Cash keeps going strong despite worthy challengers

Alternative payment methods are everywhere, but cash remains a top choice

SARINYAPINNGAM/Getty Images

{kind=link}

The end of cash has been predicted with roughly the same frequency and accuracy as the end of the world. But is it possible that today cash is really on the ropes?

Online shopping continues to accelerate, businesses that don’t accept cash look to be cropping up everywhere, and doesn’t it just seem like people aren’t using cash that much anymore? Combine all this, and maybe it’s logical to conclude cash is in big trouble.

But that doesn’t mean it actually is.

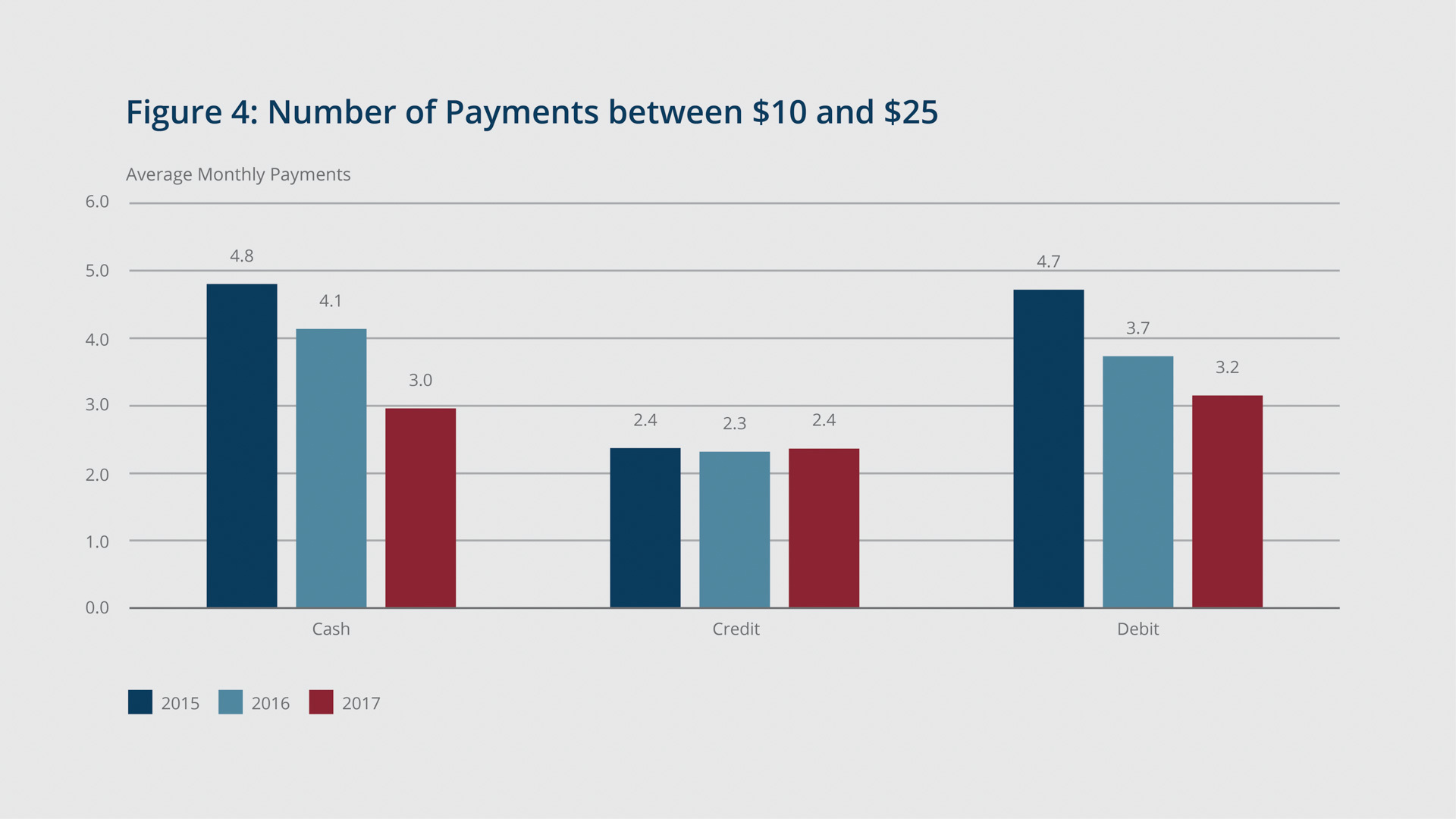

Cash is used in 26 percent of transactions, making it the second-most frequent payment method in the U.S., according to Federal Reserve research. It’s particularly prevalent in small-value transactions, as it’s used in 42 percent of transactions under $10. Cash is also still significantly used across age groups, and it’s the top choice for so-called "everyday" purchases, as it's used two-thirds of the time for items including food, personal care supplies, items related to automobiles, and general merchandise.

“Cash is alive and well,” said Boston Fed Cash department Vice President Leah Maurer in an interview just before she retired this spring. “It’s still there and it’s going to be there.”

{kind=link}

Source: 2018 Findings From the Diary of Consumer Payment Choice

The demand for cash keeps rising

The amount of cash in circulation speaks to the continuing demand for it. For instance, at the Boston Fed alone:

- An average of 5.2 million banknotes worth $88 million are received per day.

- A single stack made up of each coin bagged in the Boston vault would be 171 miles high.

- If each bank note in the Boston vault was laid side-by-side, it would extend 39,784 miles, enough to circle the globe more than 1.5 times.

Meanwhile, the value of U.S. currency globally has risen steadily for years. At the end of 2018, there were 43.4 billion notes in circulation, up from 41.6 billion a year earlier, and the value of that currency was roughly $1.7 trillion at year’s end, compared to about $1.6 trillion in December 2017.

The latest Diary of Consumer Payment Choice, which is published by the San Francisco Fed, indicates cash was used in 26 percent of transactions in 2018, second to debit cards, which were used 28 percent of the time, and ahead of credit cards (23 percent).

But the diary also indicated that both cash and debit card use were down from 2015, when they were used in 33 percent and 30 percent of transactions, respectively, while credit card and electronic payments have ticked up. Still, electronic payments remain a relatively small piece of the payments pie, clocking in at 11 percent of all transactions.

Maybe that’s hard to believe, given the prevalence of online options from retailers large and small. But the numbers say that even younger consumers use cash more than twice as much as electronic payments. According to the diary, millennials ages 25 to 34 are the least frequent users of cash. Those consumers averaged 37 payments per month in 2018, and choose cash for just seven of them. But that’s still far more than the three times per month they chose electronic payments. Debit cards (13 payments) and credit cards (11 payments) were their top payment choices.

{kind=link}

Source: 2018 Findings From the Diary of Consumer Payment Choice

Privacy and reliability are big reasons for cash’s appeal

The Boston Fed’s Lisa Perlini, who replaced Maurer as vice president in Boston’s Cash Services, thinks the privacy that comes with using cash is a big part of its appeal, and reliability is also a major factor. She recalled being at a large retail chain when their credit and debit card system went down. Some people left their carts in the aisle and left the store, but she had the cash to finish shopping.

Maurer added the reality is that electronic systems fail, even in a digital age.

“When systems are down, cash gets the job done,” she said. “So you can always rely on it.”

That’s become less true in some quarters, as various merchants refuse to take cash, citing factors like more efficiency in payments, less hassle handling money, and lower risk of robbery. Massachusetts is the only state in the U.S. that requires retailers to accept cash, but there’s been a pushback against the “cash-not-accepted” trend, with some saying it discriminates against people without bank accounts or credit cards, or against those who want their transactions to stay private. City council leaders in New York, Washington, D.C., and Philadelphia have all proposed legislation that forbids restaurants and retailers from refusing cash.

Perlini said despite cash’s resiliency, the idea that cash is on its way out will likely persist.

“You can go back decades and find covers of magazines that tell you, ‘Cash is dead,’” she said. “But the reality remains that people like cash, and they need it.”

About the Authors

About the Authors

Jay Lindsay is a member of the communications team at the Federal Reserve Bank of Boston.

Email: jay.lindsay@bos.frb.org

Site Topics

Keywords

- cash demand ,

- cash ,

- payments ,

- mobile payments ,

- consumer payments ,

- digital payments ,

- Faster payments ,

- electronic payments