2018 Series • No. 18–3

Current Policy Perspectives

Technology, the Nature of Information, and FinTech Marketplace Lending

Over the past 25 years, the retail lending market has undergone marked changes, many of which have been enabled by technological advances which have transformed the way that information is collected and analyzed to make decisions on consumer loans. Before this information technology (IT) revolution, loan officers, often at banks, would gather "soft" information about a potential borrower through direct interactions with the applicant, but by the mid-1990s this was largely replaced by credit bureau data, assembled primarily from digitized "hard" information about an individual's repayment history. IT's role in converting financial information from "soft" to "hard" data that can be precisely disseminated at a very low cost is a development that has altered the provision of consumer credit from the traditional bank-based model—where approving, funding, and servicing loans are tasks integrated within the same firm—to one where different firms can specialize in originating or funding loans along a credit supply chain. Because the critical component for lending decisions now revolves around the ability to create and utilize a large volume of data effectively, this change has enabled firms with a competitive advantage in generating and processing information to compete with traditional lenders.

Since 2007 a growing portion of the retail lending industry centers on FinTech, stand-alone firms that operate through online platforms and use advanced IT applications to provide financial services to consumers and small businesses. Other technology-focused firms also have data capabilities that can be applied to the retail lending market. Compared to banks, FinTech lenders have some competitive advantages: operating exclusively through an internet platform eliminates the costly need for brick-and-mortar retail locations, while their extensive IT infrastructure delivers financial services with efficiency, speed, and convenience. This paper uses FinTech firms as a case study to explore how IT changes can alter the boundary of what are regarded as financial firms, how this evolution impacts consumer lending activity more generally, and what these developments imply for financial stability in the long term.

Sign up for the latest updates on our Payments Innovation work

Key Findings

Key Findings

- Whether the IT-enabled changes in the informational structure of lending favor hierarchical large banks or new entrants, including small start-up firms, also depends on their relative funding cost. Banks, the traditional providers of consumer and small business loans, used to benefit from having a lower cost of funds, but this competitive advantage was reduced by enhanced capital requirements imposed on banks in the wake of the 2008 financial crisis, and an extended period of low interest rates. Compared to banks, online lenders face fewer regulatory constraints.

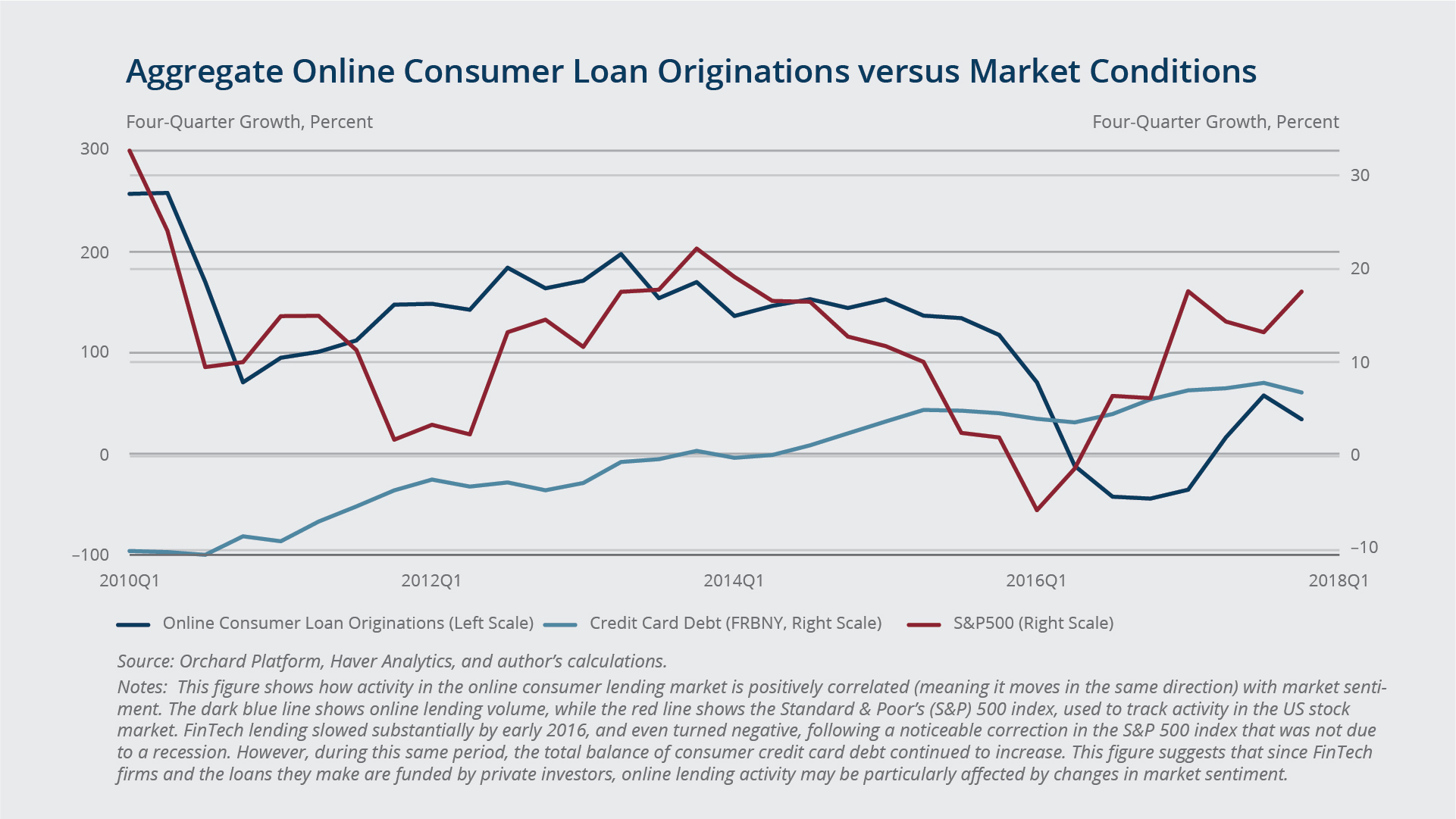

- Unlike banks, FinTech firms have no access to stable funding in the form of government-insured deposits. Most FinTech firms are financed by venture capital firms and obtain loan funding from institutional investors. Both types of investors may be inclined to scale back investment during an economic downturn. There is suggestive evidence of a positive correlation between online lending volume and market sentiment. This possibility raises a concern that at least some FinTech firms may not be able to sustain their lending operations during a recession.

Exhibits

Implications

The entrance and rapid growth of FinTech firms in retail lending is a continued manifestation of the IT-enabled evolution of lending technology. While FinTech firms have brought about greater efficiency, regulators responsible for the overall stability of the financial system should be mindful of the risk that the credit that FinTech lenders supply to consumers and small businesses may be particularly susceptible to cyclical shocks. Compared to FinTech lenders, banks play a more important role in stabilizing credit during economic downturns, barring shocks to their own capital or liquidity. Banks can also make use of these same IT advances, including through collaboration or partnership with FinTech firms, to regain some market share.

Abstract

The retail lending landscape has changed considerably over the past two decades, the most recent example being the rapid growth of online, or FinTech, lending to consumers and small businesses. This paper discusses how the boundary of the firm in the retail lending market is affected by advances in information technology that have turned what was previously soft information on borrower credit risk into encoded hard data that can be precisely transmitted across firms at a very low cost. The ability to collect and process information has become the critical resource for lending decisions, enabling entities with an advantage in producing information, such as technology firms, to compete in traditional retail lending activities. Efficiency can also be gained by relying more on hard data and firm specialization in a credit supply chain. Whether these changes favor hierarchical large banks or small start-up firms depends on their relative funding cost. In the aftermath of the financial crisis, an increase in banks' capital costs due to enhanced regulation is likely an important factor behind the faster growth of the new FinTech entrants. The need for funding to make loans means that the socially desirable objective of avoiding excessive credit contraction during economic downturns is better served in the current system by traditional banks, owing to their access to deposit insurance and the liquidity provided by the Federal Reserve. In sum, for the foreseeable future, banks will coexist as well as partner with FinTech lenders in the retail lending market. Banks' market share in loans to consumers and small businesses will likely fluctuate countercyclically.