Who Will Pay for Tariffs? Businesses’ Expectations about Costs and Prices

{kind=link}

Federal Reserve Bank of Boston

The views expressed herein are solely those of the authors and should not be reported as representing the views of the Federal Reserve Bank of Boston, the principals of the Board of Governors, or the Federal Reserve System.

Amid evolving global trade policy and rising tariff uncertainty, understanding how small and medium-sized businesses (SMBs) form expectations about future costs and adjust their pricing is critical for assessing how the recently imposed tariffs on US imports could impact consumer prices. To that end, we analyze several waves of a survey of owners and other decision-makers at a nationally representative sample of US SMBs,1 defined as companies that employ 500 or fewer workers. We focus on waves conducted during the period of December 2024 to August 2025.2

The survey elicited decision-makers’ expectations about new tariffs on US imports from specific countries or groups of countries and how long they expected those new tariffs to last. It also asked the SMBs about expected changes to their unit costs and about changes they planned to make to the prices of their primary product or service.

Sign up for Research Department Updates.

Collectively, the survey responses reveal SMBs’ average planned pass-through rate—that is, how much of the expected cost increases, which for some firms may be driven largely by new tariffs, SMBs planned to pass on to consumers in the form of price increases—and their evolving beliefs about future tariff rates.

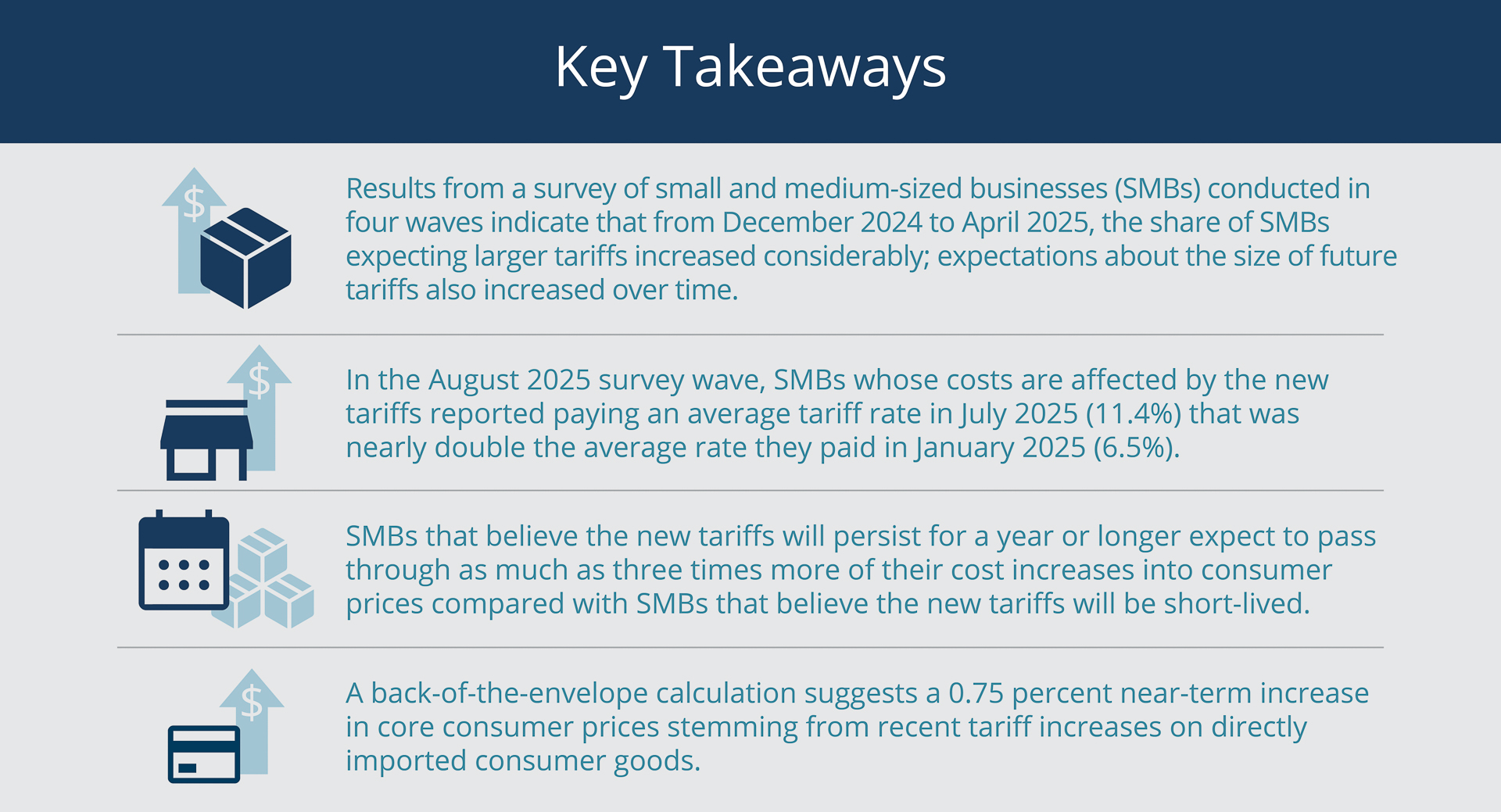

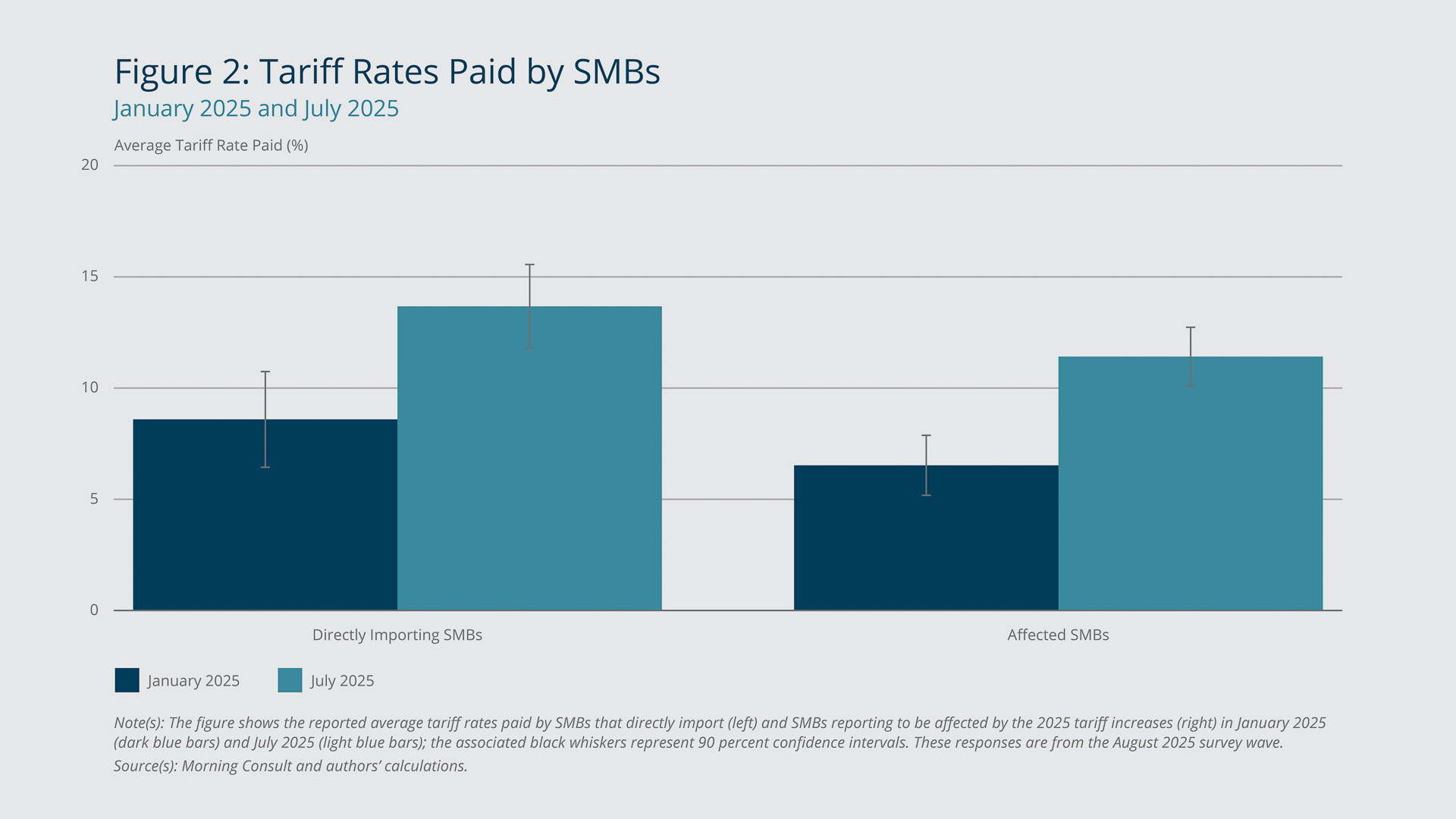

Among the findings that emerge from the survey data is that during the first four months of 2025, SMBs significantly raised their expectations about future tariffs, from an average rate of roughly 19 percent to an average rate of about 25 percent. SMBs whose costs are affected by the new tariffs also revealed that they paid an average tariff rate in July 2025 that was nearly double the average rate they paid in January 2025, up from 6.5 percent to 11.4 percent.

In the later survey waves, most of the importer SMBs said they anticipated passing a substantial portion of their cost increases into consumer prices. A back-of-the-envelope calculation using our findings suggests a 0.75 percent near-term increase in core consumer prices (which excludes food and energy prices) from the higher tariff costs on directly imported consumer goods.3

Our analysis detects an important feature of beliefs about evolving trade policy and planned pricing policies: SMBs that believe the new tariffs will persist for a year or longer anticipate notably higher pass-through rates; compared with their counterparts that believe the new tariffs will be short-lived, the former expected to pass through as much as three times more of their cost increases into consumer prices. As of August 2025, more than 45 percent of SMBs that reported being affected by the new tariffs expected their own firm’s costs to be impacted for longer than a year. This fraction exceeds 60 percent for firms affected by certain policies such as increased levies on imports from European countries and Asian countries other than China or the end of the de minimis tariff exemption on small-valued packages.

SMBs’ Tariff Expectations and Tariff Costs Increased Significantly This Year

Morning Consult, a US company that specializes in survey research, conducted the survey, administering waves in December 2024, February 2025, April 2025, and August 2025. Each wave included 500 to 600 participants. The first three waves asked the SMBs about the tariff rate they expected on US imports from each of five countries or groups of countries: Canada, Mexico, European Union countries, China, and other Asian countries. The August 2025 wave asked respondents to report the actual tariff costs they paid in January of this year, before the imposition of new tariffs, and in July.

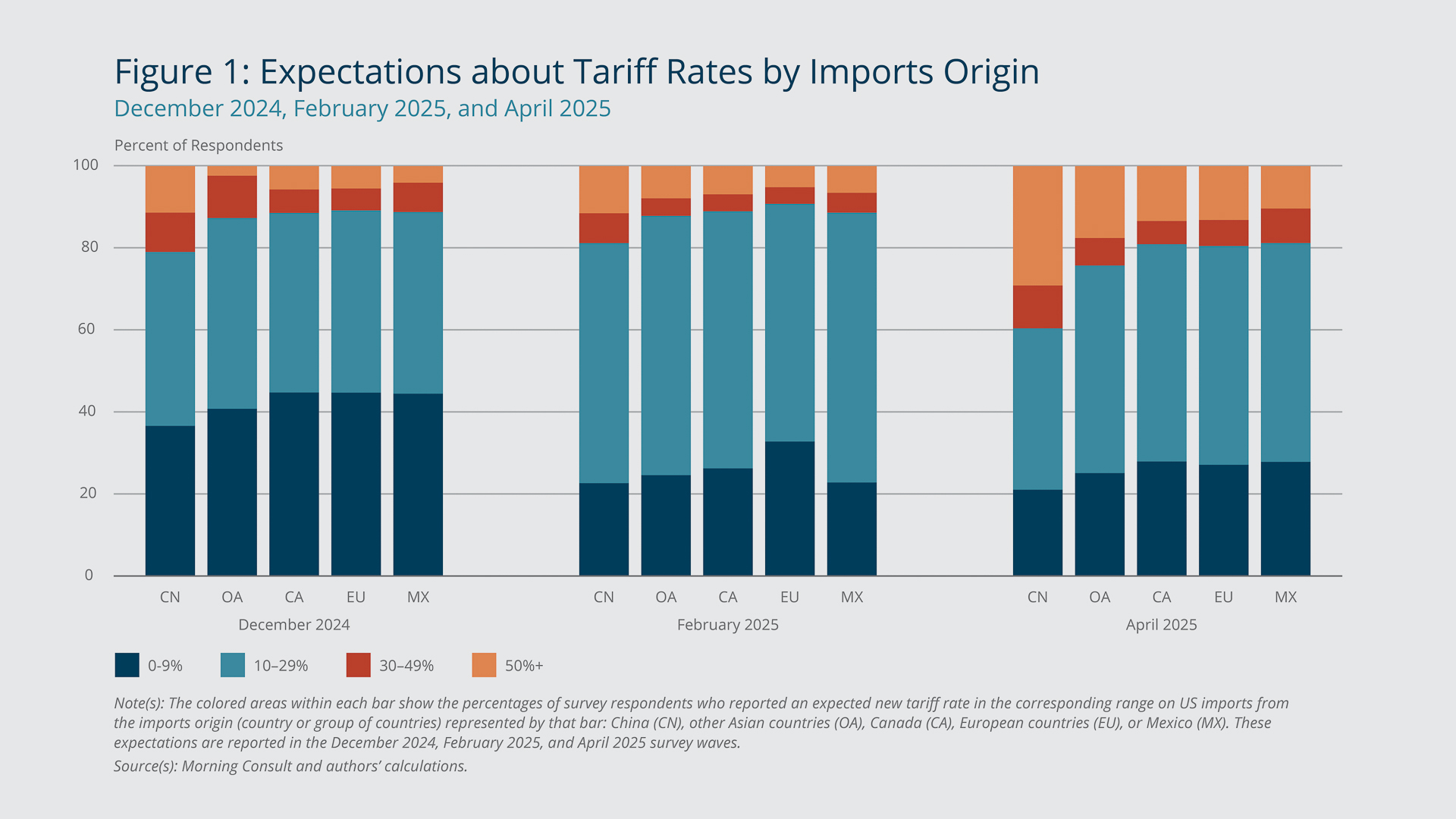

Comparing responses across the December 2024, February 2025, and April 2025 survey waves reveals a clear upward drift in tariff expectations; with each successive wave, a larger share of SMBs anticipated higher tariffs. The comparison also shows a wide range of expectations, likely reflecting continued uncertainty among SMBs about tariff policy.

As Figure 1 shows, the distribution of tariff expectations has shifted markedly over time. Compared with the responses to the initial, December 2024 survey wave, the responses to the February 2025 wave indicate that a smaller share of firms expected tariffs to remain low (at 0 to 9 percent, dark blue bars) and more firms expected moderate levies of at least 10 percent but less than 30 percent (light blue bars). In December 2024, nearly 40 percent of SMBs believed all tariffs would remain in the lowest bracket, but by April 2025, that share had declined to about 20 percent. By April 2025, the share of SMBs expecting tariffs to end up at rates of 50 percent or more (orange bars) had nearly doubled compared with the share from the December 2024 wave. This shift is particularly pronounced for tariffs related to China. In December 2024, only 10 percent of SMBs anticipated that the tariff rate on goods from China would settle in excess of 50 percent. By April 2025, the share had climbed to 30 percent.

{kind=link}

Federal Reserve Bank of Boston

When asked in August 2025 about tariff rates paid, SMBs affected by tariffs revealed that they had paid considerably higher rates in July than in January. As noted earlier and as shown in Figure 2, their average (mean) tariff rate jumped from 6.5 percent to 11.4 percent. The rates paid by SMBs that indicated they are unaffected by recent tariff changes (not shown in the figure) largely stayed the same. Note that the average rate paid by firms that identify as non-importers (not shown in the figure) also roughly doubled, though from a much lower base because, despite not self-identifying as importers, about one-third of those firms said that they are affected by tariffs.

{kind=link}

Federal Reserve Bank of Boston

Anticipated Pass-through Rates Have Risen

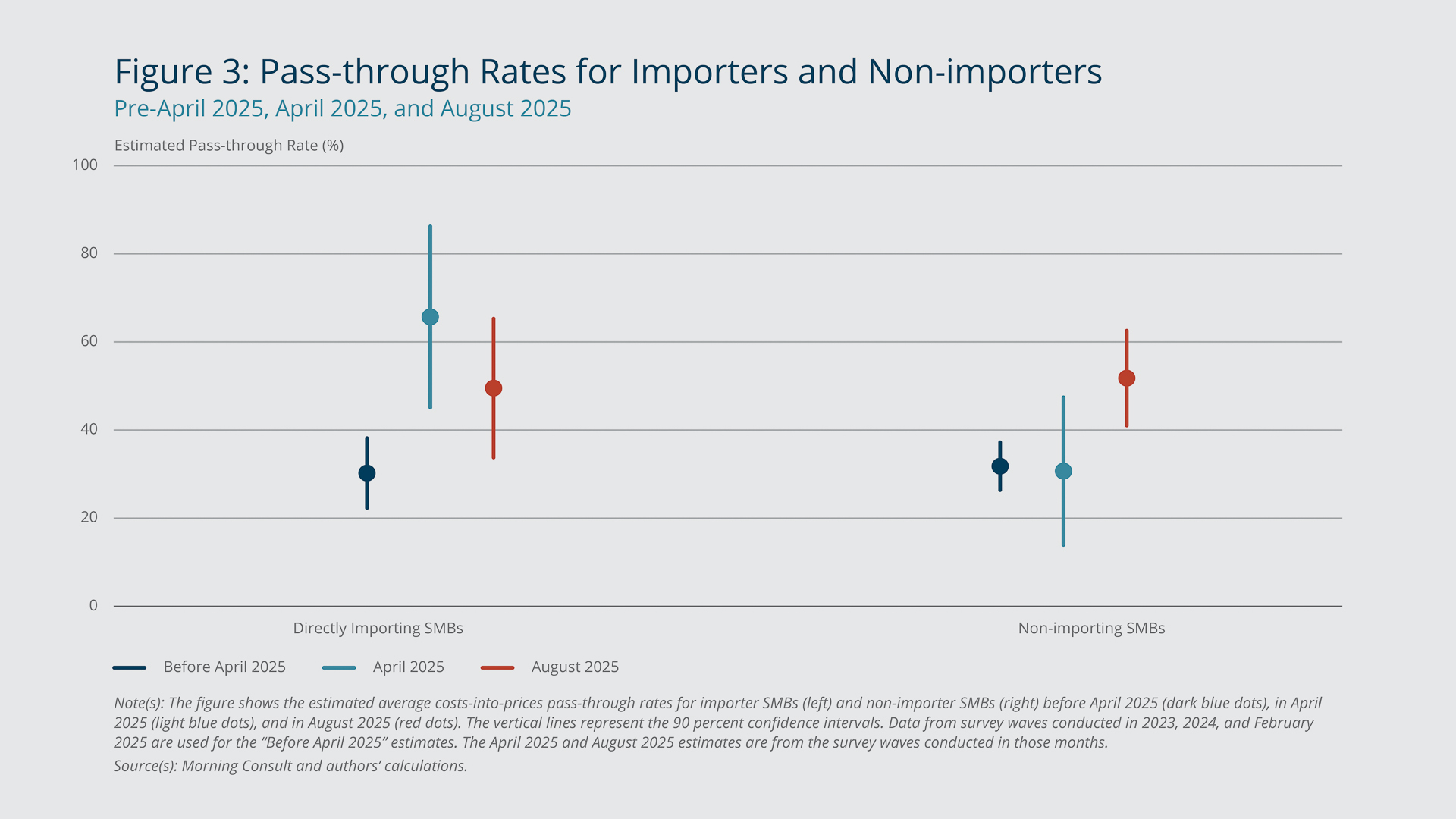

In an evolving trade-policy environment, accurately gauging the degree to which firms—especially those directly exposed to imports—intend to raise consumer prices in response to tariff-induced cost increases is crucial for assessing how tariffs could affect inflation and determining the appropriate policy response. We estimate this pass-through directly based on SMBs’ expected unit cost changes and planned price changes over the next year.

Note that, for various reasons, the pass-through could change over time. For example, firms might delay raising prices one-to-one with costs—especially when eventual tariff rates are still uncertain—if price adjustments are costly to implement or because firms want to avoid alienating customers with higher prices. However, the pass-through may eventually increase as uncertainty is resolved and firms try to recover their profit margins.

Figure 3 shows how estimated average pass-through rates changed for importers and non-importers starting in April 2025. In the April 2025 survey wave, which followed the announcement of wide-ranging reciprocal tariffs, importers indicated that they would pass through about two-thirds of their anticipated cost increases into their prices within one year. This estimated pass-through rate represents a dramatic increase relative to earlier survey waves. In the baseline of all earlier data covering 2023 through February 2025, importers and non-importers alike exhibited pass-through rates of only about one-third. By contrast, in April, non-importers still indicated that they would pass through only about one-third of their anticipated cost increases. However, by August, the pass-through rate for non-importers had risen to nearly one-half, or 50 percent, which is close to where the importer pass-through rate had settled. While expected cost increases are not limited to tariff-related costs and can include other input-cost changes, these estimates suggest that SMBs—importers and non-importers alike—would tolerate only limited compression of their profit margins (or markups) in response to rising tariffs.4

{kind=link}

Federal Reserve Bank of Boston

SMBs’ pass-through rates may have risen over the past few months for multiple reasons. First, cost pressures may have become so high that firms could not remain profitable without passing a larger fraction of the costs on to their customers. Second, many firms now expect to face higher tariff costs for a significant length of time, a point on which we elaborate later in this brief. Third, firms might feel that, with respect to customer relations, this has been a particularly good time to raise prices because major trade policy adjustments have created an environment in which customers expect price increases.

Overall, what is the implied effect of higher import tariffs on US inflation? A simple, back-of-the-envelope calculation of first-round tariff effects suggests a 0.75 percent increase in core consumer prices. Assuming imports account for 10 percent of US core personal consumption expenditures (PCE; see Barbiero and Stein 2025), a 15 percentage point increase in the average US import tariff in 2025—combined with a pass-through rate of 50 percent—yields 0.75 percent higher core PCE prices in the following year.5 Note that this calculation includes only the price impact of imported goods that are sold directly to consumers, not the effect from goods that are produced domestically with imported inputs. It also assumes that our estimate of a 50 percent pass-through rate to all customers (final consumers as well as other businesses) among SMBs that import reflects the average pass-through rate of importers of all sizes to consumers specifically.

SMBs That Expect Tariffs to Persist Are Planning Higher Pass-through Rates

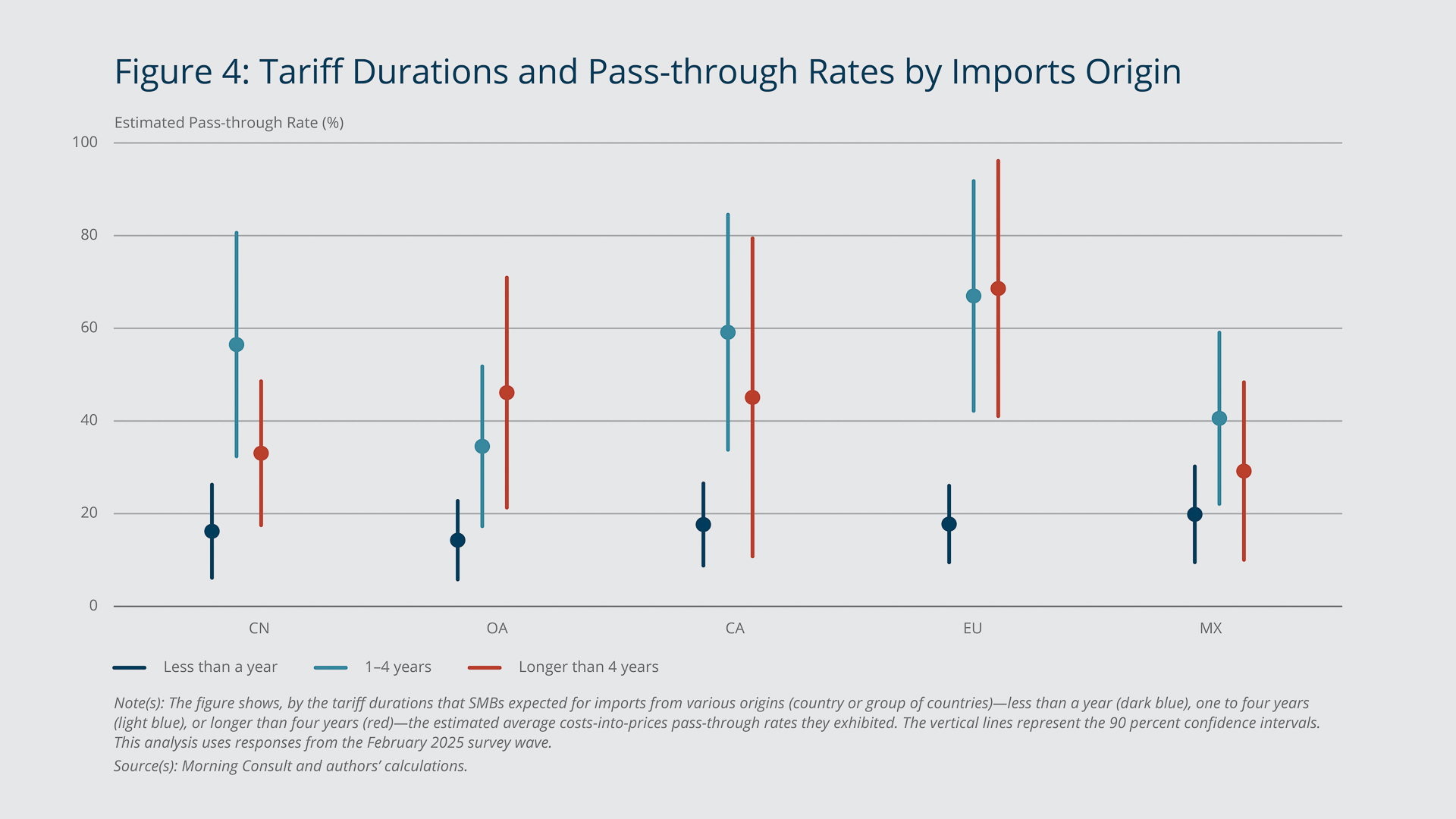

In the February 2025 wave, the survey asked SMBs to indicate how long they expected newly imposed tariffs to remain in effect for each of the aforementioned major import origins: Canada, Mexico, European Union countries, China, and other Asian countries. At that point, before the April 2 announcement of wide-ranging reciprocal tariffs, 41 to 57 percent of SMBs expected the new tariffs to last longer than a year, depending on the import origin. Firms’ beliefs about tariff persistence turn out to be a powerful driver of their price‐setting plans, regardless of whether they are importers. In the February 2025 wave of the survey, businesses that anticipated the new tariffs would last one to four years or more than four years exhibited an expected pass‐through rate of as much as 70 percent, more than three times greater than the pass-through rate of less than 20 percent recorded for firms that expected the new tariffs to last less than a year.

This stark contrast highlights that in addition to the magnitude of tariff cost shocks, the anticipated duration of trade policy changes critically shapes the degree to which SMBs intend to pass along those costs to consumers. By contrast, we do not find a significant difference between the pass-through rate of businesses that expect tariffs to remain in place for the long term (more than four years) and the rate of those expecting tariffs to last only for the medium term (one to four years). Figure 4 illustrates these insights, showing expected pass-through rates for firms anticipating tariff durations of less than one year (dark blue), one to four years (light blue), and longer than four years (red).

{kind=link}

Federal Reserve Bank of Boston

Our results suggest that for almost all major trading partners, if firms expect the new tariffs to be short-lived, their planned pass-through into prices is significantly lower. This finding suggests that some of those firms might be willing to temporarily reduce their margins instead of increasing prices. At the same time, firms that believe tariffs will be long lasting plan to pass on the largest part of expected cost increases to their customers.

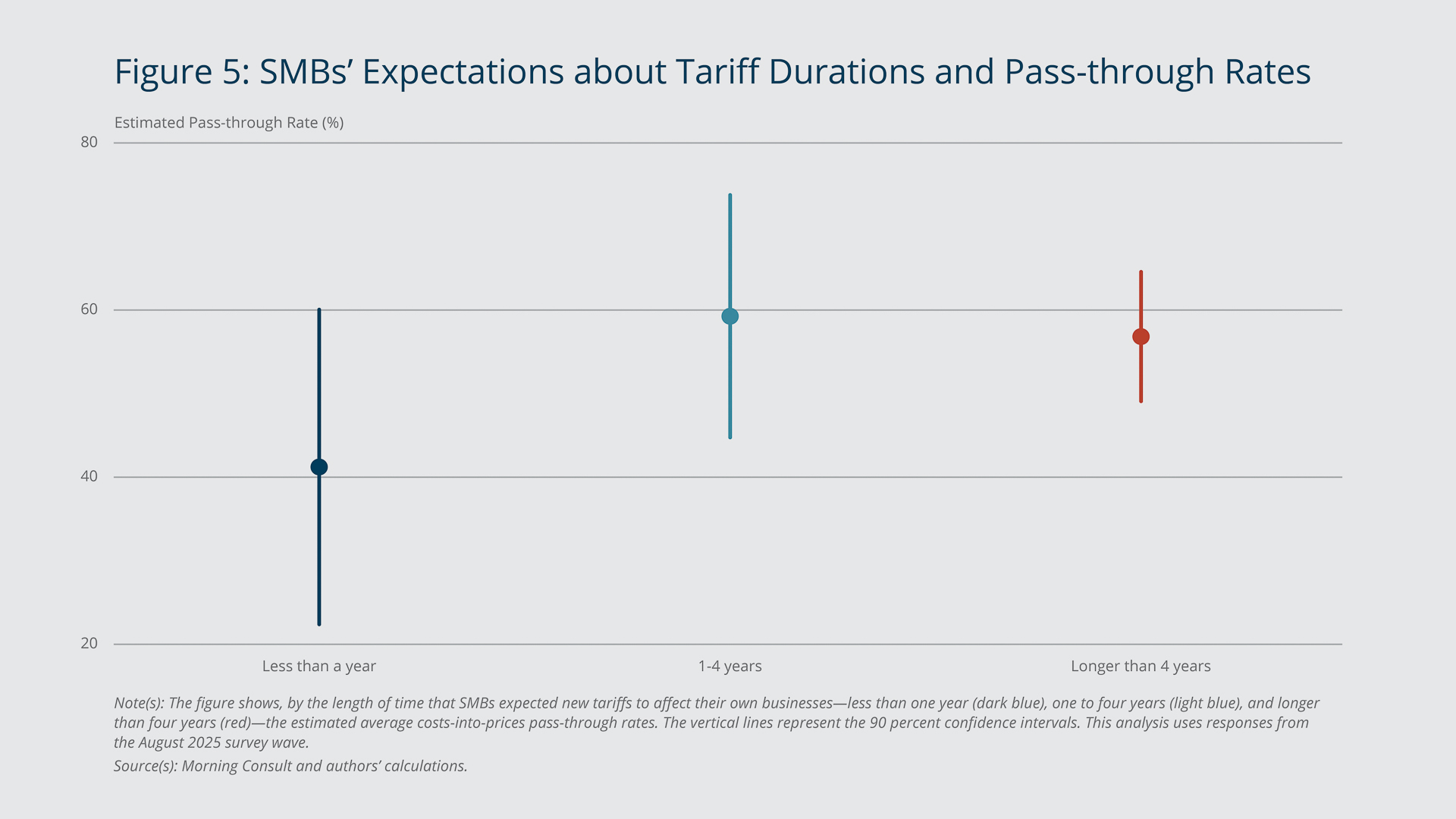

In the August 2025 wave of the survey, we asked SMBs whose costs are affected by new tariffs how long they expected their own specific costs to be affected, as opposed to their estimates of the durations of new tariff policies. These expected durations should be shorter than those for tariff policies if firms implement cost-mitigation strategies such as seeking out suppliers that are not subject to tariffs. Figure 5 shows the results from the survey question. As we found for firms expecting longer tariff durations, those expecting longer-lasting effects on their costs indicated that their pass-through rates would be higher.

{kind=link}

Federal Reserve Bank of Boston

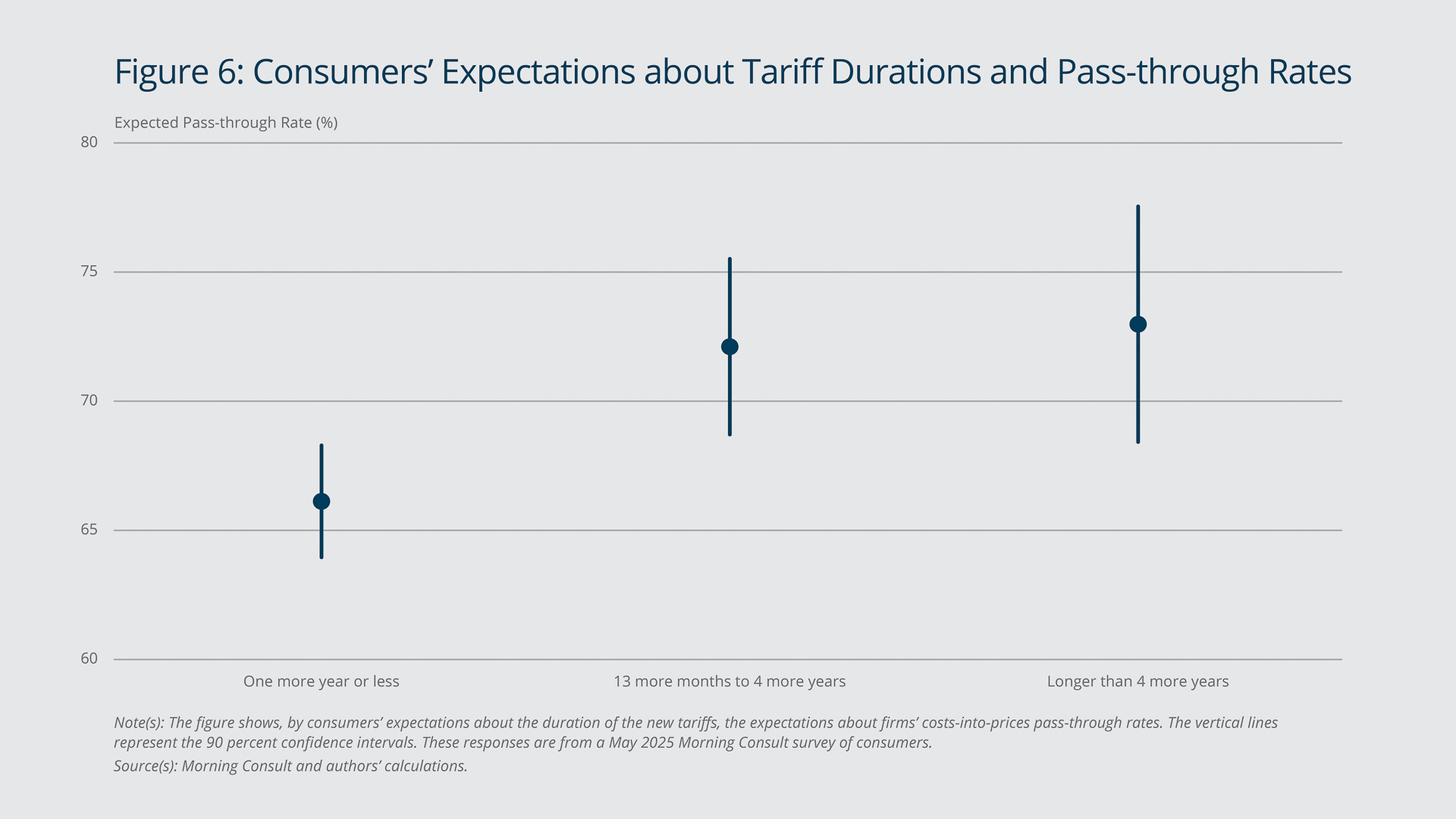

Similarly to SMBs, consumers who expected the new tariffs to last long also anticipated higher pass-through rates. The May 2025 Morning Consult Tariff Tracker surveyed about 2,200 US adults, asking how long they expected the new tariffs to last and how much of the tariff-induced cost increases they expected firms to pass through to consumers. Figure 6 depicts the results, showing a picture that is qualitatively similar to Figure 5: Consumers who expect the new tariffs to last more than a year expect a statistically significantly higher pass-through by firms compared with consumers expecting the tariffs to be removed within a year.

{kind=link}

Federal Reserve Bank of Boston

As noted, our analysis shows that firms, particularly importers, have continually revised up their tariff expectations amid persistent trade policy uncertainty, and that these evolving beliefs about tariffs translate into markedly different pricing intentions. In August 2025, importers and non-importers alike anticipated that over the next 12 months they would pass through one-half of their cost increases into their prices. Earlier in the year, they expected to pass through only one-third of their cost increases. Moreover, firms that expect tariffs to last longer plan to pass along a greater share of their increased costs to consumers.

While many firms have reported taking the brunt of the financial hit from tariffs so far (as reported by Reuters5), the patterns we find in the survey responses suggest that as firms come to believe that the new tariffs are likely to endure, they will implement more price hikes, resulting in a greater impact on consumer prices. Such a dynamic carries important implications for policymakers seeking to gauge and manage the transmission of trade-policy shocks into inflation.

Endnotes

- See the appendix to Andrade et al. (2025) for details about the survey sample.

- Refer to the figure notes for the specific survey wave or waves used to obtain each statistic or result.

- Results from an earlier wave of the survey indicate that full pass-through by importers may take closer to two years. See Andrade et al. (2025) for more details. The US Census Business Trends and Outlook Survey suggests that a similar increase in the cost-into-price pass-through occurred in or around April 2025. See the appendix accompanying this brief for additional details.

- The 15.5 percentage point increase comes from an estimate by the Budget Lab at Yale as of September 4, 2025 (“State of U.S. Tariffs: September 4, 2025”). This calculation of first-round effects from imports sold directly for consumption does not consider further effects such as higher costs of imported inputs into domestic production or substitution effects.

- See “How Companies are Responding to Trump’s Tariffs,” Reuters, July 21, 2025.

References

Andrade, Philippe, Alexander M. Dietrich, John Leer, Raphael S. Schoenle, Jenny Tang, and Egon Zakrajšek. 2025. “Small and Medium-sized Businesses’ Expectations Concerning Tariffs, Costs, and Prices.” Federal Reserve Bank of Boston Current Policy Perspectives No. 25-7.

Barbiero, Omar, and Hillary Stein. 2025. “The Impact of Tariffs on Inflation.” Federal Reserve Bank of Boston Current Policy Perspectives No. 25-2.

About the Authors

About the Authors

Philippe Andrade,

Federal Reserve Bank of Boston

Philippe Andrade is a vice president and economist in the Federal Reserve Bank of Boston Research Department.

Email: Philippe.Andrade@bos.frb.org

Alexander M. Dietrich is a research economist in the Danmarks Nationalbank Research Unit.

John Leer is the chief economist at Morning Consult.

Xiao Lin is a student in the economics and math departments at Brandeis University.

Raphael S. Schoenle,

Federal Reserve Bank of Boston

Raphael S. Schoenle is a professor of economics at Brandeis University and a visiting scholar in the Federal Reserve Bank of Boston Research Department.

Jenny Tang,

Federal Reserve Bank of Boston

Jenny Tang is a vice president and economist in the Federal Reserve Bank of Boston Research Department.

Email: Jenny.Tang@bos.frb.org

Egon Zakrajšek,

Federal Reserve Bank of Boston

Egon Zakrajšek is an executive vice president at the Federal Reserve Bank of Boston and the director of the Research Department.

Email: Egon.Zakrajsek@bos.frb.org

Acknowledgments

The authors thank David Brown, Anna Durall, Sophie Handley, and Youyang Li for excellent assistance with this brief’s data and figures.

Resources

Site Topics

Keywords

- business expectations ,

- Surveys ,

- tariffs ,

- cost pass-through ,

- inflation

JEL Codes

- E31 ,

- F13 ,

- F14 ,

- F40 ,

- C83

Citation

Andrade, Philippe, Alexander M. Dietrich, John Leer, Xiao Lin, Raphael S. Schoenle, Jenny Tang, and Egon Zakrajšek. 2025. “Who Will Pay for Tariffs? Businesses’ Expectations about Costs and Prices.” Federal Reserve Bank of Boston Current Policy Perspectives 25-13.