A New Use Case: A Supervisory Node

The Boston Fed team set out to learn what business questions are generated by the use of blockchain technology. We decided to investigate by developing capabilities for the supervisor peer subscribed to each of the channels in our simulated network.

“Intelligence is the ability to adapt to change.” —Stephen Hawking, Theoretical Physicist

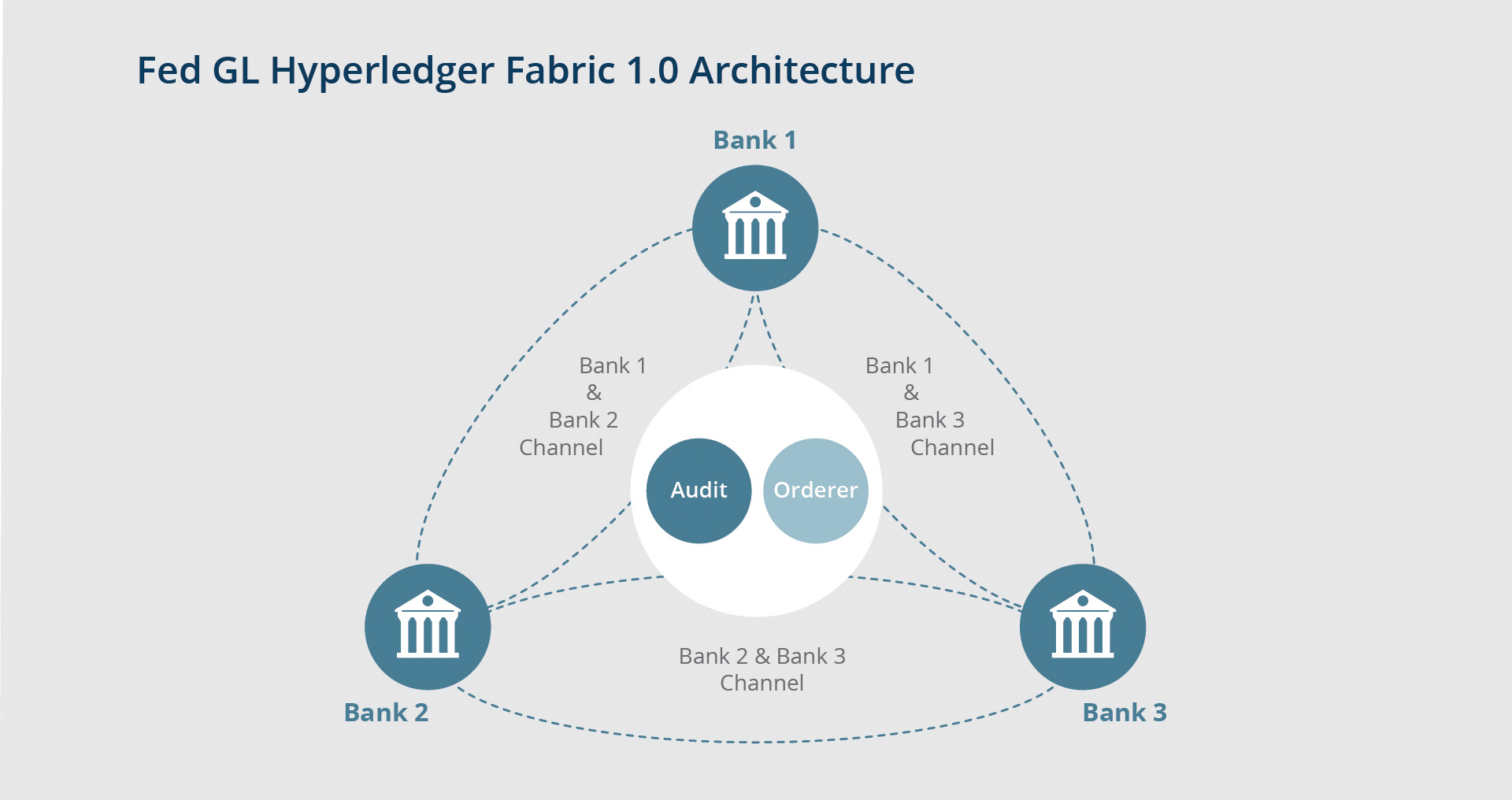

The Federal Reserve “is responsible for supervising—monitoring, inspecting, and examining—certain financial institutions to ensure that they comply with rules and regulations, and that they operate in a safe and sound manner.”1 We decided to investigate what we could learn from developing a rich set of capabilities for the supervisor peer subscribed to each of the channels in our simulated network. As with our previous experiments, our goal was simply to learn about the technology and what business questions are generated by its use. It was not our intention to imply that we would actually implement this technology as part of our supervisory function.

{kind=link}

Federal Reserve Bank of Boston

It is worth noting that “supervisory node” is a generic term and can include many roles beyond the Fed’s regulatory supervisor role, such as an auditor, payments network rule-enforcer, or data reporting entity. As such, some of our questions and potential experiments are more generic and not necessarily tied to any of our specific roles as a regulatory supervisor. The following are some questions we have about what blockchain technology and smart contract logic, possibly coupled with artificial intelligence and machine learning, could accomplish:

Sign up for the latest updates on our Payments Innovation work

- What business functions (audit, regulatory supervisor, payment network rule-enforcer) could supervisory nodes perform?

- What architectural questions do supervisory nodes create?

- How can data access be limited only to whatever is needed to perform the stated function?

- Is there any way the supervisory node could be compromised or create operation risk for the network?

- When multiple blockchain platforms are utilized for a given business process (e.g., delivery versus payment, or DvP), what impact does this have on the supervisory node(s) architecture and performance?

- If sister supervisory agencies that share oversight responsibilities were able to develop a single supervisory node structure, what new architectural/technical questions does it raise?

- What can be done to detect and control malicious actors in a private payment network? (This may extend beyond the Federal Reserve’s role, and applies more appropriately to any parties charged with enforcing rules, such as a private payment network operator.)

- How can fraud be detected? If it can be detected in a shared network by a node supported by AI logic, what possible actions are appropriate?

While we have no results on this use case yet, we hope sharing these ideas will inspire others.

The views expressed in this report are those of the authors and do not necessarily represent positions of the Federal Reserve Bank of Boston or the Federal Reserve System.

Endnotes

Endnotes

- “Board of Governors of the Federal Reserve System.” Supervision & Regulation. https://www.federalreserve.gov/supervisionreg.htm.

Resources

Site Topics

Keywords

- supervisory node ,

- blockchain ,

- distributed ledger technology ,

- proof of concept ,

- smart contracts