Buy Now, Pay Later: Who Uses It and Why

{kind=link}

Federal Reserve Bank of Boston

Buy now, pay later (BNPL), a short-term, interest-free credit option for retail purchases, is becoming increasingly popular, and evidence indicates that its use is significantly higher among financially vulnerable consumers and disproportionately high among women, Black, and Latino consumers. At roughly 9 percent (as of fall 2023), the share of all consumers using BNPL is still relatively low, but it has increased about 40 percent from two years earlier.

BNPL is offered by retailers through payment platforms such as Affirm, Klarna, or Afterpay. Consumers can use the service to make online or in-store purchases and repay only their purchase amount in installments over a short period, typically four installments over six weeks. Consumers do not pay any interest as long as they make their payments on time.

BNPL can thus provide short-term credit to consumers who lack alternative sources of credit, may not have credit cards, or have low credit limits. In addition to retailers offering BNPL, many credit card issuers offer their cardholders an opportunity to split purchases into installments after the purchase. The market is constantly evolving, addressing changing consumer needs and market conditions. On May 22, 2024, the Consumer Financial Protection Bureau (CFPB) announced that BNPL lenders will be classified as credit card providers, which will allow consumers to dispute charges and demand refunds from lenders after returning products purchased with a BNPL loan.1

Sign up for Research Department Updates.

While BNPL provides consumers with flexibility and offers attractive payment alternatives, concerns have arisen about the potential risk to consumers who accumulate too much debt (CFPB 2022, 2023). Most BNPL companies recently tightened their lending criteria in response to rising delinquencies. These precautions are consistent with findings from recent reports by the CFPB and the Federal Reserve Bank of New York (Aidala et al. 2023), which show that consumers who use BNPL are more likely to be financially fragile. Despite these concerns, BNPL loans are not reported in consumers’ credit reports or reflected in their credit scores, including FICO scores, which this brief uses in its analysis.2

This brief uses data from the 2023 Survey and Diary of Consumer Payment Choice (SDCPC)3 to show that consumers who use BNPL tend to have very low credit scores, are more likely than other consumers to have filed for bankruptcy during the previous year, have low checking account balances, and are much more likely than other consumers to revolve on their credit cards, that is, to carry a balance from month to month. Given these consumers’ financial vulnerabilities, extensive or prolonged use of BNPL could worsen their financial situation.

BNPL Awareness and Use Are Growing Steadily

Starting in 2021, the SDCPC asked respondents about their awareness and use of BNPL. The same questions were repeated in three consecutive years: 2021, 2022, and 2023. The exact questions from the survey are presented in Appendix A.

{kind=link}

Federal Reserve Bank of Boston

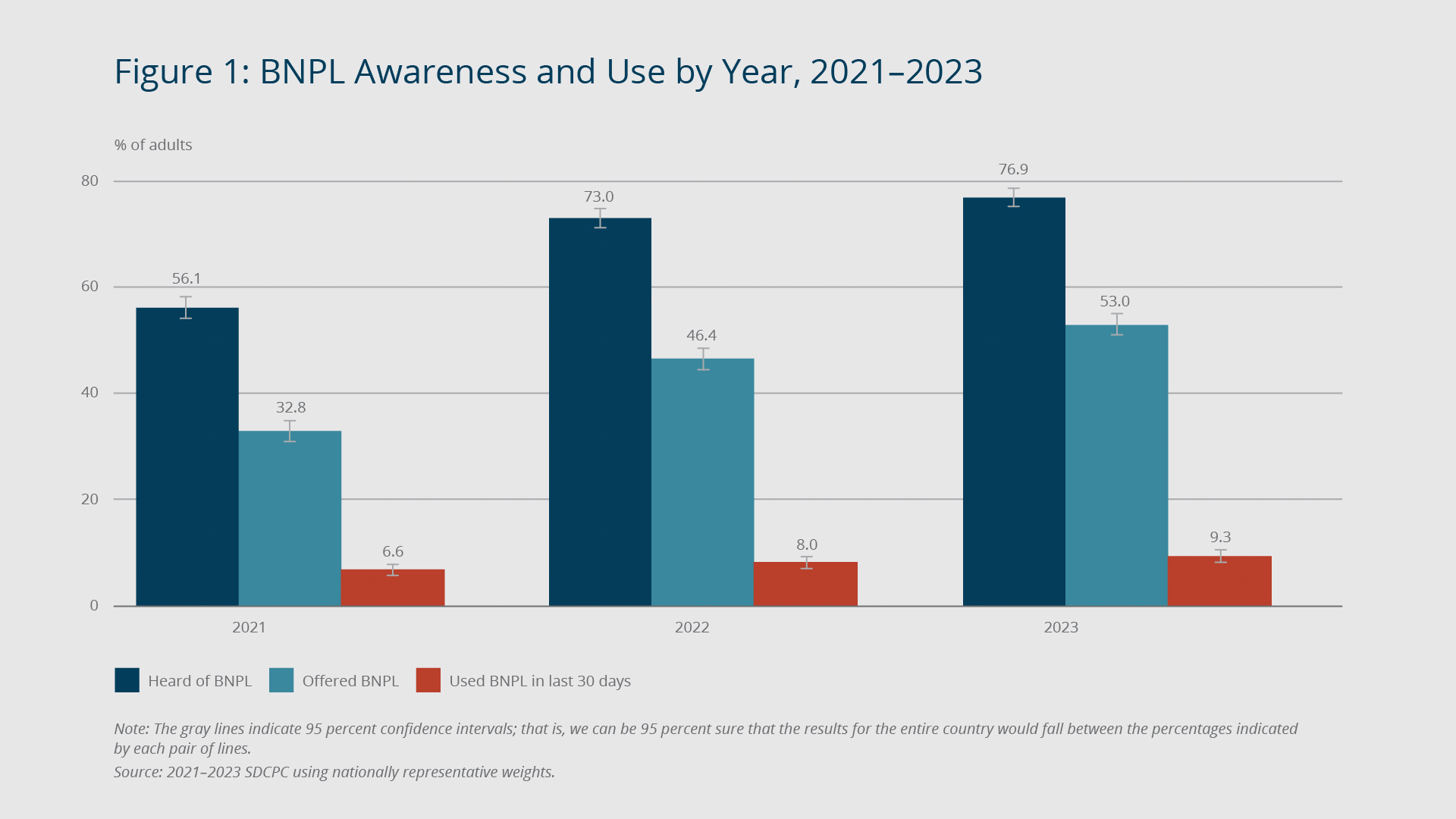

From 2021 through 2023, consumers became gradually more aware of BNPL, and the percentage of consumers who had been offered and/or used BNPL increased. The rate of use was still only 9.3 percent in October 2023, but it had risen from 6.6 percent two years earlier.4 One of the reasons for the increased popularity of BNPL was the rise in online commerce during the COVID-19 pandemic. While slightly more than half of the respondents had heard about BNPL in 2021, that share rose to nearly three-quarters in 2022 and even higher in 2023 (Figure 1).

In 2023, more than half of the respondents were offered BNPL in the 30-day period leading up to when they took the survey, compared with only one-third in 2023. By comparison, 43 percent of credit cardholders (and 35 percent of all consumers) revolved on their credit cards in 2023. Similarly to credit card revolvers, BNPL users tend to repeat their behavior over time: 55 percent of consumers who used BNPL in 2023 had also used it in at least one of the preceding two years.

BNPL Users Have Fewer Liquid Assets, More Debt

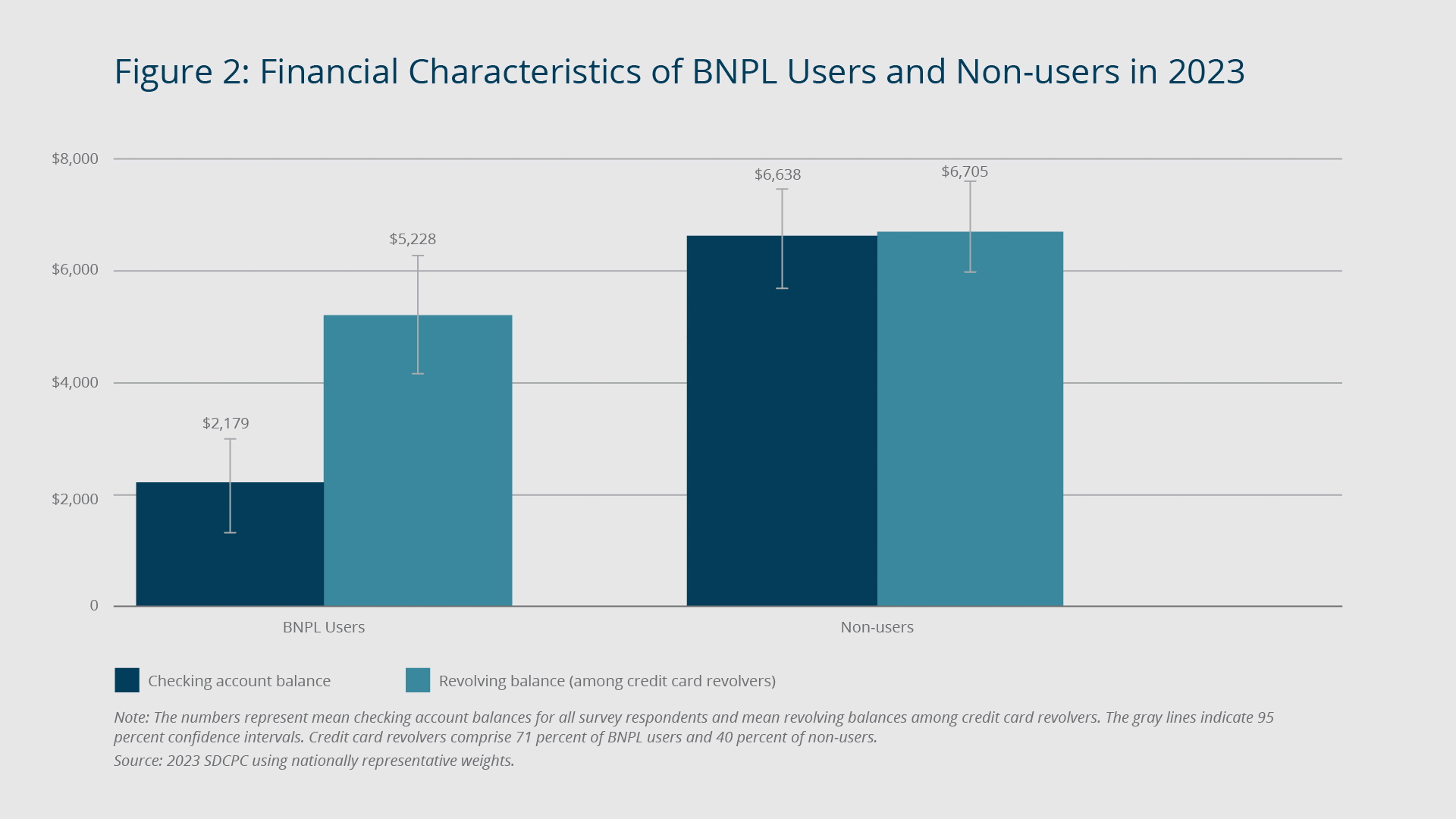

BNPL users have significantly less money in liquid assets compared with non-users, as indicated by their respective checking account balances (Figure 2): On average, a BNPL user has $2,179 in their checking account, whereas other consumers have an average of $6,638. While users and non-users are equally likely to have a credit card, BNPL users are significantly more likely to revolve on their credit cards: 71 percent of users revolved on their credit cards in 2023, compared with 40 percent of non-users. As a result, users are likely to accrue high interest costs on every dollar they charge on their credit cards. They are also likely to have reached the credit limits on their credit cards, preventing them from further borrowing.5

{kind=link}

Federal Reserve Bank of Boston

Among revolvers, non-users of BNPL carry higher unpaid balances on average—$6,705 compared with $5,228 for users. However, the average non-user (with or without a revolving balance) has a much higher checking account balance than the average BNPL user, so non-users are less likely to carry unpaid credit card debt and are in a better position to repay it.

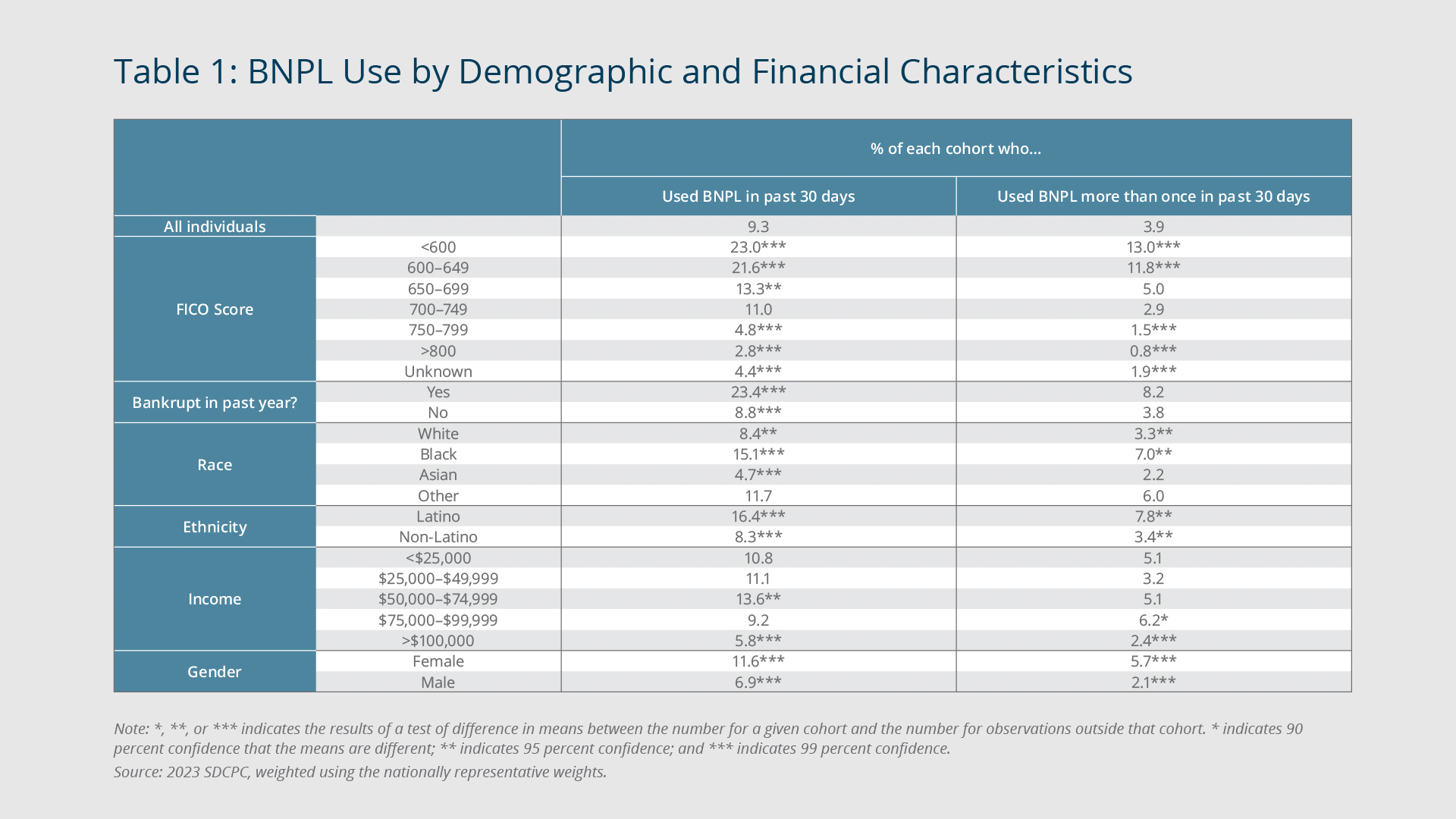

BNPL use varies significantly across demographic groups. Table 1 shows, by selected demographic and income characteristics, the percentage of consumers who used BNPL at any point during the 30 days before taking the survey and the percentage who used it more than once during that period. Low credit scores and past bankruptcy filing are the factors correlated most strongly with BNPL use, perhaps because those factors are likely to prevent consumers from obtaining other forms of credit, making BNPL especially appealing to them.

{kind=link}

Federal Reserve Bank of Boston

Consumers with low FICO credit scores are significantly more likely to use BNPL than those with higher scores: 23 percent with credit scores below 600 and 21.6 percent with credit scores between 600 and 650 used BNPL at least once, compared with only 2.8 percent with credit scores higher than 800. (FICO scores range from 300 to 850.)

Similarly, 23.4 percent of consumers who declared bankruptcy at some point during the previous year used BNPL at some point during the 30 days before taking the survey. High-income consumers are significantly less likely to use BNPL, but the use is most common among members of the middle-income group, those earning $50,000 to $75,000 a year. Women, Black, and Latino consumers are significantly more likely to use BNPL compared with consumers who are, respectively, men, not Black, and not Latino.

Less than 4 percent of the respondents used BNPL two or more times during the 30 days leading up to the survey. As with single use of BNPL, consumers with low credit scores, women, Black, and Latino individuals are more likely to be frequent users.

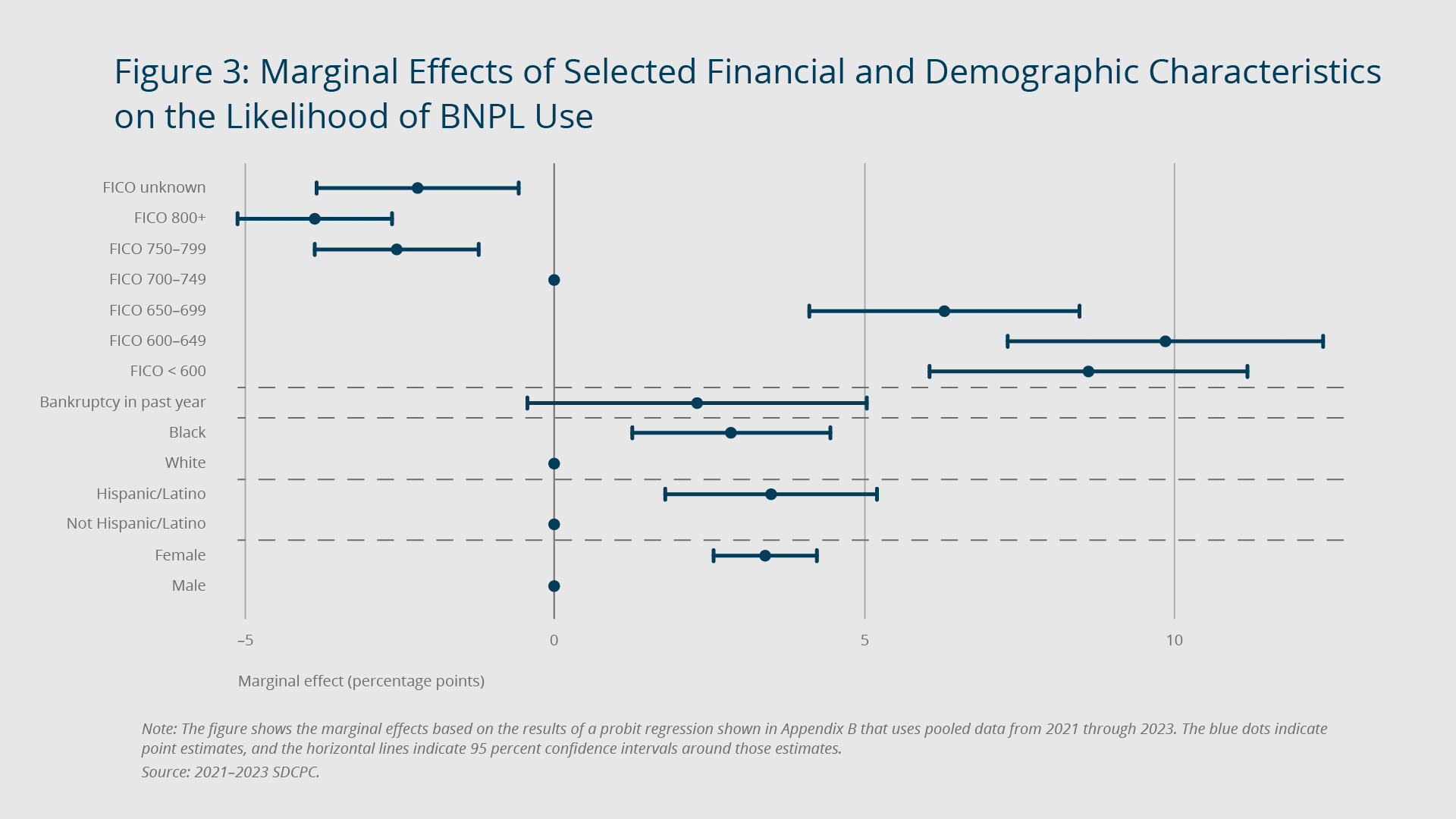

Credit Score Is the Strongest Predictor of BNPL Use

In addition to studying the summary statistics from the SDCPC, I conducted regression analysis using the survey data to estimate the marginal effects that selected financial and demographic characteristics have on the likelihood that consumers use BNPL. Appendix B describes the analysis in more detail and shows the results for each of the three years (2021 through 2023) as well as the results for the entire three-year period.

Figure 3 shows the marginal effects of selected variables on the probability of using BNPL based on the pooled 2021–2023 data. A consumer’s credit score is the most important factor predicting BNPL use, even after the analysis controls for income, education, and race. Consumers with FICO scores lower than 700 have a significantly greater probability of using BNPL compared with consumers with higher credit scores—6 to 10 percentage points greater than consumers with baseline credit scores of 700 to 749. By contrast, consumers with FICO scores higher than 750 have a significantly lower probability of using BNPL. Moreover, the effect of credit scores on the probability of using BNPL increases over time (Appendix B).

{kind=link}

Federal Reserve Bank of Boston

Having filed for bankruptcy in the previous year also increases the probability of using BNPL, although the effect is small when credit scores are included in the regression because a consumer’s credit score already reflects the impact of the default.6 Consistent with the findings from the survey’s summary statistics, the regression estimates indicate that Black, Latino, and female consumers are significantly more likely to use BNPL compared with their counterparts, even when the analysis controls for financial and other demographic characteristics including in income, employment status, and educational attainment.

The views expressed herein are solely those of the author and should not be reported as representing the views of the Federal Reserve Bank of Boston, the principals of the Board of Governors, or the Federal Reserve System.

Endnotes

- See, “CFPB Takes Action to Ensure Consumers Can Dispute Charges and Obtain Refunds on Buy Now, Pay Later Loans,” Consumer Financial Protection Bureau, press release, May 22, 2024. https://www.consumerfinance.gov/about-us/newsroom/cfpb-takes-action-to-ensure-consumers-can-dispute-charges-and-obtain-refunds-on-buy-now-pay-later-loans/

- For more information about FICO scores and BNPL, see “How Will a Buy Now Pay Later (BNPL) Account Impact My FICO Scores?” MyFICO.com, https://www.myfico.com/credit-education/faq/scores/how-does-BNPL-impact-score; and Caitlin Mullen, “BNPL Remains Mainly Absent from Consumer Credit Histories,” Payments Dive , March 27, 2023, https://www.paymentsdive.com/news/bnpl-credit-reports-payments-affirm-klarna-experian-equifax-transunion-cfpb/646002. The only exception so far to BNPL loans not being included in credit reports involves Apple, which began reporting data from its BNPL program to credit bureaus in March 2024. See James Pothen, “Apple Begins Sharing BNPL Data with Experian,” Payments Dive , February 29, 2024, https://www.paymentsdive.com/news/apple-pay-later-buy-now-pay-later-bnpl-experian-credit/708838/.

- The SDCPC is a nationally representative diary survey of US adults conducted annually in October by the Federal Reserve Banks of Atlanta, Boston, and San Francisco. For more information, see Survey and Diary of Consumer Payments Choice, Federal Reserve Bank of Atlanta, https://www.atlantafed.org/banking-and-payments/consumer-payments/survey-and-diary-of-consumer-payment-choice.

- The data were collected in October of each year, and survey participants were asked if they had used BNPL in the 30 days preceding the administration of the survey. Data collected in December or January might show higher levels of use due to holiday shopping, but the survey is administered at the same time every year, so year-to-year changes are not affected by seasonal influences.

- Previous studies have found that revolvers have much higher credit card utilization—the percentage of their credit limit cardholders use—compared with cardholders who pay their balance each month, known as convenience users (Stavins 2020). Data from the 2023 SDCPC indicate that BNPL users were more likely than non-users to have paid an over-credit-limit fee for their credit card in the preceding 12 months.

- The effect of bankruptcy filing is much larger and more statistically significant when credit scores are not included in the regressions.

References

Aidala, Felix, Daniel Mangrum, and Wilbert van der Klaauw. 2023. “Who Uses ‘Buy Now, Pay Later’?”

Consumer Financial Protection Bureau. 2022. “Buy Now, Pay Later: Market Trends and Consumer Impacts.” https://files.consumerfinance.gov/f/documents/cfpb_buy-now-pay-later-market-trends-consumer-impacts_report_2022-09.pdf

Consumer Financial Protection Bureau. 2023. “Consumer Use of Buy Now, Pay Later: Insights from the CFPB Making Ends Meet Survey.” https://files.consumerfinance.gov/f/documents/cfpb_consumer-use-of-buy-now-pay-later_2023-03.pdf

Stavins, Joanna. 2020. “Credit Card Debt and Consumer Payment Choice: What Can We Learn from Credit Bureau Data?” Journal of Financial Services Research 58: 59–90. https://doi.org/10.1007/s10693-019-00330-8.

About the Authors

About the Authors

Joanna Stavins,

Federal Reserve Bank of Boston

Joanna Stavins is a former principal economist and policy advisor in the Federal Reserve Bank of Boston Research Department.

Acknowledgments

Daniel Cooper, Joe Peek, and Egon Zakrajšek provided helpful comments. Julian Perry provided excellent research assistance.

Resources

Site Topics

Keywords

- Buy now, pay later ,

- consumer credit ,

- BNPL ,

- Payment ,

- revolving ,

- Current Policy Perspectives

JEL Codes

- G21 ,

- G51 ,

- D14 ,

- E42

Citation

Stavins, Joanna. 2024. “Buy Now, Pay Later: Who Uses It and Why.” Federal Reserve Bank of Boston Current Policy Perspectives No. 24-3.