Addressing the Economic Effects of the COVID-19 Pandemic

A perspective from Eric Rosengren, president and CEO of the Federal Reserve Bank of Boston

Peter Davis/Federal Reserve Bank of Boston

April 1, 2020

Webinar

Addressing the Economic Effects of the COVID-19 Pandemic

Greater Boston Chamber of Commerce

{kind=link}

Just 20 days ago, Dr. Paul Biddinger and I urged employers to prepare for the gathering storm by taking tangible steps, like implementing work-from-home and restricting business travel, to prevent more devastating health and economic outcomes from the pandemic.

Today, we’re witnessing the pandemic’s stark effects on public health. Meanwhile, the necessary response – social distancing – has stilled our strong economy, disrupting countless lives and livelihoods. It’s also been distorting the credit and liquidity flows that underpin our economy, threatening the greater pain of a full-blown financial crisis.

But everybody can help mitigate the pandemic’s impact. Public health officials and heroic front-line medical personnel play the most important part. Governments, civic organizations, scientific and educational institutions, and citizens also have key roles to play. And fiscal policy is crucial.

At the central bank we’re focused on addressing, and blunting, the economic effects of the pandemic. The Federal Reserve has acted quickly to address spillovers from the economic disruption. I’d like to explain some of what the Fed did, and suggest other steps that a range of parties could pursue.

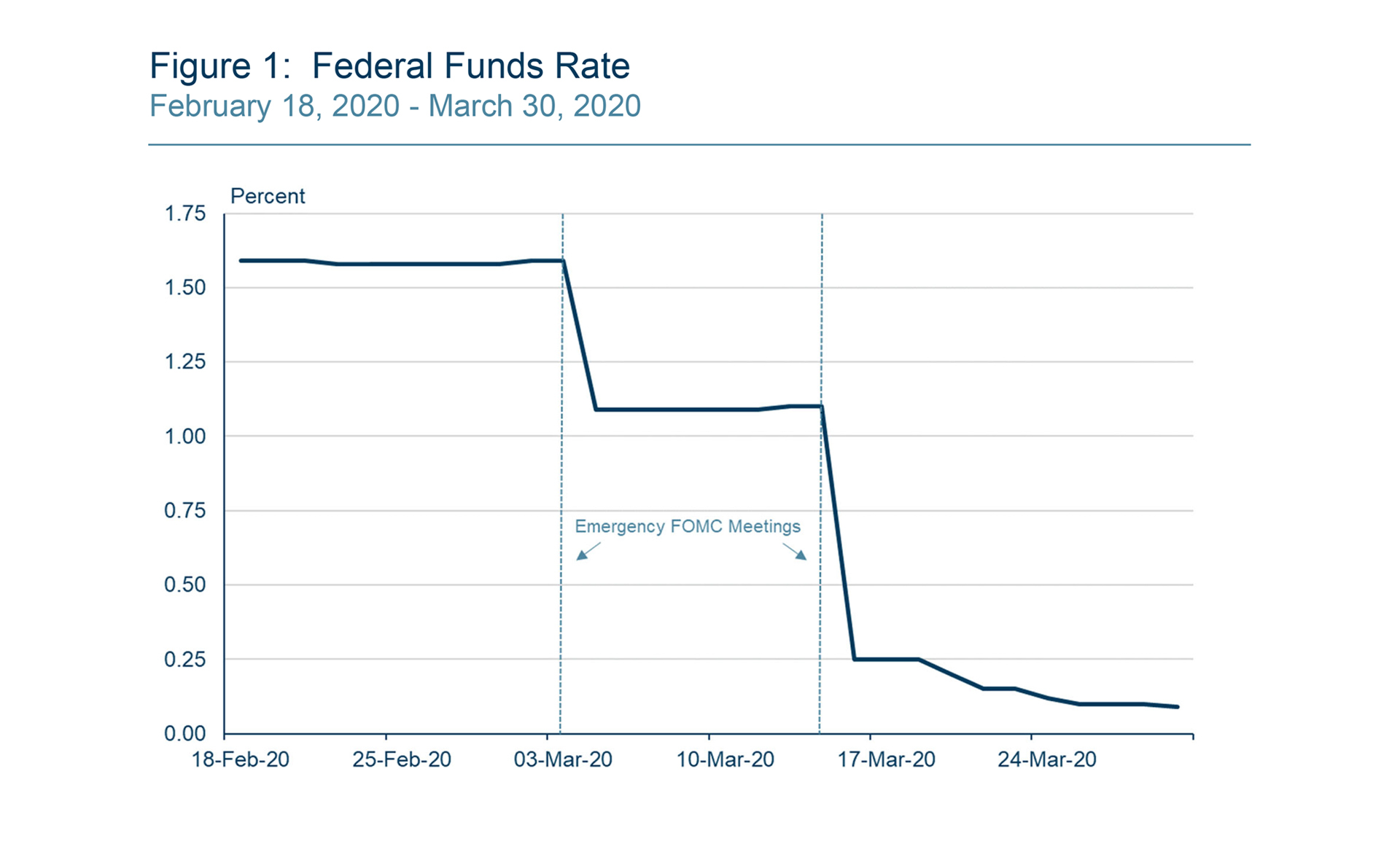

The Federal Reserve is working to limit the financial and economic distress – to take actions that help avoid even higher levels of unemployment or a slower recovery. To that end, the Fed’s interest-rate-setting committee cut the short-term rates the Fed controls to close to zero to help ease market interest rates in an economy suddenly facing challenges (see Fig. 1).

{kind=link}

Federal Reserve Bank of Boston

Further, both the Treasury and mortgage-securities markets had too many people and institutions seeking to sell assets to raise cash (rushing to more liquid assets as a crisis response), resulting in an inability to trade, and unusual volatility. To remedy distortions in these important markets, the Fed has been buying Treasuries and mortgage-backed securities to stabilize markets and make it easier for financial institutions to pass through lower interest rates to consumers and businesses.

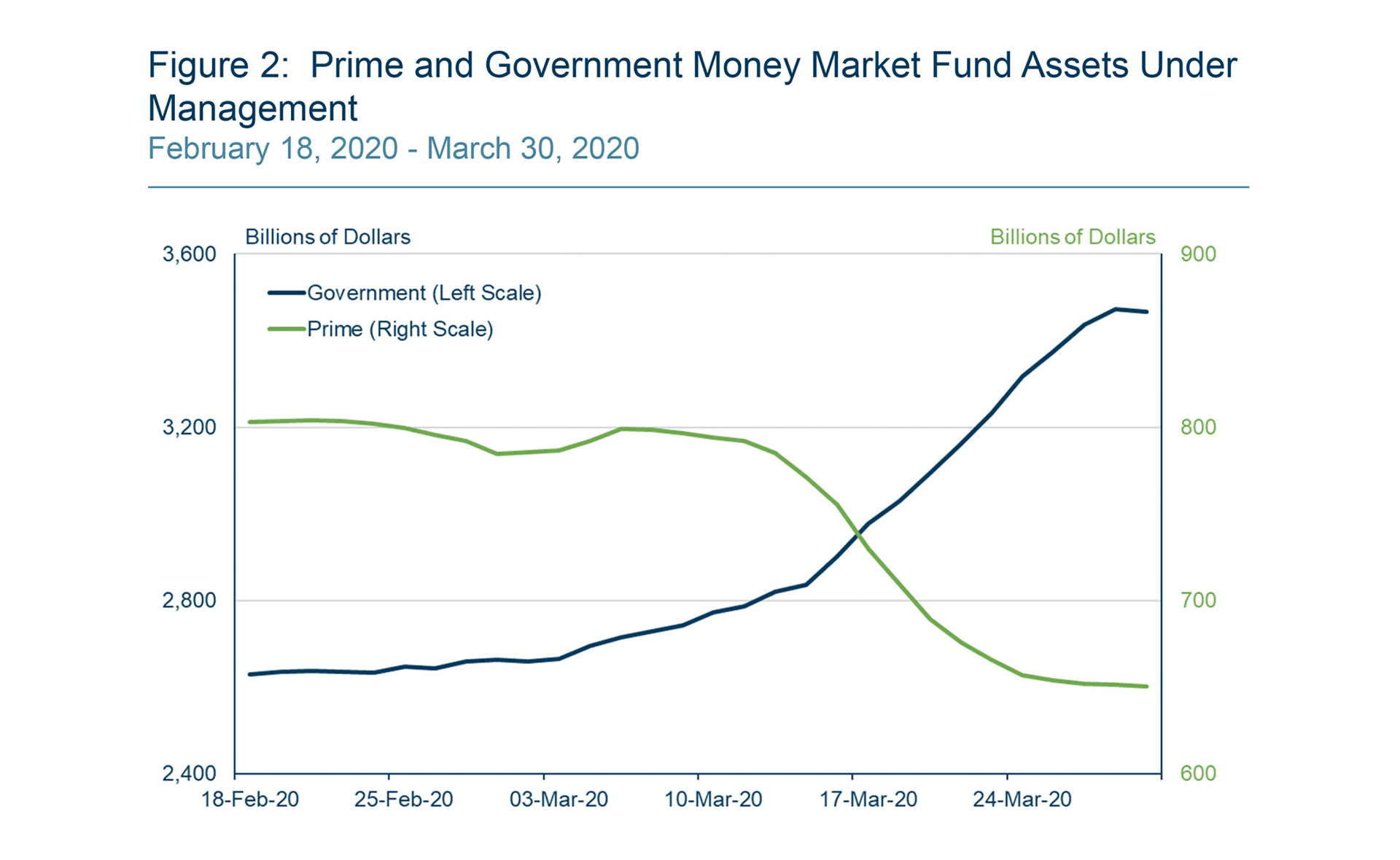

In addition, many firms and individuals keep liquid assets in money market funds, and there was a danger of seeing funds gated or closed as investors rushed to pull cash from them (see Fig. 2). Similarly, the municipal money market funds that buy short-term, highly-rated municipal securities and help meet the short-term funding needs of municipalities were seeing few trades. In sum, given the rush for cash in financial markets, it was proving a challenge for the funds to sell high-quality debt of even the strongest companies and states. The Boston Fed opened a facility that lends money to banks, so they can buy these highly-rated assets from money market funds. This ensures money market funds can meet the demands of individuals and firms seeking to redeem cash, restores a market for short-term high-quality assets, and addresses the liquidity problem impacting individuals, companies, and local governments.

{kind=link}

Federal Reserve Bank of Boston

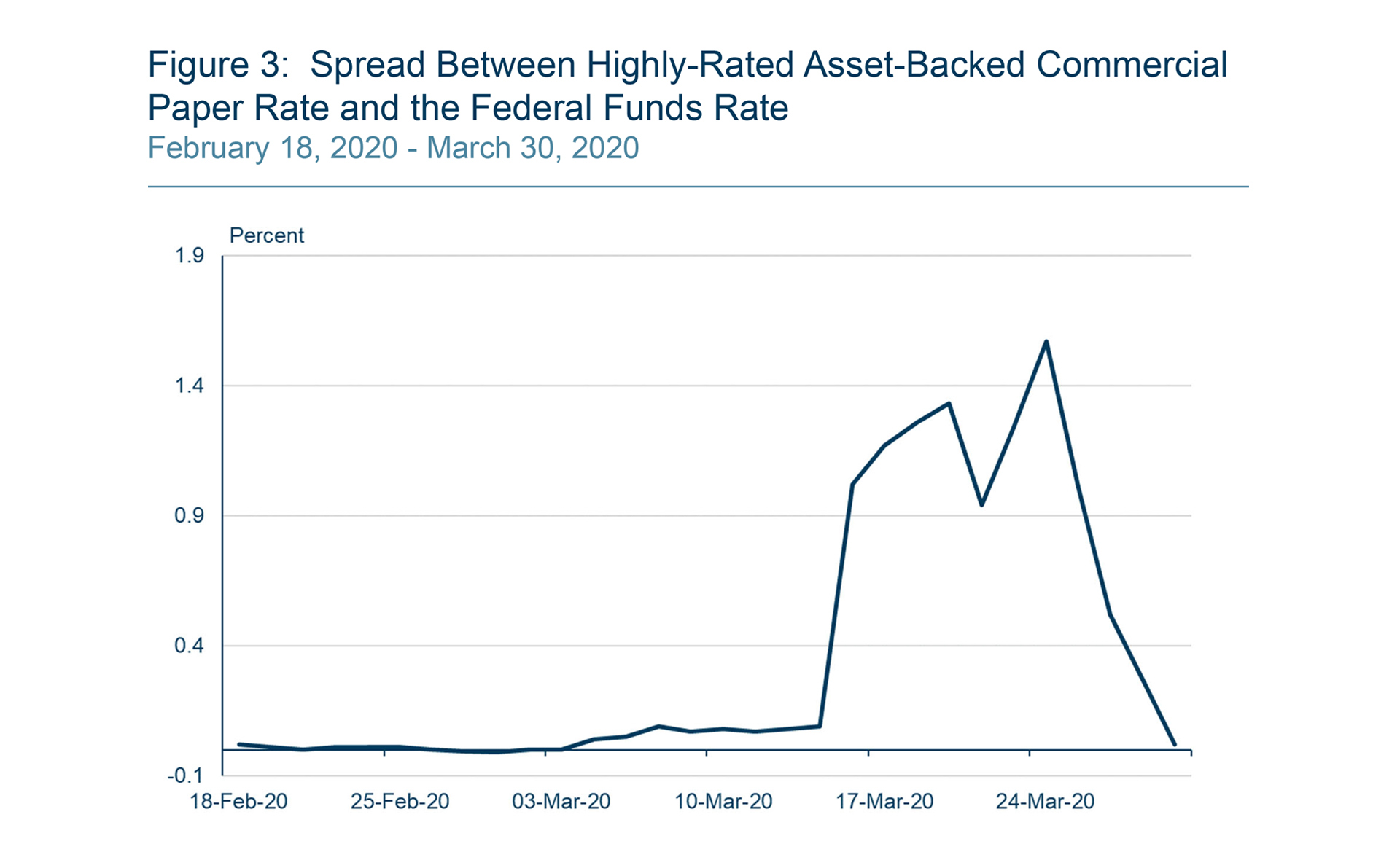

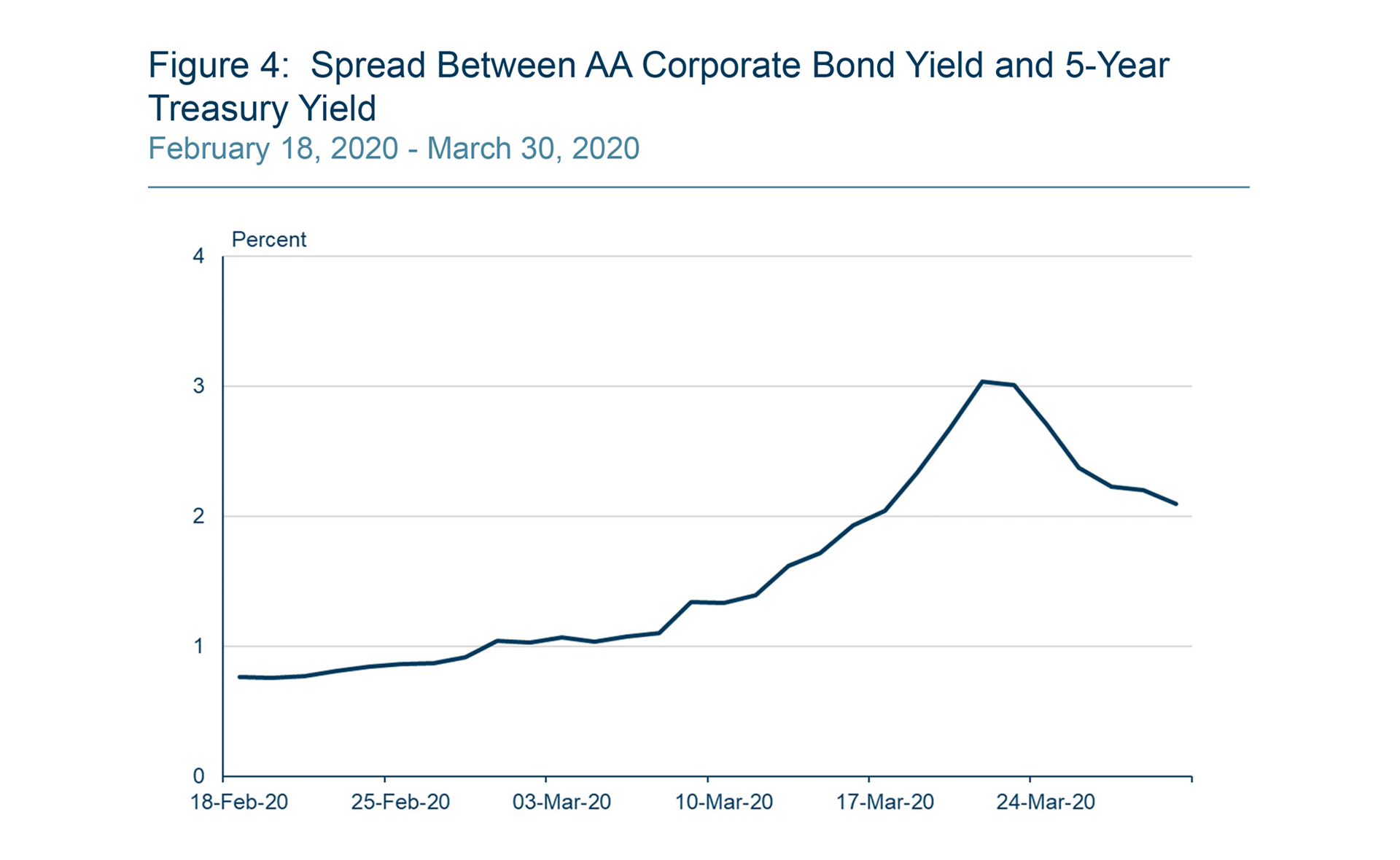

Also, the New York Reserve Bank is running a facility to buy short-term high-quality assets of firms – helping trading to resume and supporting firms’ ability to issue short-term debt. It is important for economic functioning that firms have access to funding. The New York Fed is establishing facilities for firms to issue debt and for secondary trading of debt. (see Figs. 3 & 4)

{kind=link}

Federal Reserve Bank of Boston

{kind=link}

Federal Reserve Bank of Boston

Meanwhile, problems threatened to ripple through banking markets as business closures and layoffs spiked. To meet the increased demand for liquidity, the Federal Reserve is providing collateralized loans to banks so their customers – firms and individuals – have access to liquid funds. Regulatory changes will allow banks to restructure loans to help individuals and businesses with a temporary loss of revenue avoid bankruptcy and layoffs by, for instance, deferring payment of principal and interest for up to six months.

Fiscal policymakers have acted strongly with the recently passed CARES Act. We must continue to adapt as the crisis proceeds, with constant attention to the plight of workers who have been or will be laid off. Unfortunately, we expect the unemployment rate to rise dramatically.

Social distancing is needed to avoid overwhelmed medical facilities and unnecessary deaths, but it also poses great challenges for low-income workers, who are more likely to lose jobs and have few other resources. Meanwhile, furloughs have been occurring, particularly in the hotel, retail, travel and restaurant industries. We’ve already seen an unprecedented rise in initial claims for unemployment insurance.

Traditional economic models are challenged by this unique situation. To me, the most important factors are how well we avoid financial spillovers, and how effective the fiscal stimulus is, as well as the progression of COVID-19 infections. These will all impact the speed of the economic recovery. That is not a fatalistic assessment. On the contrary, it should galvanize us. In that spirit, I offer three concluding observations:

- This is a time for public-spiritedness

Our mantra at the Boston Fed is “public service that makes a difference.” Central banks can and must do a lot in crises, to alleviate stresses in the financial system we all count on, which can hurt all citizens. But everyone – in small or big ways – can do their part to make a difference. The public interest is more important than ever; social distancing is one example. What we all do now in the public interest can help recovery, once the worst is over. - This is no time to leave anyone behind

We are all being challenged right now, but our legacy can be that we rose to the challenge and kept a focus on the vulnerable, those with low and moderate income, and those whose livelihoods operate on the thinnest of margins. The long-term prosperity of our region and the people who are our neighbors (and our customers) will shape the recovery. Among other things, we need to support the workers who keep our organizations and those we rely on (like grocery stores, shipping networks, and of course health care) up and running. And we must tide over workers and businesses that see demand dry up for a while. - This is a time for our best, together

The brainpower of our region and nation is needed more than ever, and it is important to continue being nimble, creative, proactive, and, perhaps most importantly, collaborative – because the tactics and approaches that will help are likely to be multifaceted and involve the public, private, and nonprofit sectors.

This is a time of challenge, but it’s also a time to bring out our very best.

This perspective summarizes remarks delivered at a forum hosted by the Greater Boston Chamber of Commerce, held on April 1, 2020.

About the Authors

About the Authors

Eric S. Rosengren

Resources

Keywords

- credit ,

- liquidity ,

- employment ,

- interest rates ,

- money market funds ,

- COVID-19