhat more nuanced.

{kind=link}

Rachel Bissett/Federal Reserve Bank of Boston

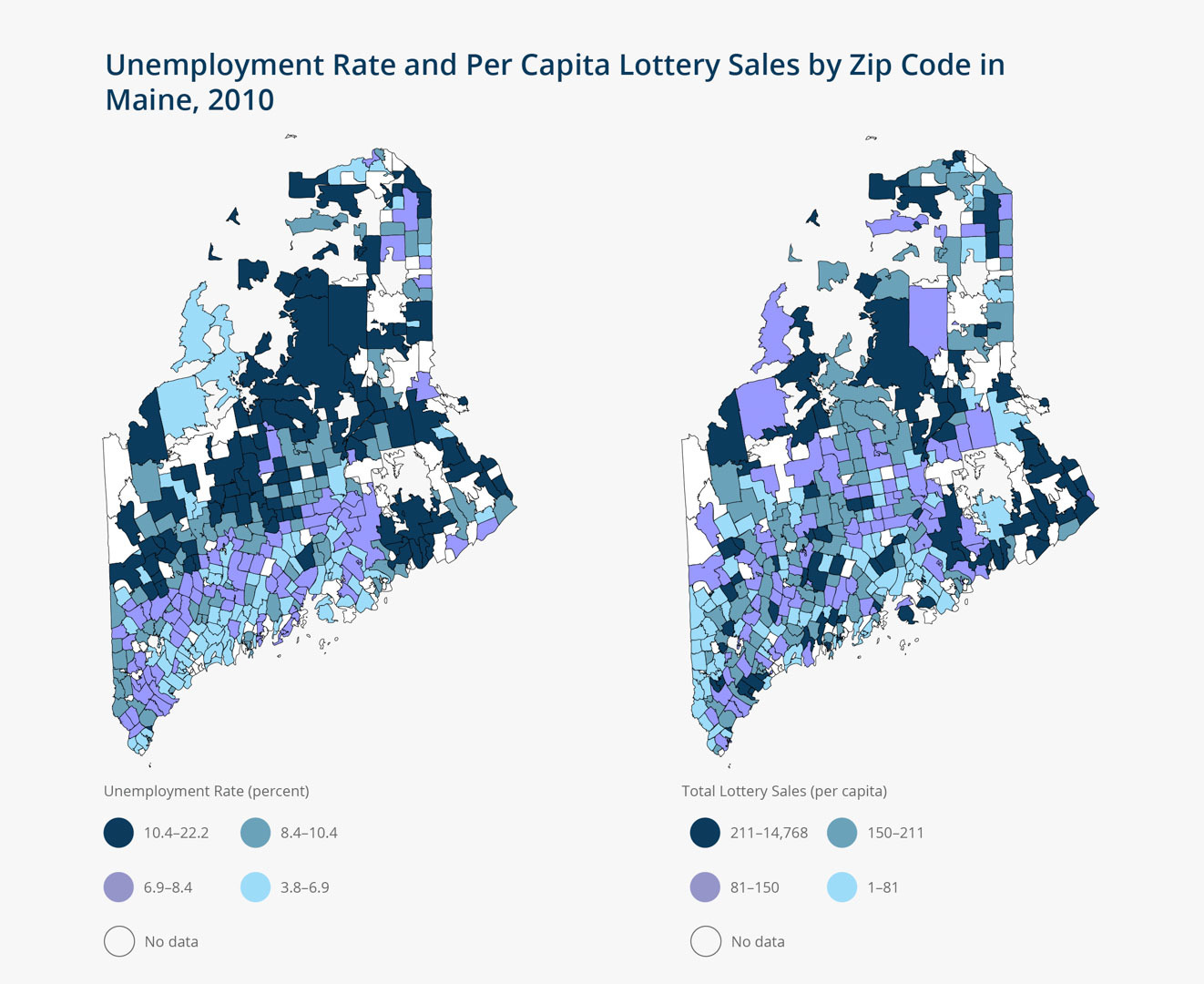

Though a rise in the percentage who are unemployed is associated with an increase in draw lottery sales, an increase in unemployment compensation within a zip code area is associated with a decrease in draw lottery sales. (See "Unemployment Rate and Per Capita Total Lottery Sales by Zip Code in Maine, 2010.") Higher average unemployment compensation can result either from having a greater number who qualify for unemployment, or from those who qualify receiving greater benefits. Unemployment benefits are generally based upon wages when previously employed. Thus, the result may indicate that increases in low-skill unemployment have very different results from increases in high-skill unemployment. An alternative explanation is that the result simply confirms that immediate reductions in income are associated with greater lottery play.

The lottery in Maine has gained significant attention lately for the number of those receiving public assistance who have won substantial jackpots.14 These winnings raise interesting questions regarding the efficiency of using the lottery for public finance and the impact on other goals, such as social welfare. In this vein, we find that both the average number of dependents per household and income from pensions or social security are associated with lottery purchases—although in this case the association is with instant-play lottery sales. In other words, these longer-term indicators are associated with seeking after cheaper and more frequent chances at smaller jackpots.

Raising the Question

Even though the probability of winning a big jackpot is very small, lotteries are thought by many of the most poor as the only means of escape to a better life. However, lotteries put an extra burden on this same socioeconomic group, and on those at risk of becoming a member of it. States offering lotteries to raise revenue for state budgets should consider the disproportionate impacts on the unemployed, the elderly, and those suffering financial setbacks and should be very careful how they market the lotteries. As Maine grapples with how to preserve its state lottery revenues without preying on the poor, it is worth asking the question more widely: what is the proper role of state lotteries?

Articles may be reprinted if Communities & Banking and the author are credited and the following disclaimer is used: "The views expressed are not necessarily those of the Federal Reserve Bank of Boston or the Federal Reserve System. Information about organizations and upcoming events is strictly informational and not an endorsement."

About the Authors

About the Authors

David Just,

Cornell University

David Just is a professor and codirector of the Cornell Center for Behavioral Economics in Child Nutrition Programs at the Charles H. Dyson School of Applied Economics and Management.

Email: drj3@cornell.edu

Gnel Gabrielyan,

Cornell University

Gnel Gabrielyan is a postdoctoral researcher at the Cornell Food and Brand Lab, also at the Dyson School.

Email: gg352@cornell.edu

Endnotes

- “Lottery Sales and Transfers,” North American Association of State and Provincial Lotteries, 2016, http://www.naspl.org/index.cfm?fuseaction=content&menuid=17&pageid=1025.

- David H. Vrooman, “An Economic Analysis of the New York State Lottery,” National Tax Journal 29, no. 4 (1976): 482–89.

- “Lottery Sales and Transfers.”

- See G. Loewenstein, “Lottery Tickets and Credit Cards: The Dangers of an Irrational Brain. Scientific American 11 (2008); G. Blalock, D.R. Just, and D.H. Simon, “Hitting the Jackpot or Hitting the Skids: Entertainment, Poverty, and the Demand for State Lotteries,” American Journal of Economics and Sociology 66, no. 3 (2004): 545–70.

- “About Us,” Maine Lottery, http://www.mainelottery.com/about/index.html.

- Thomas A. Garrett and Thomas L. Marsh, “The Revenue Impacts of Cross-Border Lottery Shopping in the Presence of Spatial Autocorrelation,” Regional Science and Urban Economics 32, no. 4 (2002): 501–19.

- See Multi-State Lottery Association, http://www.musl.com.

- “Powerball: Prizes and Odds,” Multi-State Lottery Association, http://www.powerball.com/powerball/pb_prizes.asp.

- Daniel Victor, “You Will Not Win the Powerball Jackpot,” New York Times, January 12, 2016.

- “Instant Tickets,” Maine Lottery, http://www.mainelottery.com/instant/index.html.

- Blalock, Just, and Simon, “Hitting the Jackpot or Hitting the Skids.”

- E. Haisley, R. Mostafa, and G. Loewenstein, “Subjective Relative Income and Lottery Ticket Purchases,” Journal of Behavioral Decision Making 2, no. 3 (2008), 283–95.

- Blalock, Just, and Simon, “Hitting the Jackpot or Hitting the Skids.”

- Dave Sherwood, “People on Public Assistance Spent Hundreds of Millions on the Lottery—and Took Home $22 Million in Winnings,” Pine Tree Watchdog, December 16, 2015.