Have US Households Depleted All the Excess Savings They Accumulated during the Pandemic?

During the COVID-19 pandemic, US households accumulated a historically high volume of personal savings. As the crisis waned, personal savings started to decline. Economists disagree on whether households have drained their excess savings, and they disagree on which income group is more likely to have done so. The lack of consensus stems from different assumptions about today’s long-term saving rate, which is used as a benchmark to define excess savings. If households need to set aside a higher share of their income now relative to before the pandemic, then pandemic-era excess savings have been almost entirely depleted. If households need to set aside the same share as the pre-pandemic average (6.2 percent), then only one-fourth of the excess savings has been depleted. Under the latter assumption, most income groups still had access to substantial amounts of savings through the end of 2022, and the rates of depletion of excess savings were quite similar across income groups.

Sign up for new research and data on the New England economy.

During the COVID-19 pandemic, generous government transfers and lockdown-induced reductions in spending generated an exceptional volume of personal savings. Tracking the amounts of pandemic-era savings is of significant policy interest because these unspent dollars can provide a cushion to sustain consumers when interest rates increase. These savings are as important in their distribution across households as they are in the aggregate because, for example, low-income households may be particularly vulnerable to the current monetary tightening cycle if they have depleted their savings buffer.

While the importance of tracking excess savings is undisputed, there is wide variation in published estimates.1 The difference in these estimates widens as we move away from the pandemic and as we focus on the distribution of excess savings across households. In this brief, we clarify why aggregate excess savings estimates diverge from each other and determine how these savings are allocated across income groups.

Most estimates of excess savings differ because of seemingly innocuous assumptions about the long-term saving trend in the US economy. Excess savings are now depleted only if we assume that households need to set aside a higher share of their income today compared with before the pandemic. If we assume instead that the underlying saving rate should be equal to the pre-pandemic average (6.2 percent), then only one-fourth of the excess savings has been depleted.2 Our new method for estimating excess savings across the income distribution allows us to assign excess dollars to a specific US county. After mapping counties to their income levels, we find that as of the end of 2022, most income groups still had access to significant amounts of savings and that there is no substantive difference in the savings-reduction rate across income groups.

Measuring Pandemic-induced Excess Savings

Households allocate some of their income to retirement savings, rainy-day funds, debt payments, or future large purchases. These decisions determine the national saving rate, which typically moves slowly over time. Excess savings are balances that deviate from this long-term level of saving and capture fluctuations related to the current economic cycle. To measure pandemic-induced excess savings, economists compare the observed rate of saving with the long-term rate of saving that would have prevailed in the absence of the pandemic.

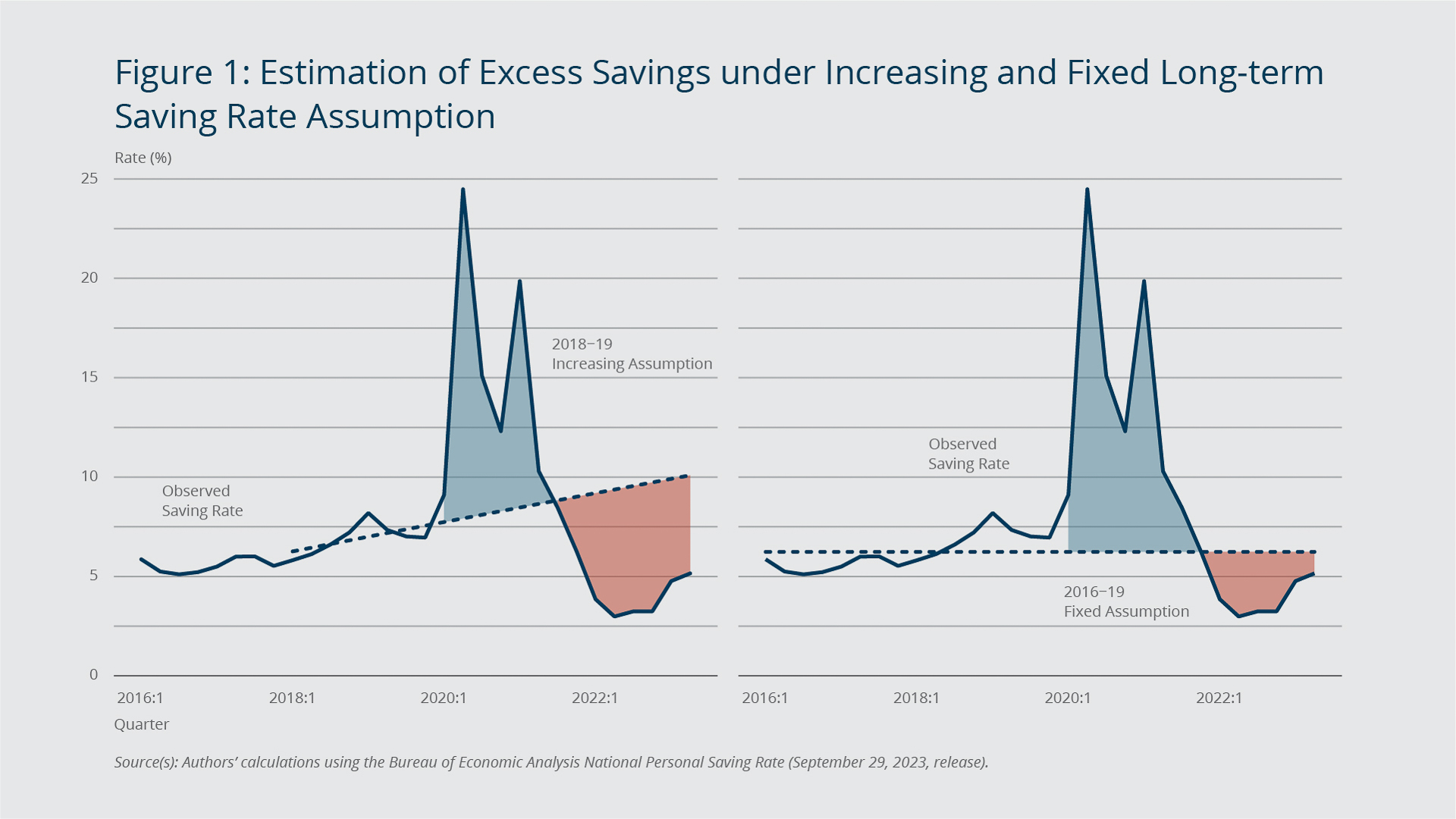

In Figure 1, we show the evolution of the saving rate from 2016 to the present at a quarterly frequency. The saving rate averaged 6.2 percent from 2016 through 2019, with an uptick starting at the end of 2018. In 2020, the pandemic-induced lockdowns limited household spending, and households received generous government transfers. Together, these two changes led to a large increase in the saving rate—nearing 25 percent in the third quarter of 2020. The final round of stimulus payments generated a second spike in the national saving rate in 2021:Q1. Since then, there has been a steady decline in the saving rate.

{kind=link}

Federal Reserve Bank of Boston

How does the observed saving rate compare with the long-term saving rate? The answer to this question has led researchers to different conclusions. To illustrate this point, we estimate excess savings by employing two contrasting assumptions about the long-term saving rate from existing studies. The left panel of Figure 1 depicts our estimate of the long-term saving rate based on the idea that absent the COVID-19 pandemic, saving rates would have continued along their 2018–2019 trajectory. The difference between the solid line (the observed saving rate) and the dashed line (the long-term saving rate) represents pandemic-induced excess savings. From 2020 through 2021, excess savings were positive because the observed saving rate exceeded the long-term average. Each quarter in which the observed rate is higher than the long-term rate implies an accumulation of excess savings, represented by the blue area. Starting in 2022, excess savings declined as the observed saving rate fell below the long-term average. The cumulative depletion of excess savings is represented in orange. In the right panel of Figure 1, we conduct a similar exercise but assume that if the pandemic had not occurred, saving rates would have remained fixed at their 2016–2019 average of 6.2 percent.

Although the estimates of excess saving rates in the left and right panels of Figure 1 might appear similar, each points to a very different amount of unspent savings available to households today.

Reasonable Assumptions Lead to Large Differences in the Current Amount of Excess Savings

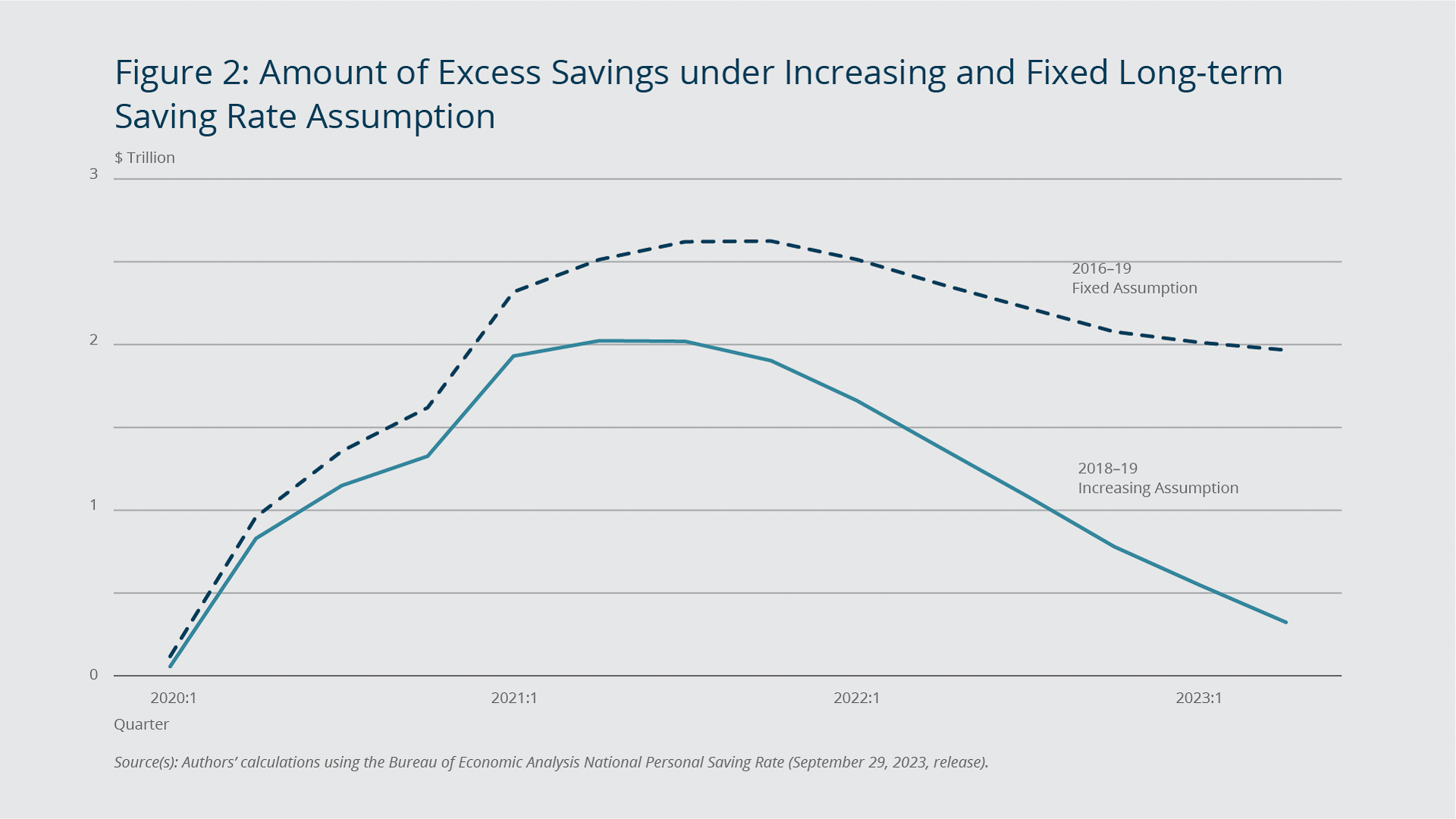

Having shown how the saving rate evolved over the course of the pandemic, we now turn to estimating the overall amount of excess savings implied under the two different assumptions. In Figure 2 we show the cumulative pandemic-induced deviations of observed savings from the long-term rate implied by each assumption. Notably, our estimates rely on data released by the Bureau of Economic Analysis (BEA) on September 29, 2023. When compared with previous data vintages, the September 2023 data revision suggests a larger level of excess savings available today regardless of the assumption about long-term saving rates.3

{kind=link}

Federal Reserve Bank of Boston

If we assume that the saving rate would have increased in line with the 2018–2019 trend, then excess savings peaked in mid-2021 at over $2 trillion, and about $321 billion remains available today. If we assume that the saving rate would have remained fixed at the 2016–2019 average, then the amount of excess savings peaked in late 2021 at about $2.5 trillion, and about $2 trillion remains.

The assumptions underpinning the estimates in Figure 2 are both plausible. On the one hand, saving rates were rising steadily in the pre-pandemic years, and the trend might represent a growing need for savings by the US population. On the other hand, at a very long horizon, saving rates are generally more stable. Under the increasing-rate assumption, the implied saving rate for 2023:Q2 would be 10.1 percent, but the United States has not seen saving rates higher than 10 percent since the early 1980s.

The fact that there is a gap of more than $1.5 trillion between the savings estimates for the current period highlights the significant uncertainty about the extent to which households’ reliance on excess savings will continue to cushion the economy. At the heart of the matter is knowing the reference point of how much savings US households need for their long-term objectives and how much of these funds is easily accessible. The policy discussion on excess savings should always highlight which long-term saving rate is assumed as a benchmark and whether that rate is higher or lower than the rate from the pre-pandemic years.

Excess Savings Are Being Drawn Down Relatively Evenly across Income Groups

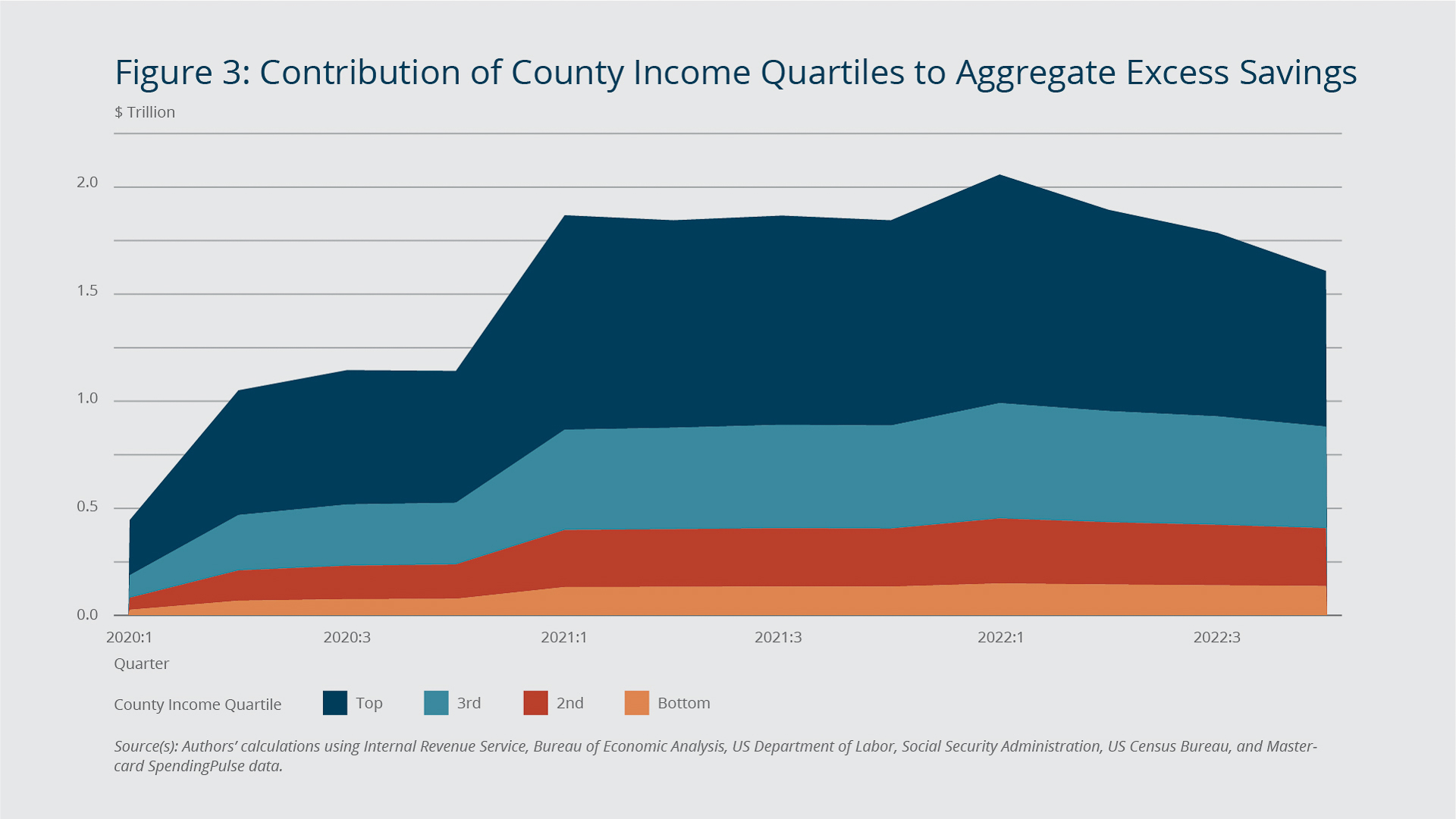

While Figure 2 shows that the aggregate excess savings varies substantially based on modeling assumptions, a related policy concern centers on measuring how excess savings are distributed across households in different income groups. National accounts data on income and spending do not provide an answer to this question because they represent the entire economy. By contrast, detailed account-level data on individual-level bank balances provide only a partial answer because they measure cash savings but exclude other potentially important forms of savings such as retirement accounts, CDs, stocks, bonds, and reductions in debt balances. To shed light on this question, we use several disaggregated sources of data and build estimates of excess savings at the county level.

Our disaggregated disposable income is constructed from several official sources, including the Internal Revenue Service, the US Department of Labor, the Social Security Administration, and the US Census Bureau. We construct our measure of spending from a proprietary data set known as Mastercard SpendingPulse, which measures in-store and online retail sales across all forms of payment within each county. We rescale these estimates so that they represent total expenditure as opposed to retail-specific spending.4

Because median household income varies substantially across counties, our estimates provide useful proxies for the underlying differences in excess savings across the household income distribution. We split the set of approximately 3,000 US counties into four equally sized groups based on the median household income in 2019. We then compute excess savings following the same method described above for the aggregate national savings, assuming a fixed 2016–2019 long-run saving rate for each income group.5 Figure 3 depicts the estimate of national excess savings that we obtain from this bottom-up approach. It shows each income quartile’s contribution to national savings. The estimates line up fairly well with the estimates obtained using aggregate series from the US Bureau of Economic Analysis.6

{kind=link}

Federal Reserve Bank of Boston

The top quartile of the income distribution represents counties where the median household income is in the highest quarter of the national income distribution, and the bottom quartile represents counties where the median household income is in the lowest quarter of the national income distribution.7 The top income quartile accounts for the largest share of excess savings, with each subsequent quartile accounting for a smaller share. This ordering represents the fact that the higher income counties tend to be more populated, as well as wealthier, than the lower income counties and therefore account for a bigger slice of the amount of national excess savings.

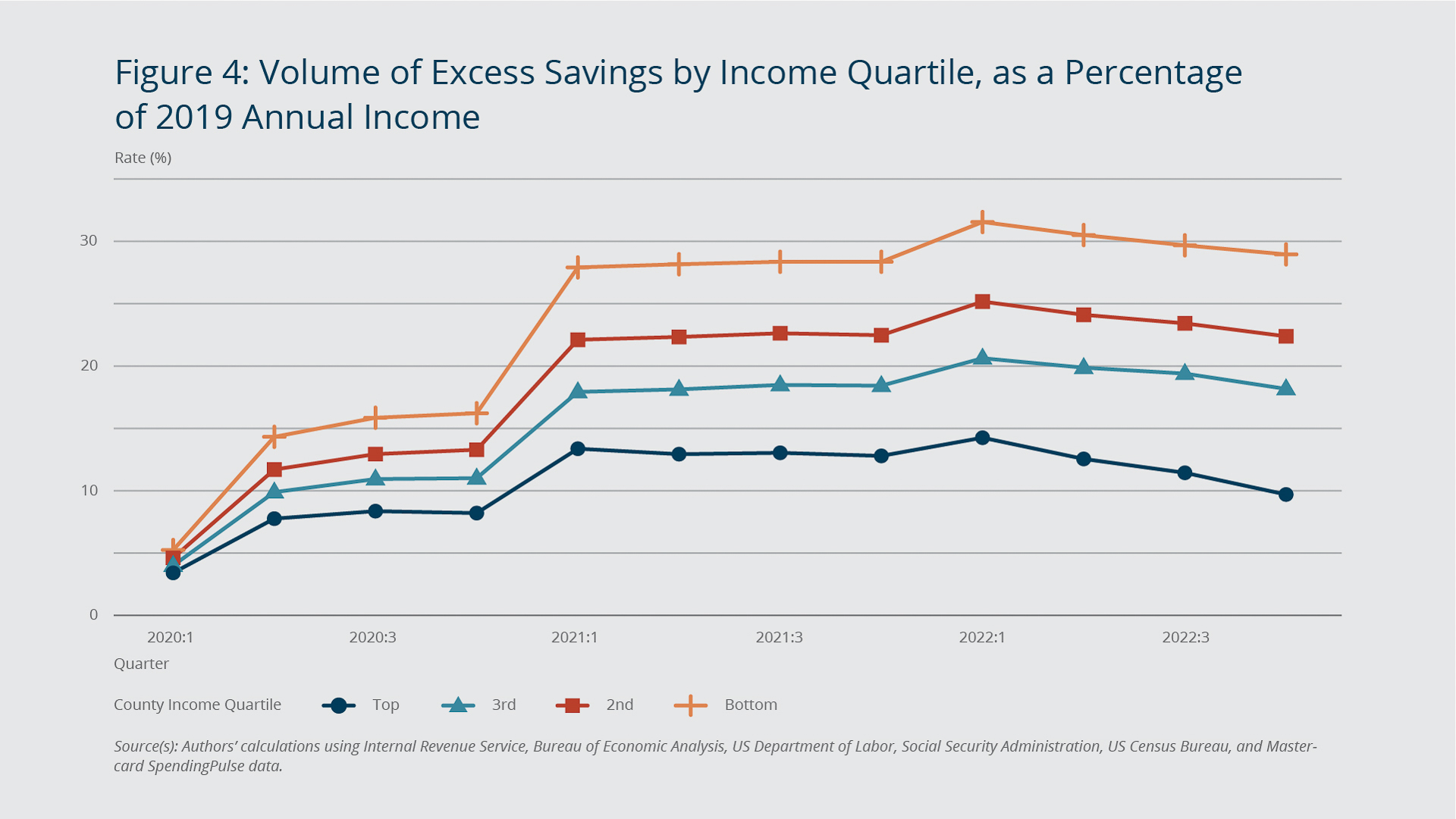

In Figure 4, we divide excess savings within each quartile by annual income. The figure reveals that, relative to income levels, excess savings are most important for the lowest quartile of the income distribution and successively less important for each higher income level. Notably, the drawdown of savings that began in early 2021 progressed at a similar rate across all four income groups at least through the end of 2022, when our data end. This pattern indicates that excess savings did not deplete faster in low-income counties relative to high-income counties. We verified that the bottom three income quartiles exhibit similar rates of savings depletion under the alternative assumption of an increasing long-term saving rate. Under the latter assumption, only the top income quartile exhibits faster savings depletion.

{kind=link}

Federal Reserve Bank of Boston

Conclusion

We make two key points in this article. First, our analysis of recently revised national data highlights that the measurement of pandemic-induced excess savings is inherently dependent on modeling assumptions about the long-term benchmark saving rate that would have prevailed in the absence of the pandemic. Consequently, policy discussions on excess savings should carefully qualify which long-term saving rate is assumed as a benchmark.

Second, using a mix of official and proprietary county-level data, we find that rates of depletion of excess savings have been very similar across income groups, regardless of the assumption about a long-term saving-rate benchmark. While these estimates indicate that low-income consumers did not draw down excess savings earlier than high-income consumers, data limitations prevent us from knowing whether the same patterns hold in 2023.

The views expressed herein are those of the authors and do not indicate concurrence by the Federal Reserve Bank of Boston, the principals of the Board of Governors, or the Federal Reserve System.

Endnotes

- Some examples are Adelrahman and Oliveria (2023a, 2023b), Aladangady et al. (2022), Bowley et al. (2023), Lieugard et al. (2023), de Soyre, Moore, and Ortiz (2023), Wheat and Deadman (2023), and Wheat and Eckerd (2023).

- Most of the excess-savings estimates cited in the note above are based on a wide variety of assumptions about the long-term saving rate that includes more than just the two we use as references in this paper. Some papers estimate a separate exponential trend on each nominal income and consumption component; others estimate a linear trend on the pre-pandemic nominal amount of savings; others use time-series filtering; and others keep the saving rate fixed at the 2019:Q4 value. However, most methods boil down to being within the spectrum of our two reference assumptions.

- In the appendix, we reproduce Figures 1 and 2 by using older BEA data that are used in several existing reports. Qualitatively, we see the same pattern; that is, the fixed long-term saving rate assumption implies a higher level of excess savings today relative to an increasing long-term saving rate assumption.

- Retail sales typically exclude important categories such as housing and health-care expenditure and is therefore only a partial measure of total outlays. We implement a statistical adjustment that enables us to surmount this limitation and estimate total county-level expenditure. Our procedure first estimates initial spending levels as disposable income times one minus the long-term saving rate in each county. We then predict subsequent spending levels by applying growth rates of retail spending estimated from the Mastercard SpendingPulse data. The key assumption underpinning our adjustment is that unobserved housing and health-care components of spending grew at rates comparable to retail spending in each county during and after the pandemic. We verify that this assumption appears to hold at the state level.

- We assume a long-run saving rate fixed at the 2016–2019 average to enable a more transparent comparison of drawdown rates by income group. Allowing for an increasing or decreasing long-run saving trend across income groups does not let us determine whether drawdown differences are due to pre-pandemic trend heterogeneity or a divergence in observed saving rates.

- Our estimate of aggregate excess savings based on county-level data differs from our estimates based on aggregate series for several reasons. First, our county-level estimates are not seasonally adjusted, which is why the amount for the first quarter of every year tends to be high. Second, our spending measure is based on adjusted retail sales spending growth and not total personal consumption expenditure. Third, while aggregate-level estimates of excess savings are computed by comparing observed savings with one aggregate saving trend, the income-group estimates assume income-group-specific saving-trend growth. Finally, we do not include some smaller counties in our estimates because spending data from these counties is suppressed in the Mastercard SpendingPulse data set for privacy protection or because some income series are not available.

- Due to data limitations, our measure of excess savings stops at the end of 2022, which prevents us from examining the more recent evolution of trends across the income distribution.

References

Adelrahman, Hamza, and Luiz E. Oliveira. 2023a. “The Rise and Fall of Pandemic Excess Savings.” FRBSF Economic Letter 2023-11, Federal Reserve Bank of San Francisco.

Adelrahman, Hamza, and Luiz E. Oliveira. 2023b. “Excess No More? Dwindling Pandemic Savings.” SF Fed Blog, Federal Reserve Bank of San Francisco.

Aladangady, Aditya, David Cho, Laura Feiveson, and Eugenio Pinto. 2022. "Excess Savings during the COVID-19 Pandemic." FEDS Notes. Washington, DC: Board of Governors of the Federal Reserve System.

Bowley, Taylor, Liz E. Krisberg, David M. Tinsely, and Anna Zhou. 2023. “Higher-income Pullback.” Bank of America Institute Consumer Checkpoint 2023-05.

De Soyres, Francois, Dylan Moore, and Julio L. Ortiz. 2023. "Accumulated Savings during the Pandemic: An International Comparison with Historical Perspective." FEDS Notes. Washington, DC: Board of Governors of the Federal Reserve System.

Lieugart, Arnaud, Karl-Philip Nilsson, Usama Karatella, and Partick Malm. 2023. “Capital Cities, British Purchasing Power and Dwindling US Savings.” Macrobond Charts of the Week.

Wheat, Chris, and Erica Deadman. 2023. “Household Pulse: Balances through March 2023.” JPMorgan Chase Institute.

Wheat, Chris, and George Eckerd. 2023. “Household Cash Buffer Management from the Great Recession through COVID-19.” JPMorgan Chase Institute.

About the Authors

About the Authors

Omar Barbiero,

Federal Reserve Bank of Boston

Omar Barbiero is an economist in the Federal Reserve Bank of Boston Research Department.

Email: Omar.Barbiero@bos.frb.org

Dhiren Patki,

Federal Reserve Bank of Boston

Dhiren Patki is a senior economist in the Federal Reserve Bank of Boston Research Department.

Email: Dhiren.Patki@bos.frb.org

Resources

Site Topics

Keywords

- excess savings ,

- consumption ,

- disposable income ,

- wealth inequality

JEL Codes

- E01 ,

- E21 ,

- E25

Citation

Barbiero, Omar, and Dhiren Patki. 2023. “Have US Households Depleted All the Excess Savings They Accumulated during the Pandemic?” Federal Reserve Bank of Boston Current Policy Perspectives. November 7, 2023.