New England Economic Conditions Through December 3, 2024

Key Takeaways

- The unemployment rate was largely stable from October 2023 to October 2024, with year-over-year increases of 0.1 percentage point in New England and 0.3 percentage point nationally. Nevertheless, the total hires rate fell steadily over this period, presenting challenges for job seekers.

- Year-over-year inflation remained higher in New England than in the United States in October 2024, though the gap narrowed slightly from the preceding month. Increases in shelter prices continued to be the primary driver of inflation both nationally and regionally.

- Inflation-adjusted real wages in New England had declined for two consecutive quarters as of 2024:Q3, a consequence of the region's higher inflation rate coupled with weaker nominal wage growth. Real wages, both nationally and regionally, were still recovering from the high inflation during the pandemic, which eroded all the nominal wage gains accrued over the previous three years.

Sign up for new research and data on the New England economy.

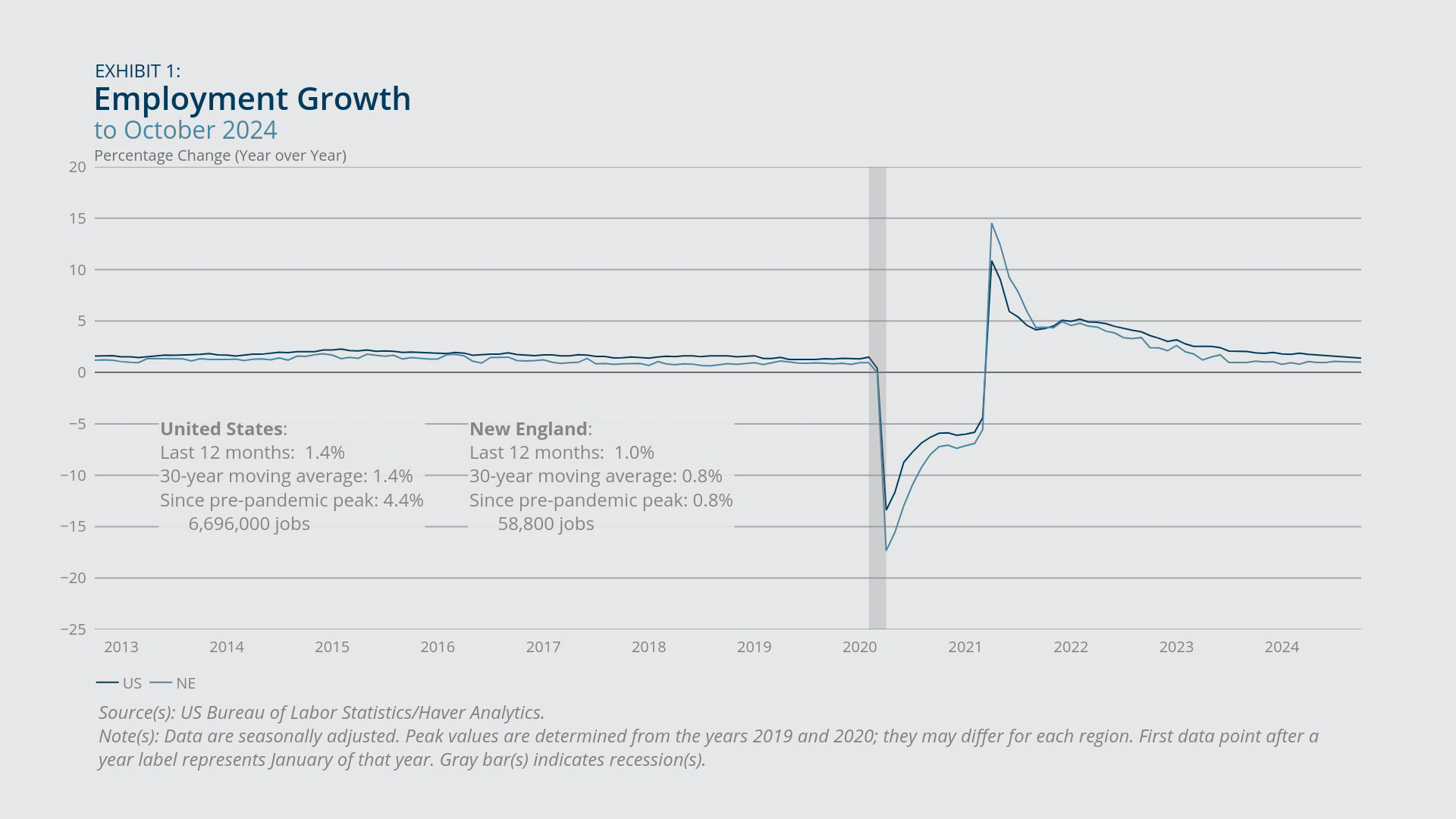

Payroll Employment

- Payroll employment growth in New England and the United States returned to levels close to the long-run year-over-year rates.

- The education and health services, leisure and hospitality, and construction sectors continued to drive recent employment growth in the region and nationally.

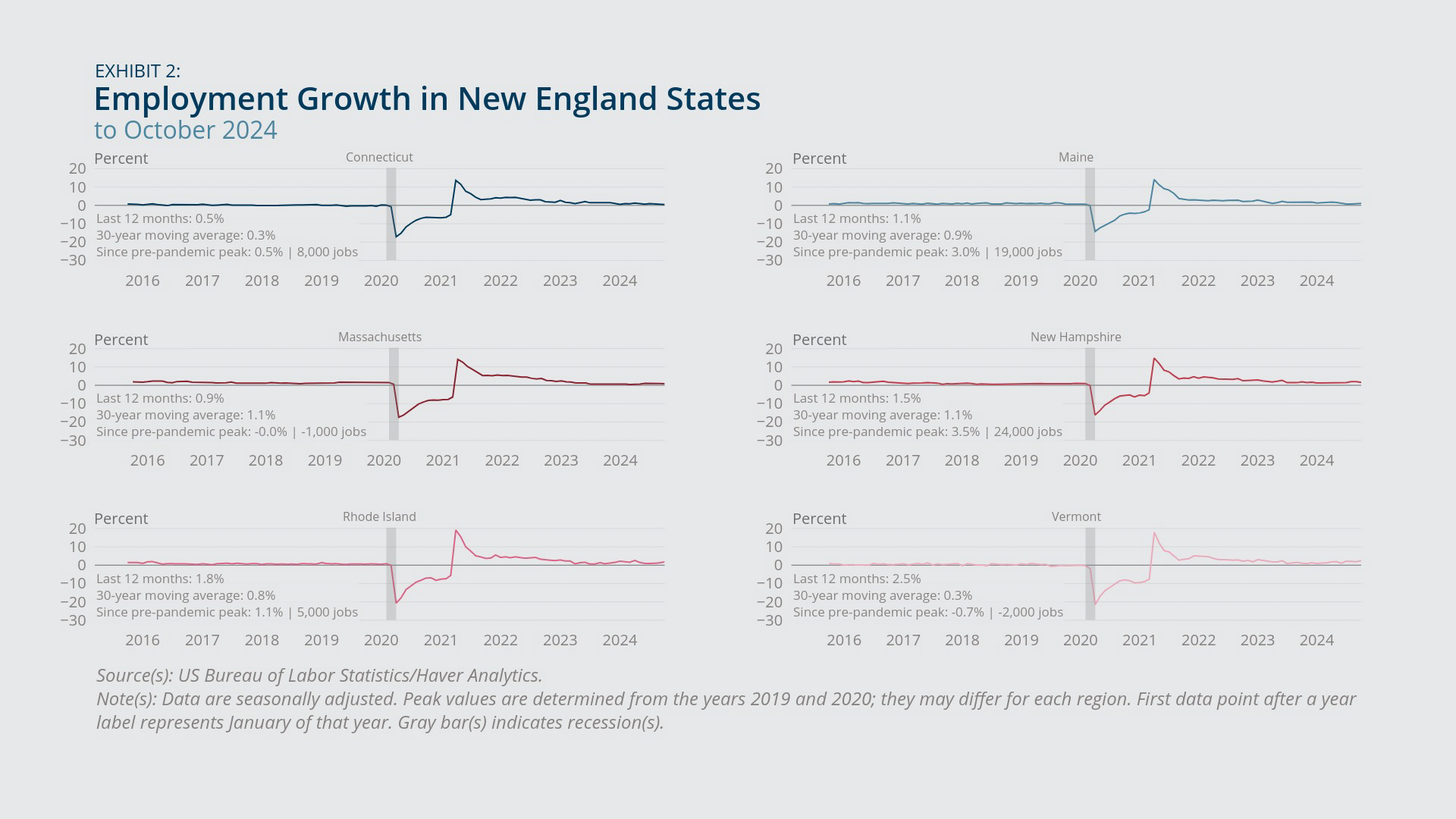

In October 2024, total nonagricultural payroll employment grew 1.4 percent year-over-year for the United States and 1.0 percent for New England (Exhibit 1). The national figure reflects the slowest year-over-year growth since March 2021, suggesting a return to the long-run, 30-year average growth rate of 1.4 percent. For the region, the 1.0 percent rate indicates stable year-over-year growth since July 2023. Massachusetts stood out as the only New England state with a year-over-year growth rate lagging its long-term average, and it was one of two states in the region (Vermont was the other) that had not fully recouped the employment losses sustained during the COVID-19 pandemic (Exhibit 2).

The education and health services, leisure and hospitality, construction, and total government sectors continued to lead employment gains both nationally and regionally (Exhibit 3). However, several other sectors reported job losses or stagnation. In New England, the information sector saw the greatest year-over-year employment decline. Across the nation, the manufacturing sector was the only sector to experience job loss over the year. Following the rapid growth seen in 2021 and 2022, the professional and business services sector exhibited modest year-over-year growth rates of 0.1 percent nationally and 0.5 percent regionally.

{kind=link}

Federal Reserve Bank of Boston

{kind=link}

Federal Reserve Bank of Boston

{kind=link}

Federal Reserve Bank of Boston

Unemployment and Labor Force Participation

- The unemployment rate trended modestly upward from October 2023 to October 2024, with year-over-year increases of 0.1 percentage point in New England and 0.3 percentage point nationally.

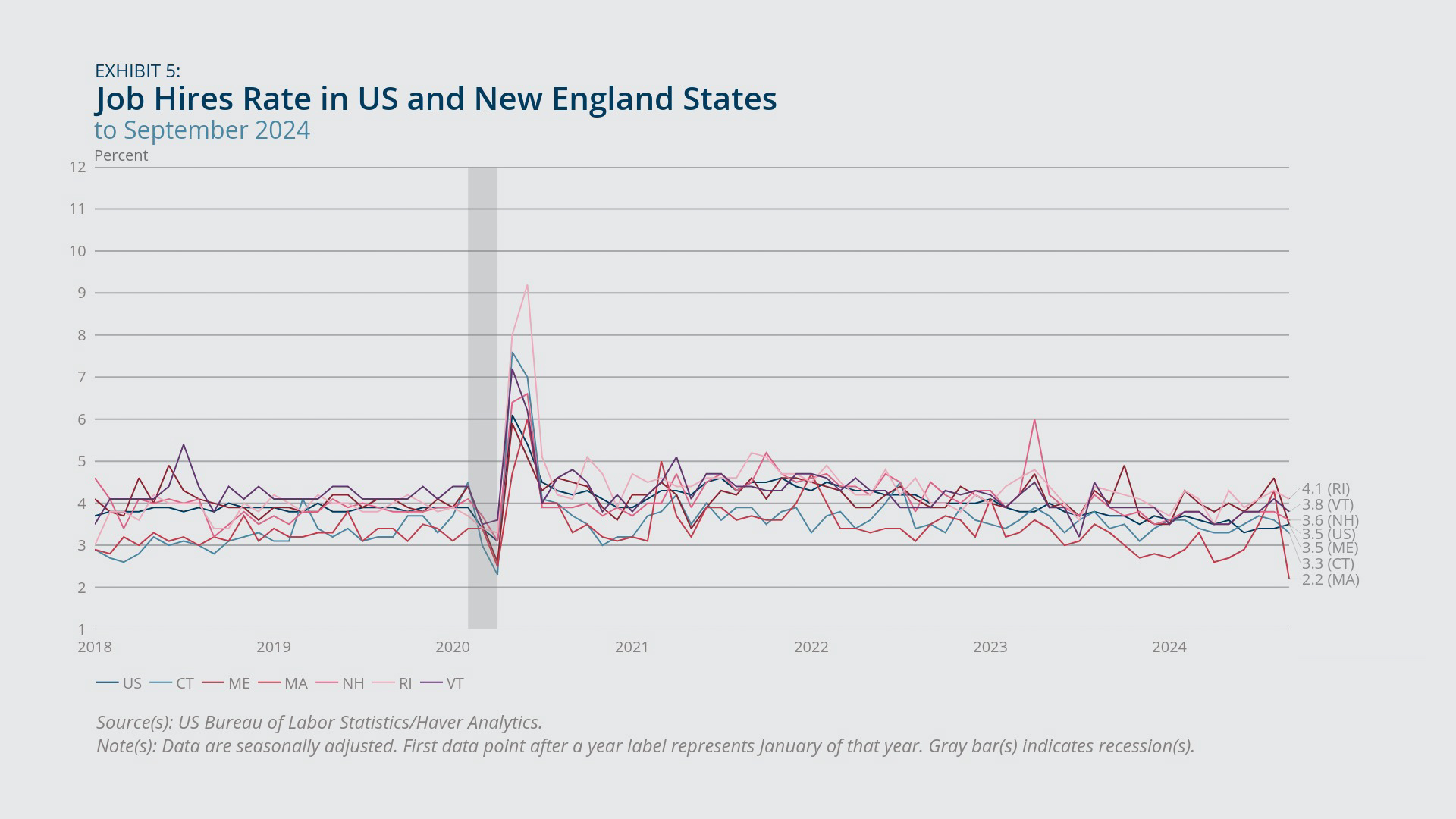

- Although the unemployment rate remained largely stable, the total hires rate declined noticeably, presenting additional challenges for job seekers.

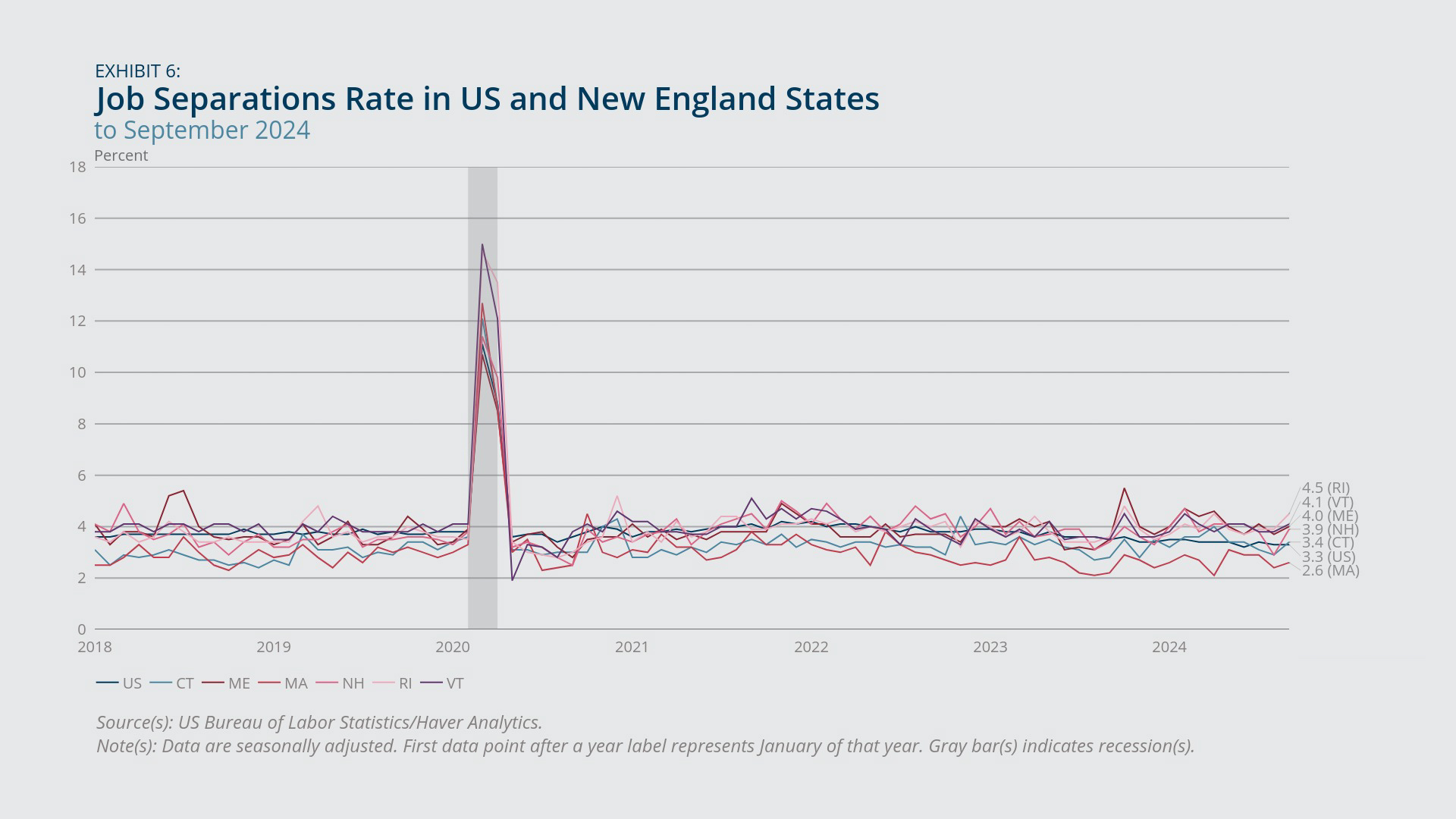

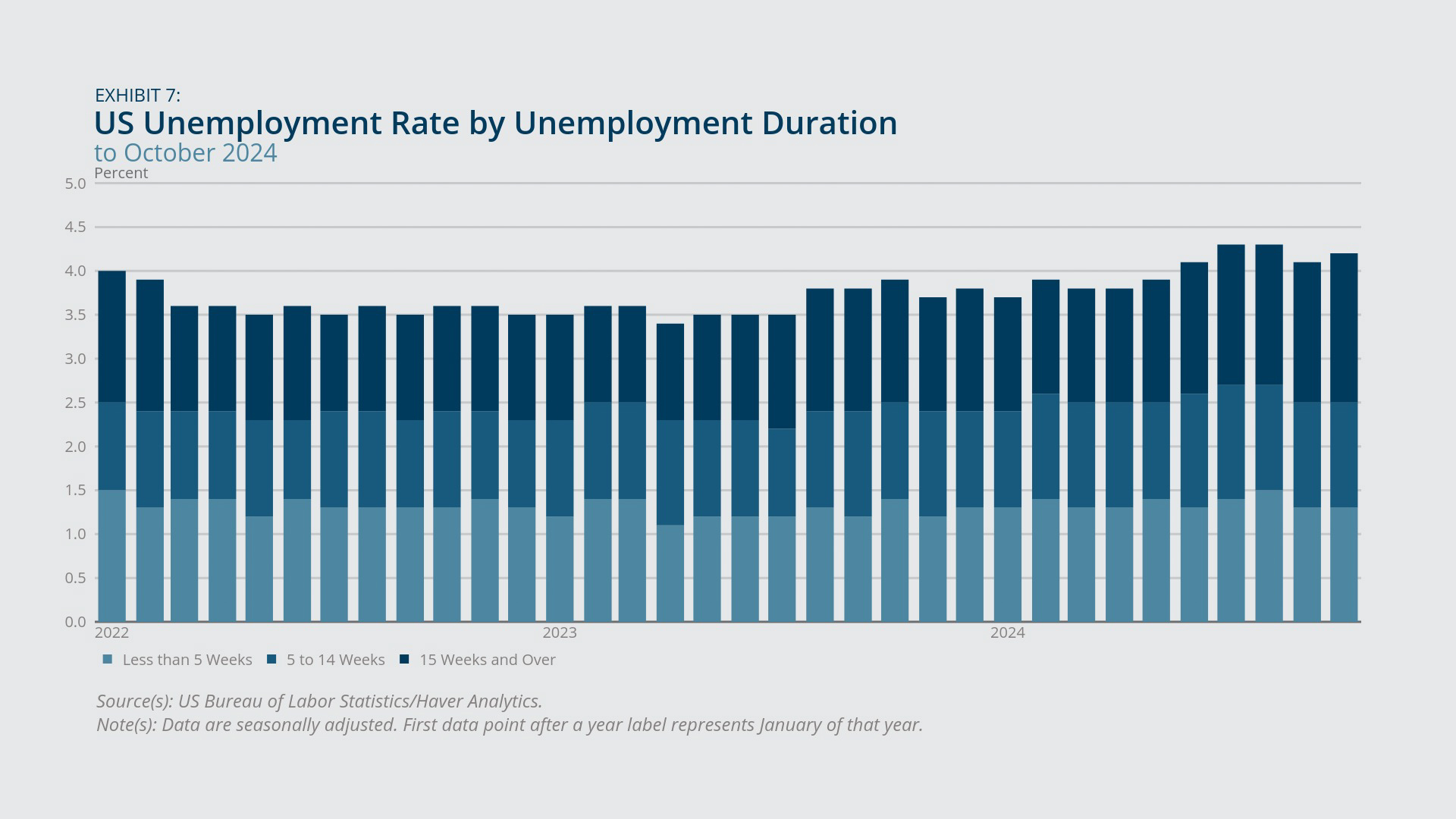

The unemployment rate stood at 3.5 percent in New England and 4.1 percent in the United States in October 2024, reflecting year-over-year increases of 0.1 and 0.3 percentage point, respectively (Exhibit 4). While unemployment trended only modestly upward over the preceding two years, labor market dynamism substantially cooled. From November 2021 to September 2024, the nationwide job hires rate (Exhibit 5) fell 1.1 percentage points, and the job separations rate (Exhibit 6) showed a parallel 0.9 percentage point decline.1 As of September 2024, both the hires rate and separations rate had dipped below their pre-pandemic baseline levels nationally. These changes placed a greater burden on job seekers, who faced fewer job openings, as reflected in their prolonged unemployment spells (Exhibit 7).

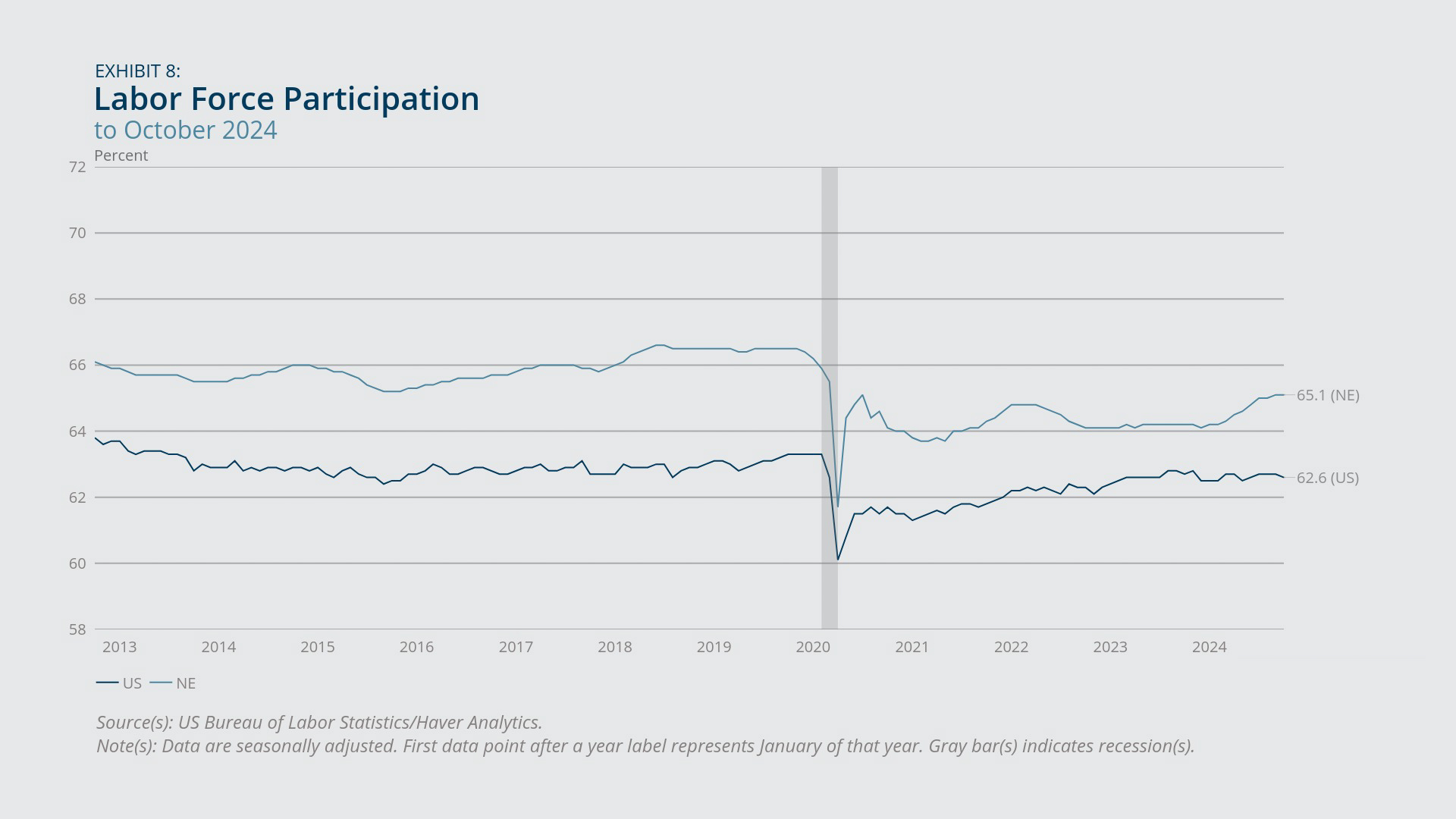

The labor force participation rate in the region continued to show an elevated level in October 2024, with a year-over-year increase of 0.9 percentage point (Exhibit 8). The corresponding national rate was flat over that 12-month period. As discussed in the October 2024 New England Economic Conditions Memo, the magnitude of the observed rate changes points to the possibility of survey-related volatility. We therefore caution against drawing conclusions about labor force participation trends in the region until the US Bureau of Labor Statistics releases its annual revision to the household employment statistics in early 2025. The revision will incorporate updated population controls and state model inputs.

{kind=link}

Federal Reserve Bank of Boston

{kind=link}

Federal Reserve Bank of Boston

{kind=link}

Federal Reserve Bank of Boston

{kind=link}

Federal Reserve Bank of Boston

{kind=link}

Federal Reserve Bank of Boston

Inflation

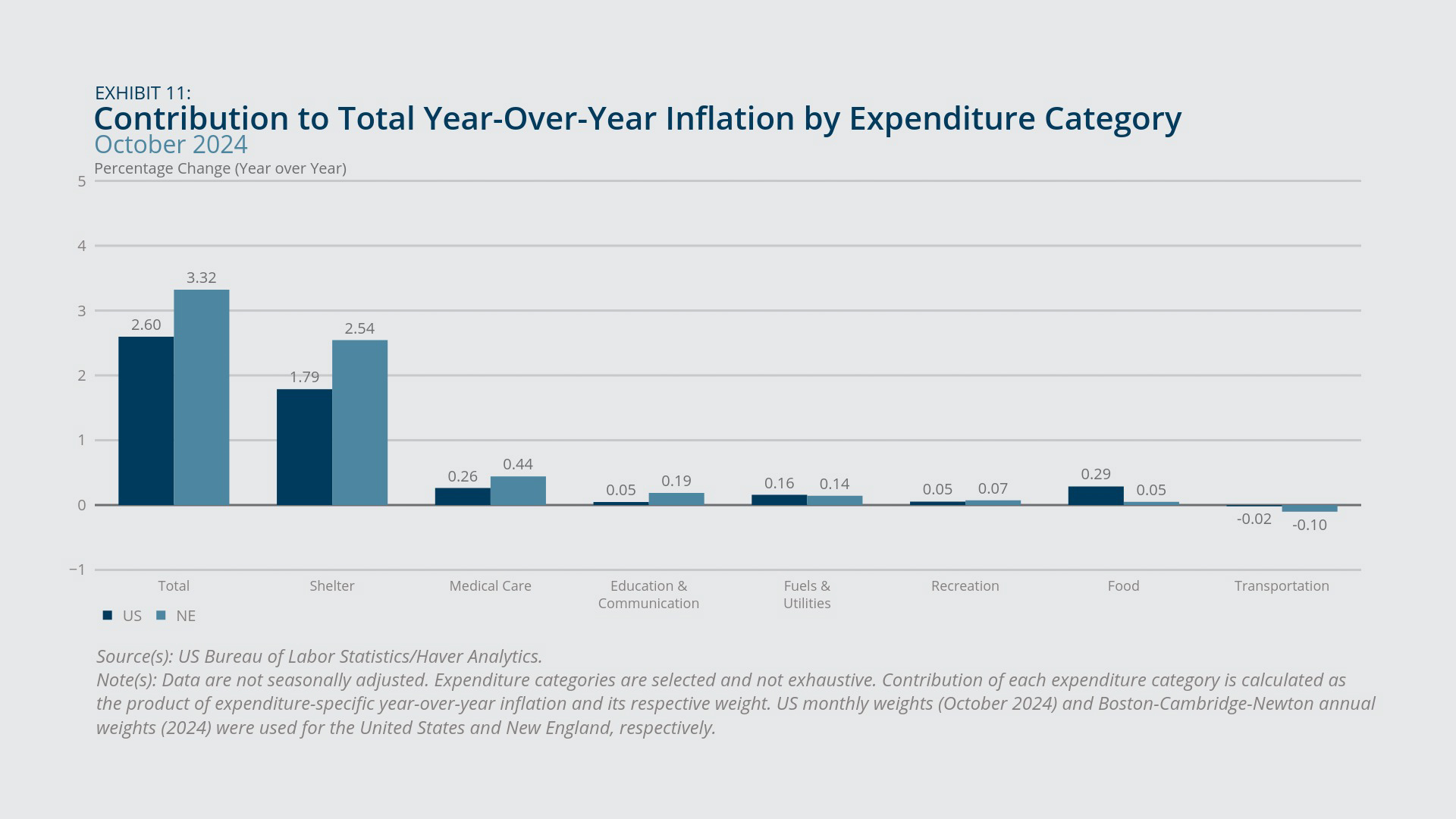

- Year-over-year inflation remained higher in New England than in the United States in October 2024, though the gap narrowed slightly from the preceding month.

- Shelter prices saw the most substantial growth and continued to be the primary driver of inflation both nationally and regionally.

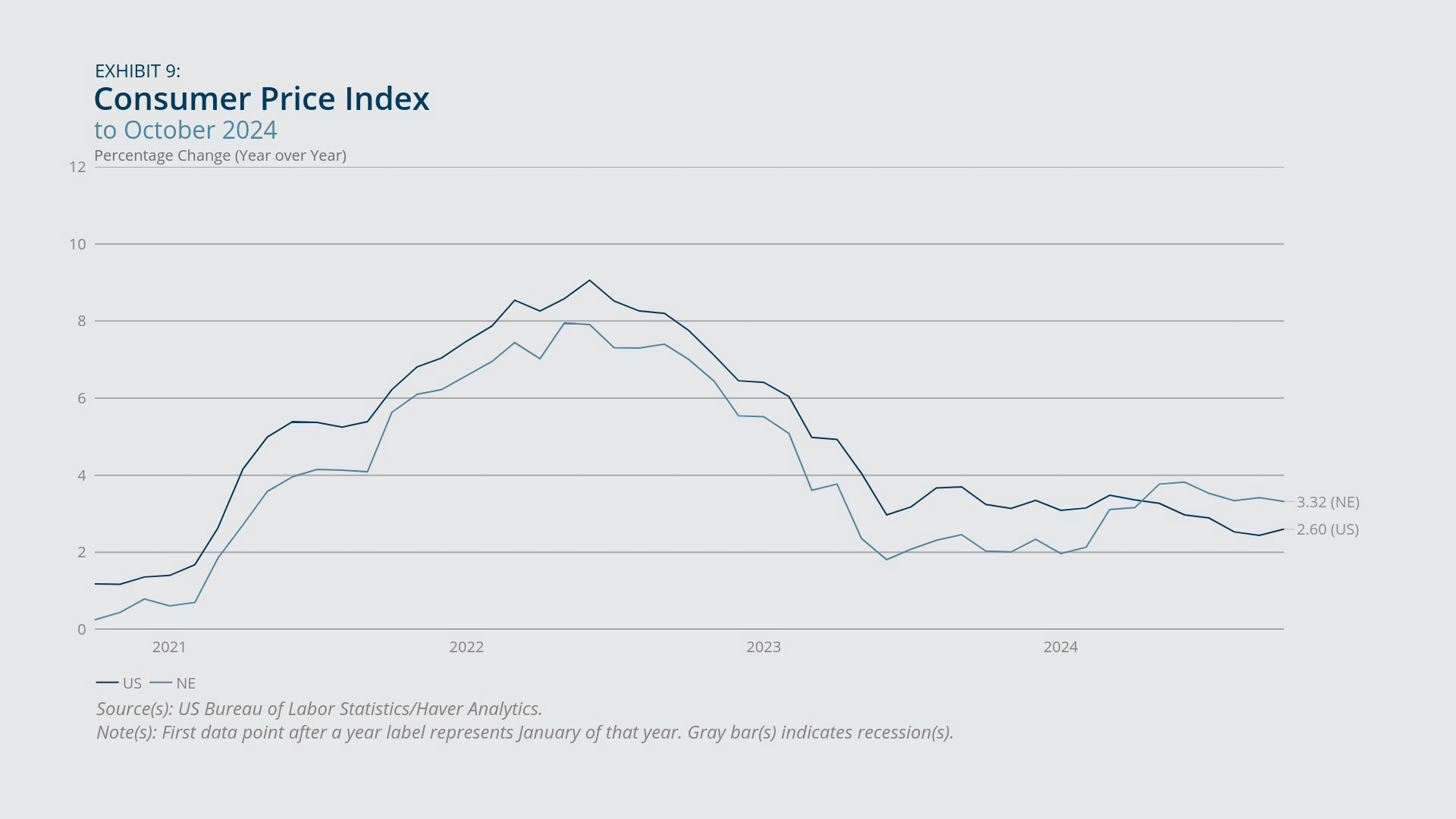

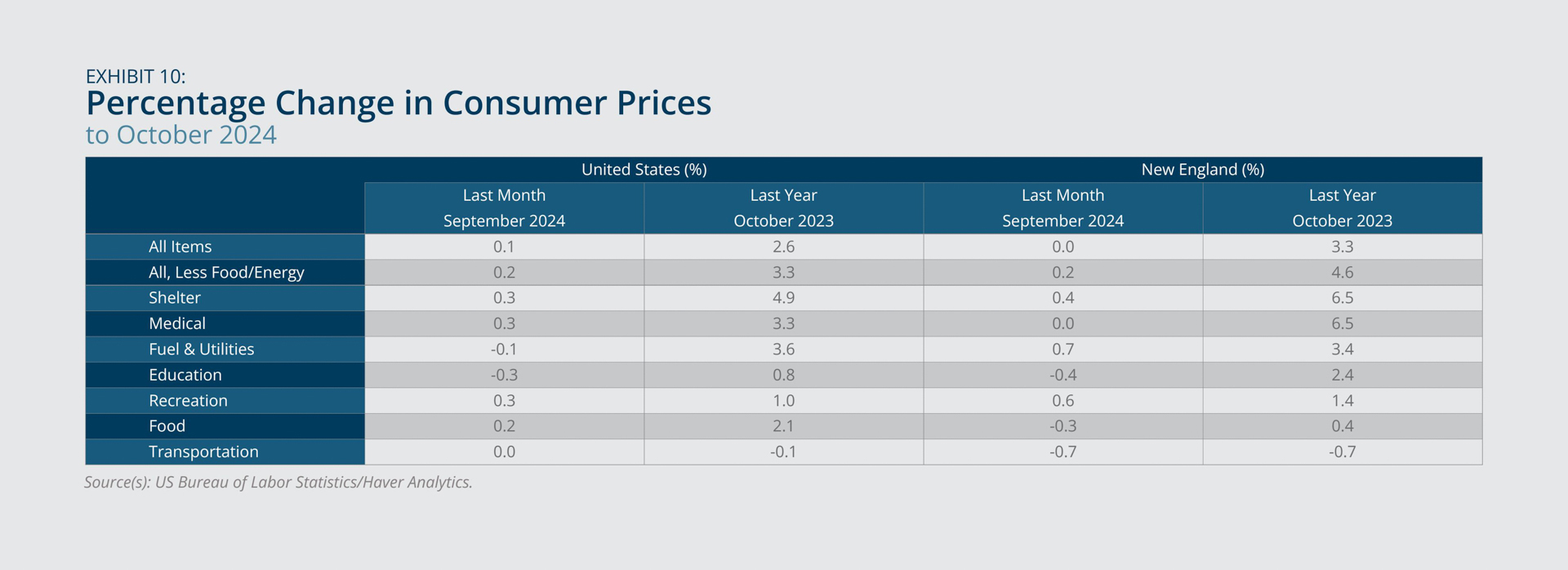

According to the Consumer Price Index for All Urban Consumers (CPI-U), year-over-year inflation in New England measured 3.3 percent in October 2024, moderately exceeding the national rate of 2.6 percent (Exhibit 9). While the regional inflation rate represented a slight decline from the September rate of 3.4 percent, the national figure ticked up slightly from 2.4 percent in September. Core inflation, which excludes the more volatile food and fuel prices, held steady in both New England and the United States at 4.6 and 3.3 percent, respectively (Exhibit 10).

Shelter prices, which maintained a persistent year-over-year growth rate of 4.9 percent across the United States and 6.5 percent in New England, continued to be a key driver of inflation, accounting for 69 percent of the overall national inflation and 77 percent of the regional inflation (Exhibit 11). Increases in medical care prices (US and New England) and food prices (US) played secondary roles in driving overall inflation during this period.

{kind=link}

Federal Reserve Bank of Boston

{kind=link}

Federal Reserve Bank of Boston

{kind=link}

Federal Reserve Bank of Boston

Wage and Compensation Growth

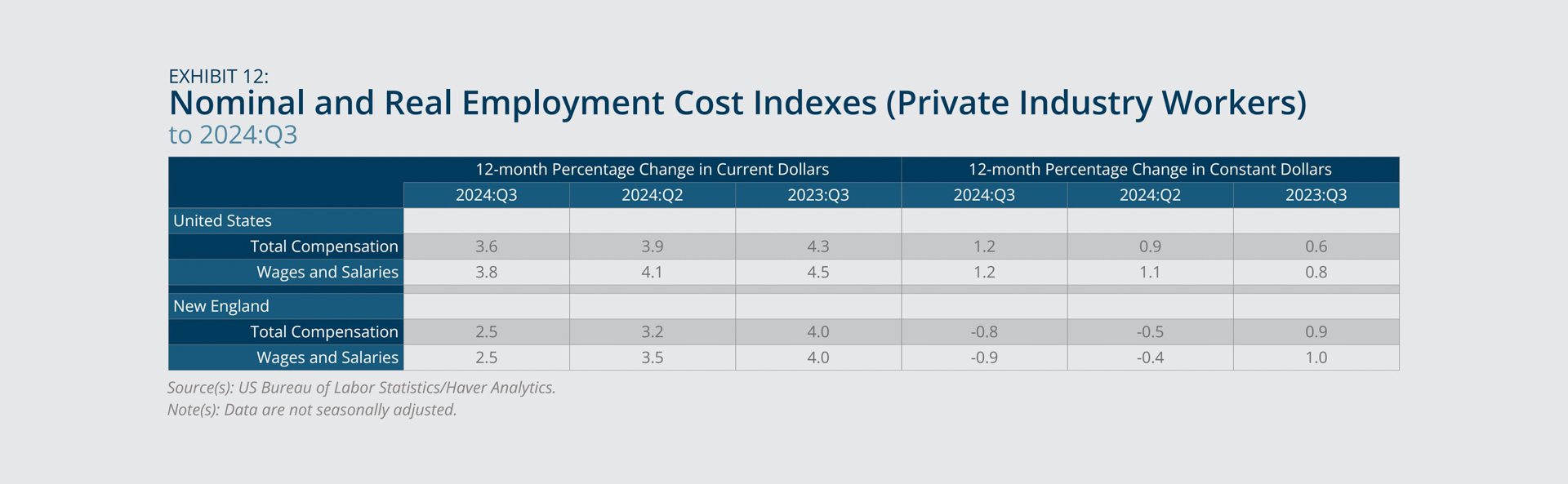

- Inflation-adjusted real wages in New England had declined for two consecutive quarters as of 2024:Q3, a consequence of the region's higher inflation rate coupled with weaker nominal wage growth since the start of the year.

- Real wages, both nationally and regionally, were still recovering from the high inflation during the pandemic, which eroded all the nominal wage gains accrued over the previous three years.

In 2024:Q3, nominal wages and salaries in New England increased 2.5 percent year-over-year, while real wages and salaries decreased 0.9 percent (Exhibit 12). This was the second consecutive quarterly drop in real wages in the region. By contrast, nominal and real wages and salaries nationwide rose 3.8 and 1.2 percent, respectively, during the same period. The region’s slower real wage growth is attributed to its higher inflation and weaker nominal wage growth compared with national rates.

Real wages in the region and nationwide were 2.1 percent and 1.8 percent, respectively, below their peak values recorded in 2021:Q1 (Exhibit 13), indicating that the high inflation during the pandemic eroded all the nominal wage gains achieved over the previous three years. Nationally, with the moderation in inflation, real wages have been steadily recovering, with the growth rate returning to its pre-pandemic level in 2024:Q3. However, the more elevated inflation in New England continued to put downward pressure on real wages, slowing the recovery in the region.

{kind=link}

Federal Reserve Bank of Boston

{kind=link}

Federal Reserve Bank of Boston

Real Estate Markets

- The rent growth rate in the Boston metropolitan area decelerated over the 30-month period ending in October 2024 and fell below its pre-pandemic level.

- While home price growth slowed during this period, total home sales remained well below pre-pandemic levels, suggesting that housing market conditions continued to constrain housing turnovers.

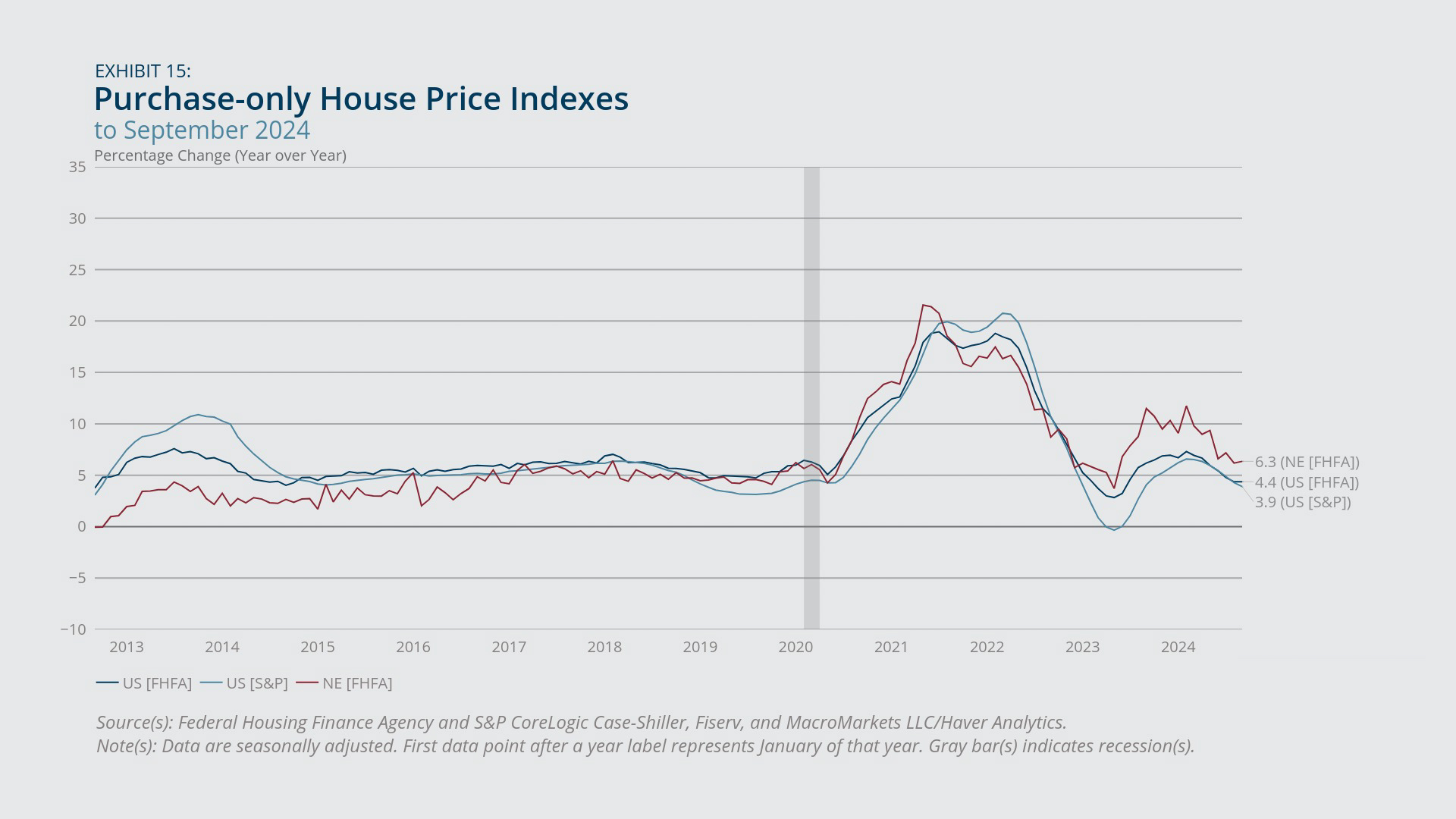

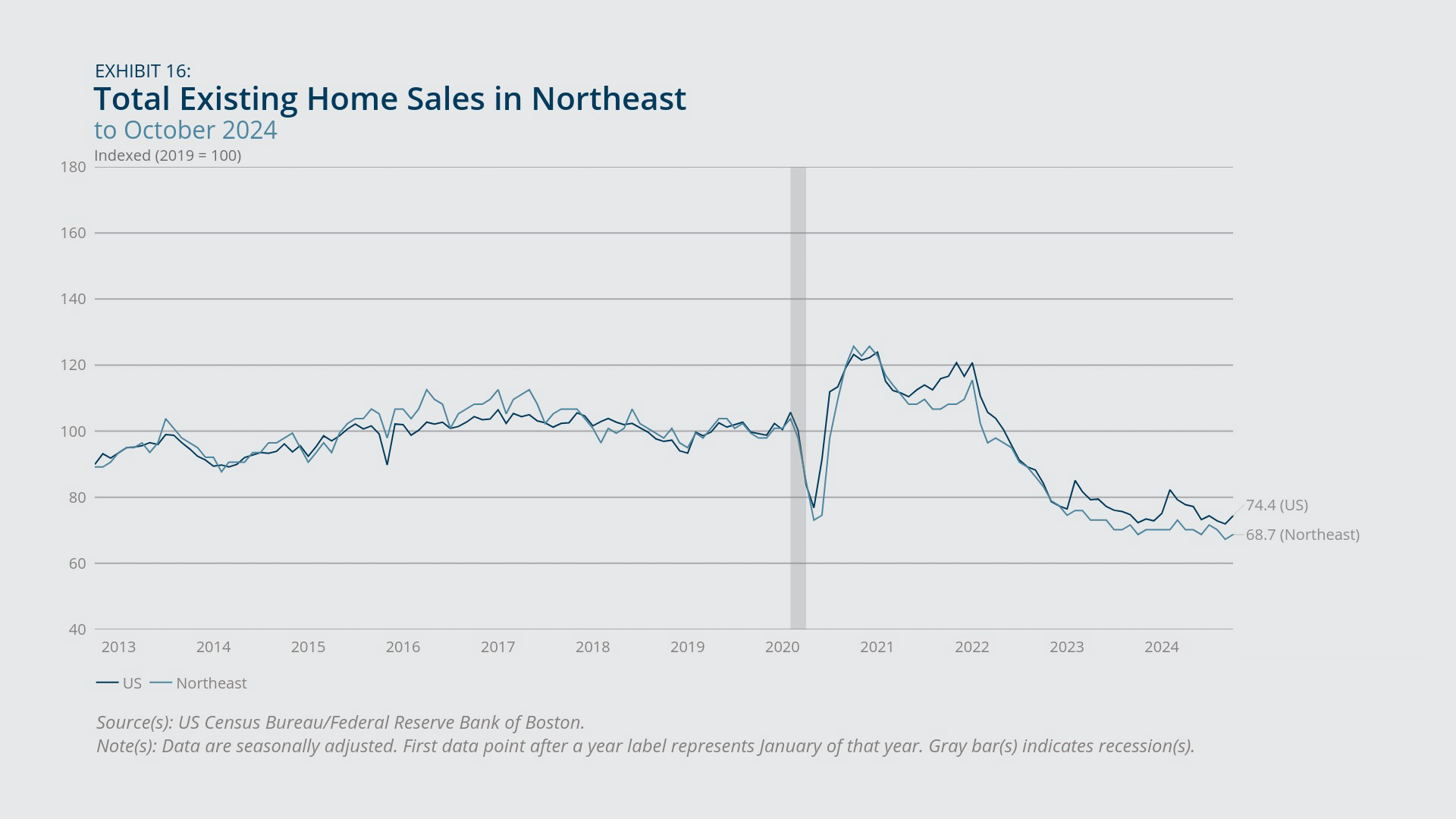

According to the Zillow Observed Rent Index, rent growth gradually decelerated in both the Boston metropolitan area and the United States over the 30-month period ending in October 2024. The year-over-year rent growth rate in October in the Boston metro area was 3.0 percent, which was modestly slower than the national growth rate for that period and slower than the area’s pre-pandemic rate (Exhibit 14). House price appreciation also slowed in New England. The Federal Housing Finance Agency (FHFA) House Price Index indicates that regional house prices grew 6.4 percent year-over-year in September 2024, down from 11.5 percent in September 2023 and approaching the pre-pandemic baseline (Exhibit 15). Despite moderating price growth, total existing home sales remained 30 percent below the 2019 level (Exhibit 16), indicating that housing market conditions—such as low inventories due to mortgage lock-in effects and high prices—continued to significantly constrain people’s ability to move.

{kind=link}

Federal Reserve Bank of Boston

{kind=link}

Federal Reserve Bank of Boston

{kind=link}

Federal Reserve Bank of Boston

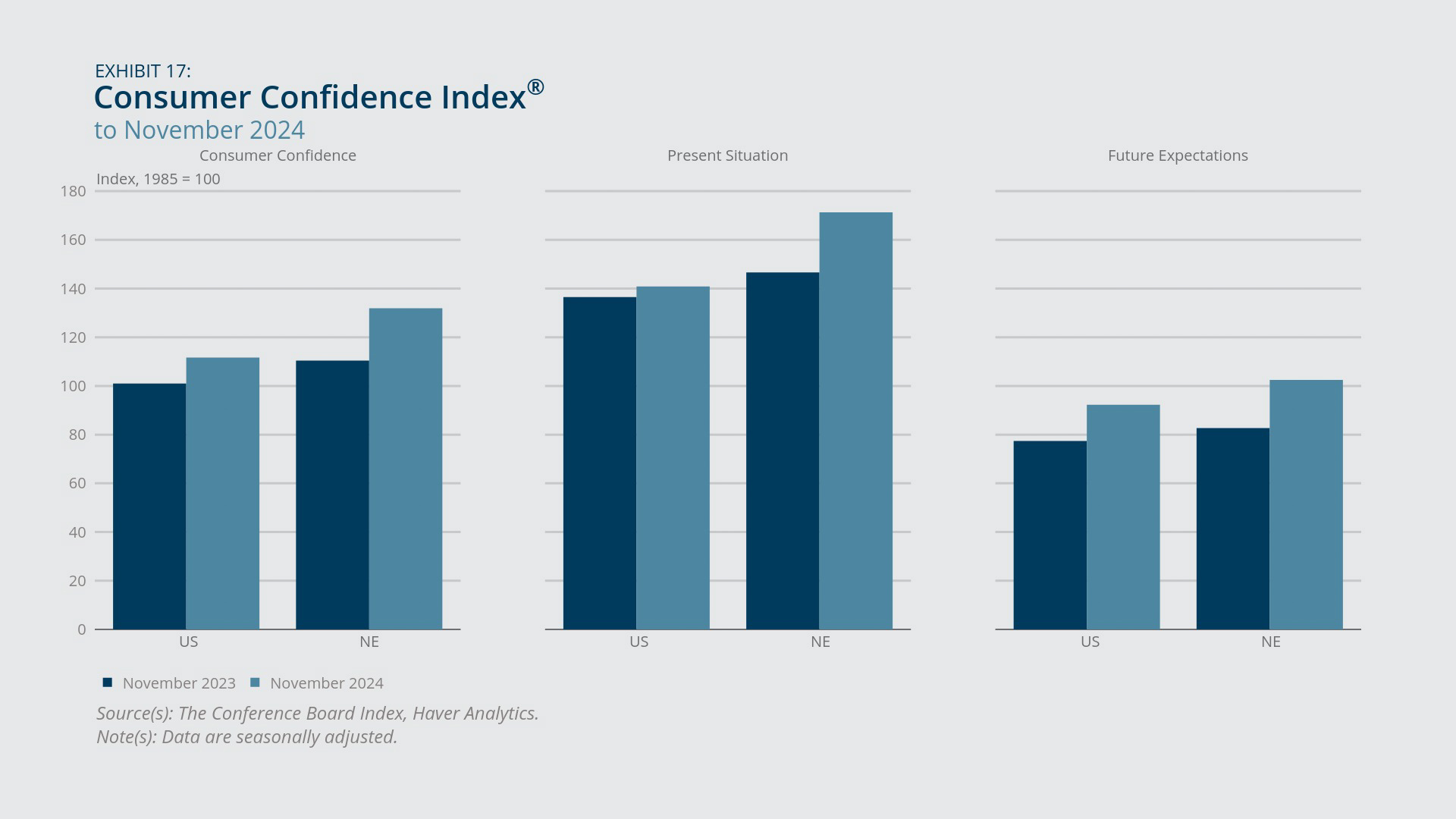

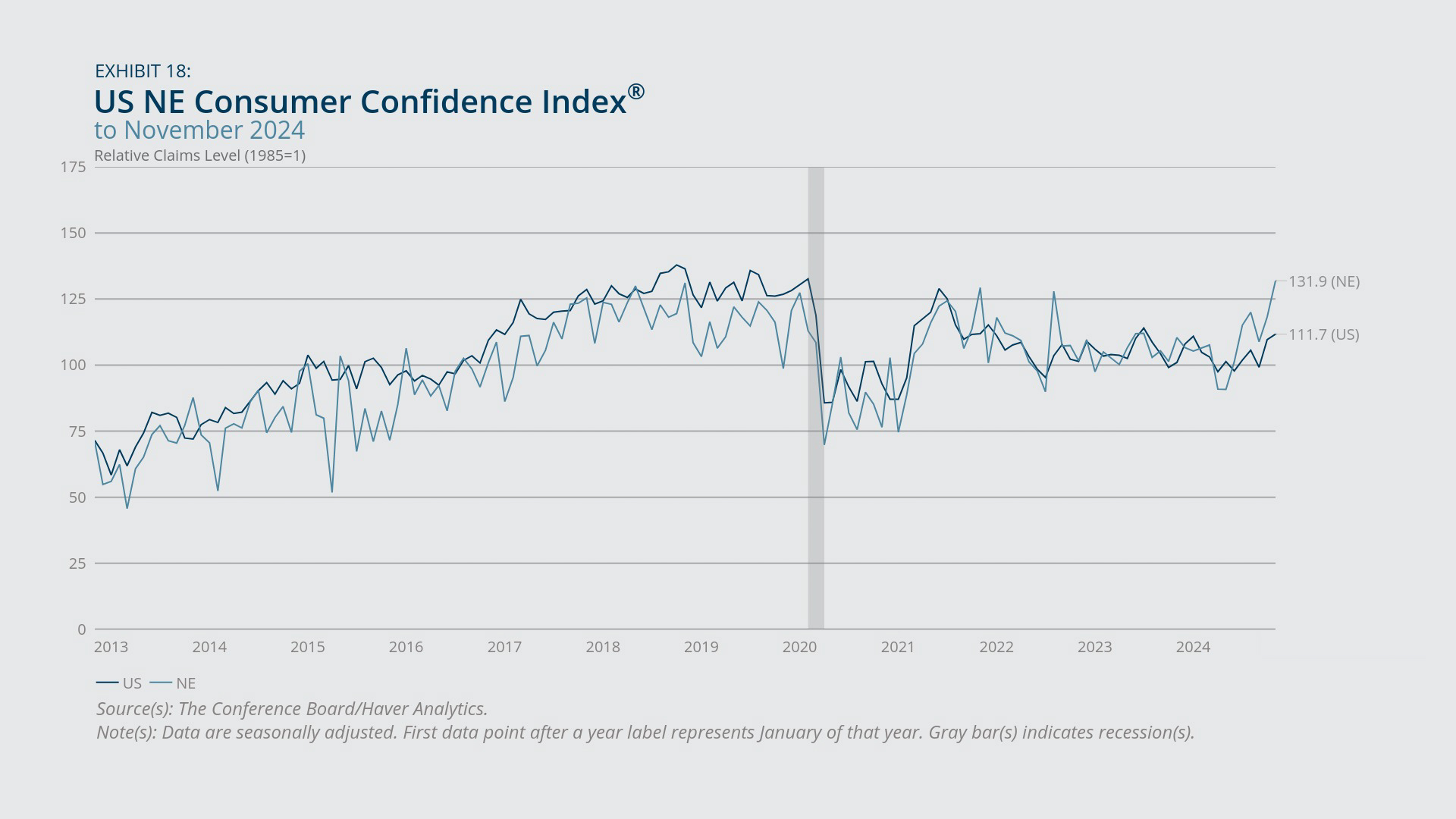

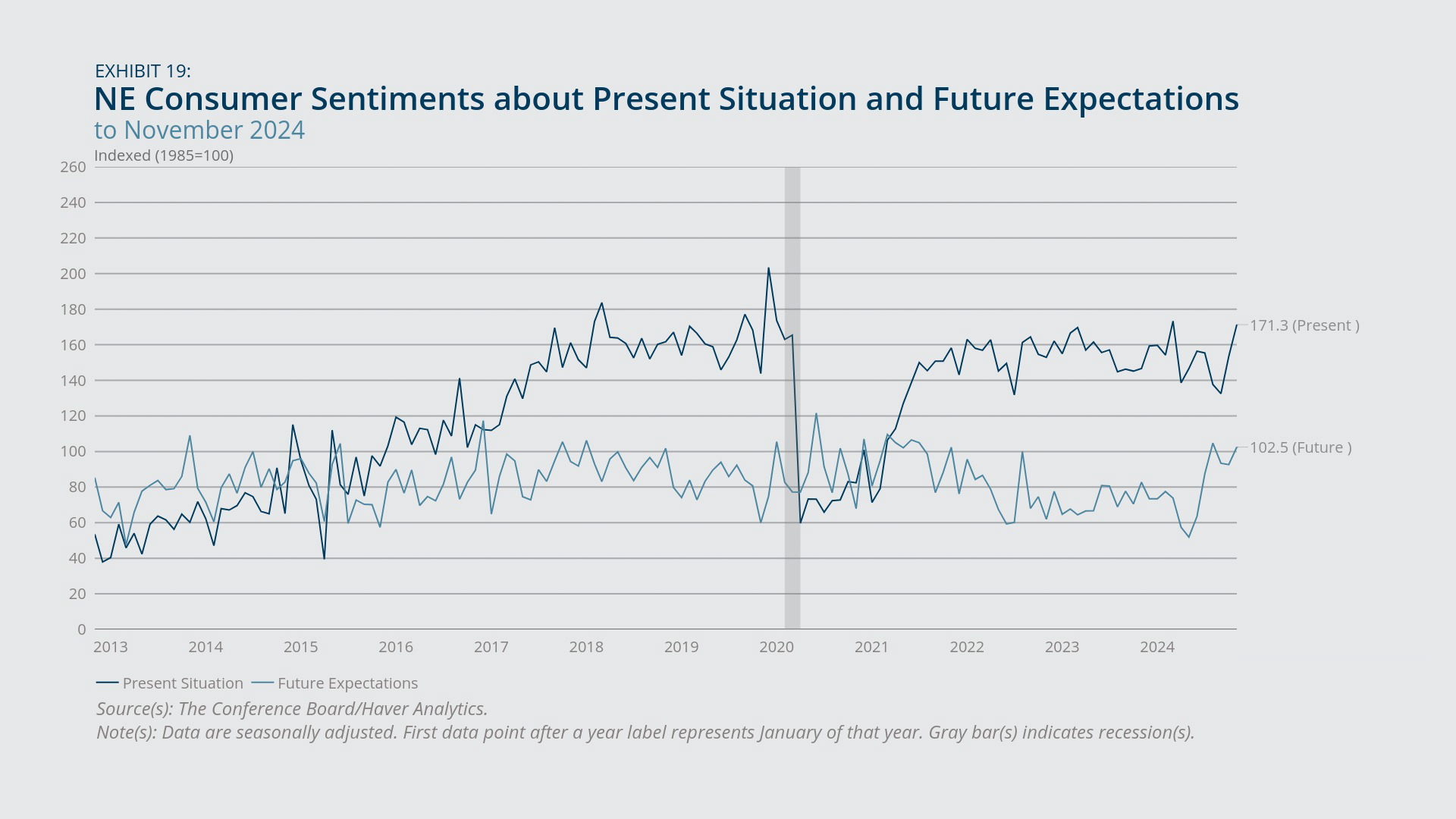

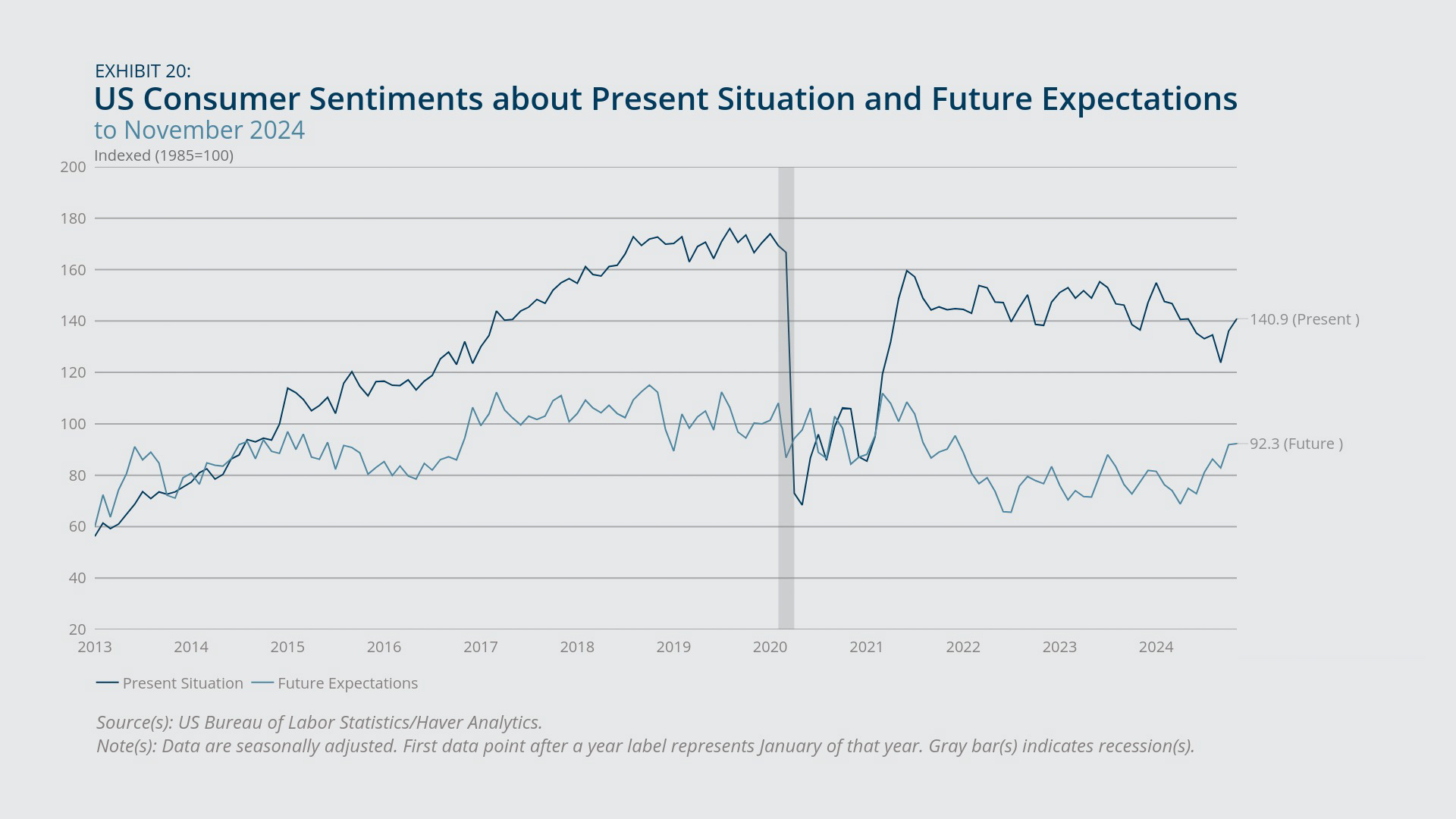

Consumer Confidence

- Consumer confidence in New England and across the United States displayed an upward trend over the 12-month period ending in November 2024, with the latest regional index surpassing the 2019 benchmark and the national index remaining modestly below the 2019 benchmark.

- The higher level of confidence in the region compared with 2019 is attributed to consumers' increased optimism about the economic outlooks, whereas consumers’ lower confidence nationwide is driven by weaker sentiment regarding their present economic situation and lower expectations for the future.

Consumer confidence in the region, as indicated by the Conference Board's Consumer Confidence Index, grew 19 percent year-over-year in November 2024 (Exhibit 17). The index exhibited an upward trend in the preceding 12 months both in New England and across the United States (Exhibit 18). The latest confidence indexes in the region and nationwide are 131.9 and 111.7, respectively, reflecting an increase of 17.6 and a decrease of 16.6 from the 2019 baseline levels. In New England, the higher level of confidence compared with the pre-pandemic period is attributed primarily to consumers’ improved future expectations (Exhibit 19), whereas nationally, the gap is driven by weaker sentiments about the present economic situation and weaker future expectations, though both did improve in recent months (Exhibit 20).

{kind=link}

Federal Reserve Bank of Boston

{kind=link}

Federal Reserve Bank of Boston

{kind=link}

Federal Reserve Bank of Boston

{kind=link}

Federal Reserve Bank of Boston

Endnotes

- The decline in the separations rate resulted from a falling quits rate, not from changes in the layoffs rate, which remained stable throughout this period.

About the Authors

About the Authors

Pinghui Wu,

Federal Reserve Bank of Boston

Pinghui Wu is a senior economist with the New England Public Policy Center at the Federal Reserve Bank of Boston.

Email: Pinghui.Wu@bos.frb.org

Annie Liu,

Federal Reserve Bank of Boston

Annie Liu is a senior research assistant with the New England Public Policy Center in the Federal Reserve Bank of Boston Research Department.

Kelly Jackson,

Federal Reserve Bank of Boston

Kelly Jackson is a senior data analyst in the Federal Reserve Bank of Boston Research Department.

Acknowledgments

Resources

Keywords

- Regional economy ,

- Economic Conditions ,

- New England