Latest NE payments survey shows growth in peer-to-peer services, shifting fraud concerns

Worries about Card Not Present fraud reflect uptick in online purchases

Getty Images/iStockphoto

{kind=link}

More New England banks than ever are offering mobile peer-to-peer payment services, the kind friends use to settle a bill at a restaurant.

But few financial institutions are promoting contactless cards – though that could be changing in a time of COVID-19.

And the biggest security worry for banks and credit unions isn’t vulnerabilities caused by customers anymore. It’s about fraud that happens when plastic debit or credit cards are nowhere to be seen.

Those were a few key findings of the 2019 Mobile Banking and Payment Survey of New England Financial Institutions. This year’s regional report is part of a broader Federal Reserve survey of banking and mobile payments attitudes and developments across the U.S.

The answers from 130 respondents across the six New England states mirror those from across the U.S., said Marianne Crowe, a vice president at the Federal Reserve Bank of Boston, a payments expert, and co-author of the regional report.

“What you are seeing in New England is what you are seeing around the country,” she said.

Zelle paves the way for higher P2P payment services adoption

The report, which Crowe co-wrote with Breffni McGuire, a principal at BMCG Consulting, notes that digital peer-to-peer, or P2P, payment services are starting to displace cash and checks for personal transactions.

PayPal and Venmo are two well-known P2P services, but since the last Fed survey in 2016, the Zelle network has emerged to help banks compete with them. Zelle was originally developed by a security organization called Early Warning Services so the larger banks it served could move money to each other. Today, the network is accessible to any financial institution.

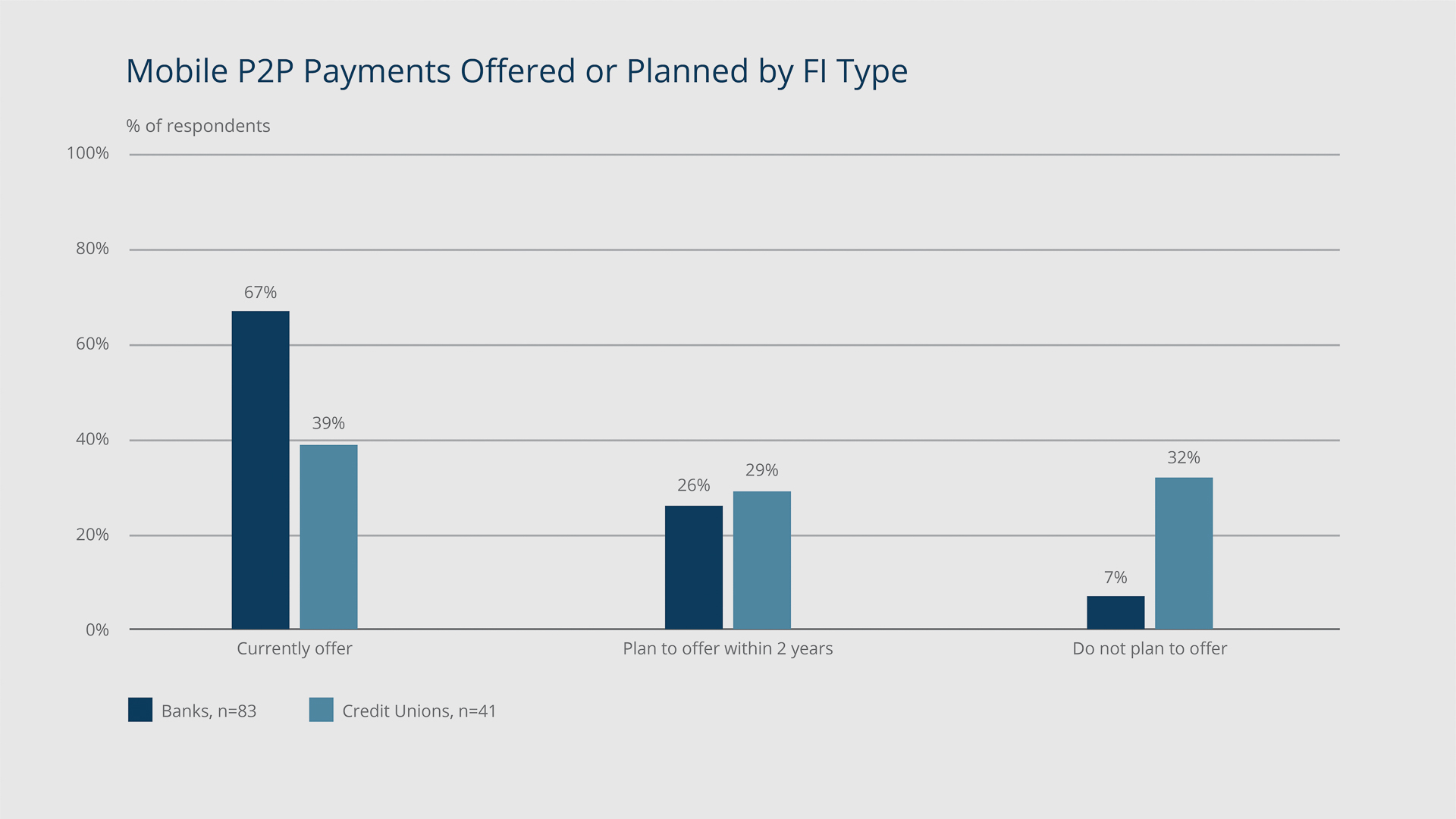

According to the survey, 67% of banks offer mobile P2P payment services, a 13% increase from 2016. Of those banks that don’t, 26% of banks planned to offer mobile P2P payments by 2021. Meanwhile, 39% of credit unions offer P2P services, and 29% plan to offer them by 2021.

“The biggest change I think had to do with Zelle, because it is a bank-driven, bank-owned, P2P mobile service,” Crowe said. “I think that has brought it to the attention of smaller banks and credits unions.”

{kind=link}

Michael Konstansky/Federal Reserve Bank of Boston

Contactless cards not catching on – yet

Interest in contactless cards, meanwhile, was tepid when the survey was taken. But that was before the onset of the COVID-19 pandemic, and there are indications the virus is changing attitudes toward contactless cards.

The cards themselves look identical to regular plastic debit or credit cards but communicate to payment terminals through an antenna in their chips when customers “tap to pay.” Some experts think they can pave the way for higher digital wallet adoption, since the wallets also use “tap to pay,” only via mobile phone. They say more digital wallet use would increase overall payments security because of the superior biometric and passcode protections on most phones.

Just 7% of banks and 4% of credit unions surveyed offered contactless cards, and only 46% of banks and 31% of credit unions plan to offer them in the next five years, according to the survey. But Crowe noted that public health guidelines that recommend reducing physical contact between people and even objects during the pandemic could increase contactless card appeal. A study by Forrester and the National Retail Federation points to an increased use of touchless payment options, including contactless cards, since the pandemic began.

“I think more financial institutions, including the smaller organizations, are starting to see contactless cards as a future strategy,” Crowe said.

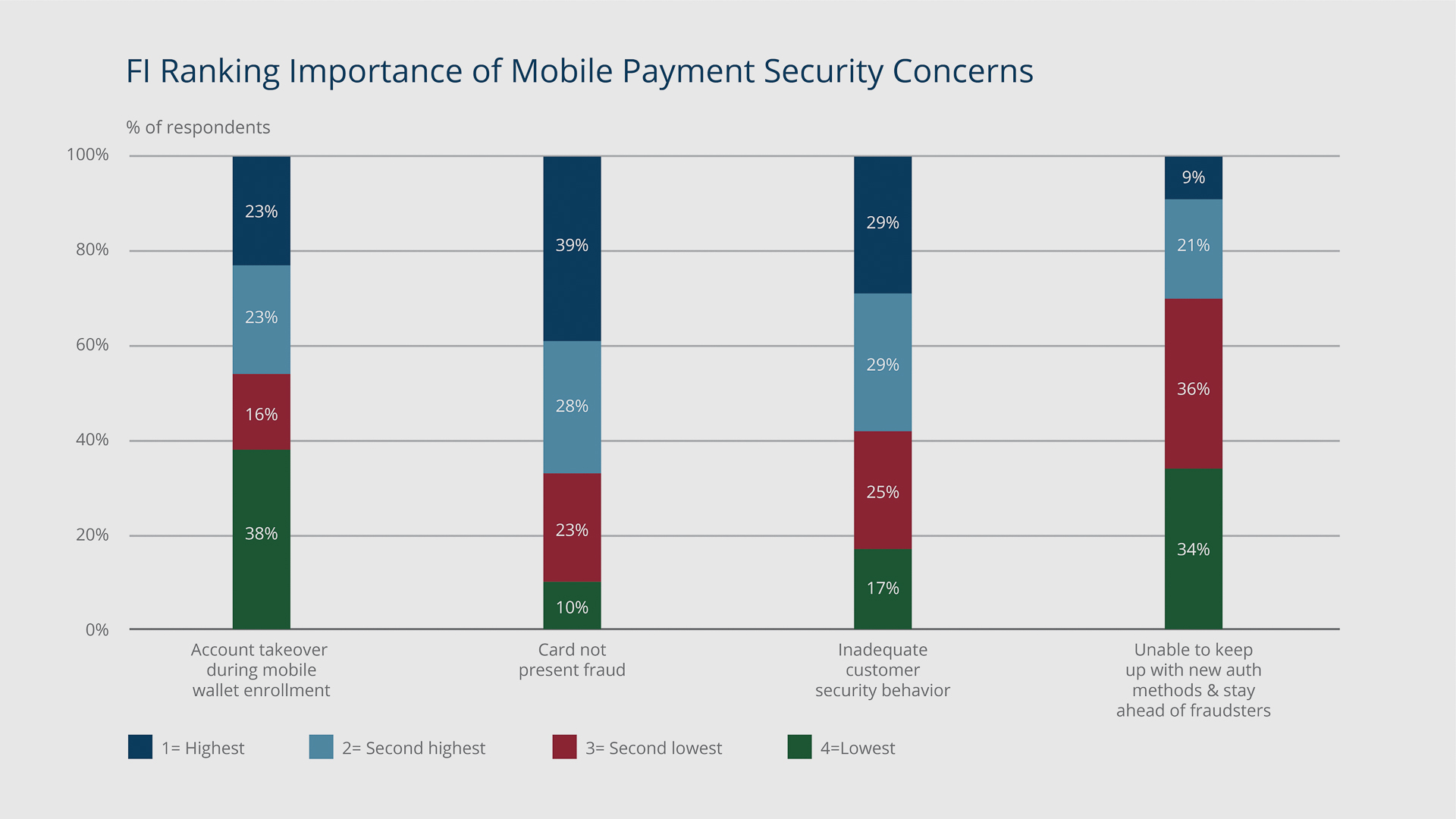

Card Not Present fraud emerges as top concern

Payment security is a perpetual concern, but the latest survey shows the primary worry of financial institutions has shifted since 2016. Then, they were most worried security would be compromised by their own customers’ behavior – for example easily cracked passwords that could give fraudsters access to their sites. Now, the top concern is “card not present” fraud, or CNP fraud, which happens on online or phone transactions, when the card isn’t physically present during the sale, but a thief obtains a consumer’s card number.

CNP fraud was the highest concern of 39% of respondents, while 29% were most concerned about “inadequate customer security behavior.” Crowe said banks have developed new ways to prevent fraud caused by consumer behavior, even as online transactions continue to increase, and that may explain the change.

“The fraudsters always go where there’s more money, so they’re increasingly shifting online, because the volume there continues to grow,” Crowe said. “Meanwhile, fraud protection tools are inconsistent, creating vulnerabilities that fraudsters take advantage of.”

{kind=link}

Michael Konstansky/Federal Reserve Bank of Boston

Pandemic may permanently increase use of mobile payments

Crowe said the pandemic is spurring behavior changes that may permanently make paying through a mobile device much more common.

The survey indicated 79% of banks and 57% of credit unions offered, or planned to offer, mobile payment/wallet services for retail customers by 2021. Crowe said those percentages could increase, as social distancing practices adopted during the pandemic force some consumers to rely more on mobile payments. As they become more comfortable, paying with mobile may become their preferred method.

“Some people ask, ‘Is this sustainable?’ I think it is,” she said. “It’s convenient. It’s easy. Why would you stop doing it down the road, even if you don’t have the health issues you have now?”

Read the New England report on the 2019 survey here.

About the Authors

About the Authors

Jay Lindsay is a member of the communications team at the Federal Reserve Bank of Boston.

Email: jay.lindsay@bos.frb.org

Site Topics

Keywords

- mobile banking ,

- consumer mobile ,

- NFC mobile payments ,

- mobile payments ,

- mobile survey ,

- fraud mitigation ,

- payments fraud ,

- fraud trends