Why Have Inflation Expectations Surged Recently? A Historical Perspective

{kind=link}

Federal Reserve Bank of Boston

The views expressed herein are solely those of the authors and should not be reported as representing the views of the Federal Reserve Bank of Boston, the principals of the Board of Governors, or the Federal Reserve System.

Inflation expectations are key determinants of price- and wage-setting decisions—when determining what to charge consumers for goods or services and what to pay employees, businesses consider the future inflation rates that are anticipated. If, for example, workers expect prices to rise 4 percent in the next year, they are likely to demand salary increases that will enable them to retain their purchasing power if prices rise as expected, therefore increasing businesses’ labor costs. Other input costs may also rise because firms that supply material or components purchased by other firms increase their prices due to expectations of higher inflation. Businesses will then want to raise prices to at least partly cover their increased labor and input costs. In this way, inflation expectations affect inflation realization.

The Federal Reserve and other major central banks therefore pay close attention to various measures of inflation expectations, looking for undue movements that, absent an appropriate monetary policy response, could lead to persistent deviations from their inflation targets.

Sign up for Research Department Updates.

US household inflation expectations increased sharply during the inflation surge that followed the onset of the COVID-19 pandemic. This increase may have reflected the usual reaction of inflation expectations to an abnormal surge in prices. Because prices take time to fully adjust to a shock, an increase in prices today typically signals higher inflation tomorrow, and households’ expectations may just have been reflecting this regularity. However, the pandemic-era increase in inflation expectations may also have resulted from an adjustment in the way individuals form their views about future inflation, leading them to believe that inflation would remain higher than its pre-pandemic levels even after the effects of the initial shocks dissipated. This type of autonomous movements in inflation expectations—or de-anchoring—is concerning because it may fuel additional price pressures, making it more difficult for the Federal Reserve to achieve its 2 percent inflation objective.

How much of the most recent surge in inflation expectations, which began in March 2025, has been the result of the usual effect of abnormal price movements? How much is left unexplained and may signal a potential de-anchoring of inflation expectations? How do the most recent and the pandemic-era surges in expectations compare with the two surges in the Great Inflation episode of the 1970s, when inflation last rose as high as it did in 2021 and 2022?

We address these questions using data on inflation expectations from the University of Michigan Survey of Consumers and a simple regression model in which households form their inflation expectations based on their perception of movements in salient prices—prices that are particularly noticeable or significant to consumers, specifically food and gasoline prices—as well as broad-based inflation. In our model, households’ perception of salient price movements is informed by their recall of past prices.

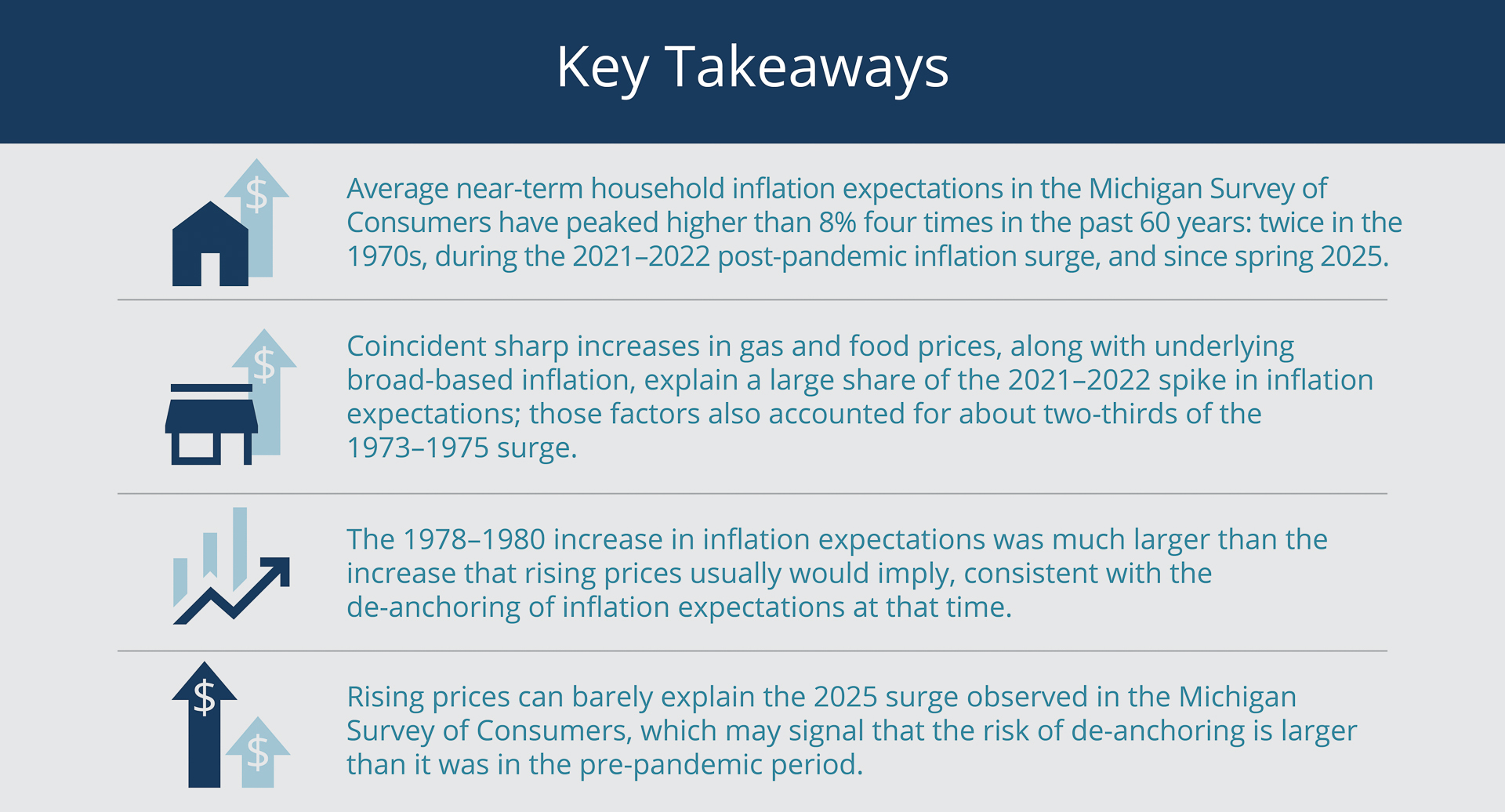

We find that the spikes in inflation expectations in the early 1970s and during the pandemic can be explained to a large degree by the steep increases in gas and food prices and the broad-based inflation that marked those periods. However, our estimates indicate that the late-1970s surge in expectations was not as closely related to price increases, and neither was the surge that began in spring 2025.

The inability of salient-price increases and broad-based inflation to account for the most recent surge observed in the Survey of Consumers could signal that the risk of inflation expectations becoming de-anchored, as they did in the late 1970s, has increased noticeably.1

US Household Inflation Expectations since the 1960s

Financial market data and surveys of professional forecasters, households, or businesses provide various measures of inflation expectations. These measures gauge either near-term expectations, which typically are for one year ahead (that is, the expected inflation rate a year from the present), or expectations for the longer term, which is typically five to 10 years ahead. While each of those measures has policy-relevant applications, here we focus on one-year-ahead household inflation expectations for two primary reasons. First, near-term household inflation expectations are more reactive to price surges or other shocks compared with longer-term measures and, therefore, are at increased risk of prolonged de-anchoring (Reis 2023). Second, relative to the inflation expectations of professional forecasters or financial-market participants, near-term household inflation expectations have a stronger influence on businesses’ wage- or price-setting decisions (Coibion and Gorodnichenko 2025), which, as noted, eventually determine realized inflation.

We chose the University of Michigan Survey of Consumers, administered by the University of Michigan Survey Research Center, as the source for data on household inflation expectations because it provides historical data that allow us to compare the post-pandemic environment with the 1970s.

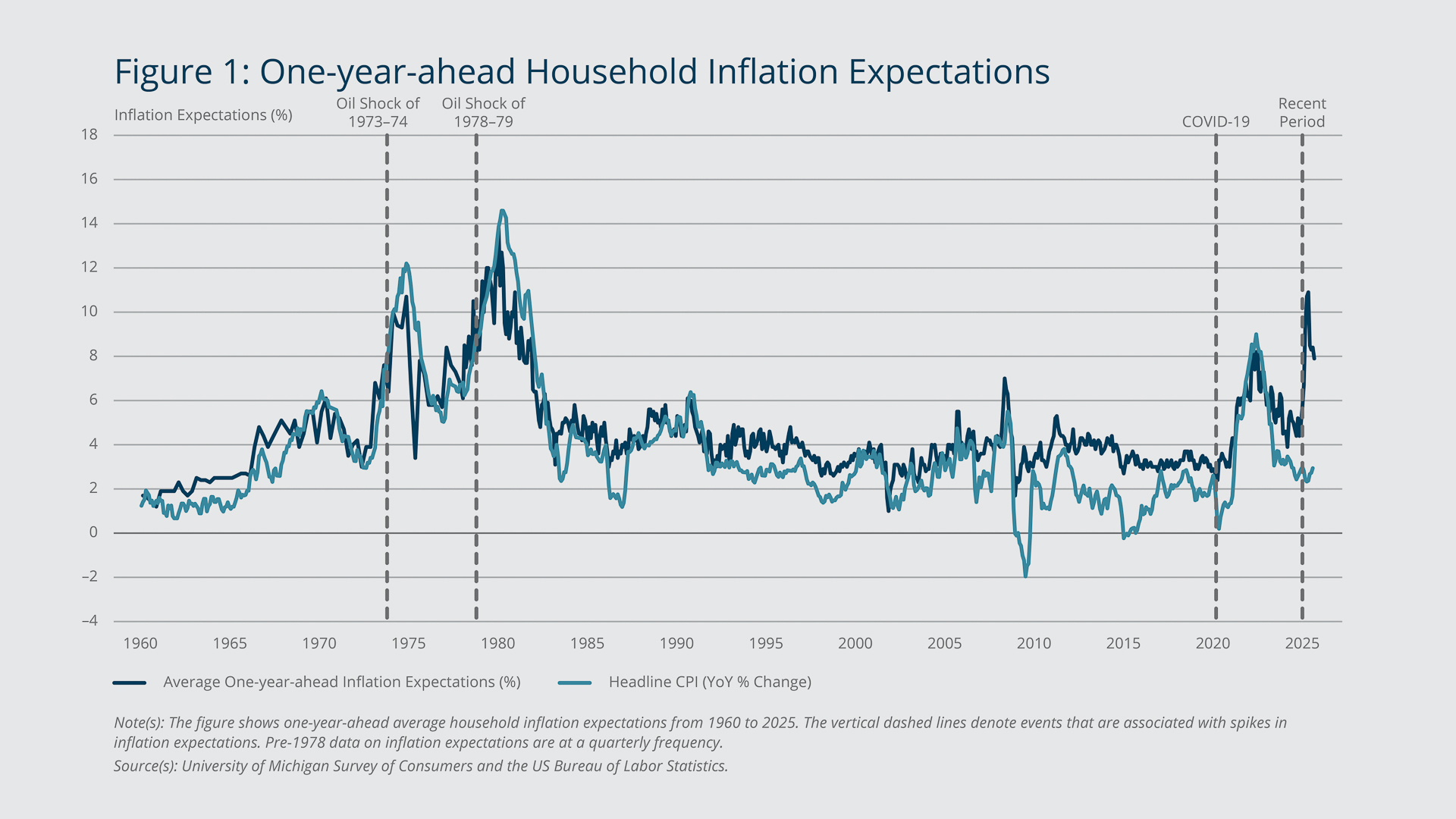

As Figure 1 shows, one-year-ahead average (mean) household inflation expectations have risen above 8 percent in four episodes since 1960. The first two occurred during the Great Inflation of the 1970s, from 1973 to 1975 and from 1978 to 1980. The third was in 2021 and 2022, during the pandemic-induced inflation surge, and the fourth began in March 2025.

{kind=link}

Federal Reserve Bank of Boston

These spikes in inflation expectations are mostly associated with commensurate surges in realized inflation that resulted partly from specific price shocks, including the oil-price shocks of the 1970s. Several studies show that household inflation expectations are strongly influenced by changes in salient prices, particularly changes in gasoline prices (Coibion and Gorodnichenko 2015) and food prices (D’Acunto et al. 2020). Consumers who buy gasoline are aware of the prices, as is anyone who sees the often large, bright signs displaying the per-gallon cost at gas stations. Food prices are seen by anyone who shops at grocery stores or dines at restaurants.

Given the connection between salient prices and household inflation expectations, we look at the extent to which the usual association between the two explains the four inflation-expectation spikes that have occurred since 1960. More to the point, we examine the extent to which the recent surge in inflation expectations reflects changes in salient prices.

Rising Salient Prices and Broad-based Inflation Do Not Fully Explain Surges in Inflation Expectations

We measure salient prices using the consumer price indexes (CPIs) for gasoline and food from the US Bureau of Labor Statistics. In addition to salient-price changes, our regression model incorporates core CPI (which excludes the often-volatile prices of food and energy) to allow for an effect of broad-based inflation on inflation expectations. We merge these CPI series with data from the University of Michigan Survey of Consumers to model how reactions to changes in salient prices and broad-based inflation during “normal times” (represented by the 1990–2019 period when prices and inflation expectations were relatively stable) have affected inflation expectations historically and in the post-pandemic period.

As noted earlier, our regression model also accounts for consumers’ recall of past prices when forming their expectations about future inflation. Recent research emphasizes the importance of recall in the formation of economic beliefs in general (Bordalo et al. 2020) and inflation expectations in particular (Weber et al. 2022, Gennaioli et al. 2024).

We describe our model and regression analysis, including our selection of variables and how we model memory recall, in detail in the appendix accompanying this brief.

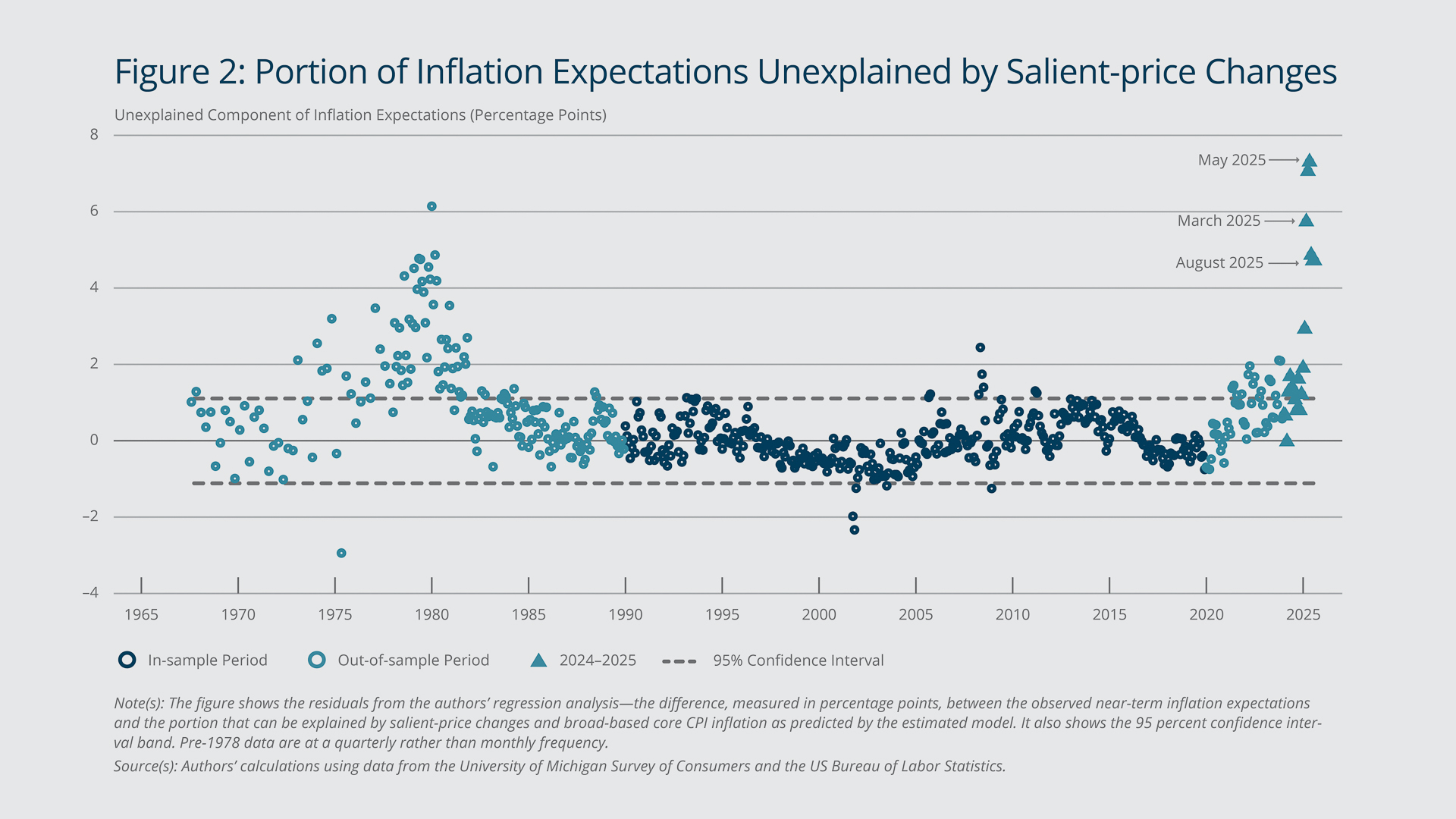

Figure 2 shows the residuals from our regression analysis—the portion (measured in percentage points) of the observed near-term inflation expectations that cannot be explained by salient-price changes and broad-based core CPI inflation as predicted by our estimated model. It also shows the 95 percent confidence interval, that is, the range of values of this unexplained component in inflation expectations that, according to our model estimates, should be observed with 95 percent confidence.

{kind=link}

Federal Reserve Bank of Boston

As the figure illustrates, each of the four spikes in one-year-ahead average inflation expectations observed since the 1970s is associated with a large unexplained component, which is above the 95 percent confidence interval: Although prices increased during those episodes, the surges in inflation expectations were much larger than what would be predicted by the usual effect of salient-price changes and underlying core inflation that characterize the three decades of relatively stable inflation expectations preceding the pandemic.

However, there are noteworthy differences among the four surges. The 1973–1975 surge in inflation expectations is associated with residuals that peak at slightly more than 3 percentage points. But the spike in expectations was relatively short lived.

The 1978–1980 episode is associated with a much more protracted period in which the unexplained increase in inflation expectation peaked even higher above the 95 percent confidence interval, at about 6 percentage points, consistent with the fact that expectations were more de-anchored in the late 1970s than in the early 1970s.

During the 2021–2022 episode, residuals also rose above the 95 percent confidence interval but only for a short period and to a lesser degree than in the 1970s; the unexplained portion was limited to about 2 percentage points. The anchoring of inflation expectations was tested during that episode, but, as monetary policy tightened swiftly in 2022 and 2023, expectations quickly returned to a more normal range of fluctuations given the movement in salient prices and broad-based inflation.

By contrast, starting in March 2025, we see a sudden and large increase in households’ near-term inflation expectations —more than 7.5 percentage points—that is not related to the usual drivers. While that unexplained increase receded notably over the summer, it is still unusually large, as it remains clearly above the 95 percent confidence interval.

How Much Salient Prices and Broad-based Inflation Have Contributed to the Inflation Expectation Surges

Our regression model also enables us to estimate the degree to which increases in salient prices and broad-based inflation explain changes in inflation expectations during the four episodes of heightened price instability observed since the 1970s.

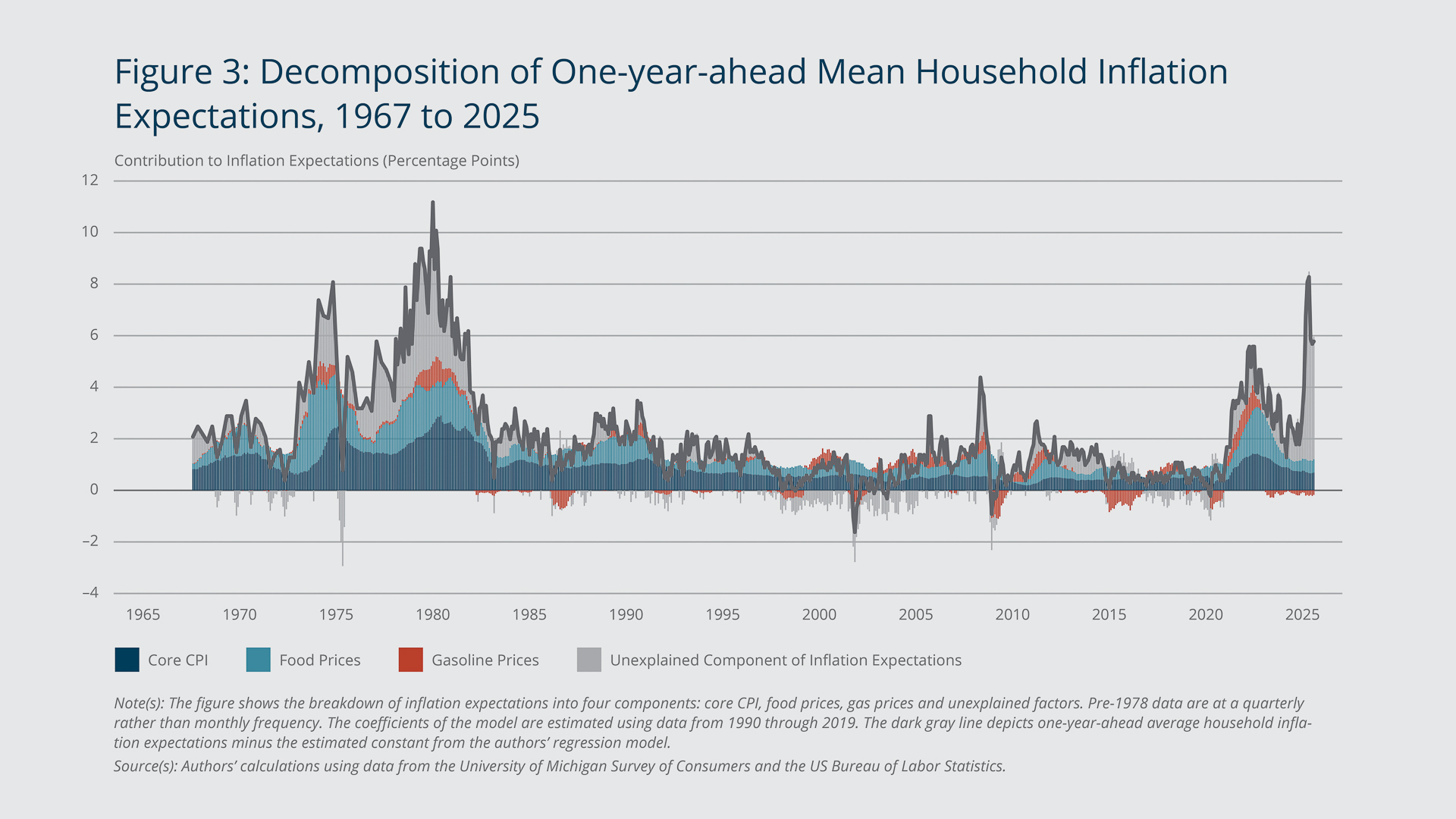

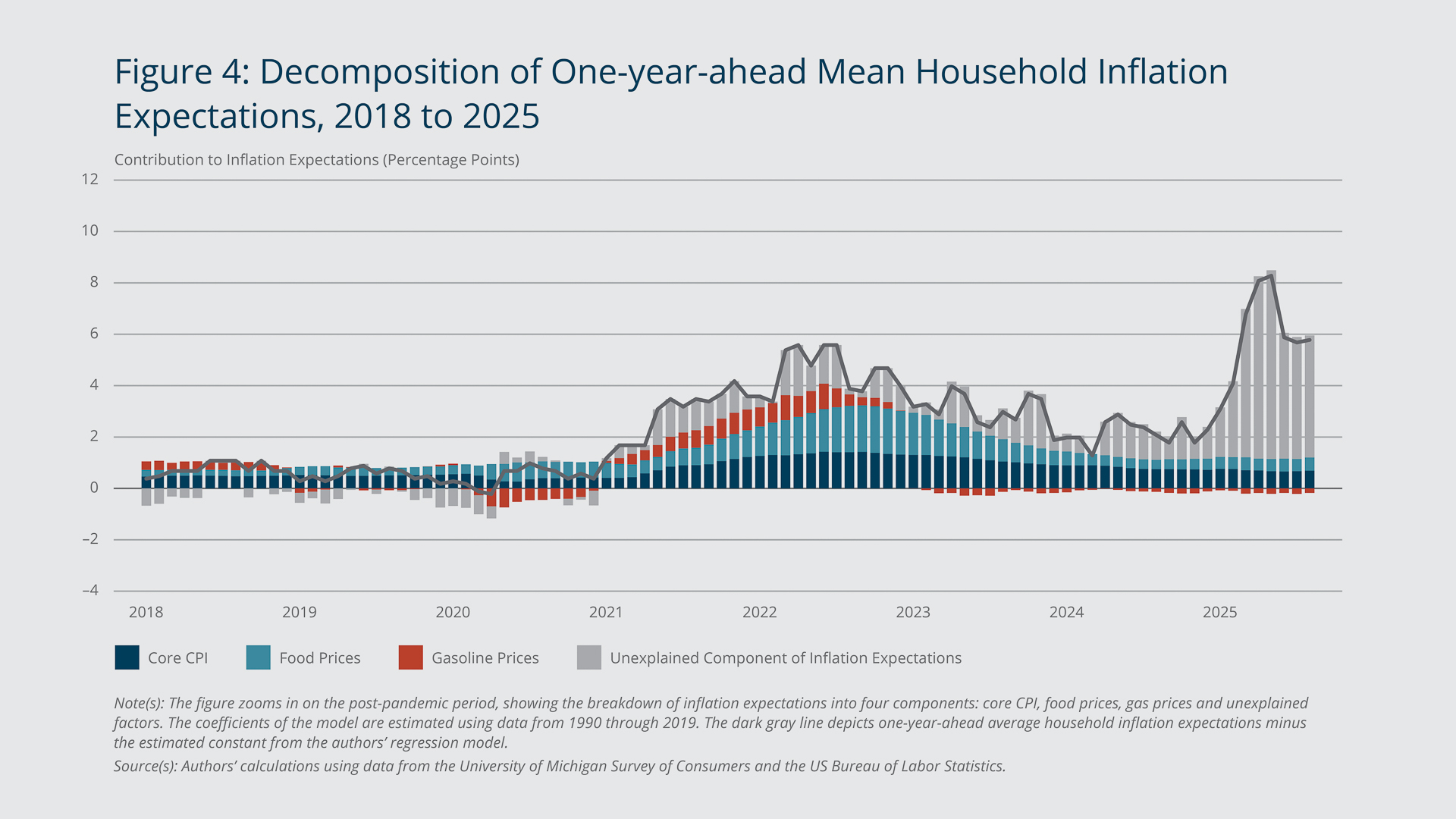

Figure 3 complements the preceding analysis by showing the individual contributions of the different drivers of fluctuations in one-year-ahead average household inflation expectations. Note that the figure depicts fluctuations from an average level (of about 2.5 percent) that would have been observed had prices remained stable during the 1990–2019 normal-time period. By contrast, Figure 1 shows just the levels of inflation expectations. This distinction explains why the spikes in Figure 3 are not as high as the spikes in Figure 1.

{kind=link}

Federal Reserve Bank of Boston

In the two surges of the 1970s, gasoline prices, which are directly affected by oil-price shocks, contributed about 1 percentage point to the fluctuation from the normal-time average, while food prices and broad-based inflation each accounted for about 2 percentage points. Overall, these drivers of inflation expectations explain about 5 percentage points of the 1970s surges.

We can use these contributions to compute the shares of the surges above the usual average level that salient prices and broad-based inflation can explain. Comparing the decade’s two episodes, we see that during the 1973–1975 surge, nearly 3 percentage points were unexplained, indicating that salient prices and broad-based inflation explain close to two-thirds of the increase at its 8 percentage point peak above the normal-time average. But in the 1978–1980 surge, the unexplained portion accounted for more than 5 percentage points, indicating that about one-half of the 11 percentage point peak above the normal-time average was due to unexplained factors.

Figure 4 illustrates the same analysis as Figure 3 but zooms in on the post-pandemic period. It shows that in 2021 and 2022, sharp increases in gasoline prices, food prices, and underlying inflation together contributed about 4 percentage points to the surge, while unexplained factors contributed to 2 percentage points. In other words, about two-thirds of the period’s 6 percentage point peak increase in inflation expectations above the normal-time average can be explained by households observing changes in salient prices and increased broad-based inflation. By contrast, changes in the salient prices and underlying inflation explain little—less than 1 percentage point—of the most recent surge, leaving about 7.5 percentage points unexplained at the 8 percentage point peak. Indeed, unexplained factors have played a much larger role than usual.

{kind=link}

Federal Reserve Bank of Boston

This increase in the unexplained component could be partly attributable to tariff-related price uncertainty. The University of Michigan publicly released an analysis using the Survey of Consumers that shows inflation expectations were closely related to perceptions about tariff policies at the beginning of 2025 (University of Michigan 2025). Still, the observed increase in inflation expectation remains far larger than the estimated inflationary impact that the new tariffs would imply. For example, depending on the trade policy scenario, Barbiero and Stein (2025) estimate that new tariffs could add about 0.8 to 2.2 percentage points to inflation, well below the 8 percentage point increase observed in the Michigan Survey of Consumers measure of inflation expectations.

Endnotes

- Such risk of de-anchoring appears to be contained so far. Indeed, in contrast to what occurred in the late 1970s, most measures of longer-term inflation expectations have remained broadly stable around levels consistent with a return to the Federal Reserve’s 2 percent inflation target. Moreover, the increase in near-term inflation observed in other surveys of household inflation expectations is more muted compared with the Michigan Survey of Consumers.

References

Barbiero, Omar, and Hillary Stein. 2025. “The Impact of Tariffs on Inflation.” Federal Reserve Bank of Boston Current Policy Perspectives 25-2.

Bordalo, Pedro, Nicola Gennaioli, and Andrei Shleifer. 2020. “Memory, Attention, and Choice.” Quarterly Journal of Economics 135(3): 1399–1442.

Coibion, Olivier, and Yuriy Gorodnichenko. 2015. “Is the Phillips Curve Alive and Well after All? Inflation Expectations and the Missing Disinflation.” American Economic Journal: Macroeconomics 7(1): 197–232.

Coibion, Olivier, and Yuriy Gorodnichenko. 2025. “Inflation, Expectations and Monetary Policy: What Have We Learned and to What End?” National Bureau of Economic Research Working Paper 33858.

D’Acunto, Francesco, Ulrike Malmendier, Juan Ospina, and Michael Weber. 2021. “Exposure to Grocery Prices and Inflation Expectations.” Journal of Political Economy 129(5): 1615–1639.

Gennaioli, Nicola, Marta Leva, Raphael Schoenle, and Andrei Shleifer. 2024. “How Inflation Expectations De-anchor: The Role of Selective Memory Cues.” NBER Working Paper 32633.

Reis, Ricardo. 2023. “Four Mistakes in the Use of Measures of Expected Inflation.” AEA Papers and Proceedings 113: 47–51.

University of Michigan. 2025. Survey of Consumers Featured Charts.

Weber, Michael, Francesco D’Acunto, Yuriy Gorodnichenko, and Olivier Coibion. 2022. “The Subjective Inflation Expectations of Households and Firms: Measurement, Determinants, and Implications.” Journal of Economic Perspectives 36(3): 157–184.

About the Authors

About the Authors

Philippe Andrade,

Federal Reserve Bank of Boston

Philippe Andrade is a vice president and economist in the Federal Reserve Bank of Boston Research Department.

Email: Philippe.Andrade@bos.frb.org

Michael Wicklein is a PhD student in public policy at the University of Chicago Harris School of Public Policy. He was a senior research associate in the Federal Reserve Bank of Boston Research Department when he coauthored this brief.

Acknowledgments

The authors thank Giovanni Olivei, Jenny Tang, and Egon Zakrajšek for their constructive feedback. Maxwell Cozean provided excellent research assistance.

Resources

Site Topics

Keywords

- inflation expectations ,

- inflation ,

- de-anchoring ,

- Great Inflation of the 1970s ,

- post-COVID inflation ,

- survey of households

JEL Codes

- D83 ,

- E31

Citation

Andrade, Philippe, and Michael Wicklein. 2025. “Why Have Inflation Expectations Surged Recently? A Historical Perspective.” Federal Reserve Bank of Boston Current Policy Perspectives 25-14.