Effects of Tariff Uncertainty on the Outlook of Small and Medium-sized Businesses

{kind=link}

Federal Reserve Bank of Boston

The views expressed herein are solely those of the authors and should not be reported as representing the views of the Federal Reserve Bank of Boston, the principals of the Board of Governors, or the Federal Reserve System.

Uncertainty about future business conditions can exert an important influence on the economic decisions of firms. For example, when import tariffs increase, but the level at which they will settle and how long they will remain elevated are unclear, firms may decide to temporarily pause imports and await clarity. In fact, after US tariffs on imports from China increased by a staggering 145 percentage points in early April 2025, and it became apparent that the two countries were going to negotiate tariff rates over the coming months, US goods imports from China fell in May to about half their value at the start of this year—a collapse even larger than the one that followed the initial COVID-19 pandemic shock.1

A large body of research demonstrates that uncertainty affects many dimensions of firms’ decisions, from investment and hiring to pricing and profitability. To gain a better understanding of how uncertainty induced by shifting trade policy shapes the behavior of small and medium-sized businesses (SMBs, firms employing 500 or fewer workers)—which account for roughly half of private-sector employment and about a third of international trade2—we surveyed decision-makers at SMBs.

Sign up for Research Department Updates.

The survey, administered by Morning Consult, was conducted in three waves: in December 2024, February 2025, and late April 2025. Each wave contained a nationally representative sample of about 600 SMBs. We implemented additional quality assurance checks and used appropriate statistical techniques to ensure that the sample of businesses in the survey is nationally representative of all SMBs in the United States. See the accompanying appendix for details. The questions, a selection of which are included in the appendix accompanying this brief, focus on SMBs’ uncertainty concerning what would happen over the ensuing 12 months with import tariffs and with their own growth in employment, investment, prices, costs, revenues, and profit margins.

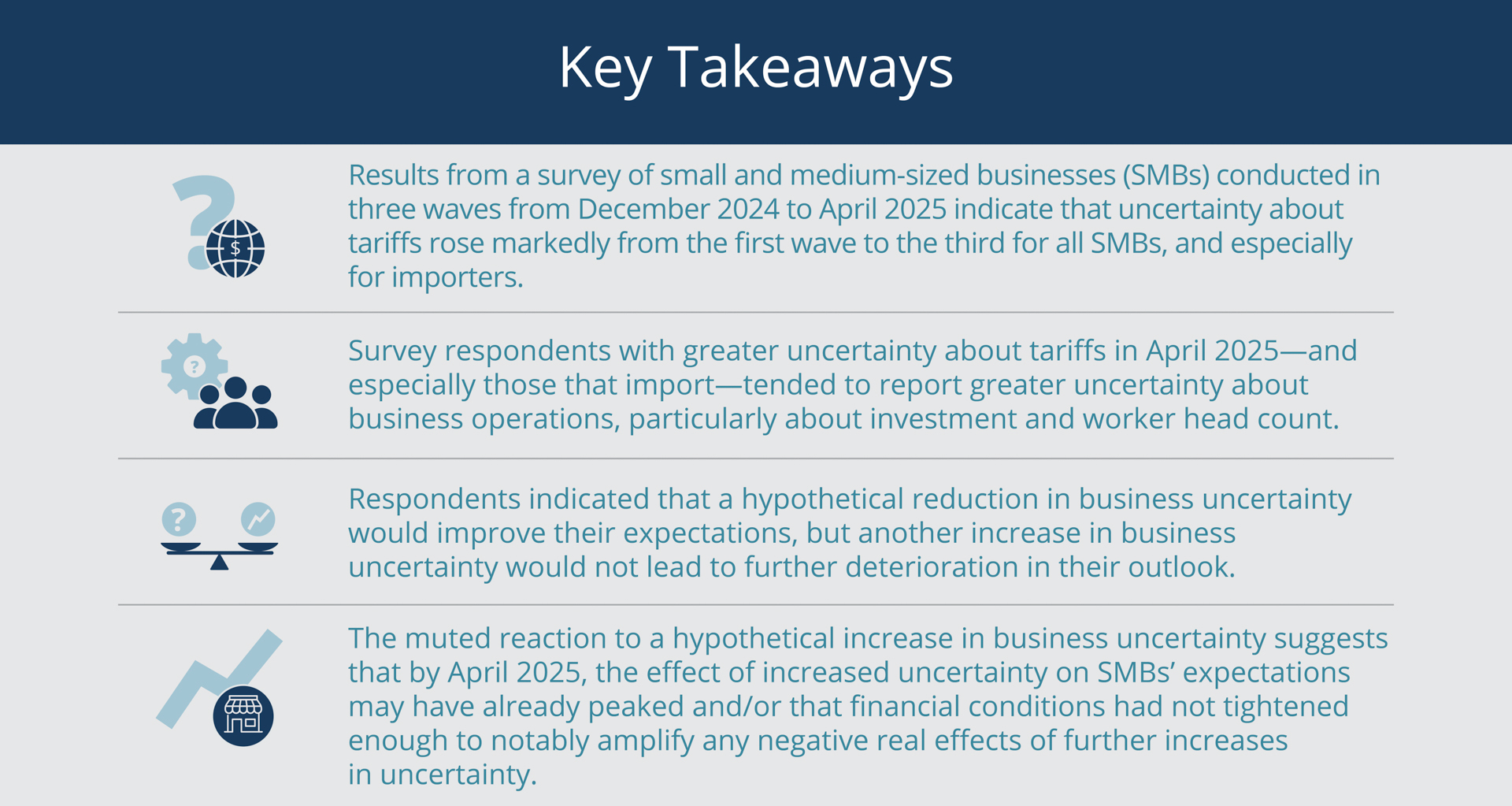

Our analysis of the responses indicates that uncertainty about tariffs rose markedly for all SMBs—and especially for those that import—from the first wave to the third, increasing sharply in April 2025 and reflecting heightened trade-policy ambiguity at that time. Moreover, uncertainty about tariffs in April 2025 was closely linked to uncertainty about business operations—particularly about investment and worker head count among importers—indicating that SMBs view trade-policy risk as intertwined with their broader planning environment.

What is the effect of uncertainty on key economic variables for SMBs, according to responses to the April 2025 wave of the survey? When we asked a randomly chosen sample of SMBs how a hypothetical increase or decrease in their business uncertainty would affect their outlook for investment, demand, revenues, profitability, head count, and costs and prices, the respondents indicated that a reduction in uncertainty would improve their expectations, but another increase in uncertainty would not lead to further deterioration.

The responses reveal a clear asymmetry: A reduction in uncertainty elicits an outlook that is substantially more optimistic—again, more so for importers—whereas an increase in uncertainty does not trigger a similarly strong pessimistic response. The muted reaction to the latter hypothetical scenario suggests that by April 2025, the effect of increased uncertainty on firms’ expectations may have already peaked. Another possibility is that financial conditions had not tightened enough to notably amplify any negative real effects of further increases in uncertainty. Together, these findings shed new light on how SMBs adjust their decision-making in the current economic environment, which holds important implications for the transmission of trade-policy shocks to the broader economy.

SMBs Became More Uncertain about Tariffs in April 2025

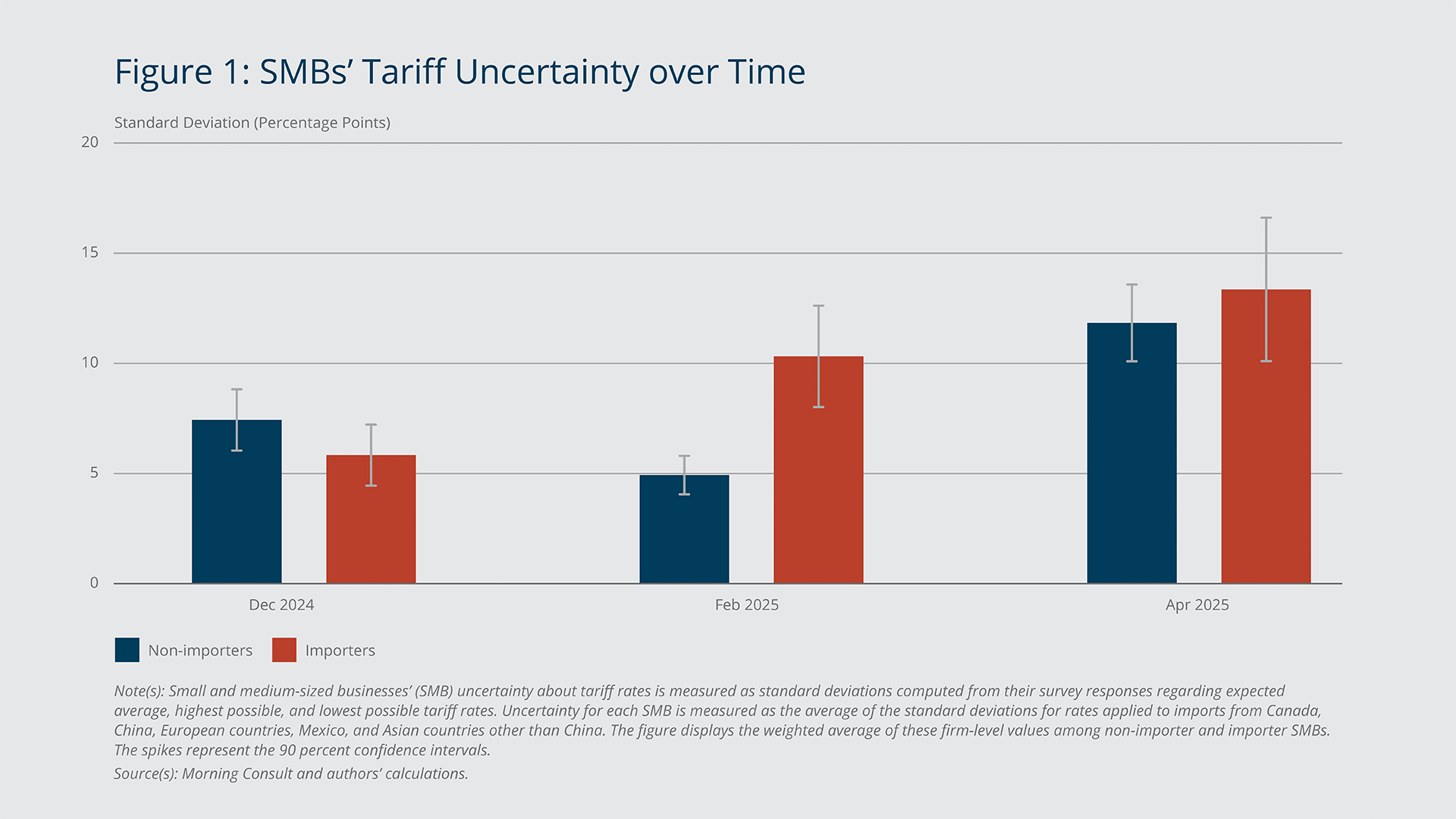

To capture individual SMB’s uncertainty about key business outcomes, our survey elicited, in each wave, three-point forecasts for the coming year. For import tariffs, we asked decision-makers what they expected the average level, the lowest level, and the highest level (all in percentages) would be for each of five major geographical regions that may serve as import sources. For employment, investment, prices, costs, revenues, and profit margins, we asked decision-makers the percentage changes they anticipated their SMB would experience in each of those outcomes under the expected scenario, the worst-case scenario, and the best-case scenario. (These questions are included in the appendix.) We then computed the standard deviations of possible outcomes implied by each firm’s set of responses. A standard deviation increases with the difference between possible outcomes and the average/expected outcome (in percentage point units); therefore, in this case, larger values indicate greater uncertainty.

Figure 1 illustrates several findings from the three waves of the survey. First, importers’ uncertainty about tariffs rose markedly in February relative to December and increased further in April, coincident with substantial changes in US trade policy. In April 2025, the average uncertainty about tariffs among importers was 13.4 percentage points, in terms of the standard deviation, while it stood at 5.8 percentage points in December and 10.3 percentage points in February. Second, non-importers’ uncertainty also increased substantially over time. However, it declined from 7.4 percentage points in December to 4.9 in February before rising to 11.8 percentage points in April. Overall, this pattern suggests that SMB decision-makers swiftly and markedly became more uncertain about tariff rates, especially importers, who would be directly affected by tariffs.

{kind=link}

Federal Reserve Bank of Boston

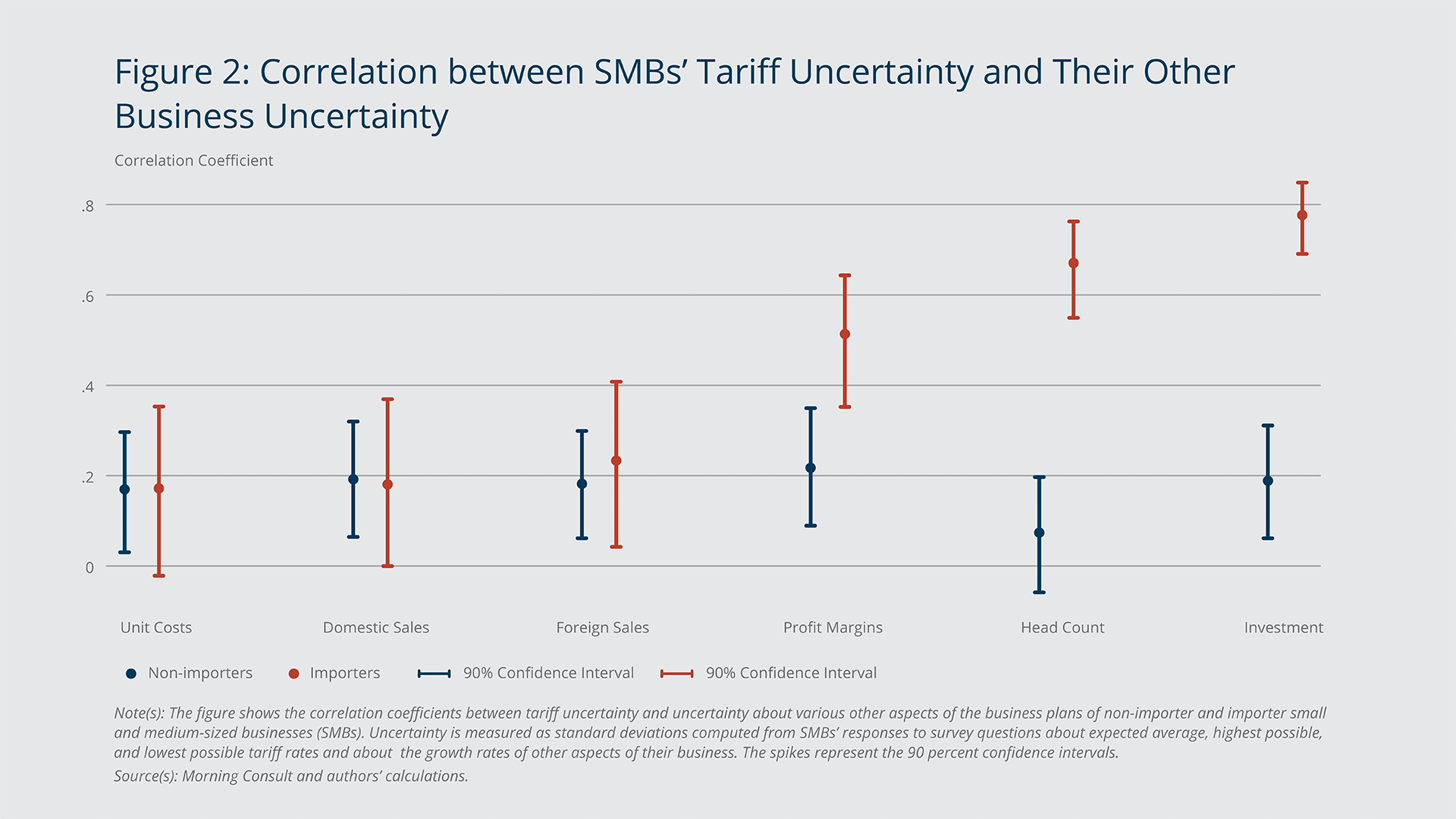

Comparing our measures of tariff uncertainty with those for uncertainty about broader conditions reveals that SMBs’ dispersion in tariff forecasts is positively correlated with the dispersion they report for expectations and plans regarding employment, investment, prices, costs, revenues, and profit margins—that is, higher levels of uncertainty about tariffs were associated with higher levels of uncertainty about other aspects of SMBs’ business plans. This relationship is notably stronger for importers than for non-importers. These patterns are depicted in Figure 2, which plots the pairwise correlations between tariff uncertainty and each measure of business uncertainty for importers (in red) and non-importers (in blue): The larger the coefficient, the stronger the correlation with tariff uncertainty.

{kind=link}

Federal Reserve Bank of Boston

Resolution of Business Uncertainty Would Improve SMBs’ Outlook

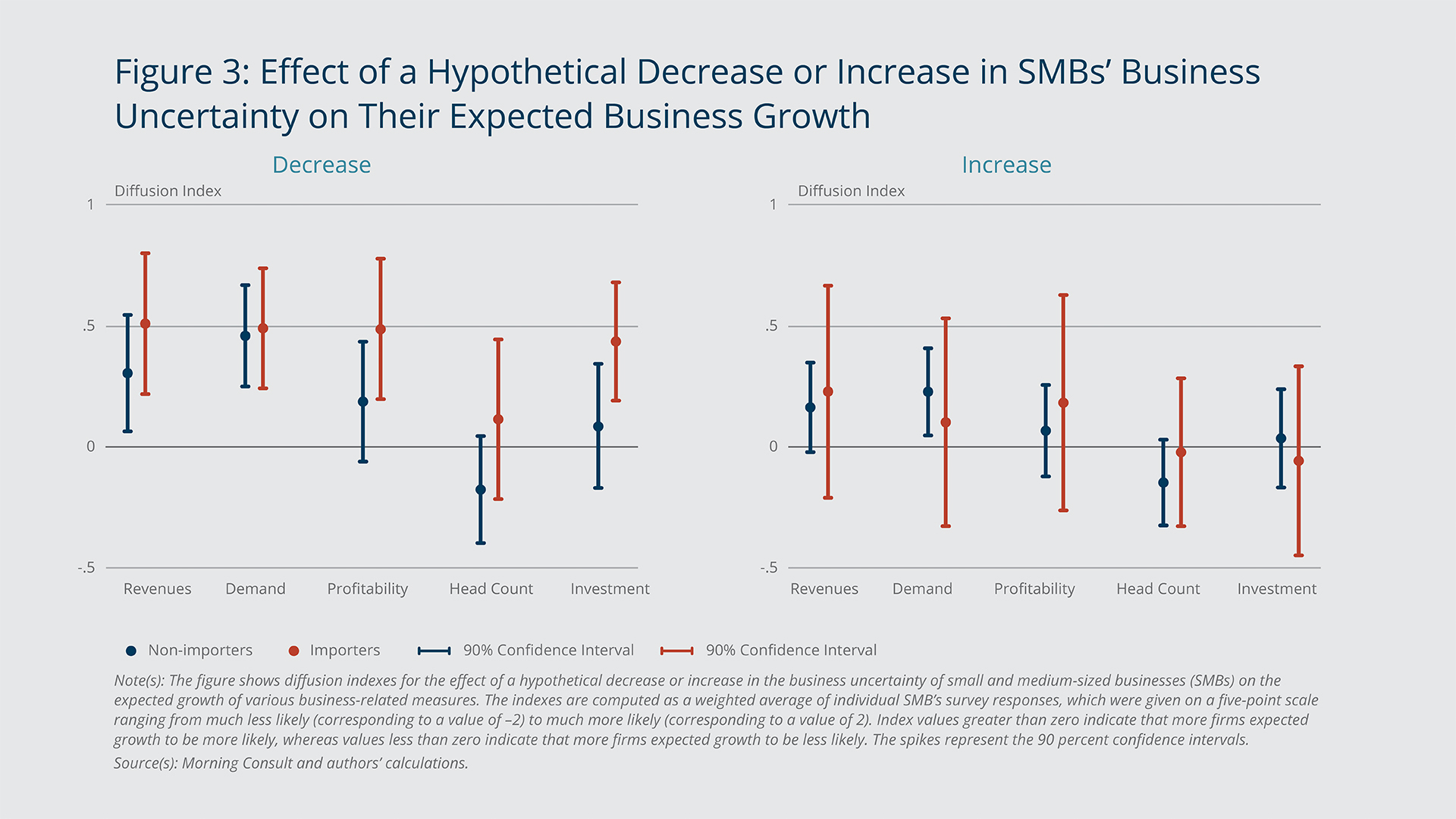

The increase in uncertainty about business expectations could also reflect the possibility of worse prospects due, for instance, to expectations of higher tariffs.3 To assess how a pure increase in general business uncertainty shaped SMBs’ real‐time decisions in April 2025, we embedded a randomized “what‐if” experiment in our survey. Respondents were asked to imagine a hypothetical increase or decrease in their firm’s overall uncertainty (not just uncertainty about tariffs) and to indicate, on a scale from “much less likely” to “much more likely,” how this change would alter their propensity to expand revenue, demand, profitability, head count, and investment. Figure 3 shows the results.

{kind=link}

Federal Reserve Bank of Boston

As we anticipated, respondents expected that a decrease in general business uncertainty would boost all these outcomes—especially for importers, which is consistent with our earlier finding of a stronger connection between tariff uncertainty and business uncertainty among importing SMBs. It is important to keep in mind that our experiment was designed to isolate the effect of a change in business uncertainty while other variables, including the level of actual tariff costs, remained constant. Since the height of tariff uncertainty in April of 2025, businesses exposed to the new tariffs likely have experienced an improvement in their outlook due to some resolution of tariff uncertainty. At the same time, however, they also face increasing tariff costs, the effects of which are beyond the scope of this study.4

We were surprised to find that SMBs did not report a similarly strong negative outlook in response to an increase in general business uncertainty. One interpretation of this result is that by April 2025, the adverse effects of trade‐policy uncertainty had already materialized or “peaked,” leaving respondents little additional pessimism to express about a potential further increase in uncertainty.

A related factor is that, despite elevated uncertainty, financial conditions had not tightened appreciably at that time, as reflected by market proxies such as corporate bond credit spreads (the difference between the yields of longer-term corporate bonds and those of comparable maturity Treasury securities). In fact, banks—an important source of external finance for SMBs—on net reported having eased loan-rate spreads (the difference between the interest rate banks charge borrowers and banks’ cost of funds) for small firms during the first quarter of 2025.5 Moreover, rates on credit cards, a source of financing used by 57 percent of SMBs in our survey, remained lower than their late-2024 peak.6

Because tightening credit often amplifies the real costs of uncertainty (Caldara et al. 2016), its absence may help explain why firms did not express that more uncertainty would further deteriorate their prospects. However, if financial conditions were to tighten going forward, greater business uncertainty may begin to weigh more heavily on the economy.

Endnotes

- This observation is based on the authors’ calculations using US Census Bureau data on seasonally adjusted nominal imports from China. See US Census Bureau, “Imports, Seasonally Adjusted (Nominal).” Exports, Imports and Trade Balance by Selected Countries and Areas (accessed July 18, 2025).

- See “A Profile of U.S. Importing and Exporting Companies, 2022–2023,” US Census Bureau Release Number CB25-52, April 3, 2025.

- See our previous Current Policy Perspectives brief, Andrade et al. (2025), for such evidence.

- See the estimates of realized tariff rates being paid by US importers in Gary Clyde Hufbauer and Ye Zhang, “Trump’s Tariff Revenue Tracker: How Much Is the US Collecting? Which Imports Are Hit?” PIIE Charts, Peterson Institute for International Economics, August 21, 2025.

- See “The April 2025 Senior Loan Officer Opinion Survey on Bank Lending Practices,” Board of Governors of the Federal Reserve System.

- See “Commercial Bank Interest Rate on Credit Card Plans, All Accounts (TERMCBCCALLNS),” May 2025, Board of Governors of the Federal Reserve System, retrieved from FRED, Federal Reserve Bank of St. Louis.

References

Andrade, Philippe, Alexander M. Dietrich, John Leer, Raphael S. Schoenle, Jenny Tang, and Egon Zakrajšek. 2025. “Small and Medium-sized Businesses’ Expectations Concerning Tariffs, Costs, and Prices.” Federal Reserve Bank of Boston Current Policy Perspective 25-7.

Caldara, Dario, Cristina Fuentes-Albero, Simon Gilchrist, and Egon Zakrajšek. 2016. “The Macroeconomic Impact of Financial and Uncertainty Shocks.” European Economic Review 88(C): 185–207.

Kotz, Samuel, and Johan Rene van Dorp. 2004. Beyond Beta: Other Continuous Families of Distributions with Bounded Support and Applications. World Scientific.

About the Authors

About the Authors

Philippe Andrade,

Federal Reserve Bank of Boston

Philippe Andrade is a vice president and economist in the Federal Reserve Bank of Boston Research Department.

Email: Philippe.Andrade@bos.frb.org

Alexander M. Dietrich is a research economist in the Danmarks Nationalbank Research Unit.

Sophie Handley,

Federal Reserve Bank of Boston

Sophie Handley is a research assistant in the Federal Reserve Bank of Boston Research Department.

John Leer is the chief economist at Morning Consult.

Raphael S. Schoenle,

Federal Reserve Bank of Boston

Raphael S. Schoenle is a professor of economics at Brandeis University and a visiting scholar in the Federal Reserve Bank of Boston Research Department.

Jenny Tang,

Federal Reserve Bank of Boston

Jenny Tang is a vice president and economist in the Federal Reserve Bank of Boston Research Department.

Email: Jenny.Tang@bos.frb.org

Egon Zakrajšek,

Federal Reserve Bank of Boston

Egon Zakrajšek is an executive vice president at the Federal Reserve Bank of Boston and the director of the Research Department.

Email: Egon.Zakrajsek@bos.frb.org

Acknowledgments

Resources

Site Topics

Keywords

- business expectations ,

- Surveys ,

- tariffs ,

- uncertainty

JEL Codes

- F13 ,

- F40 ,

- D22 ,

- D81 ,

- C83

Citation

Andrade, Philippe, Alexander Dietrich, Sophie Handley, John Leer, Raphael Schoenle, Jenny Tang, and Egon Zakrajšek. 2025. “Effects of Tariff Uncertainty on the Outlook of Small and Medium-sized Businesses.” Federal Reserve Bank of Boston Current Policy Perspectives 25-12.