Manufacturing Gains from Green Energy and Semiconductor Spending since the CHIPS and Inflation Reduction Acts

{kind=link}

Federal Reserve Bank of Boston

The views expressed herein are solely those of the author and should not be reported as representing the views of the Federal Reserve Bank of Boston, the principals of the Board of Governors, or the Federal Reserve System.

Real investment—spending (net of inflation) on nonresidential construction, manufacturing equipment, and intellectual property products (IPP)—in the United States has grown substantially over the last few years despite the high-interest-rate environment that emerged in 2022 and is only now beginning to subside. The current strength of investment is important to policymakers because its sensitivity to interest rates makes it a key channel through which monetary policy is transmitted into the economy and because real private domestic investment constitutes 15 percent of US real GDP.

Sign up for Research Department Updates.

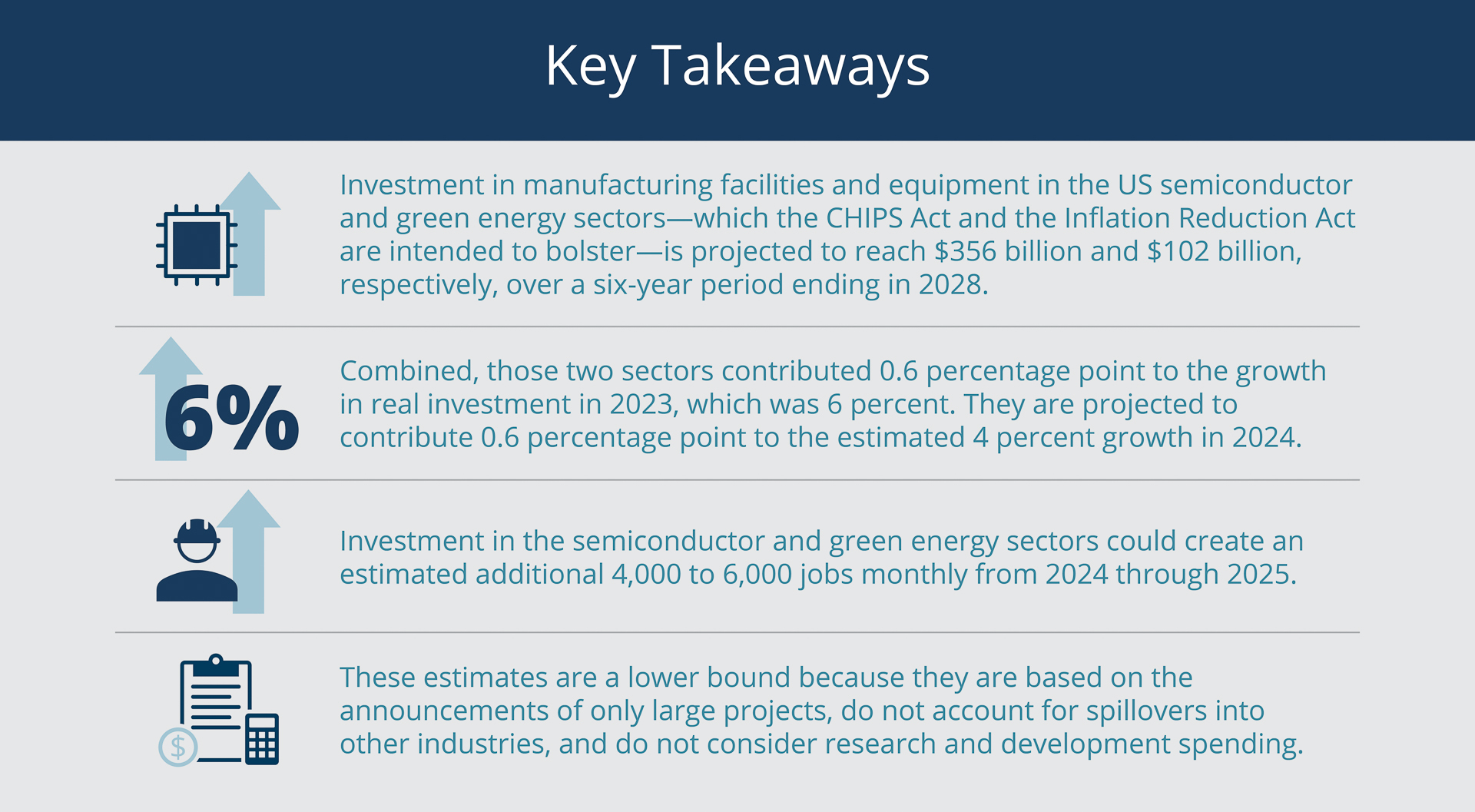

Since 2023, real investment has been boosted by spending in the semiconductor and green-energy industries that may have been spurred by enactment, in 2022, of the Creating Helpful Incentives to Produce Semiconductors (CHIPS) and Science Act and the Inflation Reduction Act (IRA). Real investment in the US semiconductor industry is projected to reach at least $356 billion over a six-year period ending in 2028, and real investment in US green energy is projected to total at least $102 billion over that period.1 Those estimates are conservative because they do not include additional spending that likely is and will continue to be substantial, such as on research and development.

I analyze how spending on the construction of and equipment for semiconductor and green energy manufacturing facilities will affect aggregate real investment, employment, and GDP. I find that investment in the construction of semiconductor and green energy manufacturing facilities has been responsible for a significant share of the recent growth in nonresidential structure investment (one-third of the growth in 2023), and it accounted for 10 percent of the growth in aggregate real investment (spending on manufacturing equipment and IPP as well as nonresidential structures) in 2023 (0.6 percentage point of the 6.0 percent growth). For 2024, projected spending on semiconductor and green energy manufacturing equipment2 will account for an estimated 15 percent of real investment growth (0.6 percentage point of the 4.0 percent growth that I estimate). Employment growth, particularly in the green energy sector, is also expected to increase as the manufacturing facilities become operational.

Potential Impact of the CHIPS Act and IRA

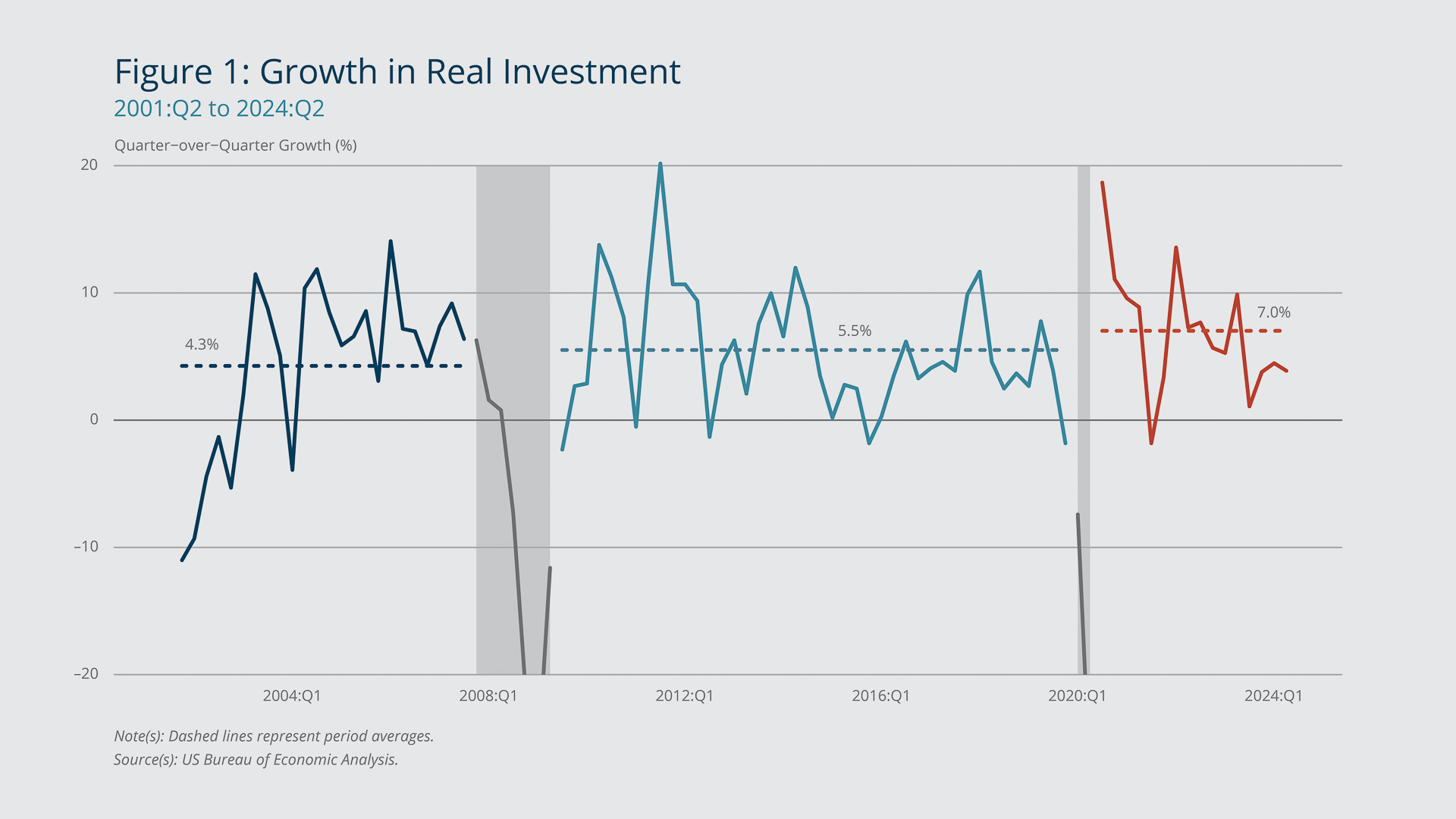

US spending on consumer goods and services remained surprisingly resilient following the onset of the COVID-19 pandemic, and the resilience of investment has been even more surprising. As Figure 1 shows, average quarterly real investment growth since early 2020 (7 percent) has been slightly faster than it was in each of the previous two decades (4.3 percent from 2000 to 2010 and 5.5 percent from 2010 to 2020). This is unexpected given the tight monetary policy environment and how elevated real interest rates result in a higher cost of capital, which is typically associated with a decrease in real private investment.

{kind=link}

Federal Reserve Bank of Boston

Growth in investment in manufacturing construction—the building of production facilities and other nonresidential structures—over the past three years has been particularly striking. According to the US Census Bureau, private manufacturing construction spending grew from $79 billion in June 2021 to $236 billion in June 2024 (equivalent to 44 percent annualized growth). Numerous reports suggest that fiscal and industrial policies are playing a major role in this boom (see, for example, Abecasus et al. 2023 and Van Nostrand, Sinclair, and Gupta 2023).

Since 2021, the US government has implemented several measures to bolster domestic investment in semiconductors and green energy, including tax credits, tariffs, export control bans, and the issuance of loans and other funding means. Most notable among these measures are the CHIPS and Science Act and the IRA, both of which were signed into law in August 2022. The CHIPS and Science Act allocates $52.7 billion to finance a 25 percent tax credit on investments in new manufacturing facilities primarily but also to fund grants, loans, and research. The IRA dedicates $369 billion over the next decade to incentivize domestic investment in green energy. It targets the supply through tax credits for producers (of solar or wind energy, for example), manufacturers (of inverters, battery components, etc.), and miners (of critical minerals). In addition, the act targets the demand side through tax credits for businesses or households that produce or use clean energy or energy-efficient systems.

I assess the historical and potential contributions of the semiconductor and green energy projects to aggregate real investment using data on plans for major manufacturing-facility construction projects in those industries. The projects were announced over the period of August 2022—when the two laws went into effect—through July 2024.

I drew on two data sources to track those announcements. The announcements of new semiconductor plants came from jackconness.com. I verified the information and updated it as needed to account for delays or project expansions.3 The green energy manufacturing data came from the Big Green Machine, a repository created by Jay Turner, a professor of environmental studies at Wellesley College. The Big Green Machine data set aggregates regulatory filings, government reports, media coverage, and other publicly available information detailing project locations, investment forecasts, employment projections, and more.

Manufacturing Investment Grew Substantially in 2023 and Is Projected to Remain Strong through 2024

As noted, the data indicate that announced real investment (as of August 2024) will amount to at least $356 billion in the semiconductor sector and $102 billion in green energy over the six-year period from 2023 through 2028. I imputed those expenditures across quarters starting in 2023.4

{kind=link}

Federal Reserve Bank of Boston

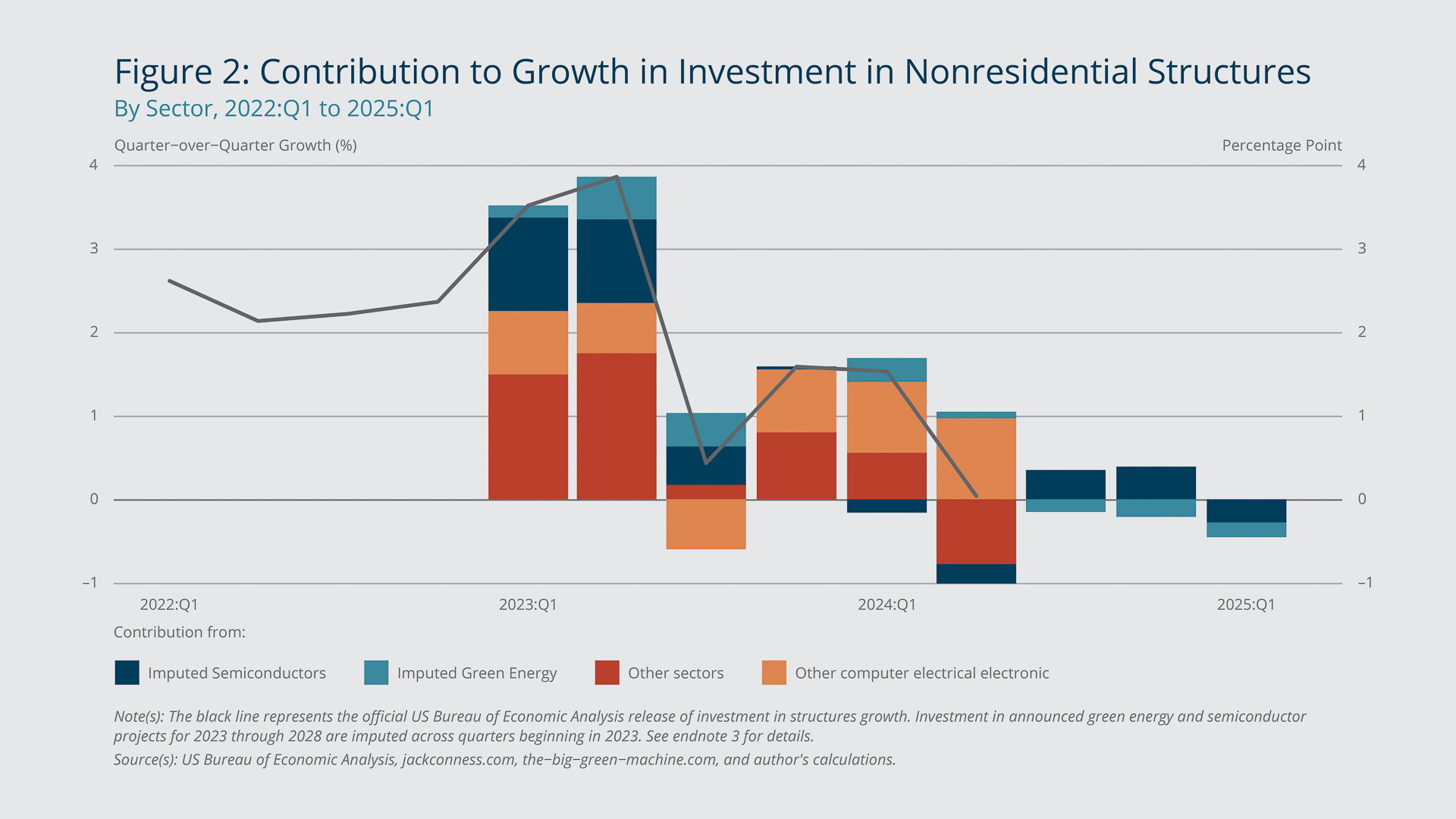

Figure 2 breaks down quarterly growth in real investment in nonresidential structures into semiconductor investment announced since the enactment of the CHIPS Act, green energy investment announced since the enactment of the IRA, residual investment in the computer, electronics, and electrical manufacturing sector (that is, investment in that sector not explained by the announced spending on semiconductor and green energy projects used in this study), and investment in other sectors.5 In 2023, total annual investment in nonresidential structures grew 10 percent, and semiconductor and green energy investment contributed one-third (3.3 percentage points) of that growth. As noted earlier, aggregate real investment (overall spending on nonresidential structures plus manufacturing equipment, and IPP) grew 6 percent in 2023, and semiconductor and green energy investment accounted for 10 percent (0.6 percentage point) of that growth.

For context, before the pandemic, the entire computer, electronics, and electrical manufacturing sector—of which semiconductors and green energy are subsectors—accounted for, on average, less than 2 percent of total nonresidential structure spending, and the sector’s contribution to annual growth in aggregate real investment was, on average, 10 times less than what we observe for 2023. Spending on nonresidential structures in the semiconductor and green energy sectors is expected to continue contributing to growth in aggregate real investment through the end of 2024, but to a lesser degree than in 2023.

{kind=link}

Federal Reserve Bank of Boston

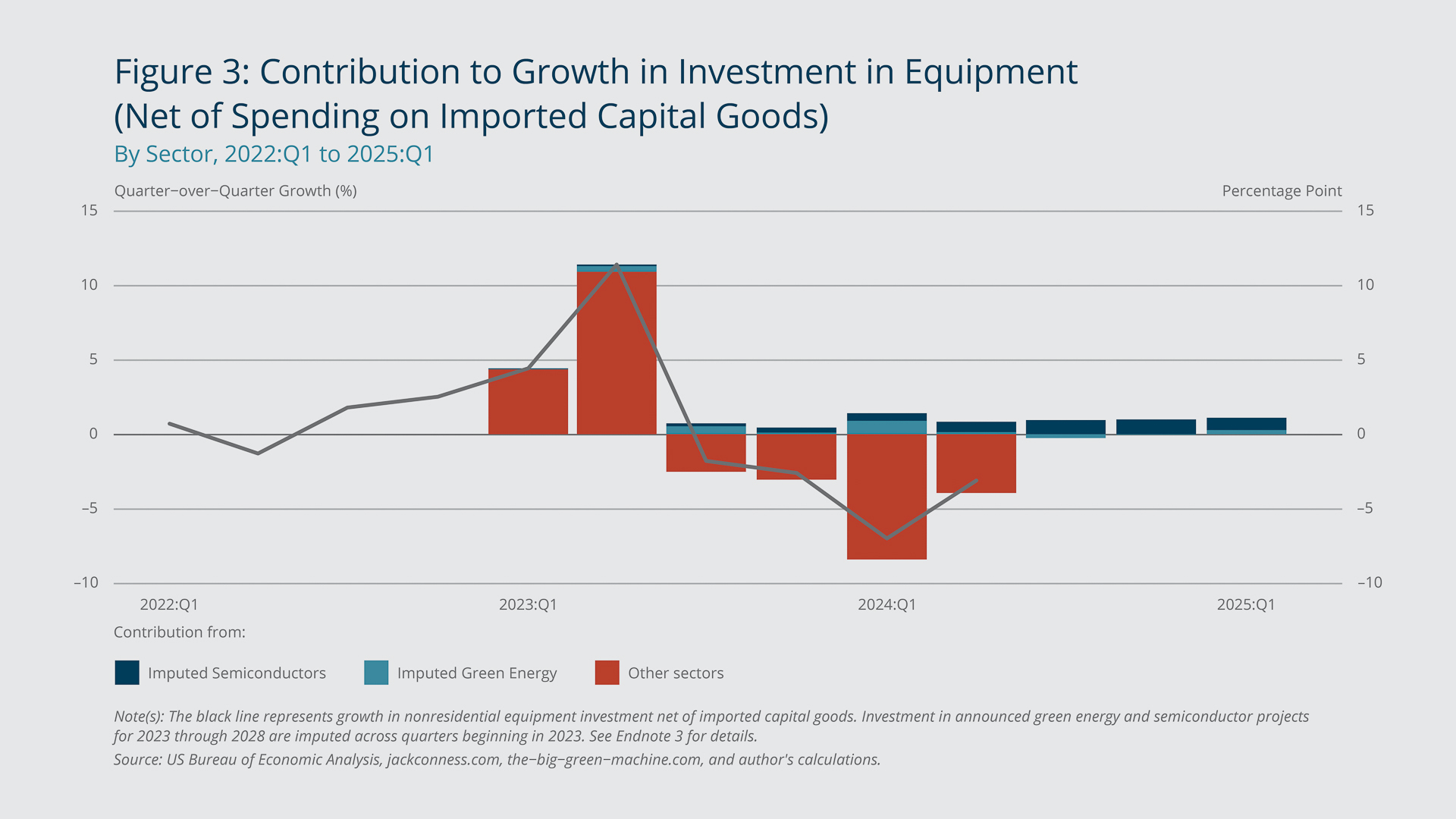

Figure 3 separates monthly growth in manufacturing equipment investment into the contributions from the semiconductor, green energy, and other sectors. Because much of the equipment used in those sectors is imported, the figure accounts for the net effect of imported capital goods on equipment investment growth (see Endnote 5), providing a clearer view of domestic contributions to GDP. The contribution of semiconductor and green energy manufacturing equipment spending to growth in aggregate real investment was modest in 2023, but I project an additional 4 percentage point growth in annual net equipment investment for 2024.6 That spending will contribute an estimated 15 percent (0.6 percentage point) of the growth in aggregate real investment in 2024, which I project will be 4 percent by assuming that the average quarterly growth observed in the first two quarters of the year will continue.

{kind=link}

Federal Reserve Bank of Boston

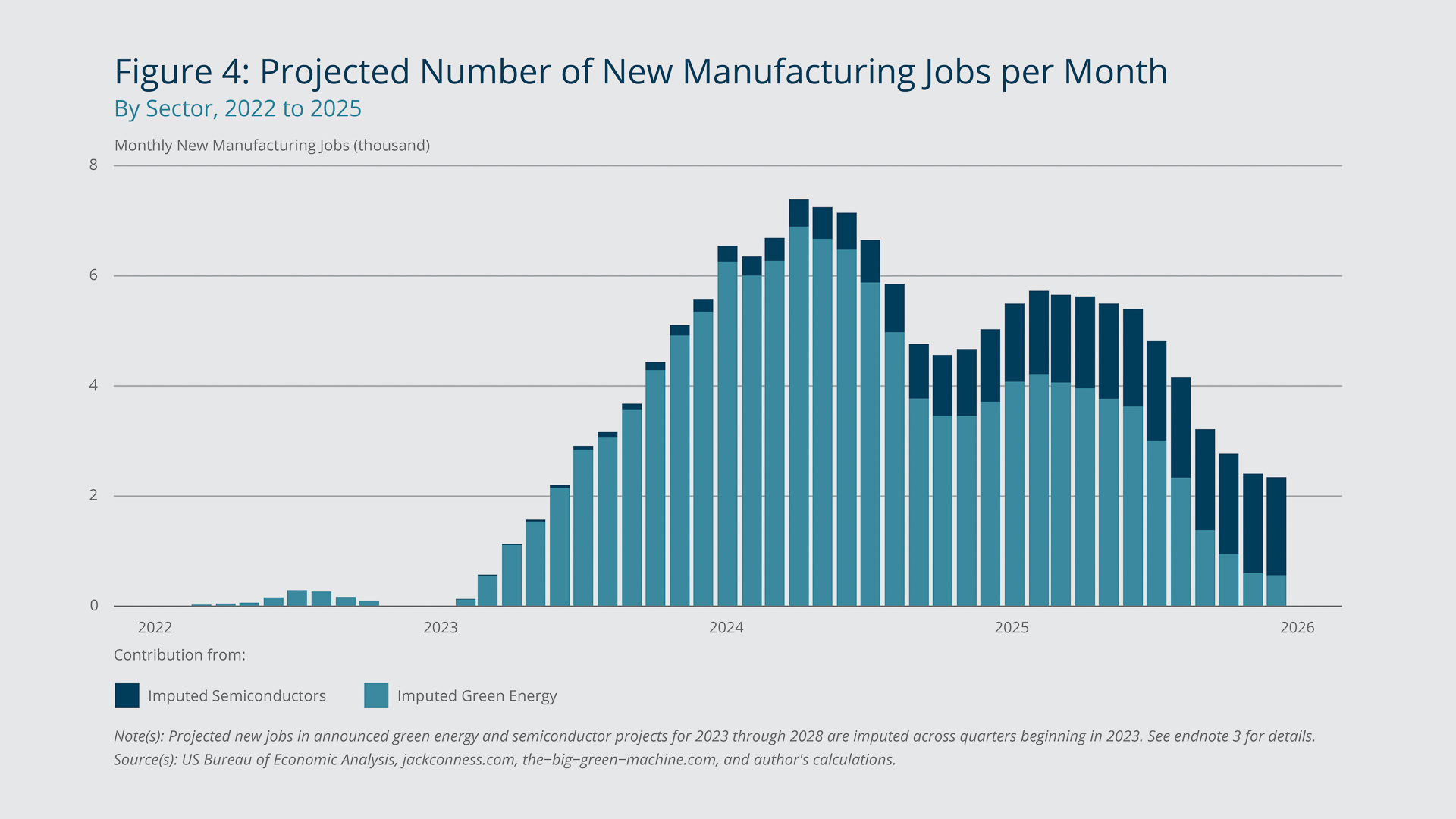

In addition to contributing to real investment, new and expanded semiconductor and green energy manufacturing plants are expected to make a notable impact on employment, despite the relatively small size of those industries. Based on the announced plans for major manufacturing-facility construction projects, I estimate that these investments will create, on average, an additional 6,000 jobs monthly in 2024 and 4,000 in 2025 (Figure 4). According to the US Bureau of Labor Statistics Employment Situation Summary, those totals are equivalent to 1 to 2 percent of the national monthly average of new jobs for 2023. The entire computer, electronics, and electrical manufacturing sector employed less than 1 percent of all US nonfarm workers in 2019.

According to the announcements, the green energy sector will provide a much larger employment boost compared with the semiconductor industry due to its lower investment-to-employment ratio: about $1 million per employee versus about $3 million per employee. Additionally, the announced green energy manufacturing facilities are expected to become operational sooner than semiconductor plants.

While the semiconductor and green energy projects announced since the enactment of the CHIPS Act and the IRA have contributed to the observed resilience of investment and will continue to contribute in 2024, their impact on US GDP growth remains limited. This is because total real investment represents only 15 percent of US GDP. Therefore, the 0.6 percent point contribution to aggregate real investment translates to only a 0.1 percentage point contribution to US GDP growth in 2023 and 2024; real GDP growth was 2.9 percent in 2023. However, pre-pandemic (2019) investments in the entire computer, electronics, and electrical manufacturing sector accounted for less than 0.7 percent of US GDP.

Realized Numbers May Be Greater than Projections

Several factors suggest that my estimates of the boosts to aggregate real investment and employment from semiconductor and green energy investment understate the impact of the ongoing boom in those sectors. First, the data I use do not capture all new projects, particularly smaller projects and defense-related projects. Second, my estimates do not account for spending on research and development, which likely is and will continue to be significant given how much increased demand and expanded government funding in these sectors could further incentivize businesses to invest in R&D. Third, as Figure 2 shows, residual spending in the computer, electronics, and electrical manufacturing sector continued to rise, contributing 1 percentage point to the growth in nonresidential structure spending in each quarter from 2023:Q4 through 2024:Q2 even though overall spending weakened (data for 2024:Q3 and beyond are not yet available).

The residual spending data may indicate that other forces, such as demand for artificial intelligence or remote-work tools, are stimulating investment indirectly by requiring an expansion of existing capacity in several sectors to keep up with that demand. Additionally, announced green energy and semiconductor projects typically generate spillover within and beyond those sectors. The investment boom should benefit not only suppliers of semiconductor and green energy manufacturing plants, but also, indirectly, workers and investors in construction and local services. In the long term, increased income from the investment boom likely will become more difficult to estimate and pin down to a specific sector.

Note that this analysis does not identify the causal effects of the CHIPS and Science Act and IRA on aggregate real investment. The increase in investment does not prove that the manufacturing projects in those sectors would not have materialized without government support. In fact, investment in computer manufacturing facilities and green energy was already growing before 2022. However, the rapid expansion seen in recent years likely reflects the role that targeted policy has played in accelerating the growth of these industries.

Endnotes

- Semiconductor businesses manufacture the computer chips used in smartphones, computers, automobiles, solar panels, and most other electronic products and devices. The green energy (or renewable energy) manufacturing industry analyzed in this brief includes companies that produce, for example, electric vehicles, heat pumps, or solar panels. My analysis does not include announcements of new mining operations (for lithium and other critical minerals) or power plants that produce solar or wind power or other renewable energy.

- The semiconductor and green energy sectors’ contribution to investment growth in equipment net capital import was minimal in 2023, and their contribution to investment growth in nonresidential construction is projected to be minimal in 2024.

- See Amanda Chu, Alexandra White, and Rhea Basarkar, “Delays Hit 40% of Biden’s Major IRA Manufacturing Projects,” Financial Times, August 12, 2024.

- For each manufacturing plant that was announced after the enactment of the CHIPS and Science Act and the IRA, I impute the completion date if it is missing through regression analysis of the plants for which the completion dates are available. The regression coefficient is sector specific—for semiconductor, solar panel, electric vehicle batteries, etc. A Granger causality test established that annual equipment manufacturing spending lags construction spending by one year. (The data are from the Detailed Fixed Assets Tables of the US Bureau of Economic Analysis [BEA]). I allocate construction versus equipment spending based on the 4:1 ratio predicted by my regression analysis of equipment spending on one-year-lagged construction spending. I distribute spending over time by front-loading construction spending and back-loading equipment spending according to the tails of a normal distribution that is centered at either the start or the end of a project. I compute the ratio of spending on imported manufacturing equipment versus spending on domestic manufacturing equipment as the value of imported capital goods (except automotive) versus investment in nonresidential fixed equipment from the BEA data. The ratio is projected to remain constant beyond 2024:Q2. I sum the imputed investment in structures and the imputed investment in equipment and use those totals to determine their respective contributions to overall investment growth.

- I compute the residual computer, electronics, and electrical manufacturing component from the seasonally adjusted US Census data on the value of announced private construction in the computer, electronics, and electrical manufacturing sector net of the announced spending on semiconductor and green energy manufacturing for each quarter.

- My analysis assumes the effects of equipment investment will be delayed to reflect the results from the Granger causality test discussed in Endnote 3.

References

Abecasus, Manuel, Jan Hatzius, Spencer Hill, Tim Krupa, David Mericle, Alec Phillips, and Ronnie Walker. 2023. “The Boost to Manufacturing Investment and Employment from the IRA and CHIPS Act.” Goldman Sachs Economic Research US Daily. August 18.

Van Nostrand, Eric, Tara Sinclair, and Samarth Gupta. 2023. “Unpacking the Boom in US Construction Manufacturing Facilities.” US Department of the Treasury. June 27.

About the Authors

About the Authors

Omar Barbiero,

Federal Reserve Bank of Boston

Omar Barbiero is an economist in the Federal Reserve Bank of Boston Research Department.

Email: Omar.Barbiero@bos.frb.org

Resources

Site Topics

Keywords

- CHIPS Act ,

- Inflation Reduction Act ,

- green energy ,

- semiconductors ,

- manufacturing investment ,

- fiscal incentives

JEL Codes

- E01 ,

- E22 ,

- E62 ,

- E65 ,

- Q58

Citation

Barbiero, Omar. 2024. “Manufacturing Gains from Green Energy and Semiconductor Spending since the CHIPS and Inflation Reduction Acts.” Federal Reserve Bank of Boston Current Policy Perspectives 24-7.