New England Economic Conditions through October 7, 2025

Key Takeaways

- Payroll employment growth in New England slowed significantly in 2025, driven by deceleration in both the education and health services sector and the government sector. The softened labor demand was reflected in reduced hiring activity, creating additional challenges for unemployed workers who faced fewer job openings and lower rates of finding employment.

- Year-over-year inflation in New England surpassed the national rate for the 16th consecutive month in August 2025. Shelter costs continued to be the primary driver of the region’s more elevated inflation.

- Due to a deteriorating outlook on future economic conditions, consumer confidence in New England declined in the first eight months of 2025 relative to the levels observed during the previous three years.

Sign up for new research and data on the New England economy.

Payroll Employment

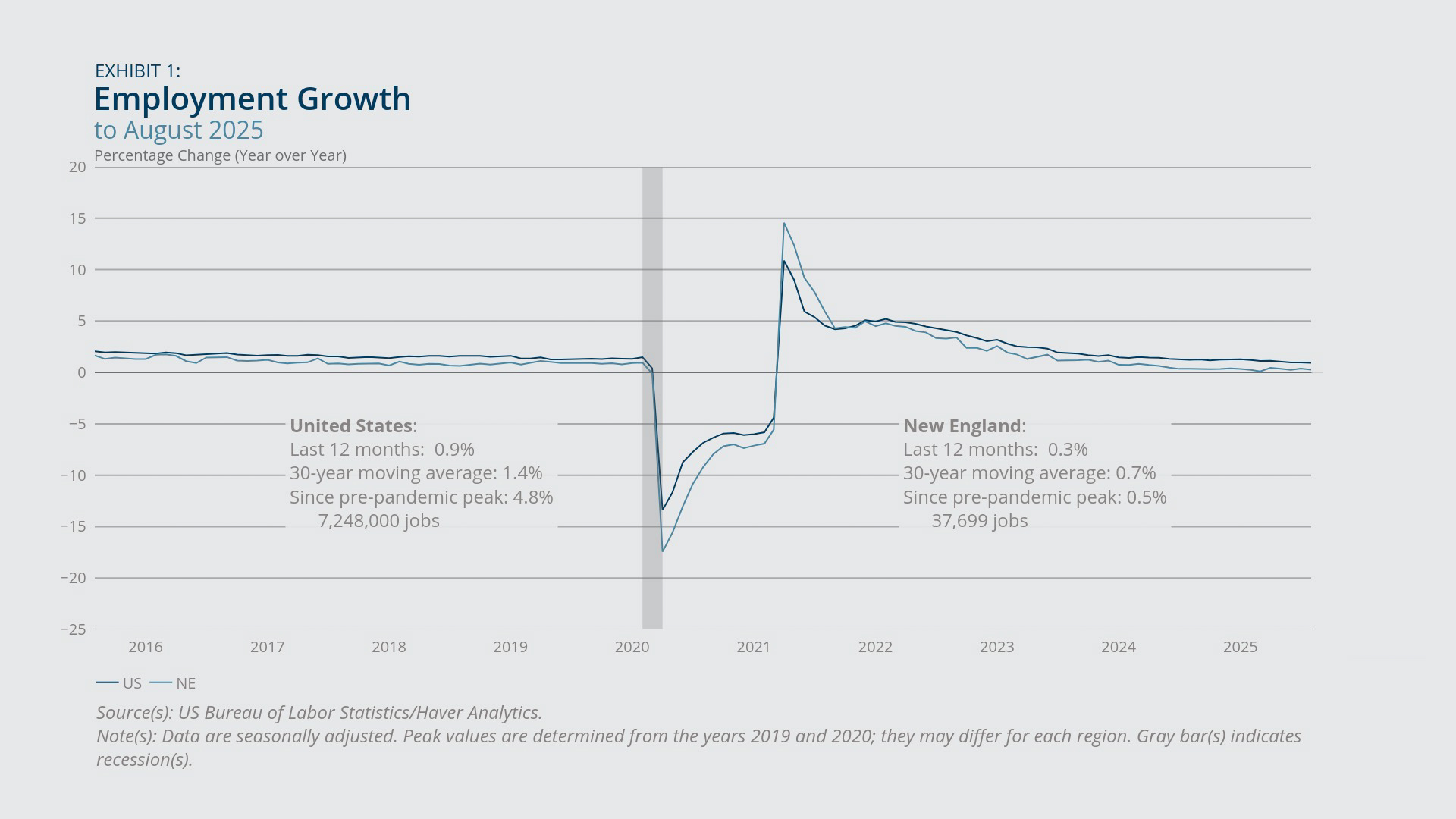

- The August 2025 year-over-year payroll employment growth rates for New England and the United States both are among the slowest since 2011, excluding the COVID-19 pandemic period of widespread net job losses.

- New England’s recent employment stagnation can be attributed primarily to slowing growth in education and health services sector and the government sector—the same two sectors that sustained the region’s growth in 2024.

In August 2025, total nonagricultural payroll employment grew 0.9 percent year-over-year for the United States and 0.3 percent for New England (Exhibit 1). Those growth rates are among the slowest since June 2011, excluding the March 2020–March 2021 period, when the region and the country both saw net job losses due to the COVID-19 pandemic. Note that the August rates are subject to further revision when the US Census Bureau adjusts its employment estimates as more comprehensive administrative data become available. In the preliminary benchmark revision released by the US Census Bureau in September 2025, payroll employment for March 2025 was revised down by 911,000 jobs (–0.6 percent) for the United States and 8,500 jobs (–0.1 percent) for New England.1 When incorporating these revisions, the year-over-year growth rates for the 12-month period ending in August 2025 drop further to 0.6 percent nationwide and 0.2 percent for the region.

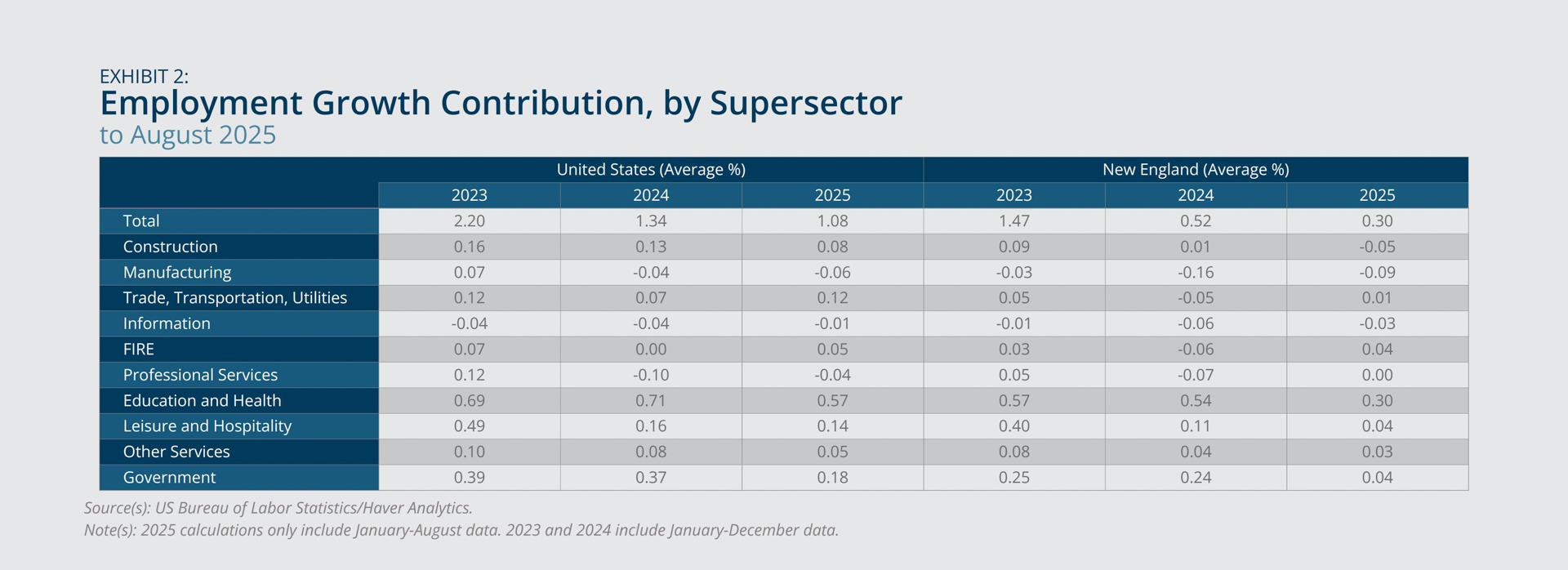

In New England, the deceleration of payroll employment growth since 2024, following a robust recovery period when the economy rebounded from pandemic-related job losses, was driven by distinct changes in sectoral growth patterns. Exhibit 2 illustrates these changes by comparing sectoral contributions to the average 12-month total employment growth rate across 2023, 2024, and the first eight months of 2025. In 2024, most sectors experienced stagnation or contraction in employment levels, with only the education and health services sector and the government sector maintaining strong growth comparable to their 2023 rates. Jobs created by these two sectors sustained the region’s positive overall employment growth that year. However, in 2025, both of these previously resilient sectors saw significant slowdowns. Although employment declines moderated in other sectors, including manufacturing, financial activities, and professional and business services, the recovery was insufficient to offset the diminished growth in the education and health services sector and the government sector, resulting in an overall stagnation in the region’s employment.

{kind=link}

Federal Reserve Bank of Boston

{kind=link}

Federal Reserve Bank of Boston

Unemployment and Labor Force Participation Rate

- Reflecting the slowdown in job creation, New England’s unemployment rate rose steadily over the 12-month period ending in August 2025.

- The softened labor demand was reflected primarily in reduced hiring activity, creating additional challenges for unemployed workers who faced fewer job openings and lower rates of finding employment. Although hiring conditions deteriorated, the rates of layoffs and discharges remained steady as of July 2025.

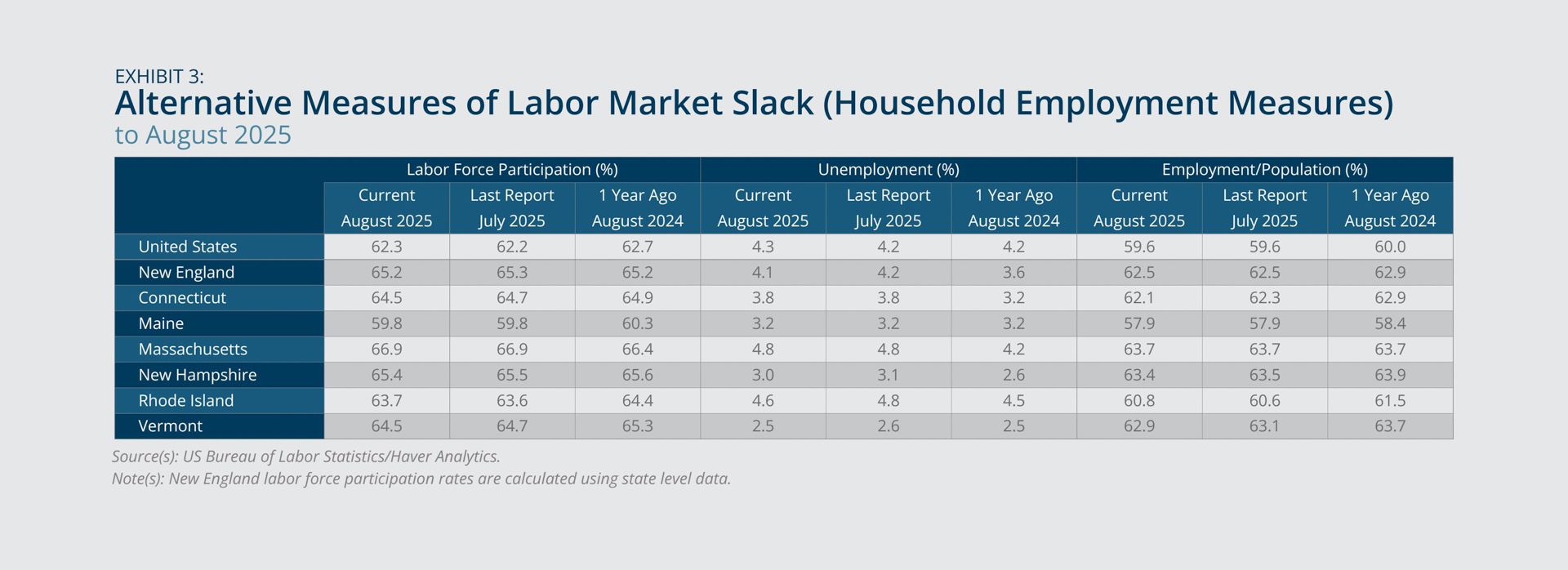

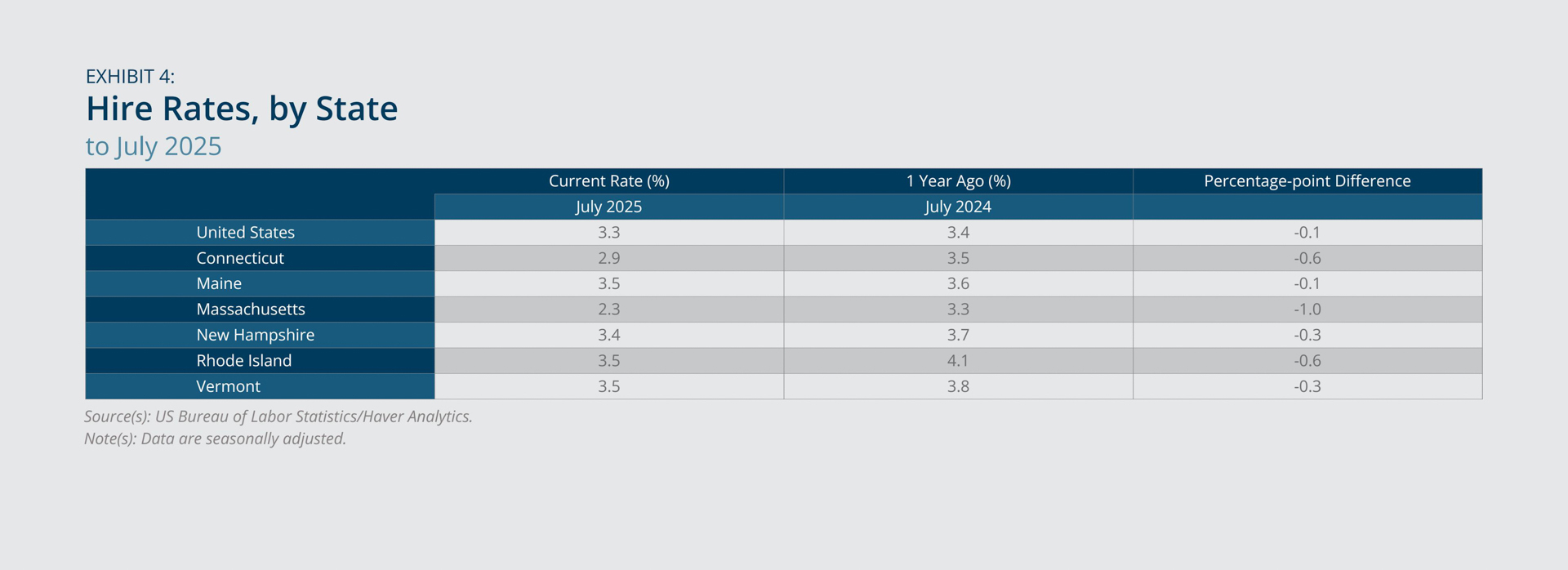

The unemployment rate was 4.1 percent in New England and 4.3 percent in the United States in August 2025 (Exhibit 3). The rates represent year-over-year increases of 0.5 and 0.1 percentage point, respectively. Over the same period, New England’s employment-to-population ratio demonstrated a simultaneous decline of 0.4 percentage point (Exhibit 3). These changes, along with the slowdown in job creation, suggest that softened labor demand had substantially raised the risk of unemployment within the region. The softened demand was reflected primarily in reduced hiring activities. Across all states in the region, hire rates declined from July 2024 to July 2025, with decreases ranging from 0.1 percentage point in Maine to 1.0 percentage point in Massachusetts, compared with a 0.1 percentage point decline nationwide (Exhibit 4).

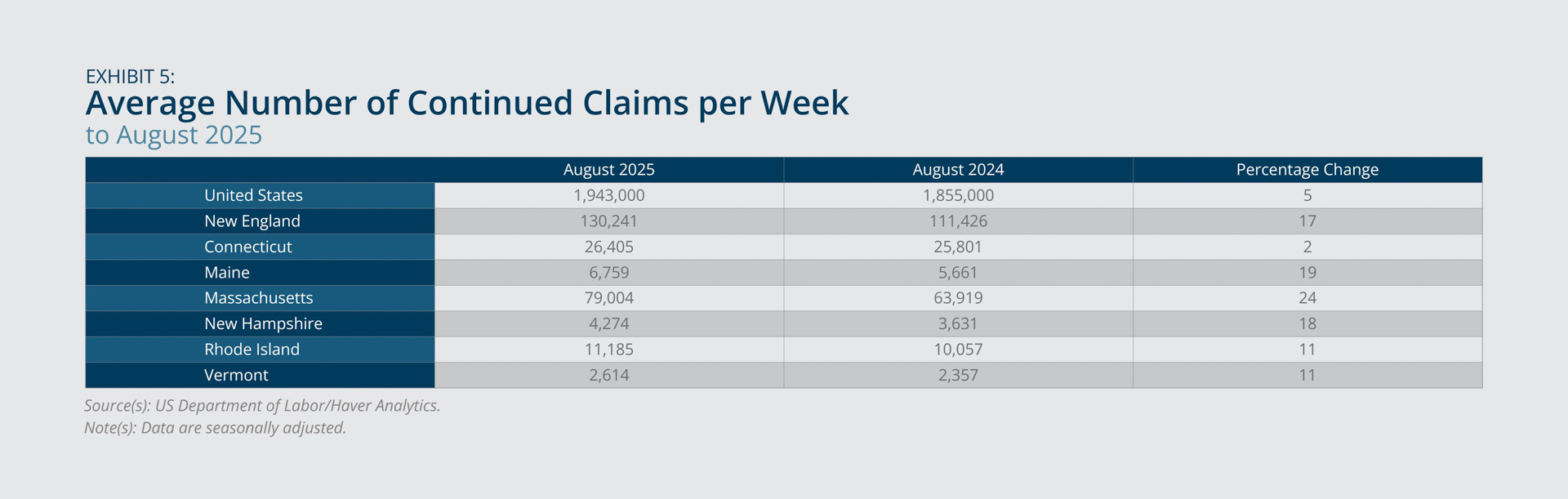

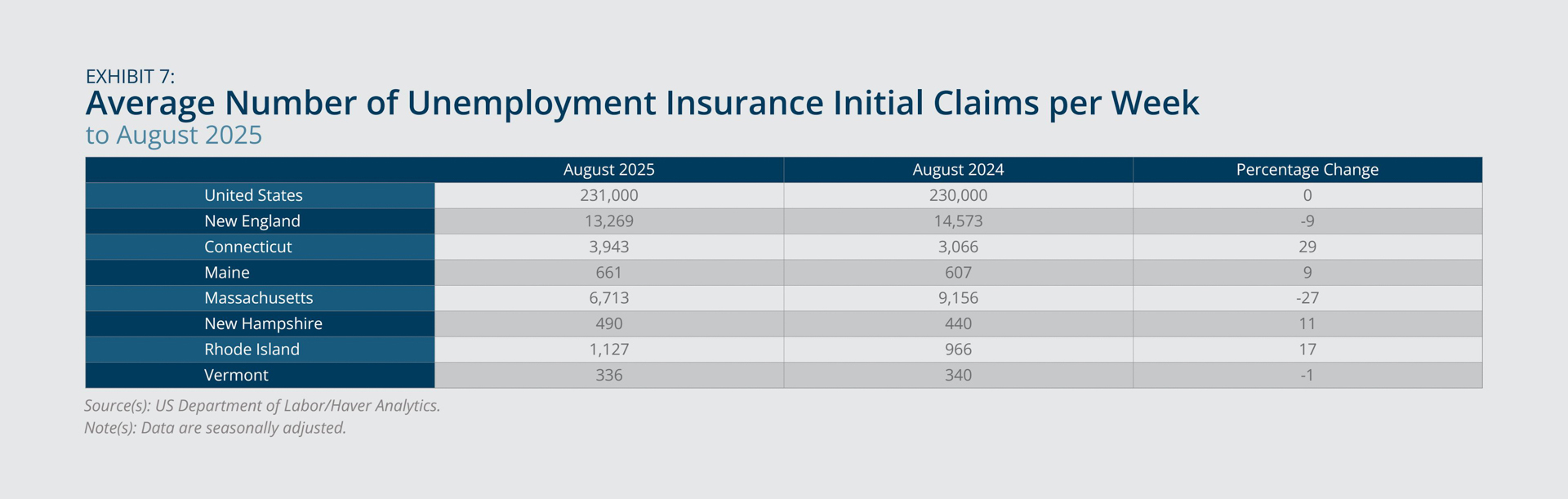

The weakened hiring placed greater burdens on unemployed workers, who faced fewer job openings and lower job-finding rates. Consistent with this observation, the average number of continued unemployment insurance (UI) claims per week, which measures the total number of workers who continued to receive unemployment insurance after an initial eligible job loss incident, rose 17 percent from August 2024 to August 2025 (Exhibit 5). Although the hiring environment deteriorated, layoff and discharge rates remained stable during this period (Exhibit 6). Correspondingly, the average weekly initial unemployment claims, reflecting newly filed UI-eligible job loss cases, were modestly below last year’s levels (Exhibit 7). However, if labor demand continues to cool, employers may explore additional strategies beyond hiring freezes to reduce workforce sizes, as evidenced by recently announced layoff plans from several regional employers.2

{kind=link}

Federal Reserve Bank of Boston

{kind=link}

Federal Reserve Bank of Boston

{kind=link}

Federal Reserve Bank of Boston

{kind=link}

Federal Reserve Bank of Boston

{kind=link}

Federal Reserve Bank of Boston

Inflation

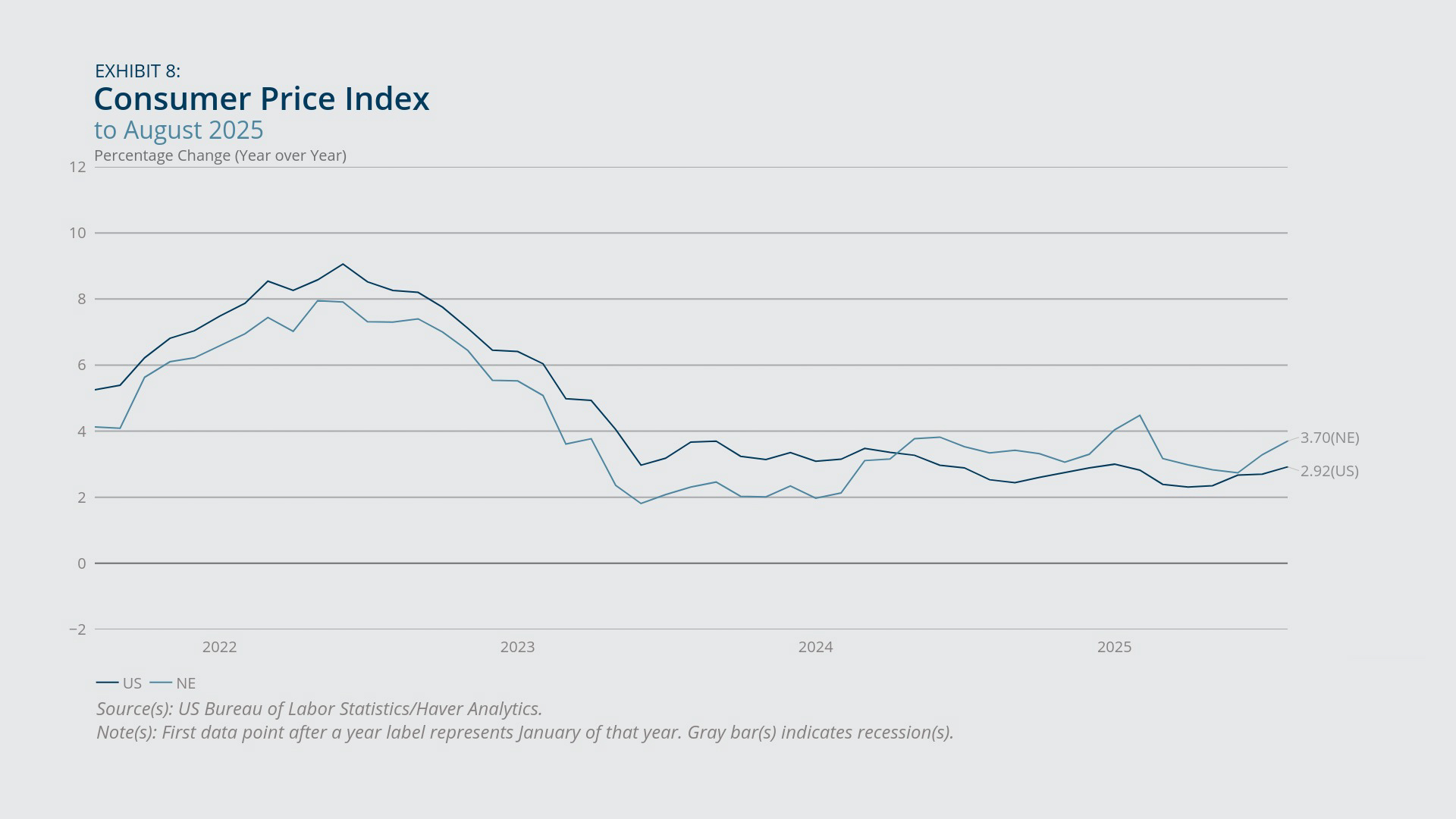

- Year-over-year inflation in New England reached 3.7 percent in August 2025, surpassing the national rate for the 16th consecutive month.

- Shelter costs remained the primary driver of the region’s more elevated inflation, rising 5.6 percent from the previous year, considerably higher than the national shelter inflation rate of 3.6 percent.

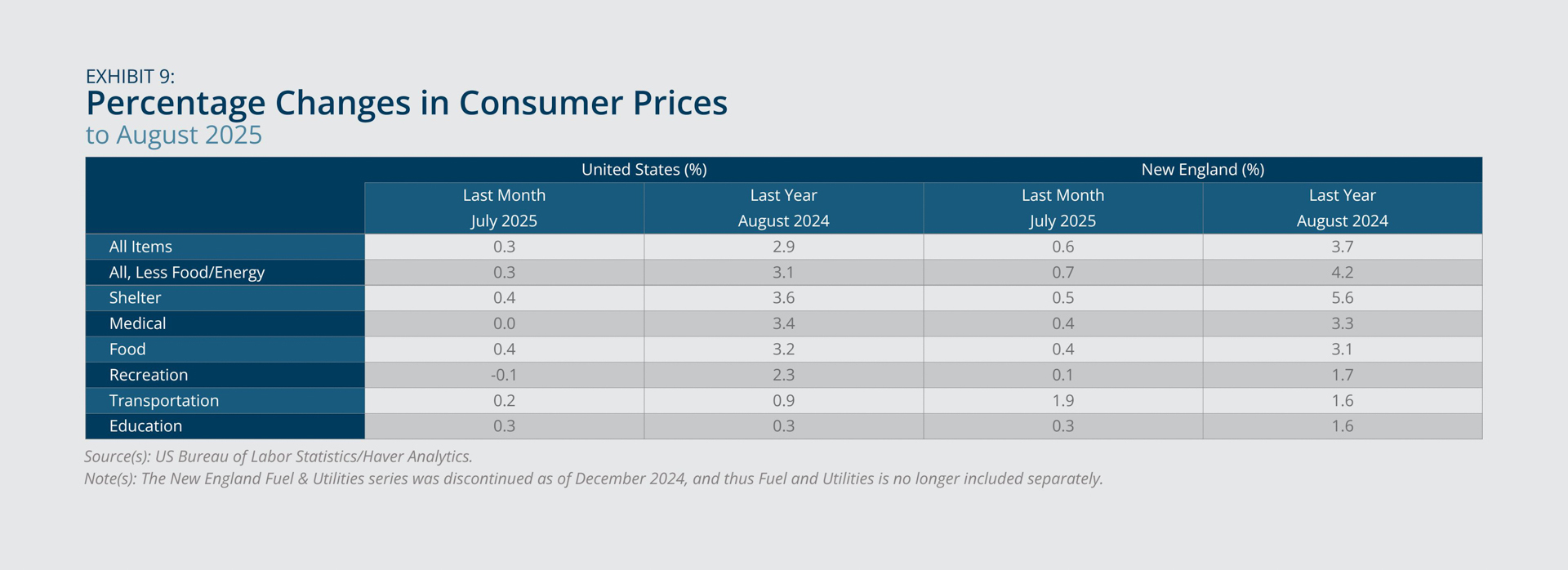

In August 2025, inflation, as measured by the year-over-year change in the Consumer Price Index for All Urban Consumers (CPI-U), was 3.7 percent in New England and 2.9 percent nationwide (Exhibit 8). The rates reflect a 0.4 and 0.2 percentage point increase from the preceding month in the region and nationally, respectively. During the same period, core inflation, which excludes the often more volatile food and energy expenditure components, rose 4.2 percent in the region (Exhibit 9). These figures highlight the increased inflation pressure the region experienced over the past summer.

Shelter inflation remained the primary driver of the region’s more elevated inflation, rising 5.6 percent year-over-year in August 2025, substantially exceeding the national rate of 3.6 percent (Exhibit 9). Although shelter inflation has softened from its peak of 8.4 percent in June 2024, the deceleration has been sluggish compared with the swifter adjustment observed across the country. The stickiness of shelter inflation largely accounts for the divergence between the inflation trajectories of New England and the United States since 2024. Transportation-related expenditure was a secondary factor behind the region’s recent inflation hike. It contributed through both accelerated price increases for motor vehicles and stagnation in previously declining motor fuel costs (not shown).

{kind=link}

Federal Reserve Bank of Boston

{kind=link}

Federal Reserve Bank of Boston

Real Estate Markets

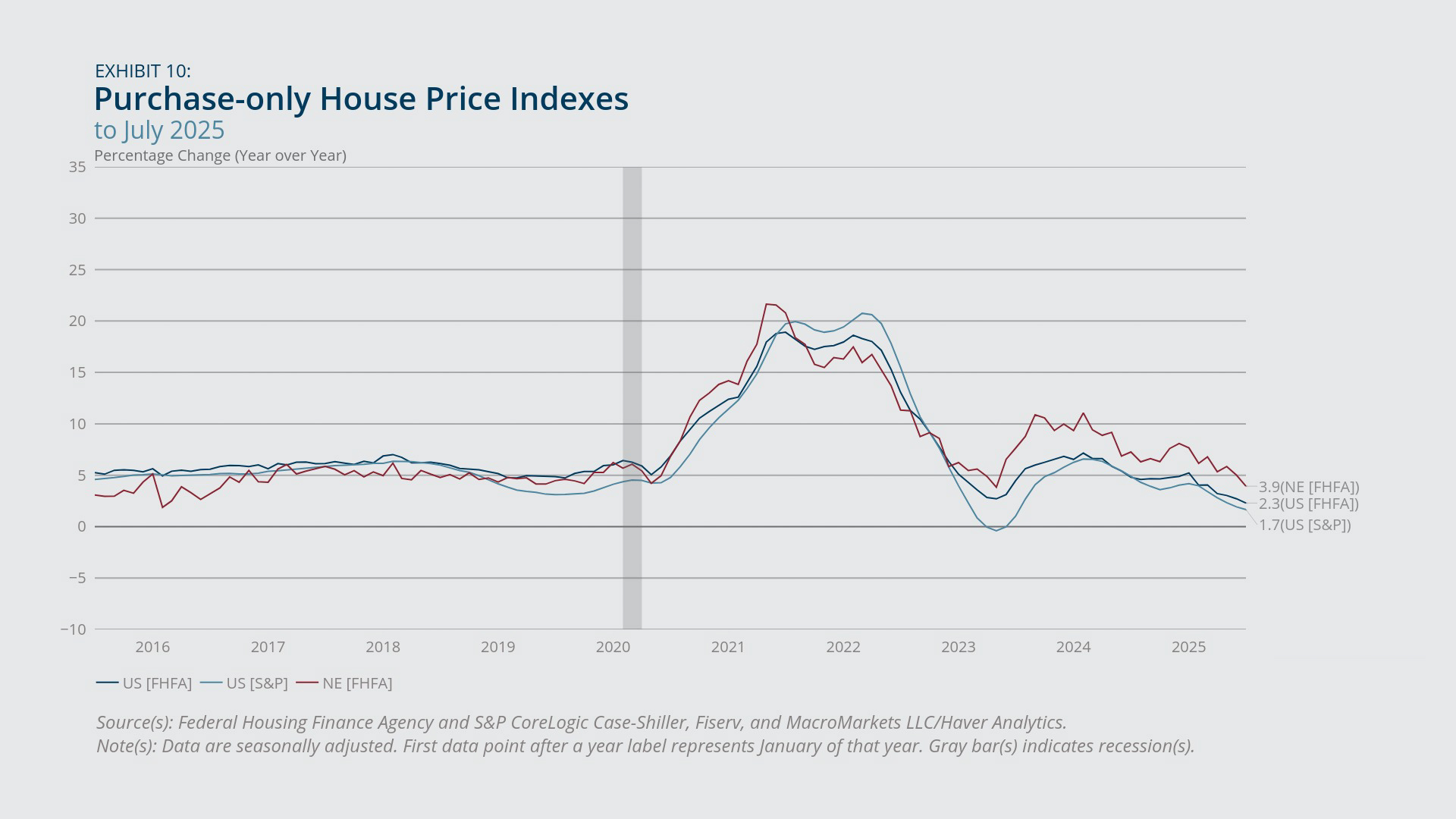

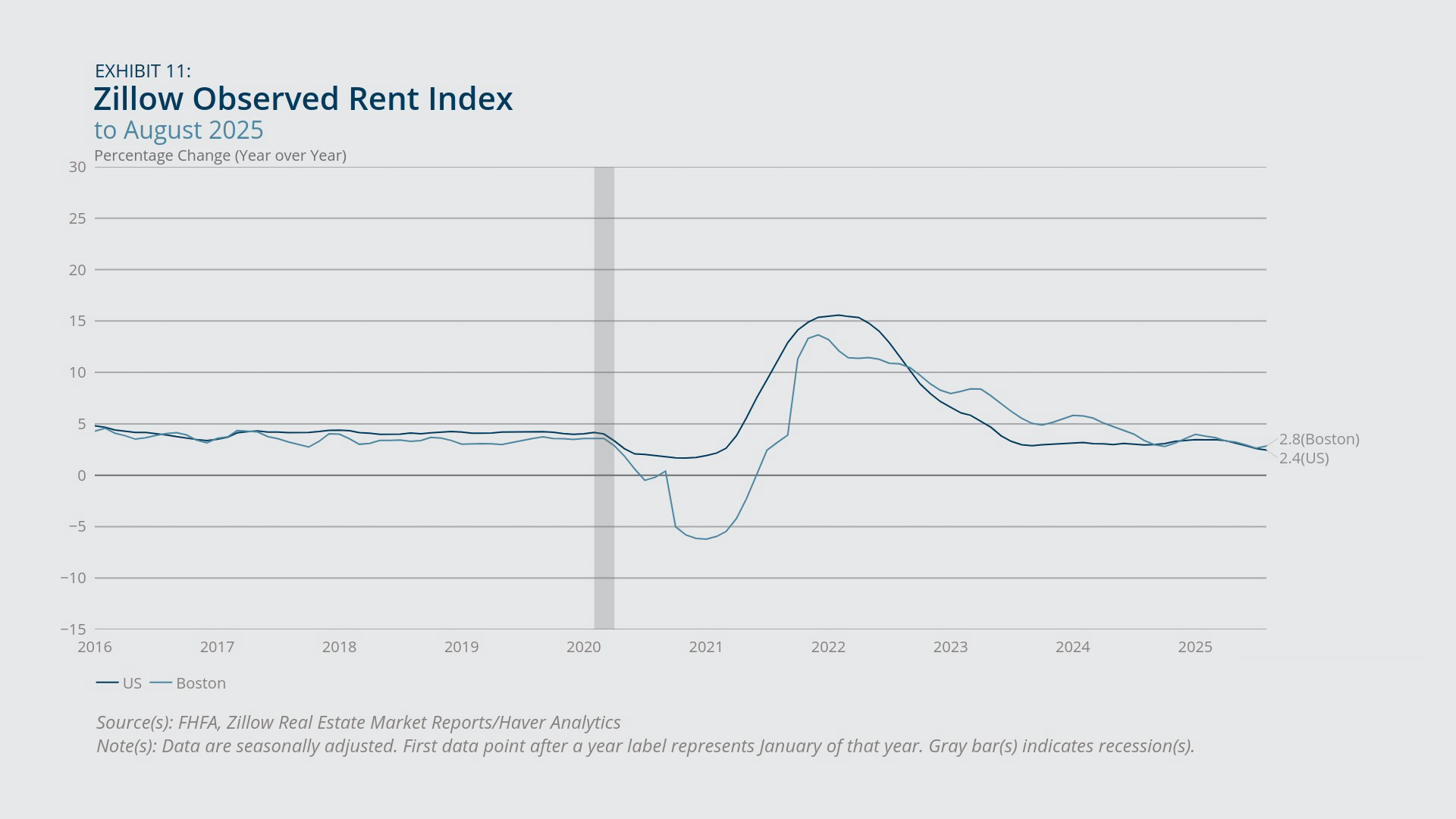

- From January through July 2025, house-price growth and rent growth continued to decelerate throughout New England and across the nation, falling below pre-pandemic levels.

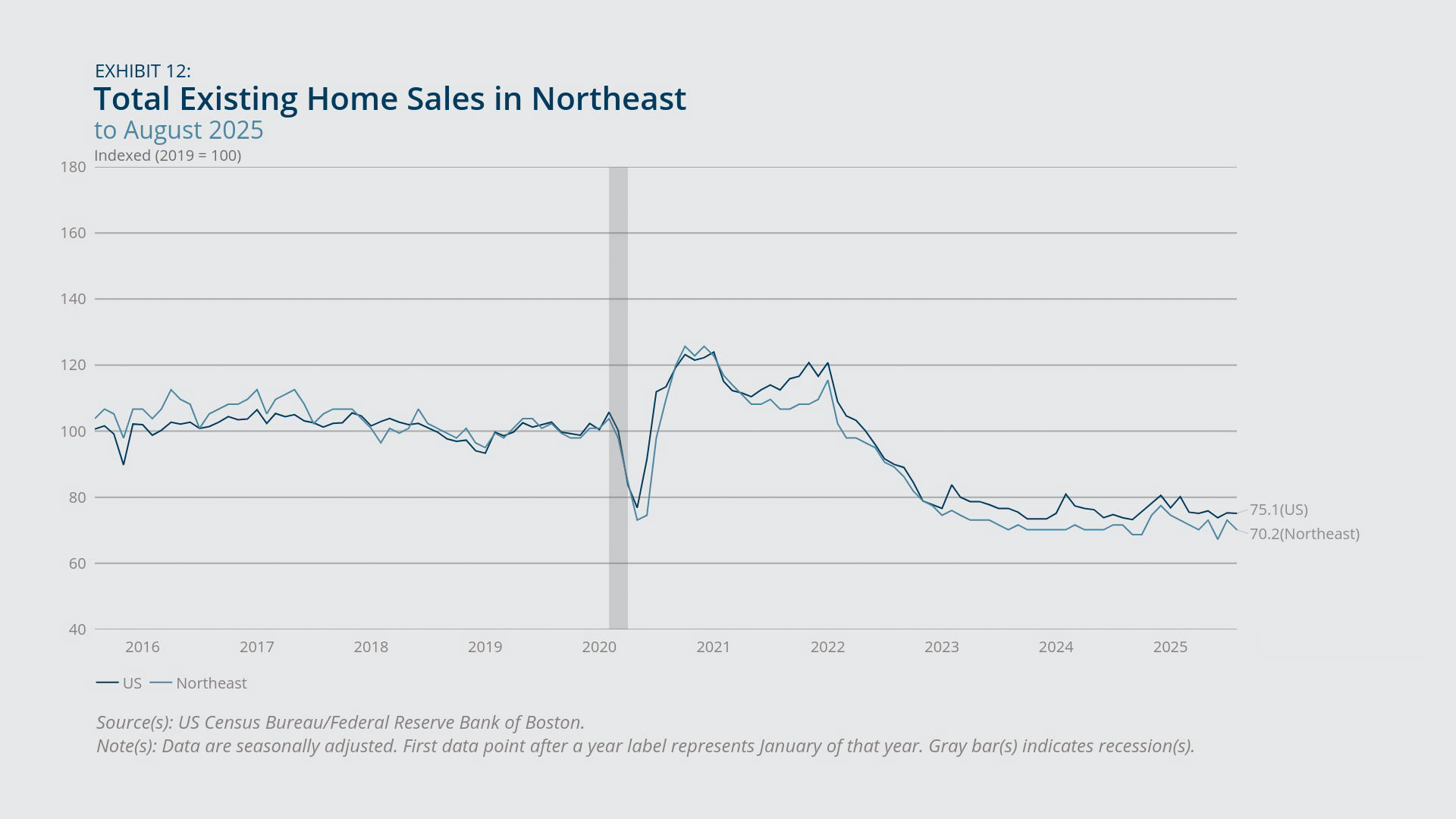

- Housing market activity remained sluggish despite cooling price growth, with existing home sales in the Northeast standing 30 percent below their 2019 levels as of August 2025.

In New England and nationwide, house-price appreciation continued the deceleration that began at the start of 2025. According to the Federal Housing Finance Agency (FHFA) House Price Index, regional house prices grew 3.9 percent year-over-year in July 2025, a significant decline from the 7.6 percent growth recorded in January 2025 and slightly below pre-pandemic levels (Exhibit 10). Nationally, the year-over-year house-price growth fell to 2.3 percent in July 2025, considerably below pre-pandemic rates. The difference suggests that while the housing market cooled across the country, New England experienced a more moderate slowdown compared with the United States as a whole.

The rental market followed similar patterns. In the Boston metropolitan area, rent growth, as measured by the year-over-year change in the Zillow Observed Rent Index, declined to 2.8 percent in August 2025, slightly below the area’s pre-pandemic levels (Exhibit 11). Meanwhile, national rent growth fell to 2.4 percent during the same period, substantially below its 2019 rate.

Despite moderating price growth, housing transaction volumes remained persistently low. As of August 2025, existing home sales in the Northeast were 30 percent lower than 2019 levels (Exhibit 12), indicating that insufficient inventory and elevated prices continued to limit housing market mobility within the region.

{kind=link}

Federal Reserve Bank of Boston

{kind=link}

Federal Reserve Bank of Boston

{kind=link}

Federal Reserve Bank of Boston

Consumer Confidence

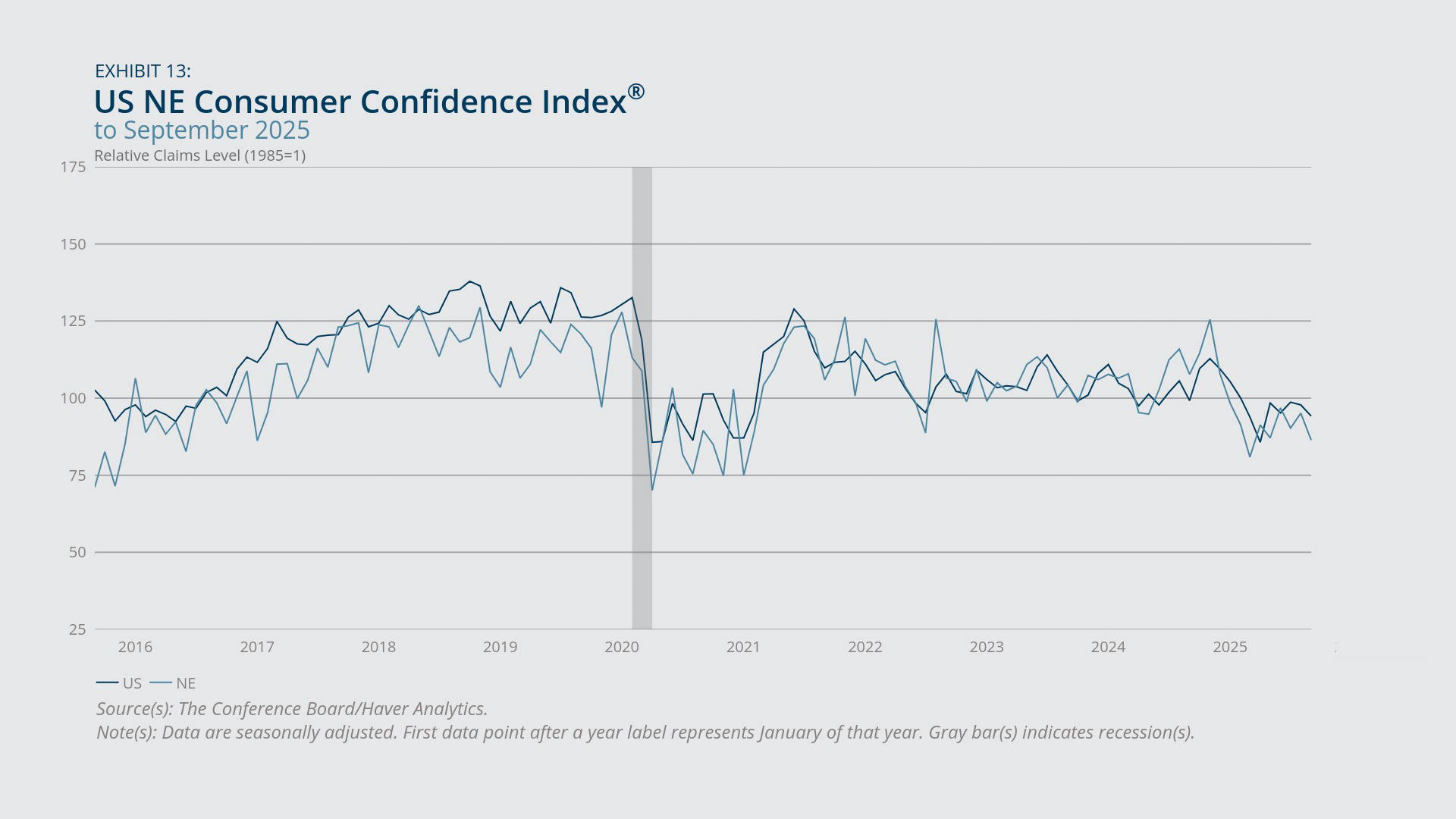

- Consumer confidence in New England and nationwide weakened in the first eight months of 2025 compared with levels observed during the previous three years.

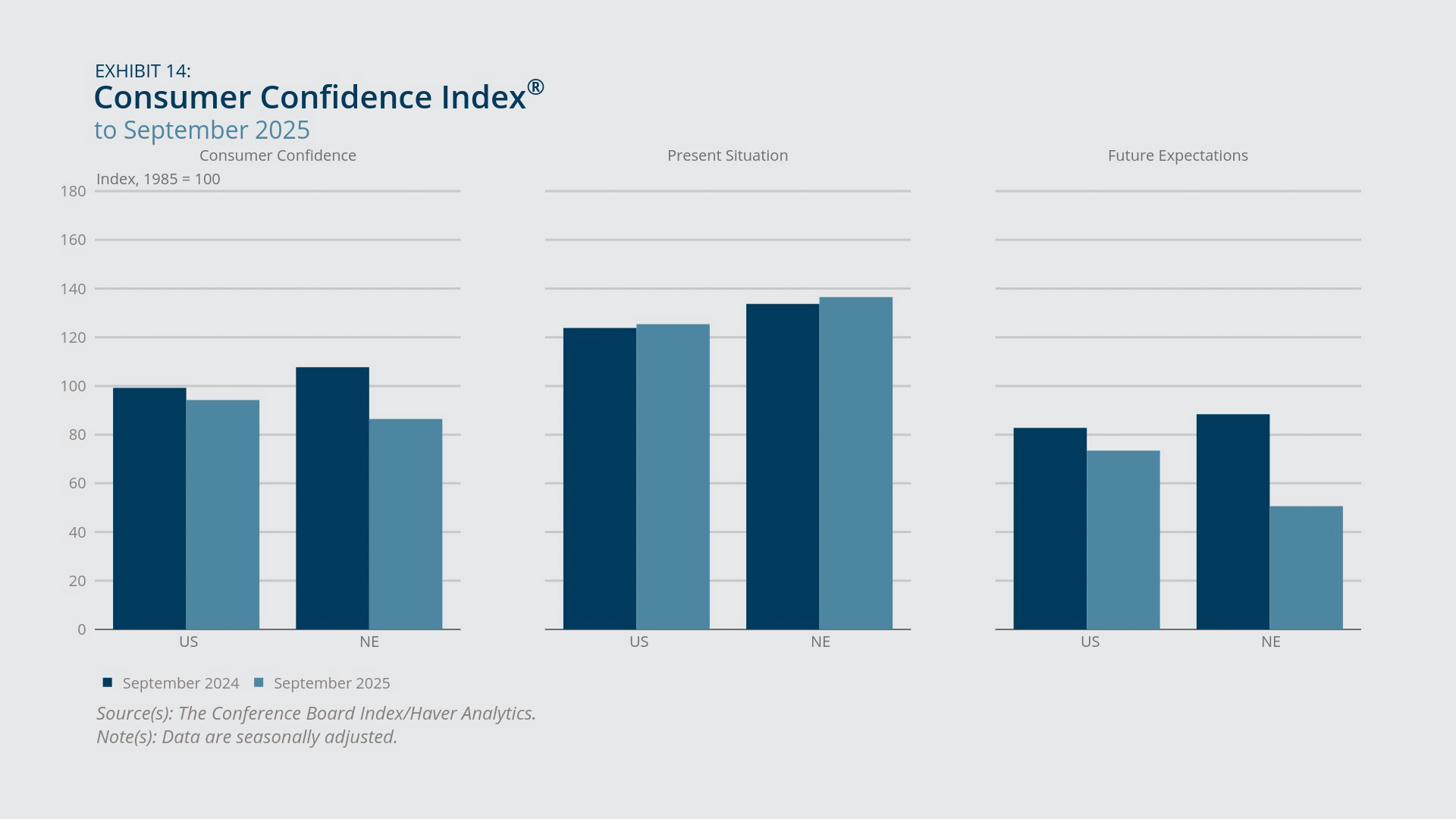

- The deterioration in consumer confidence can be attributed primarily to pessimism about future economic conditions, with the regional future expectations index hitting its lowest point since March 2013 in September 2025.

Consumer confidence in New England, as measured by the Conference Board’s Consumer Confidence Index, stayed within the 80 to 100 range throughout 2025, declining from the above-100 readings recorded during the previous three years (Exhibit 13). This regional pattern closely mirrored the national consumer confidence trajectory observed during the same period.

In both New England and across the country, the weakened confidence stemmed primarily from deteriorating outlooks regarding future economic conditions. From September 2024 to September 2025, the future expectations index fell sharply from 88.4 to 50.6 in the region, while the national index declined more modestly from 82.8 to 73.4 (Exhibit 14). Although national future expectations showed a partial recovery after April 2025, the regional index in September 2025 fell to its lowest point since March 2013. New Englanders’ more pessimistic view of their short-term economic prospects may be influenced by the recent rise in inflation levels and slower employment growth that disproportionately affected the region’s economy.

{kind=link}

Federal Reserve Bank of Boston

{kind=link}

Federal Reserve Bank of Boston

Endnotes

- See “Current Employment Statistics Preliminary Benchmark (National) Summary,” US Bureau of Labor Statistics Economic News Release, September 9, 2025.

- See, for example, Ben Unglesbee, “Boston University To Lay Off 120 Staffers amid Budget Challenges,” Higher Ed Dive, July 8, 2025; Matt Schooley, “Moderna Will Lay Off 10% of Employees, Massachusetts-based Company Announces,” CBS News, July 31, 2025; and Isabel Hart, “Major Mass. Biomanufacturer Plans Dozens of Layoffs,” Boston Business Journal, September 12, 2025.

About the Authors

About the Authors

Pinghui Wu,

Federal Reserve Bank of Boston

Pinghui Wu is a senior economist with the New England Public Policy Center at the Federal Reserve Bank of Boston.

Email: Pinghui.Wu@bos.frb.org

Nathaniel R. Nelson,

Federal Reserve Bank of Boston

Nathaniel R. Nelson is a senior research associate with the New England Public Policy Center in the Federal Reserve Bank of Boston Research Department.

Acknowledgments

Kelly Jackson, a senior data analyst in the Federal Reserve Bank of Boston Research Department, prepared the exhibits for this memo.

Resources

Site Topics

Keywords

- Regional economy ,

- Economic Conditions ,

- New England ,

- NEPPC