Shaping the Future of Work: Workers’ Optimism and Pessimism about AI

{kind=link}

Federal Reserve Bank of Boston

The views expressed herein are solely those of the authors and should not be reported as representing the views of the Federal Reserve Bank of Boston, the principals of the Board of Governors, or the Federal Reserve System.

The artificial intelligence (AI) revolution is here and is expected to transform the labor market, creating new opportunities for some workers while eliminating the jobs of others. We surveyed a sample of US household heads working in different industries and with different educational backgrounds to better understand how they view AI and its potential effects on their job prospects and financial well-being.

The survey was conducted in December 2024 as a special component of the Federal Reserve Bank of New York Survey of Consumer Expectations (SCE), a nationally representative, internet-based, monthly survey of a rotating panel of approximately 1,300 household heads.1 Our survey asked participants questions concerning their expectations about AI for the following year (2025) and for the next one to five years (through 2029).

Sign up for Research Department Updates.

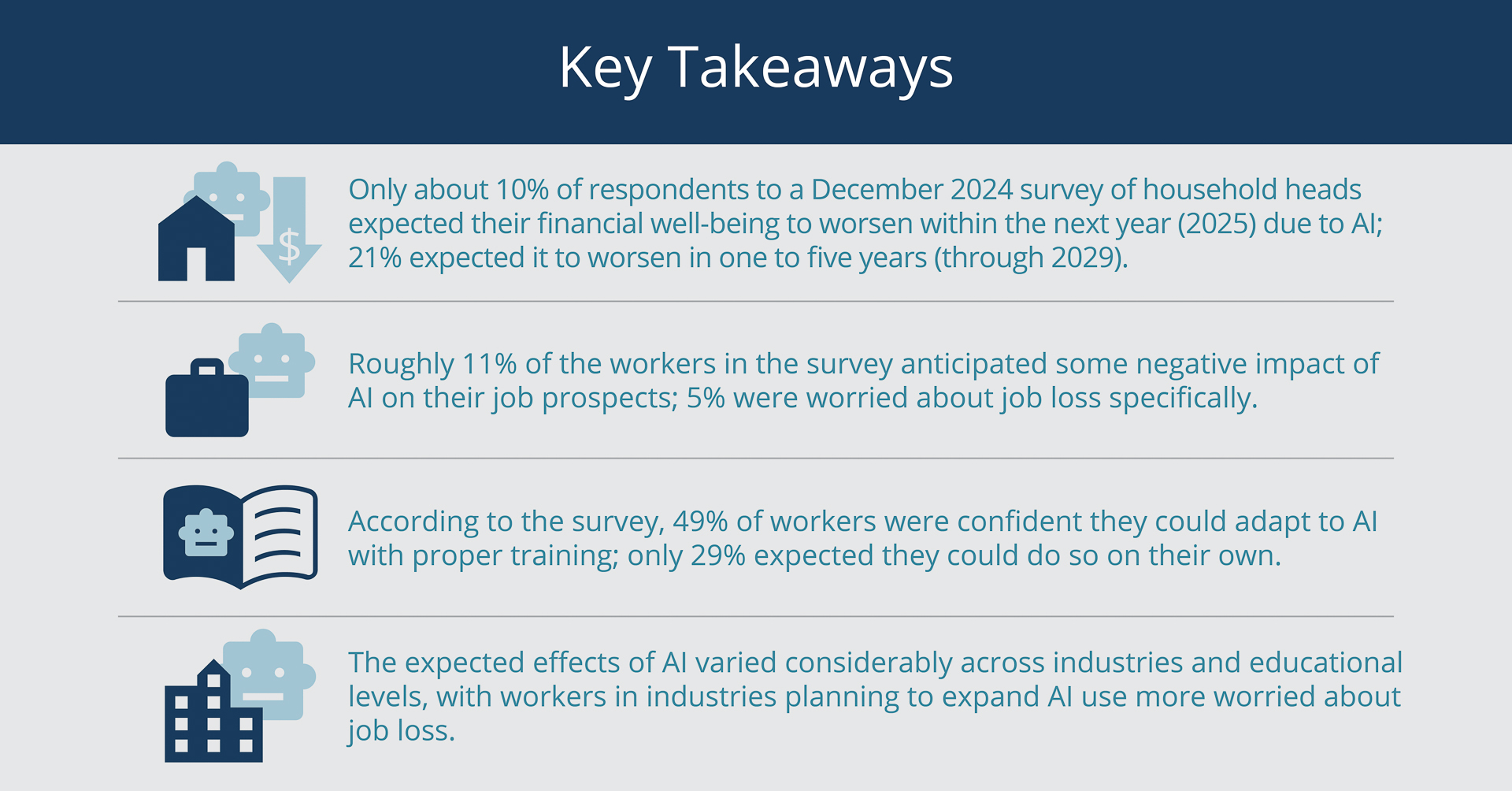

The findings indicate that at the time of the survey, most workers were not immediately worried about AI-driven job loss—which is consistent with an August 2025 New York Fed survey showing that few firms had laid off workers due to AI (Abel et al. 2025). However, about 21 percent of the survey respondents expected that AI would cause their financial situation to worsen within one to five years.

Overall, the survey results suggest that while widespread worry about AI-driven job loss had not yet materialized at the end of last year, many workers anticipated worsening financial conditions and disruption in their industries.

The responses varied substantially across industries and education levels. In general, workers who are more educated expected greater boosts to productivity due to AI. Workers with high school diplomas or undergraduate or master’s degrees indicated that they were somewhat worried about AI hurting their job prospects, whereas workers with doctorate degrees did not expect any adverse employment effects.

Respondents employed in leisure services (which includes jobs in arts and entertainment as well as in hotels and restaurants) and consumer services (which includes information-services positions such as librarians and cloud computing professionals as well as jobs in finance, insurance, and real estate) were the most worried about their job prospects due to AI.

The survey results also suggest a strong interest in AI training opportunities among workers. Forty-nine percent of the workers in our survey indicated that they could adjust to AI technology with proper training, while only about 29 percent expressed confidence that they could do so on their own.

AI Worries May Be Driving Longer-term Overall Concerns about Financial Well-being

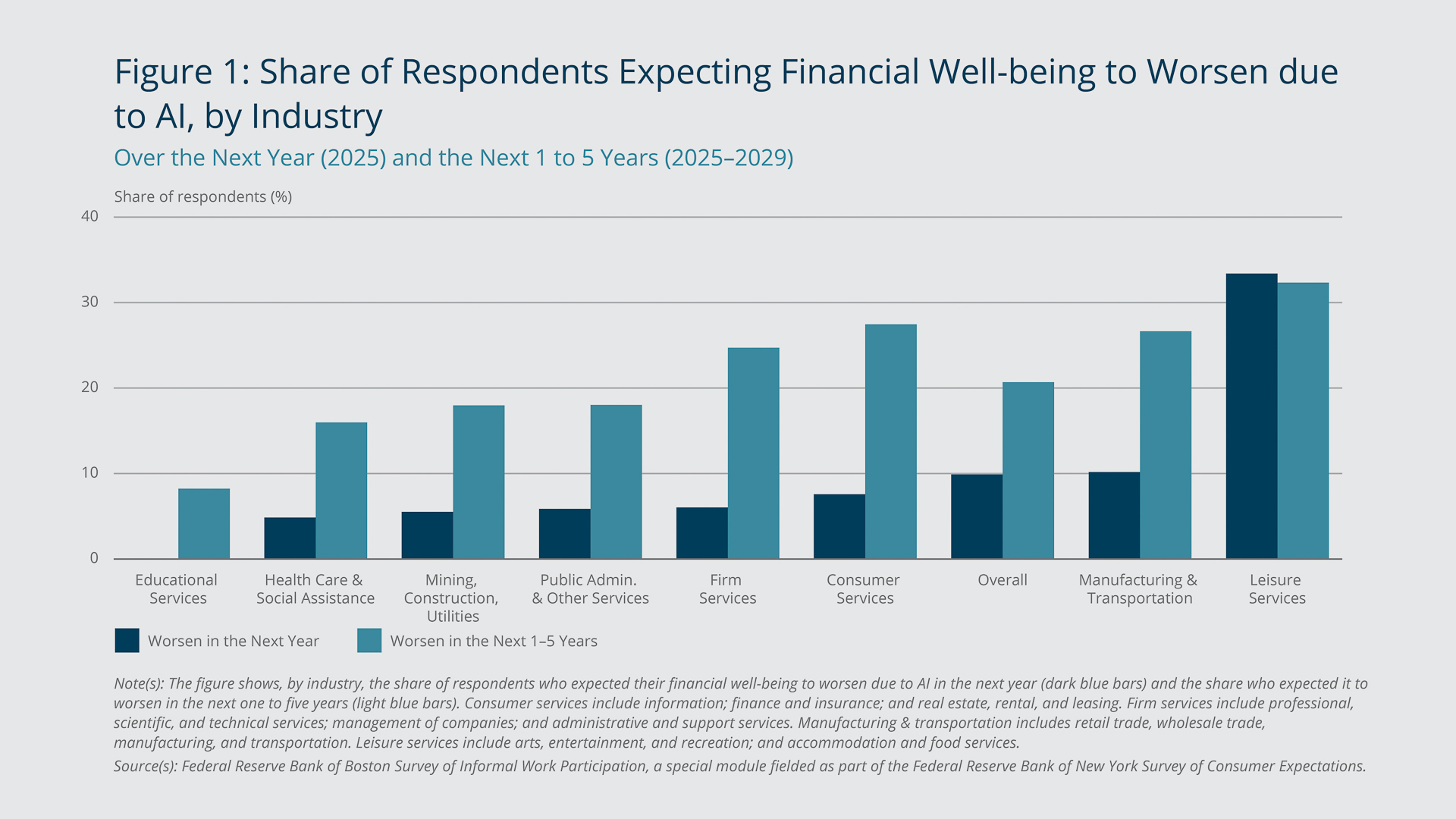

At the time of the survey, AI’s potential negative impact on household finances was more of a longer-term concern. When asked, “Do you think that AI will affect your financial well-being in the next year (12 months)?” roughly 10 percent of the respondents said they expected their household finances to deteriorate. However, the share expecting to be worse off financially in the next one to five years due to AI was twice as large, about 20 percent.

The University of Michigan Surveys of Consumers (MSC), a monthly representative survey of US households, also asks participants about their one-year and five-year outlooks for household finances, but it doesn’t tie those expectations to specific factors.

We compare the results from our survey and the MSC to gain insight into the extent to which concerns about AI could be a prominent driver of general pessimism about financial well-being. In the December 2024 MSC, the share of respondents who thought they would be worse off financially in the next year (2025) was 24 percent, versus the 10 percent of our survey’s respondents who were pessimistic about their financial well-being in the next year due specifically to AI.

Regarding financial well-being in the next five years (through 2029), the level of AI-related pessimism in our survey was nearly as high as the pessimism in the MSC. In the December 2024 MSC, 22 percent of respondents indicated that they expect to be worse off in five years. In our survey, the corresponding share was 21 percent. (All respondents in our survey who expected to be worse off in one to five years also expected to be worse off within one year.) The latter result is consistent with AI being a major factor contributing to the longer-term negative outlook captured in the MSC.

Concern about AI Varies by Industry and Education Level

When we look at the share of respondents who expressed worry about their financial well-being due to AI by industry and by education, we find notable heterogeneity. Figure 1 shows the contrast between, for example, educational services, where no respondents expressed worry about the short-term impact of AI, and leisure services, where more than 30 percent of workers were concerned about their financial well-being, for both the short term and longer term.

{kind=link}

Federal Reserve Bank of Boston

The share of respondents worried about their financial well-being due to AI also varied by educational level. As noted, the most educated respondents were the most optimistic—or the least worried. Only 5 percent of respondents with doctorates expressed concern that their financial well-being would worsen within the next year compared with 10 percent of all respondents. And only about 9 percent of doctorate holders were worried about the next one to five years versus 21 percent of all respondents. These results come with the caveat that doctoral graduates comprise a small group in our survey, as they do in the general population.

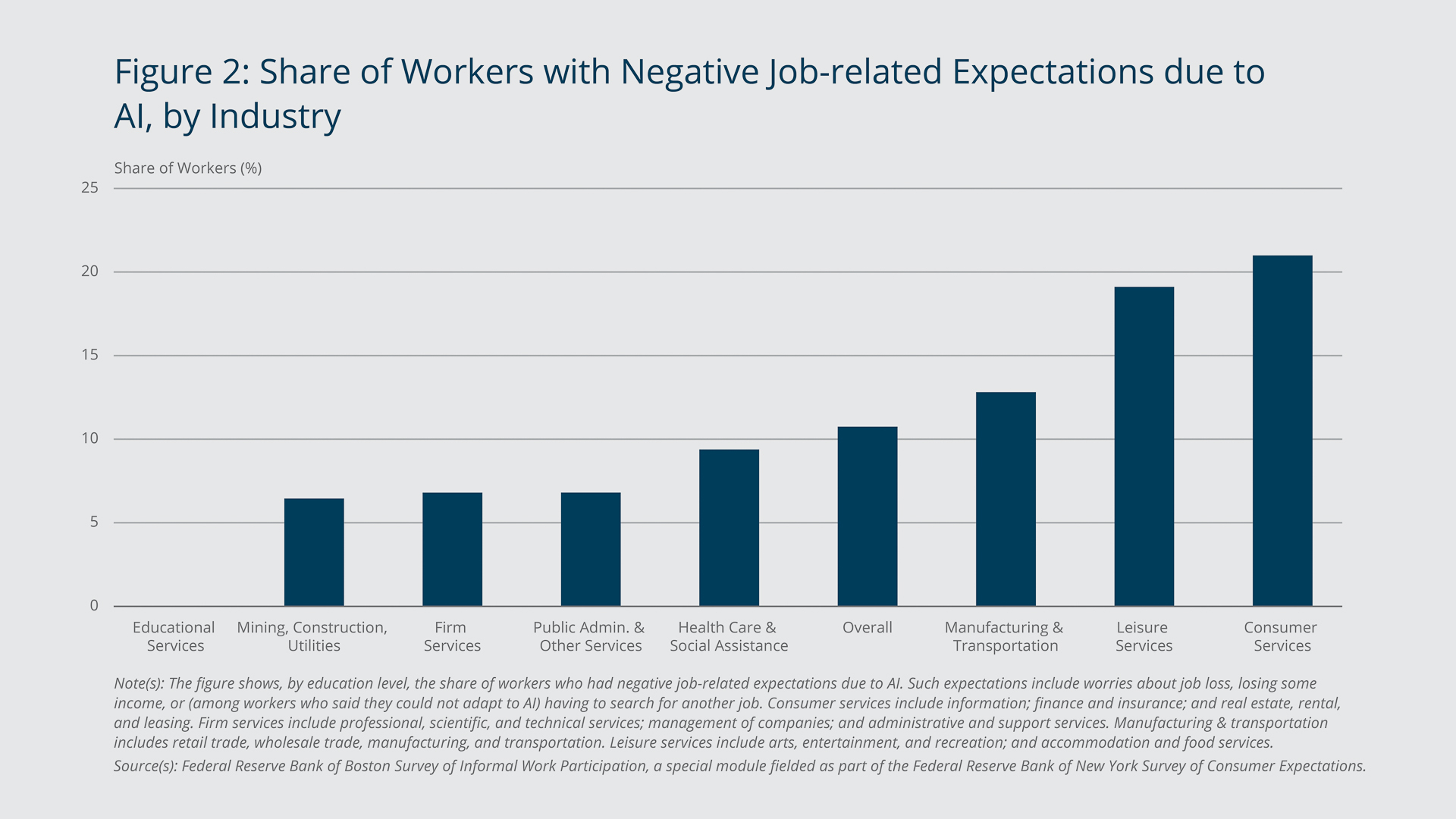

By asking workers—survey respondents who indicated they are employed—how they thought AI would affect their job, our survey provides insight into why respondents were expecting their financial well-being to worsen. The results show that close to 11 percent of workers were worried about the effects of AI on their job; that is, they expected that they would lose their job, lose some income, or have to search for another job. We consider the last of those three responses—having to search for another job—as reflecting worry only if the respondent also indicated that they did not believe they could adjust to AI on their own.

The share of workers who were worried about experiencing a negative job outcome varied substantially across industries. As Figure 2 shows, it ranged from 0 percent in education services to more than 20 percent in consumer services. The worried-worker share was similar across education levels, at about 10 to 13 percent, except for the highest level; workers with a doctorate indicated that they had no worries at all.

{kind=link}

Federal Reserve Bank of Boston

Fearing Less Job Security or Expecting More Opportunities

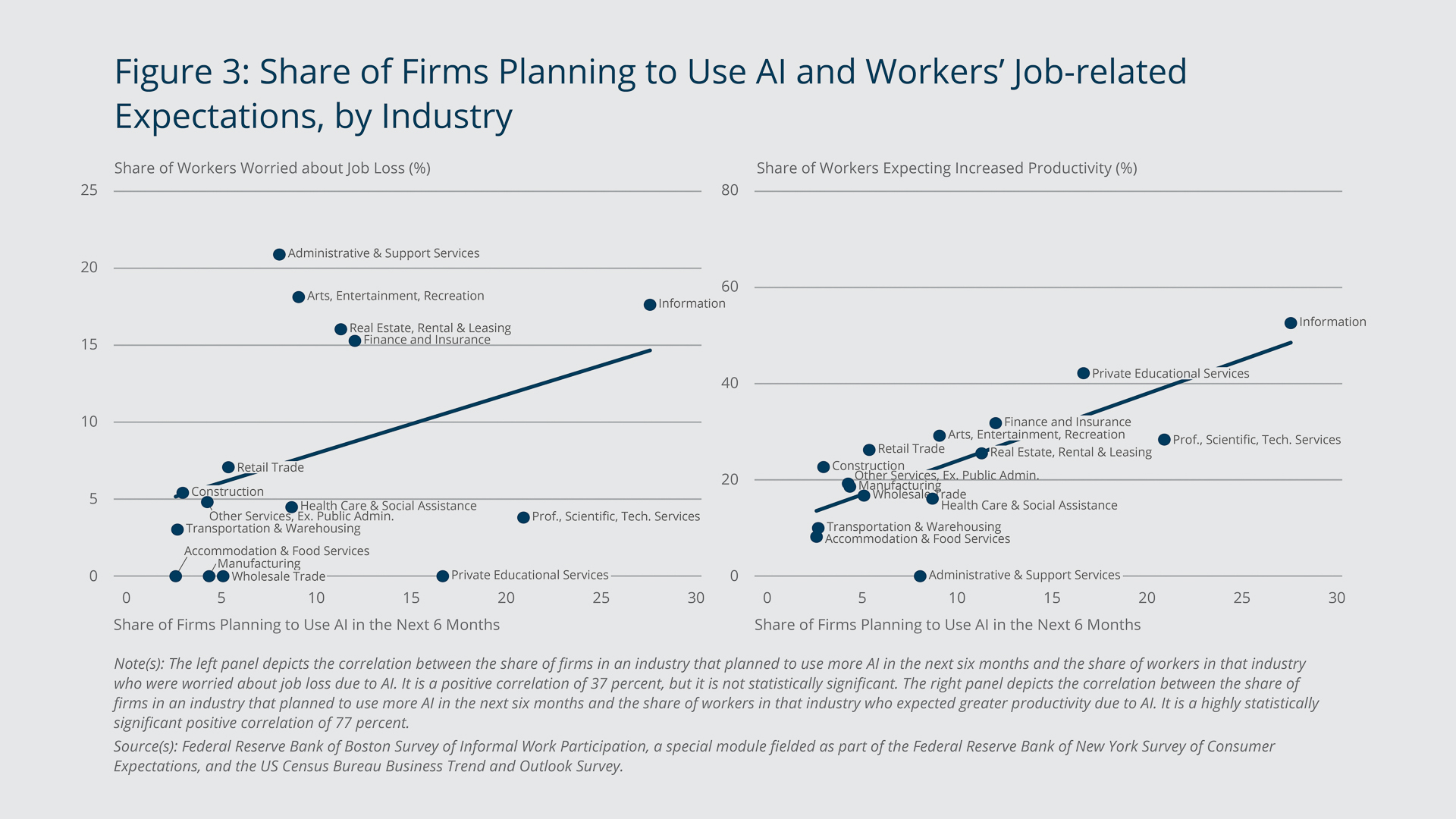

To gain further insight into the reasons for workers’ worries, we examine job loss specifically and find that 5 percent of workers surveyed were worried about losing their job due to AI. For comparison, consider that 6 to 7 percent of MSC respondents, taking that survey the same month our survey was conducted (December 2024), indicated that they thought they had a better-than 50 percent chance of losing their job in the next five years for any reason. A more granular study of our survey results reveals that the specific industries with the largest worried-worker shares were administration (21 percent), arts and entertainment (18 percent), information (18 percent), real estate (16 percent), and finance and insurance (15 percent).

Notably, the share of workers who were worried about job loss due to AI is positively related to the share of firms in their industry that expected greater use of AI in the next six months, as reported in the Business Trend and Outlook Survey (BTOS)2 conducted in late 2024, about the same time that our survey was administered. This relationship is apparent in the left panel of Figure 3, which, using results from the BTOS and our survey, plots the share of firms in an industry that were planning to use more AI in the next six months with the share of workers in that industry who were worried about job loss due to AI. Using the most granular industry information to increase statistical power, the figure depicts a positive correlation of 37 percent, but the correlation is statistically insignificant.3

{kind=link}

Federal Reserve Bank of Boston

Collectively, the results from the two surveys indicate that while overall worry about job loss due to AI did not seem to be acute at the end of last year, the intensity varied across industries and related mildly to the extent to which an industry planned to use AI.

While many workers in our survey were worried about how AI could affect their job, others indicated that they expect it will bring increased productivity and new opportunities; 22 percent of workers anticipated boosts to productivity, and 10 percent expected to have new AI-driven job or business opportunities.

As with pessimism about AI, optimism varied substantially across industries. The shares of workers expecting AI-related productivity boosts were the largest in information (53 percent), private educational services (42 percent), and finance and insurance (32 percent). Expectations of greater productivity are related positively to the share of an industry’s firms that expected to use more AI in the next six months, as recorded in the BTOS at the end of 2024. This relationship is seen in the right panel of Figure 3. The correlation is strong at 77 percent, and it is highly statistically significant.4

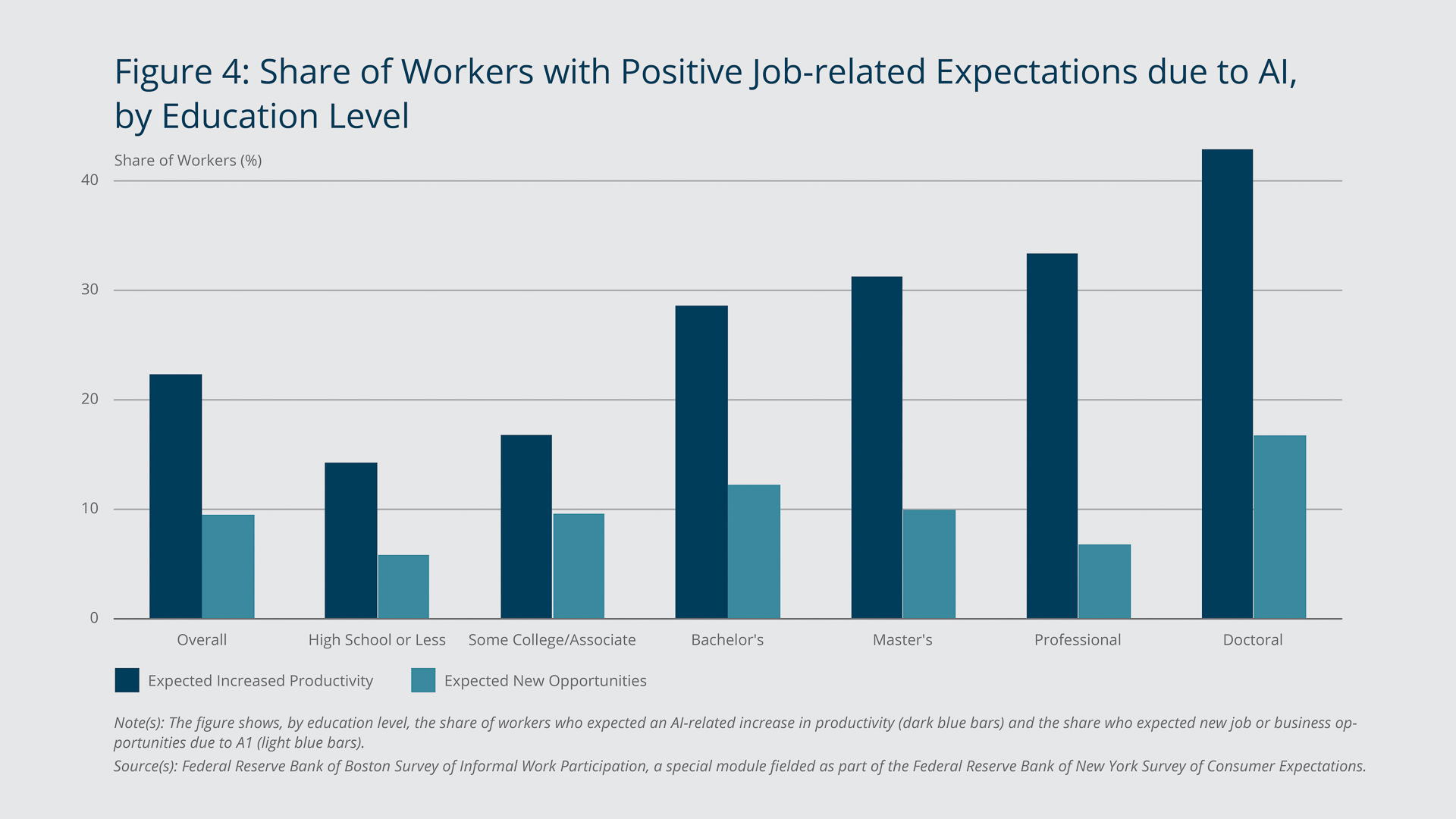

As Figure 4 shows, optimism about AI also varied by academic background, with the share of workers expecting a productivity boost increasing monotonically with workers’ education level. Expectations of increased productivity rise from about 14 percent among workers with a high school diploma or less to 29 percent among holders of bachelor’s degrees to 43 percent among doctorate holders. The share of workers with a professional degree who expected a productivity boost was 33 percent, which is similar to the share of workers with a master’s degree (31 percent) who expected a productivity gain.5

{kind=link}

Federal Reserve Bank of Boston

The difference in expectations across education levels highlights the potential importance of targeted skill-development policies, which could help ensure that productivity gains from AI adoption are broadly shared.

The Need for AI Training

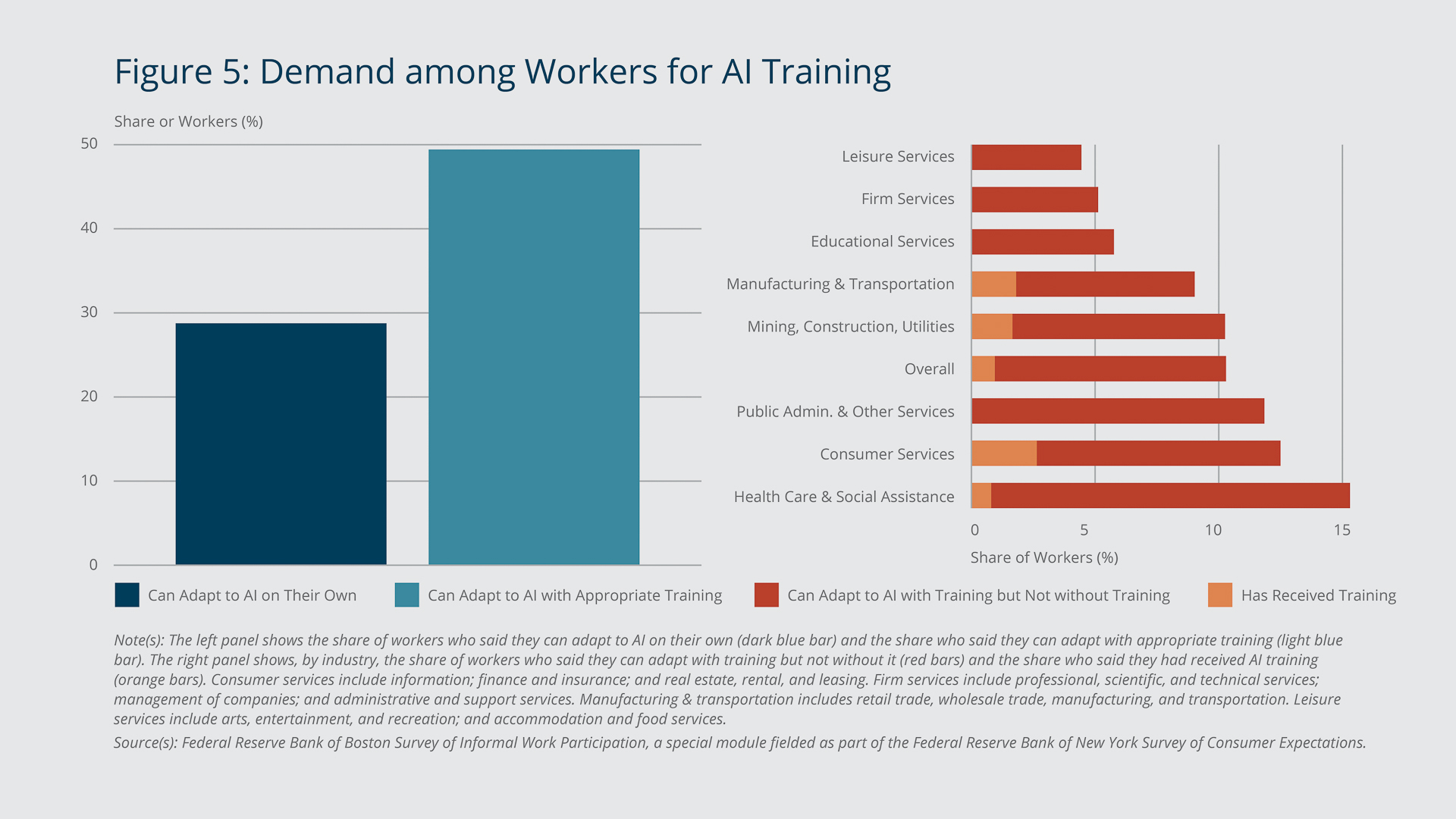

Across industries, workers emphasized a need for training to adapt to AI-driven changes. Less than 29 percent of workers in our survey said they can adjust to AI on their own, and 49 percent said they are confident they can adjust to the new technology with proper training (see the left panel of Figure 5). Further examining this demand for AI preparedness on an individual basis enables us to identify workers who need training to adjust: About 10 percent of workers in our survey indicated they are both confident they can adapt with proper training and do not believe they can do so without training. Only a small minority of those 10 percent had received training (see the right panel of Figure 5). This individually perceived training gap varies by industry, and it is largest in health care and social assistance, where 15 percent of workers said they will be unable to adapt to AI without proper training (right panel of Figure 5).

{kind=link}

Federal Reserve Bank of Boston

The results from the survey questions about actual training, when paired with the BTOS results, show that the larger the share of firms in an industry that expected to adopt more AI technology, the larger the share of workers in that industry who had received some training (a positive yet statistically insignificant correlation of 46 percent).6

Addressing workers’ demand for training may ease the adjustment to using AI, reduce mismatches between businesses’ adoption of AI and workers’ preparedness to work with the technology, and ultimately promote more broad-based positive economic outcomes.

Endnotes

- The analysis in this brief uses results from the Federal Reserve Bank of Boston Survey of Informal Work Participation, a special module fielded as part of the Federal Reserve Bank of New York Survey of Consumer Expectations.

- The BTOS is a US Census Bureau survey conducted to capture key economic data as well as expectations about future business conditions. The BTOS sample consists of approximately 1.2 million businesses split into six rotating panels (approximately 200,000 cases per panel), with businesses in each panel surveyed once every 12 weeks for a year.

- The p-value associated with this correlation is 0.18, which means that even if there is no real relationship between the share of firms and the share of workers, there is still an 18 percent chance of observing one as strong as or stronger than the one we observe. Therefore, the correlation is not considered statistically significant. The highest possible value for a correlation is 100 percent, which would be represented in the figures by all the points lining up in a diagonal line. Instead, we see a meaningful amount of statistical noise around this relationship.

- The p-value associated with this correlation is 0.001, which, again, means that if there is no real relationship between the share of firms and the share of workers, the chance of observing one as strong as or stronger than the one we observe is 0.1 percent—very unlikely.

- Our finding that worker optimism rises with educational attainment aligns with recent studies’ arguments that AI technology is seniority-biased (Brynjolfsson et al. 2025; Lichtinger and Hosseini 2025), as workers with higher educational attainment often hold more senior positions.

- The p-value associated with this correlation is 0.25.

References

Abel, Jaison R., Richard Deitz, Natalia Emanuel, Ben Hyman, and Nick Montalbano. 2025. “Are Businesses Scaling Back Hiring Due to AI?” Federal Reserve Bank of New York Liberty Street Economics blog. September 4, 2025.

Brynjolfsson, Erik, Danielle Li, and Lindsey Raymond. 2025. “Generative AI at Work.” The Quarterly Journal of Economics 140(2): 889–942.

Lichtinger, Guy, and Seyed Mahdi Hosseini Maasoum. 2025. “Generative AI as Seniority-biased Technological Change: Evidence from U.S. Resume and Job Posting Data.” Working paper.

About the Authors

About the Authors

Anat Bracha,

Federal Reserve Bank of Boston

Anat Bracha is the academic director of the Financial Economics program and an associate professor in the Banking and Finance Department at the Hebrew University Business School. She is also a visiting scholar with the Federal Reserve Bank of Boston Research Department.

Email: Anat.Bracha@mail.huji.ac.il

Jenny Tang,

Federal Reserve Bank of Boston

Jenny Tang is a vice president and economist in the Federal Reserve Bank of Boston Research Department.

Email: Jenny.Tang@bos.frb.org

Acknowledgments

The authors thank Rees Hagler for excellent assistance with the data and figures.

Resources

Site Topics

Keywords

- household survey ,

- Artificial Intelligence ,

- AI ,

- financial well-being ,

- labor market perceptions ,

- Worker training

JEL Codes

- C83 ,

- D84 ,

- O33 ,

- J24 ,

- E24

Citation

Bracha, Anat, and Jenny Tang. 2025. “Shaping the Future of Work: Workers’ Optimism and Pessimism about AI.” Federal Reserve Bank of Boston Current Policy Perspectives 25-16.