A Portrait of First District Banks

{kind=link}

Federal Reserve Bank of Boston

The views expressed herein are solely those of the author and should not be reported as representing the views of the Federal Reserve Bank of Boston, the principals of the Board of Governors, or the Federal Reserve System.

In the popular media, the current era is characterized by the emergence of nontraditional finance, as represented by crypto assets, fintech lender buy-now-pay-later loans, and fintech and Big Tech payment services. Receiving less media attention is the reality that traditional banks, though their numbers have declined steeply over the last four decades, continue to perform a broad range of important financial functions in today’s economy.

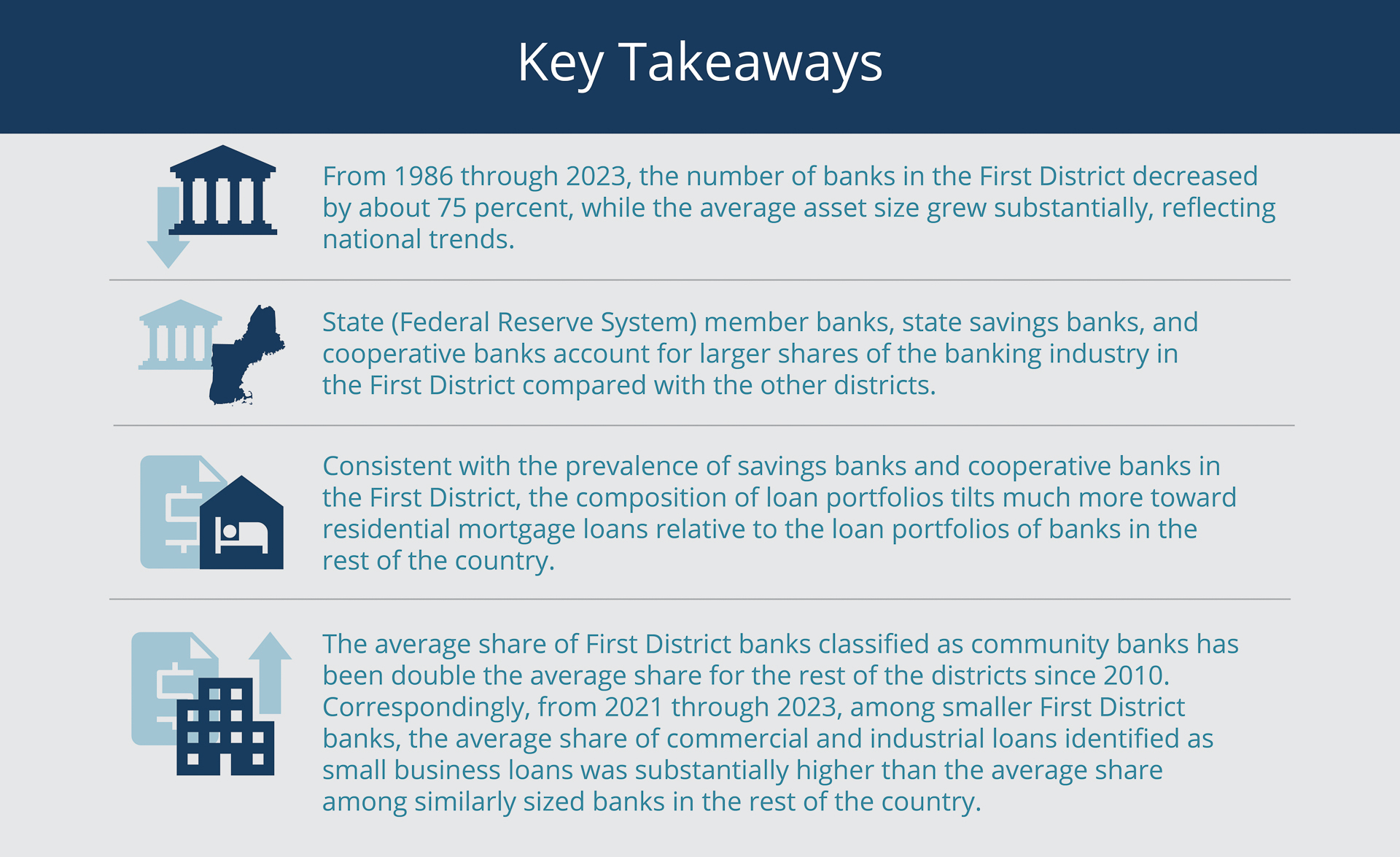

This Regional Brief sketches a portrait of the banks1 in the Federal Reserve System’s First Federal Reserve District (referred to as “the First District” hereafter), which includes all of New England except Connecticut’s Fairfield County.2 It highlights a few characteristics that distinguish the district’s banking industry, noting that, relative to the rest of the United States, larger shares of the region’s banks are state (Federal Reserve System) member banks, state savings banks, and cooperative banks, and the share of banks classified as community banks is twice as large.

Sign up for new research and data on the New England economy.

Corresponding to the prevalence of smaller banks in New England, residential real estate loans and small business loans constitute larger shares of First District loan portfolios compared with the loan portfolios of banks in the other districts.

As with the rest of the country, the market for bank deposits is generally considered concentrated in the rural areas of the First District, according to US Department of Justice antitrust guidelines. On the other hand, the market is at least reasonably competitive in the more densely populated areas, even though, as noted, the number of banks in the district has decreased sharply since the 1980s.

Banks Have Declined in Number and Grown in Size

The US banking industry, including in the First District, has undergone a dramatic transformation in the quantity of banks and their (inflation-adjusted) asset sizes since the mid-1980s following a series of regulatory and legislative efforts aimed at deregulation. In particular, in the 1980s, several states removed restrictions on interstate banking, reciprocally or unilaterally. This process culminated in the 1994 Riegle-Neal Interstate Banking and Branching Efficiency Act, which removed many of the obstacles to opening bank branches across state lines. In doing so, the act effectively eliminated restrictions on the number of branches a bank could operate nationwide.3

{kind=link}

Federal Reserve Bank of Boston

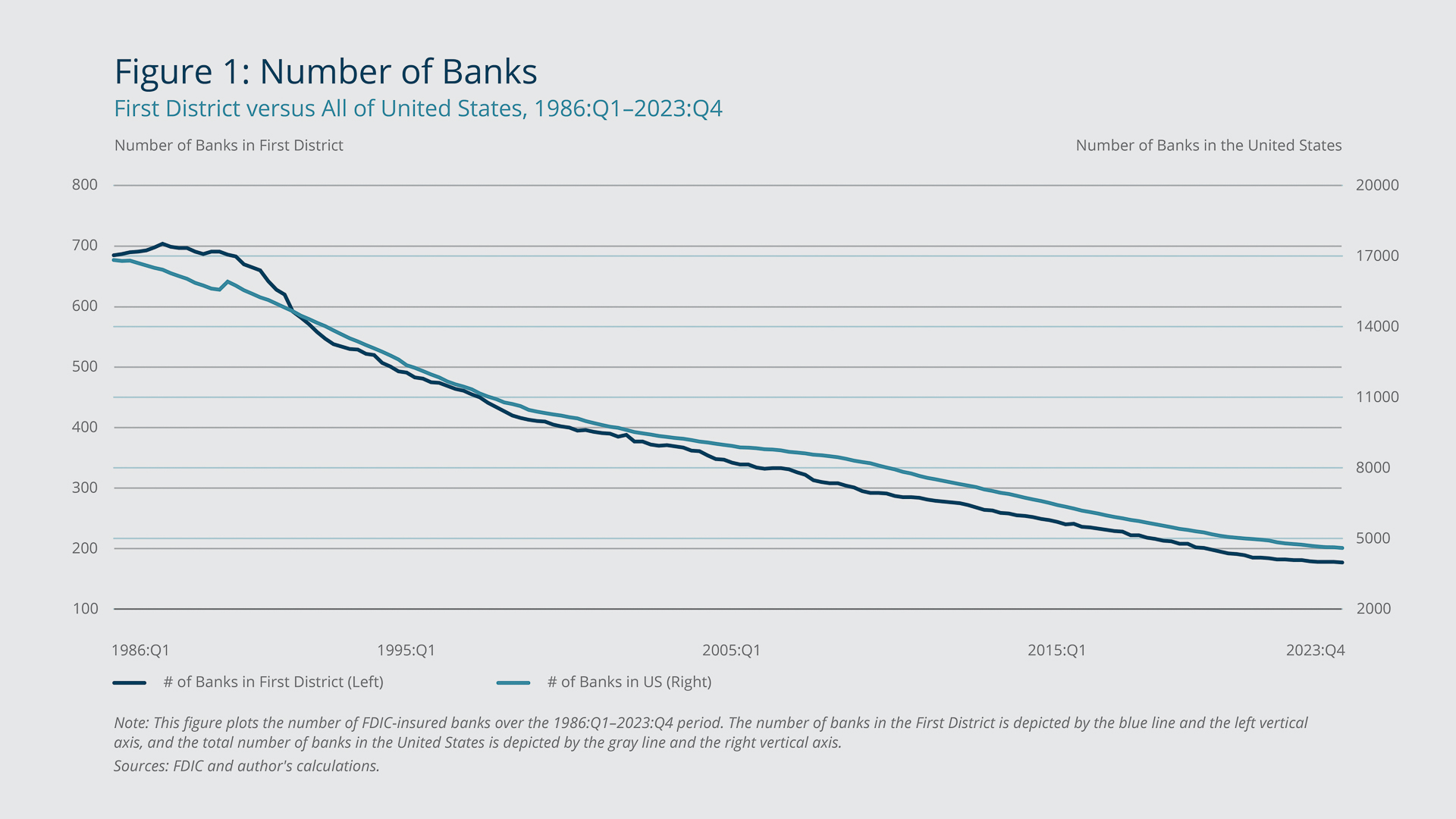

Over roughly the same period, advances in technology, especially in information and communication technology (such as the spread of computers and the advent of the Internet), also brought about profound changes in the operations of financial institutions. The combination of technological advances and deregulation precipitated, among other consequences, a wave of mergers and acquisitions, especially in the late 1980s and through the 1990s. As a result, the number of Federal Deposit Insurance Corporation (FDIC)–insured banks declined from more than 16,000 at the beginning of 1986 to just over 4,400 at the end of 2023 (the last available full year of data), as shown in Figure 1 (the gray line and right axis).

A similar trend is evident in the First District: The number of banks fell from nearly 700 in the first quarter of 1986 to fewer than 200 in the fourth quarter of 2023 (the blue line and left axis in Figure 1). The decline in the First District was close to 75 percent, which is as steep as the decline in the United States as a whole.

{kind=link}

Federal Reserve Bank of Boston

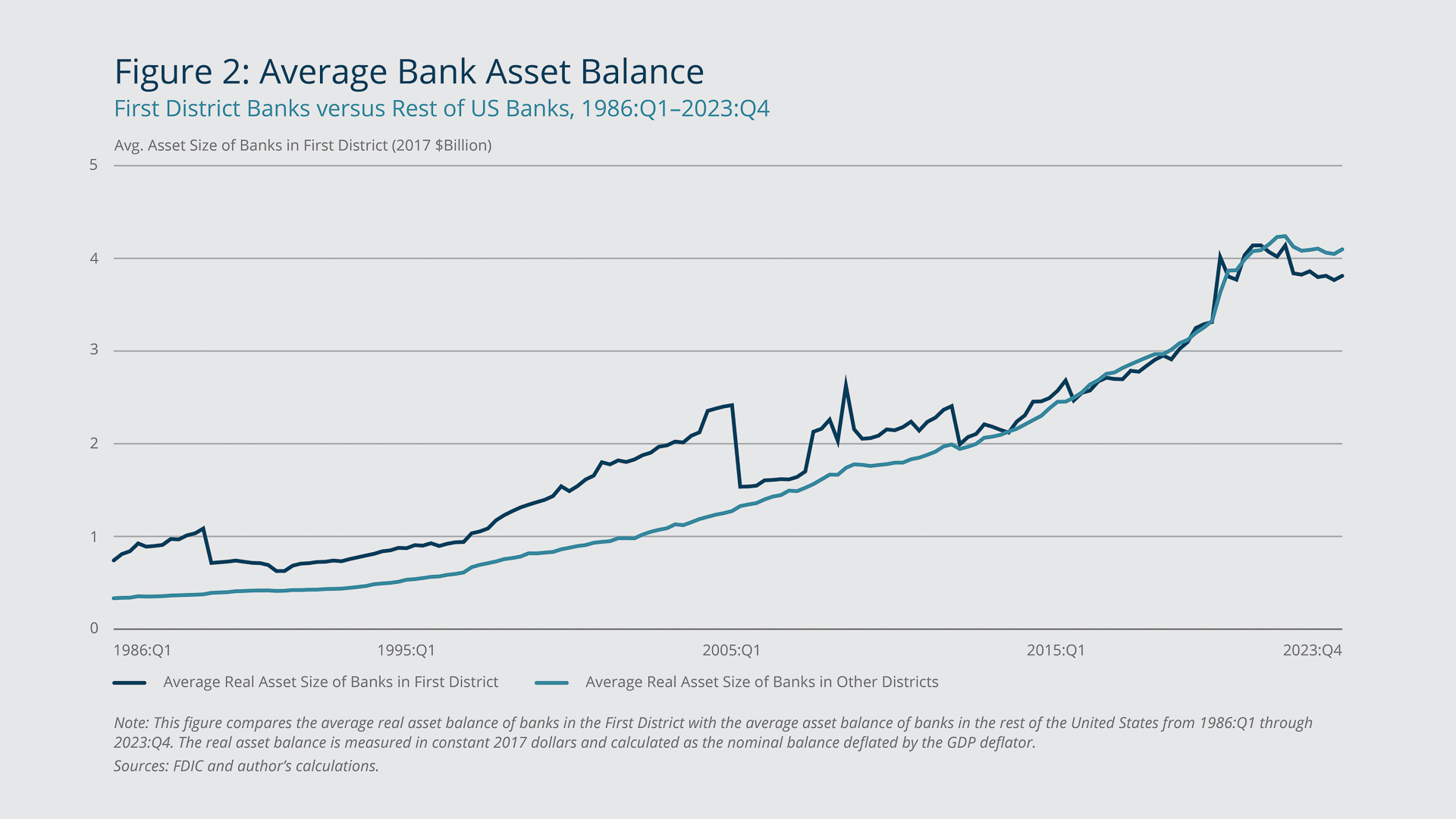

One predictable consequence of the successive waves of consolidations is that the average size of banks, measured by assets, has grown substantially. Figure 2 shows the increase in the average inflation-adjusted bank real assets (in constant 2017 dollars) from the beginning of 1986 through the end of 2023 for banks in the First District (from $781 million to $3.89 billion) and banks in the rest of the United States (from $352 million to $4.25 billion).4

More Cooperative and State Savings Banks in the First District

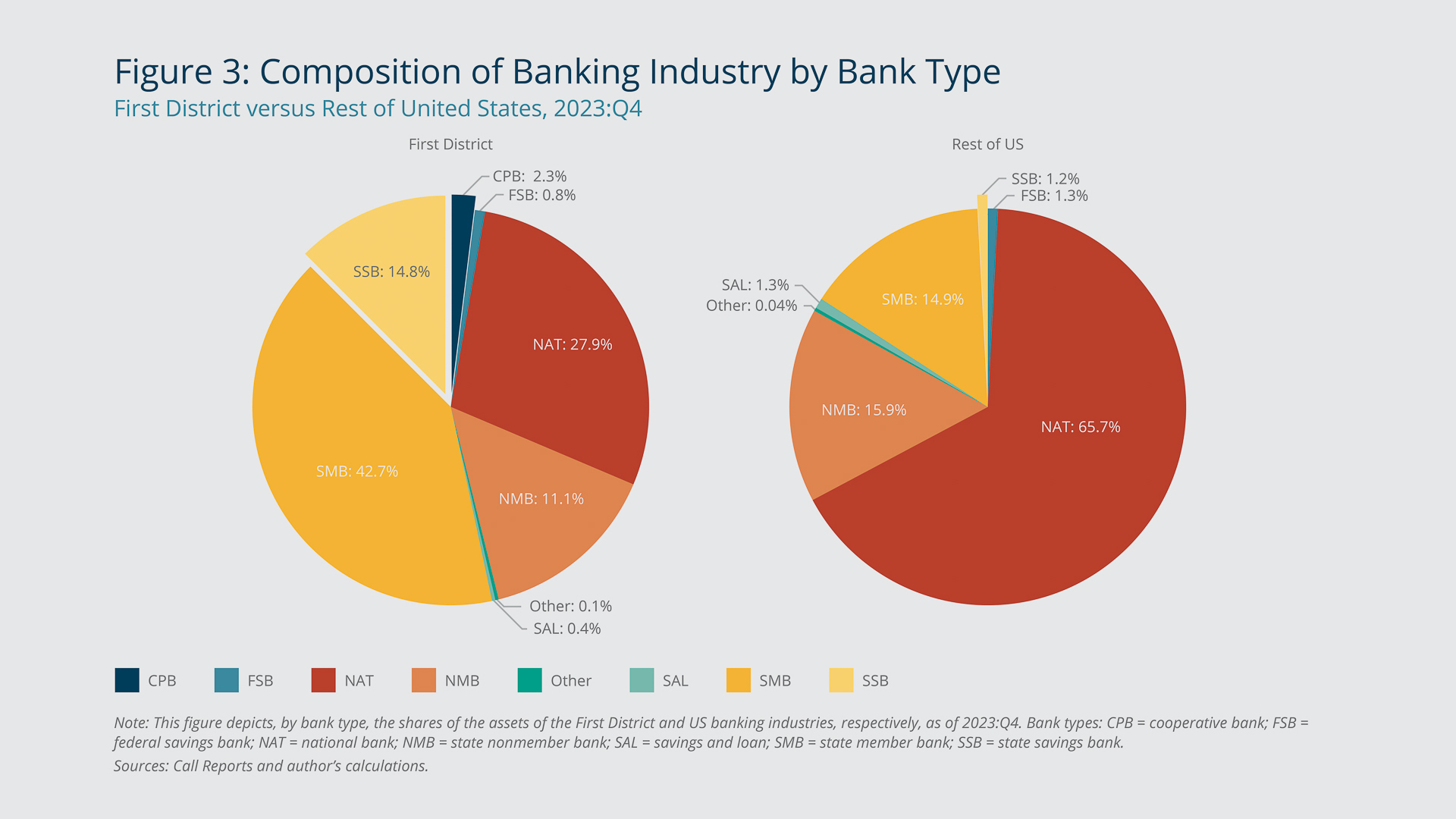

Figure 3 shows the composition of the banking industry by bank type in the First District versus the rest of the country as of 2023:Q4. The figure illustrates that, compared with the rest of the Federal Reserve System districts, a higher share of banks in the First District is classified as state member banks (SMBs, state-chartered banks that are members of the Federal Reserve System): 42.7 percent versus 14.9 percent. The shares that are state savings banks (SSBs) and cooperative banks (CPBs) are also higher but to lesser extents: 14.8 percent versus 1.2 percent for SSBs and 2.3 percent versus 0 percent for CPBs.5 Correspondingly, the share of national banks is noticeably higher in the rest of the United States: 65.7 percent versus 27.9 percent.

{kind=link}

Federal Reserve Bank of Boston

Savings banks and cooperative banks tend to be smaller in asset size compared with other banks and focus more on serving customers living in the local communities.6 Historically, more than other banks, they have specialized in providing home mortgage loans. Consistent with this tradition and the greater presence of such banks in New England, the composition of loan portfolios of First District banks tilts much more toward residential mortgage loans relative to the loan portfolios of banks in the rest of the country.

As the left panel of Figure 4 shows, there is a common, almost monotonic pattern in which, among all banks, smaller banks generally hold higher shares of residential mortgages on their balance sheets. The average shares, however, differ markedly. As of 2023:Q4, among banks within each asset-size grouping, or bin, the share of residential real estate loans (as a percentage of a bank’s total loan portfolio) was notably higher for banks in the First District, especially First District banks with assets of less than $1 billion.

{kind=link}

Federal Reserve Bank of Boston

Not surprisingly given the data on mortgage loans, for a given asset-size range, First District banks hold clearly lower shares of commercial real estate (CRE) and commercial and industrial (C&I) loans in their portfolios relative to the rest of the banks in the United States, as shown in the middle and right panels, respectively, of Figure 4.

Important Role of the First District’s Community Banks

The First District also features a larger share (in terms of overall bank assets) of banks that are community banks compared with the other districts. The FDIC designates a banking organization as a community bank if its asset balance falls below a threshold or if it satisfies several other criteria even though its assets exceed the threshold value. Community banks thus tend to be smaller, or they operate in fewer states or cities or have fewer offices than other bank types, and they tend to engage in traditional banking activities such as providing loans funded with deposits.7 Figure 5 shows that, since 2010:Q1, the average share (as measured by the percentage of overall bank assets) of First District banks classified as community banks has basically been double the average share of the rest of the districts.8

{kind=link}

Federal Reserve Bank of Boston

As many studies of small business credit note, community banks, especially relatively small banks, tend to specialize in relationship lending to small businesses;9 that is, they cultivate long-term relationships with small business borrowers to overcome the information-opacity problem—a lack of data on which a bank can evaluate a potential borrower’s creditworthiness—which is the primary obstacle to small businesses’ access to credit.

{kind=link}

Federal Reserve Bank of Boston

Consistent with this understanding that smaller banks engage more than larger banks in making relationship loans to small businesses, loans with balances of $1 million or less constitute a higher share of relatively small First District banks’ collective C&I loan portfolio, even though C&I loans, on the whole, make up a smaller percentage of those banks’ total loan portfolio (as shown in Figure 4). This pattern can be seen in Table 1, which reports the mean and median shares of small business loans (that is, loans with balances of $1 million or less) as a percentage of overall C&I loans among the First District banks with asset balances of $1 billion or less versus similarly sized small banks in the rest of the country for the post-pandemic period of 2021:Q1 through 2023:Q4.10

{kind=link}

Federal Reserve Bank of Boston

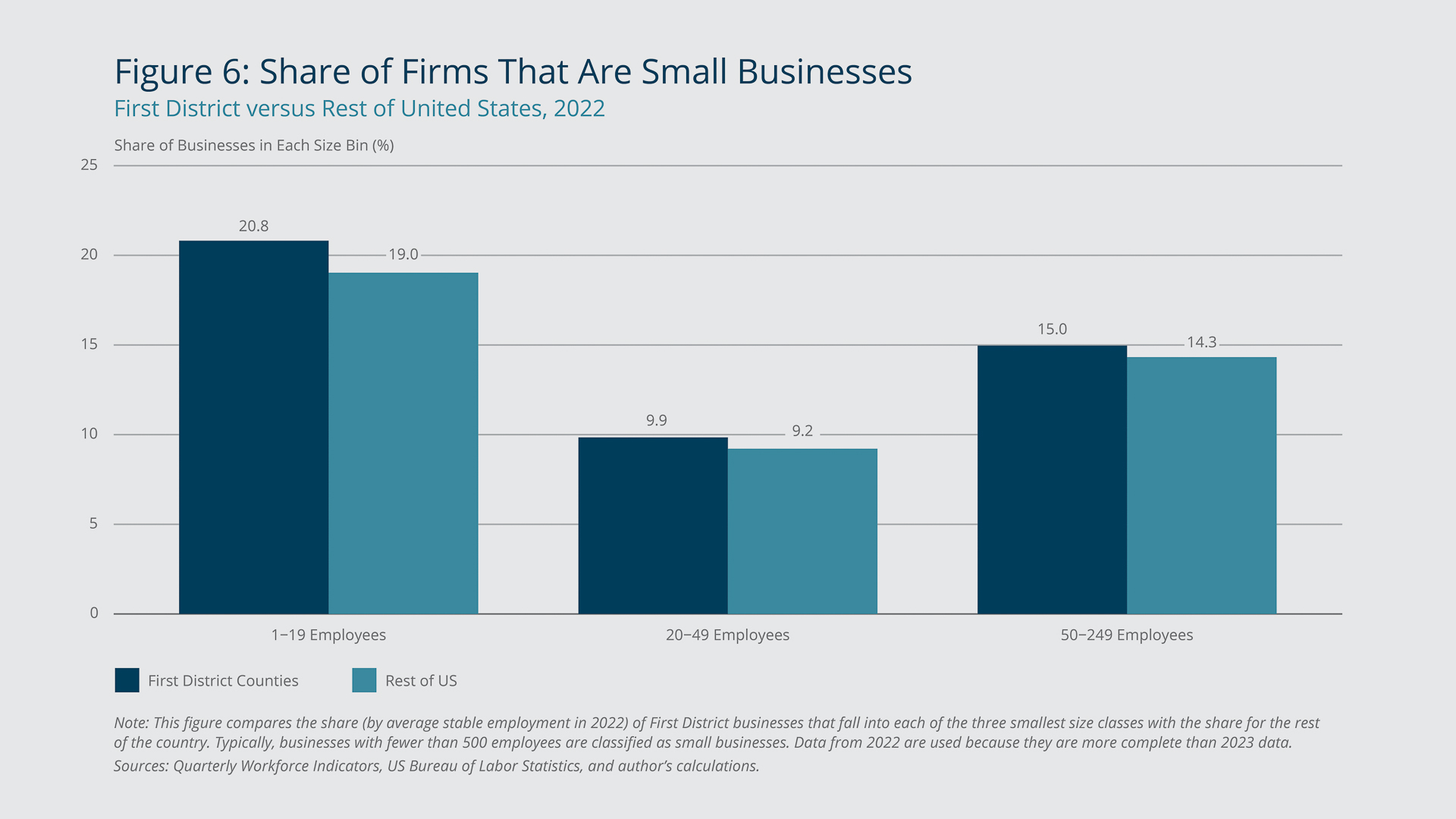

Small banks in the First District are thus well suited to serve the local business communities, which is particularly important for the district, where, compared with the rest of the country, a higher percentage of firms are small businesses. As Figure 6 shows, the First District features a higher share (by employment) of businesses in each of the three smallest size groupings: 1 to 19 employees, 20 to 49 employees, and 50 to 249 employees, according to US Bureau of Labor Statistics data from 2022.

Deposit-market Competition Now and in the Coming Years

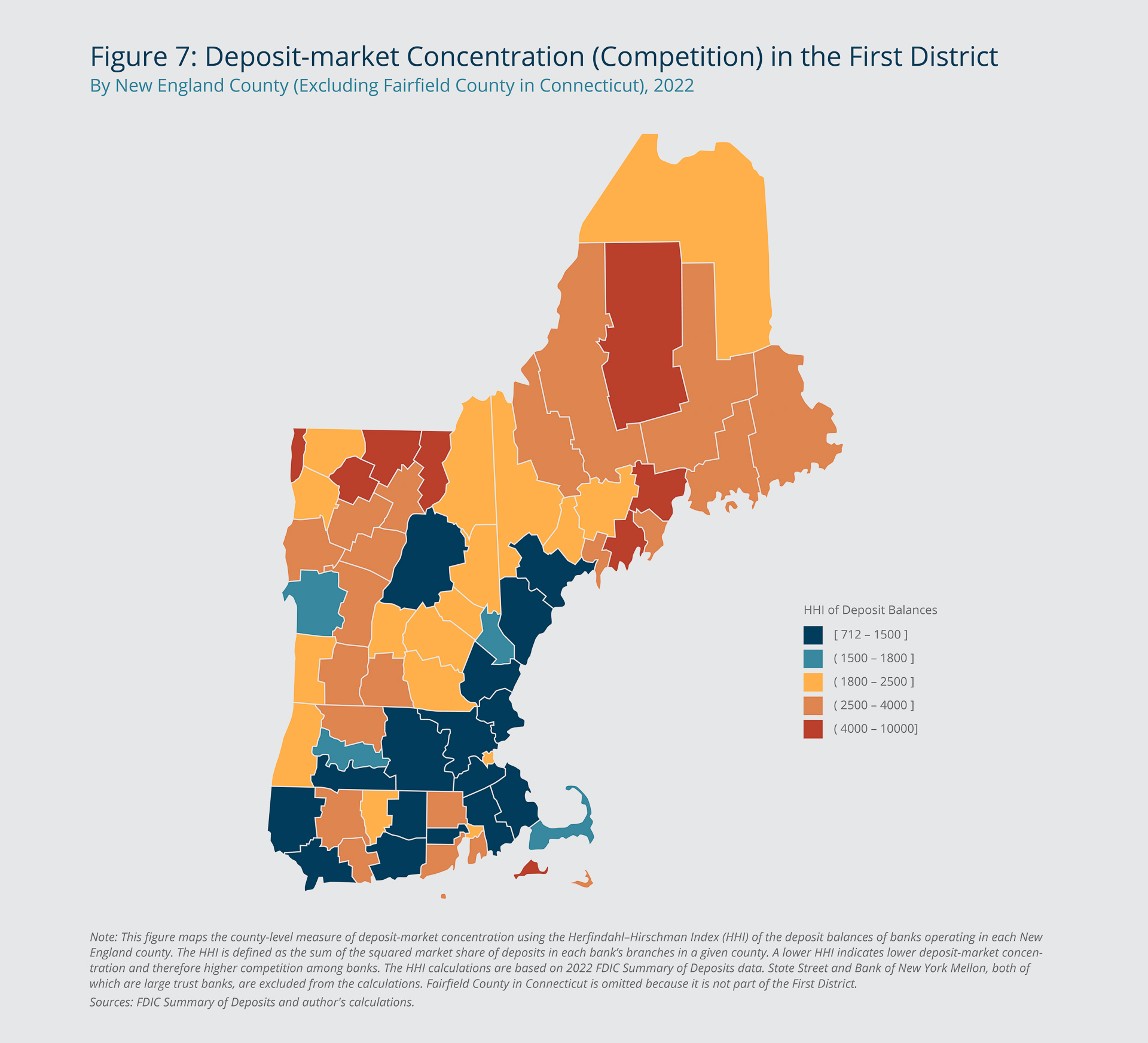

Besides serving the local communities through their lending, banks in the First District provide consumers with liquidity and transaction services through deposit products. The degree of deposit concentration suggests that the majority of deposit markets in the First District are “reasonably competitive,” according to the criteria set by the US Department of Justice. A low deposit concentration—when the total balance of deposits is spread among a relatively large number of banks and bank branches in a given area—indicates a competitive market, whereas a high deposit concentration indicates a noncompetitive market.

{kind=link}

Federal Reserve Bank of Boston

According to the Justice Department’s antitrust guidelines, markets with a Herfindahl–Hirschman Index (HHI) above 1,800 points are considered highly concentrated (and therefore not competitive), whereas those with an HHI of 1,000 to 1,800 are considered moderately concentrated (and reasonably competitive).11 Figure 7 maps the HHI in 2022 in each county of the First District. The darker colors (corresponding to lower HHI values) signify greater competition in a county.

The figure illustrates that the competition tends to be greater in more populous counties (including several in Massachusetts). A qualitatively similar pattern is also observed in the rest of the country, as the deposit concentration (and HHI) tends to be higher in rural areas than in urban areas.

While fintech and Big Tech firms increasingly penetrate the financial services industry and technology continues to advance rapidly, as epitomized by the recent major breakthroughs in generative artificial intelligence (GenAI), banks are expected to keep up with these developments so they can provide competitive products to their customers and retain their market share. Over the past several decades, information technology (IT) has tended to confer advantages to large banking organizations due to economies of scale, as evidenced by the massive increase in bank size largely through consolidations. Yet, many relatively small community banks in New England have not only survived but also continue to perform well by offering products that serve the needs of their local communities.

How the advent of GenAI will impact the operations of these banks and community banks in general is still an open question. Due to the technical complexity and high cost of developing AI tools, community banks will most likely need to partner with external technology providers. While offering opportunities, such partnerships also inevitably entail risks, as highlighted by the regulators in their guide to community banks for managing the risks associated with third-party relationships.12 Ideally, however, AI tools should enable community banks to deliver better-tailored products by augmenting their local knowledge and personal attention.

Endnotes

- In this Regional Brief, the term banks refers to both commercial banks and Federal Deposit Insurance Corporation–insured savings institutions (such as savings banks and savings and loans).

- When the Federal Reserve System was established in 1913, the United States was divided geographically into 12 Districts, each served by a separately incorporated Reserve Bank. For more details about the structure of the Federal Reserve System, see https://www.federalreserve.gov/aboutthefed/structure-federal-reserve-system.htm.

- See, for example, Berger et al. (1995) and Kroszner and Strahan (1999) for analyses of the period of deregulation and the resulting transformation of the US banking industry.

- Specifically, the nominal value of total assets is deflated by the gross domestic product deflator. The sharp decline and subsequent rebound in the average asset size for First District banks that appears in the middle of the graph resulted from two large banks changing their district assignments. Fleet was acquired by Bank of America and left the First District in 2005:Q2. Then, Citizens switched to the First District in 2007:Q3.

- The vast majority of CPBs are chartered in Massachusetts, and the rest are chartered in New Hampshire.

- Most SSBs and CPBs are mutual organizations in that they are owned by their depositor members, not stockholders. Therefore, they are more likely to prioritize the interests of their members over maximizing profits.

- The majority of community banks hold assets below the FDIC’s threshold value, which was indexed to $1.65 billion in 2019, for example. For a bank with assets exceeding the threshold to be designated a community bank, it must satisfy additional criteria that include having no more than the maximum number of offices (which was set to 94 in 2019) and operating in three or fewer states and two or fewer large metropolitan statistical areas (MSAs, which are cities and surrounding communities that are linked by social and economic factors). Details on the criteria for the community bank designation can be found on the FDIC’s website at https://www.fdic.gov/resources/community-banking/cbi-data.html.

- The share of community banks remained stable in New England over this period but slipped by about 2 percentage points in the rest of the country.

- Given the extensive literature on small business lending, it is far beyond the scope of this brief to cite even all the major studies. Thus, only a few especially relevant and more recent studies are listed here. For example, DeYoung et al. (2015) show that despite a substantial decline in business credit during the Great Recession, strategically focused community banks maintained higher levels of lending to small businesses. Berger et al. (2005) test the comparative advantage of relationship lending of small versus large banks. Berger and Udell (2006) and DeYoung, Hunter, and Udell (2004) both discuss smaller banks’ strategic advantage in relationship lending. Holod, Peek, and Torna (2024) is a recent study quantifying the value of small business relationship lending.

- This pattern has remained essentially unchanged from the pre-pandemic economic recovery period of 2010 through 2019.

- The HHI is defined as the sum of the squared market share (typically as a percentage) of each firm competing in a given market. For more details, see https://www.justice.gov/atr/herfindahl-hirschman-index. This measure, therefore, depends on the market definition. It is beyond the scope of this brief to examine the extent to which a county is the appropriate geographic area for defining a local market, and which types of depository institutions besides banks (such as credit unions) and which nondepository institutions (such as money market mutual funds) should be considered competitors.

- The Federal Reserve, the FDIC, and the Office of the Comptroller of the Currency jointly issued “Third-Party Risk Management: A Guide for Community Banks,” which is available at https://www.occ.gov/news-issuances/news-releases/2024/pub-third-party-risk-management-guide-for-community-banks.pdf. See also the white paper issued by the Federal Reserve studying the benefits, risks, and challenges concerning community banks’ partnerships with fintech firms. It is available at https://www.federalreserve.gov/publications/files/community-bank-access-to-innovation-through-partnerships-202109.pdf.

References

Berger, Allen N., Anil K. Kashyap, Joseph M. Scalise, Mark Gertler, and Benjamin M. Friedman. 1995. “The Transformation of the U.S. Banking Industry: What a Long, Strange Trip It’s Been.” Brookings Papers on Economic Activity 1995(2): 55–218. https://www.brookings.edu/articles/the-transformation-of-the-u-s-banking-industry-what-a-long-strange-trip-its-been/

Berger, Allen N., Nathan H. Miller, Mitchell A. Petersen, Raghuram G. Rajan, and Jeremy C. Stein. 2005. “Does Function Follow Organizational Form? Evidence from the Lending Practices of Large and Small Banks.” Journal of Financial Economics 76(2): 237–269. https://doi.org/10.1016/j.jfineco.2004.06.003

Berger, Allen N., and Gregory F. Udell. 2006. “A More Complete Conceptual Framework for SME Finance.” Journal of Banking Finance 30(11): 2945–2966. https://doi.org/10.1016/j.jbankfin.2006.05.008

DeYoung, R., Anne Gron, Gökhan Torna, and Andrew Winton. 2015. “Risk Overhang and Loan Portfolio Decisions: Small Business Loan Supply before and during the Financial Crisis.” The Journal of Finance 70(6): 2451–2488. https://doi.org/10.1111/jofi.12356

DeYoung, R., W. C. Hunter, and Gregory F. Udell. 2004. “The Past, Present, and Probable Future for Community Banks.” Journal of Financial Services Research 25(1): 85–133. https://link.springer.com/article/10.1023/B:FINA.0000020656.65653.79

Holod, Dmytro, Joe Peek, and Gökhan Torna. 2024. “Relationship Lending: That Ship Has Not Sailed for Community Banks.” Federal Reserve Bank of Boston Working Paper 24-5. https://doi.org/10.29412/res.wp.2024.05

Kroszner, Randall S., and Philip E. Strahan. 1999. “What Drives Deregulation? Economics and Politics of the Relaxation of Bank Branching Restrictions.” The Quarterly Journal of Economics 114(4): 1437–1467. https://doi.org/10.1162/003355399556223

About the Authors

About the Authors

J. Christina Wang,

Federal Reserve Bank of Boston

J. Christina Wang is a principal economist and policy advisor in the Federal Reserve Bank of Boston Research Department.

Email: Christina.Wang@bos.frb.org

Acknowledgments

The author thanks Daniel Cooper, Giovanni Olivei, Joe Peek, Jenny Tang, Egon Zakrajšek, and other colleagues for helpful suggestions, and she thanks Calvin Zhang for assistance creating the map for Figure 7.

Resources

Keywords

- New England ,

- NEPPC Regional Brief ,

- community banks ,

- small business credit