New England Economic Conditions through September 3, 2024

Key Takeaways

- Payroll employment in New England grew year-over-year by 1.2 percent in July 2024 as the region continued to exceed its pre-pandemic employment benchmark, but 1,300 jobs were lost during the month. Employment in educational and health services rose by 3.2 percent over the past year to lead growth among sectors, while the largest year-over-year employment declines occurred in the information and manufacturing sectors (3.6 percent and 1.3 percent, respectively).

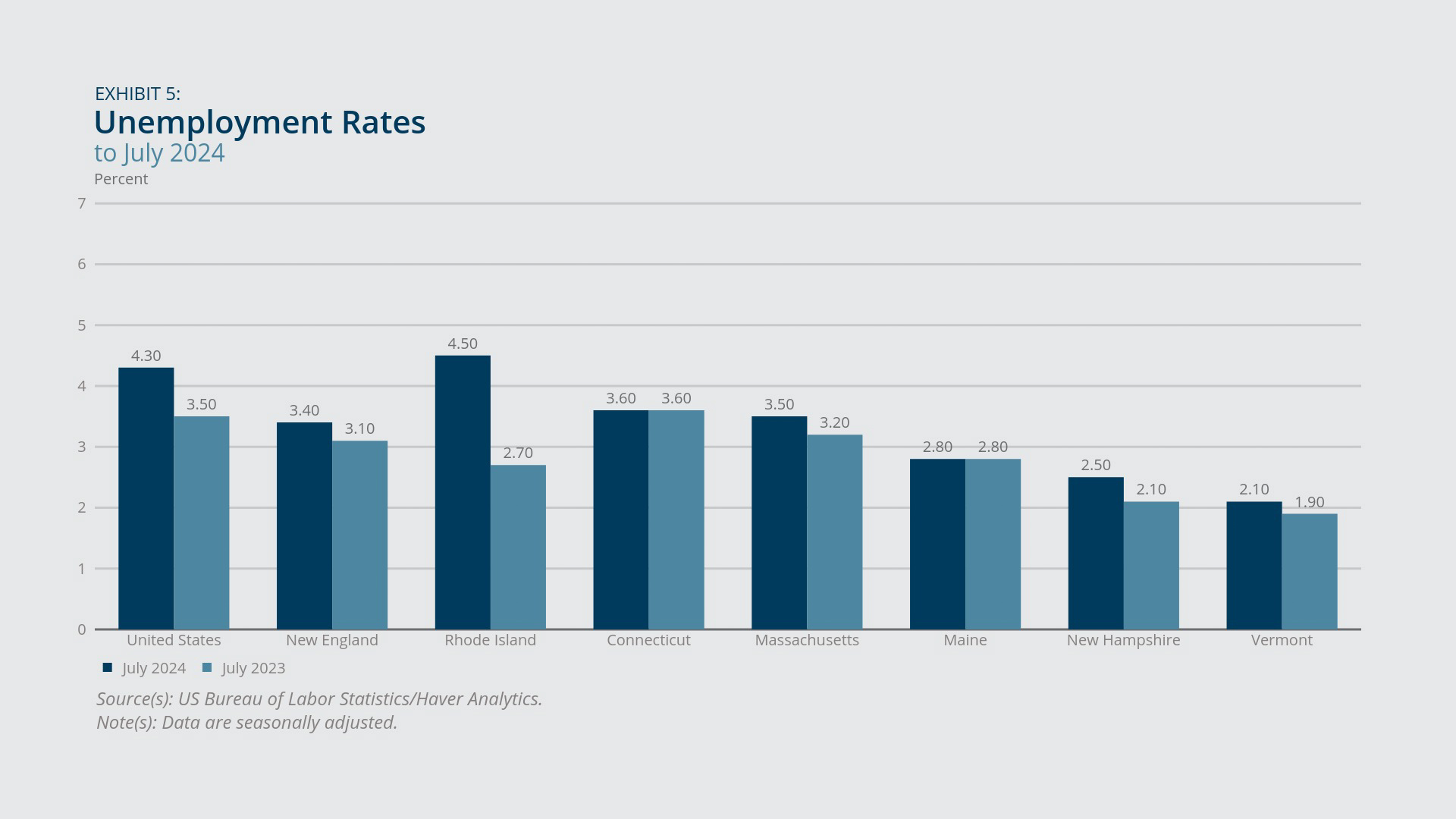

- Unemployment in New England was 3.4 percent in July 2024, which was below the national rate of 4.3 percent but represents a year-over-year increase of 0.3 percentage point. Unemployment rates in each New England state remained the same or grew year-over-year, including in Rhode Island, where the notable increase was at least partly due to a higher labor force participation rate.

- Year-over-year price growth for July 2024 was faster in New England (3.5 percent) compared with the United States overall (2.9 percent). Prices in the region grew most rapidly for shelter, fuel and utilities, and medical product categories.

- New England house prices increased more quickly year-over-year than concurrent house-price growth in the United States in the second quarter of 2024. Vermont’s growth rate was the fastest in the country, and Rhode Island’s ranked third.

Sign up for new research and data on the New England economy.

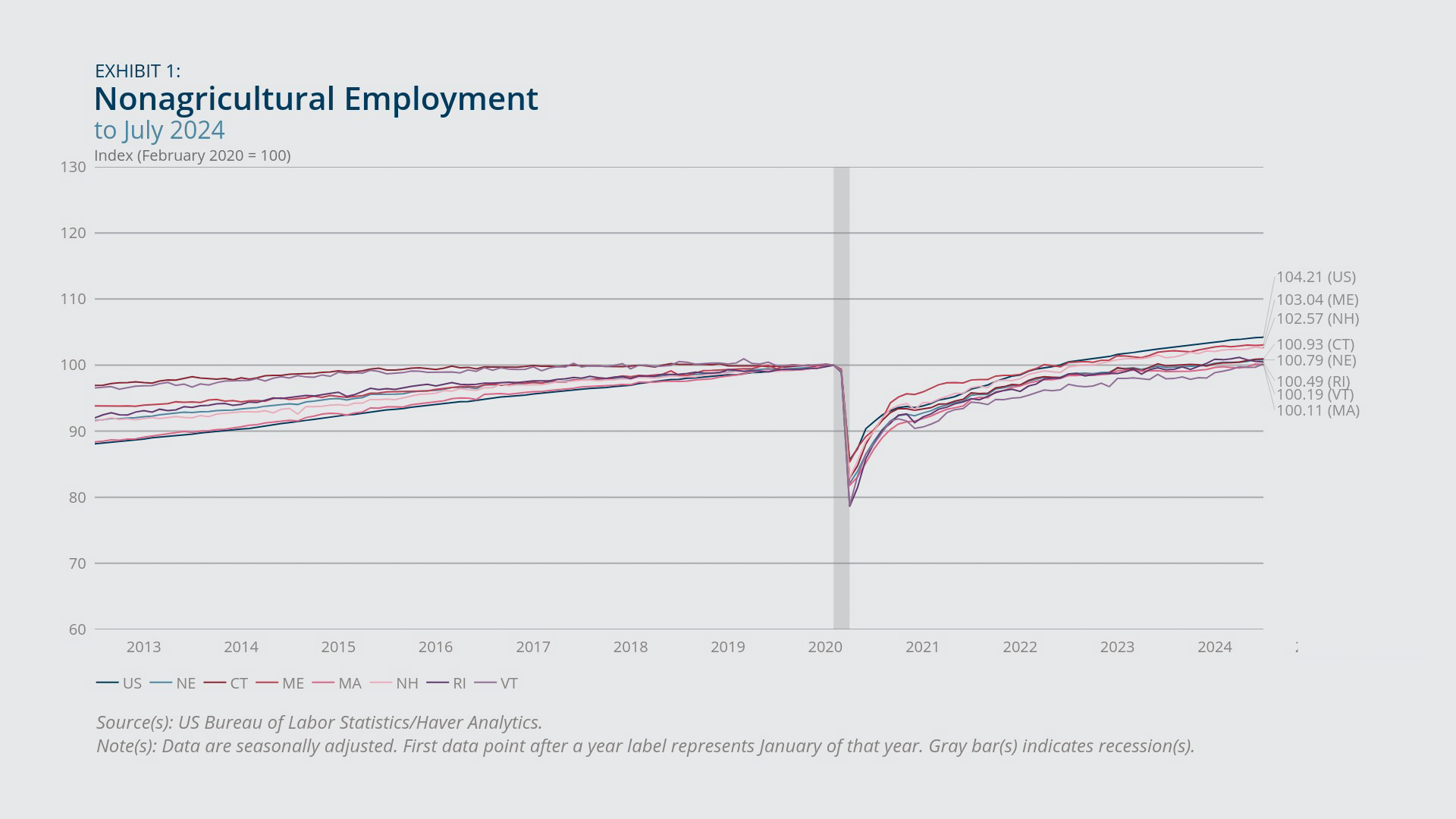

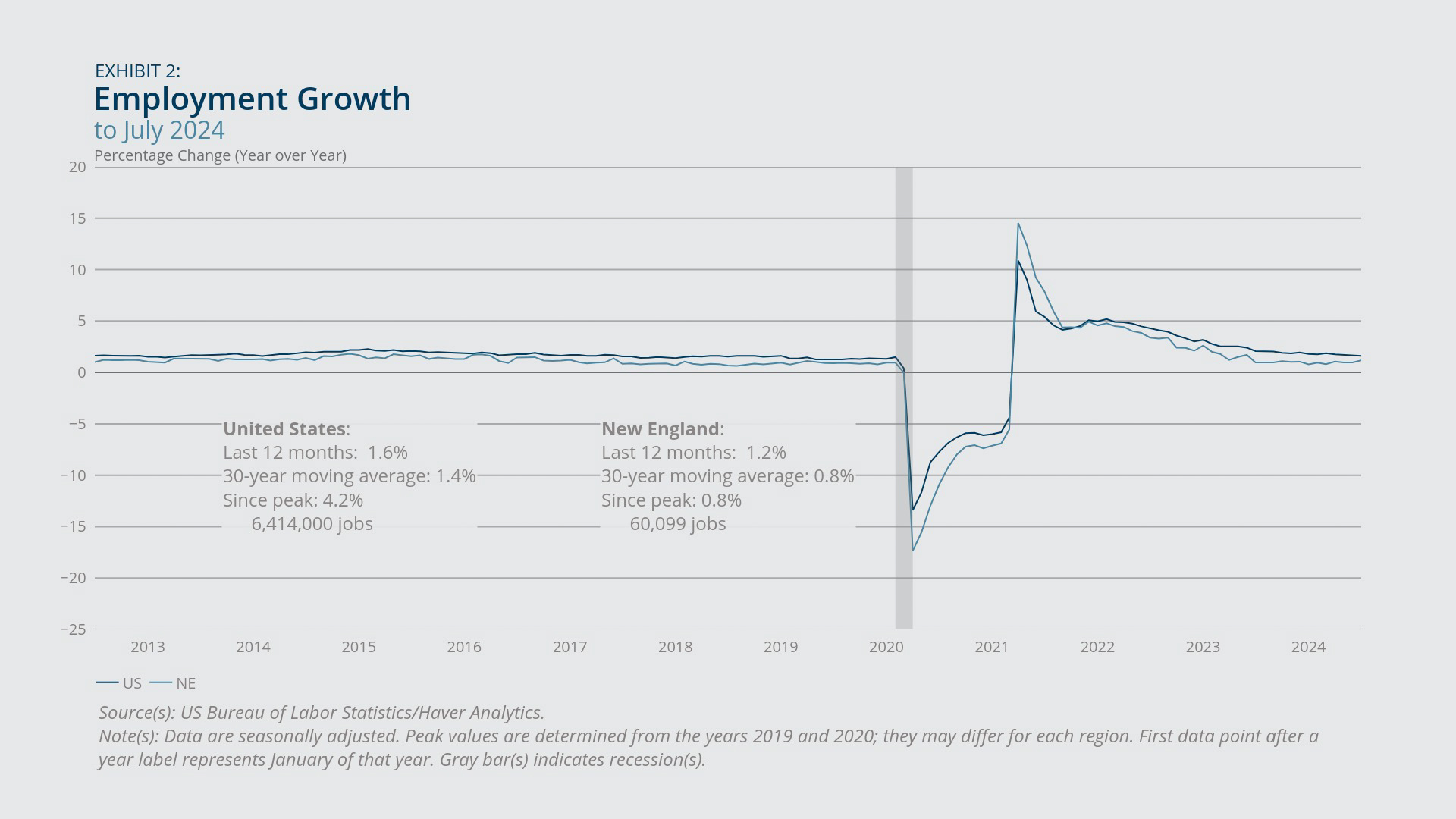

Payroll Employment

- Payroll employment in New England grew year-over-year by 1.2 percent in July 2024 and remained above its pre-pandemic employment benchmark, though the region did lose 1,300 jobs during the month.

- Over the past year—and since the onset of the COVID-19 pandemic—employment has grown notably in educational and health services, but negative job growth in the supersectors reflecting information; manufacturing; and trade, transportation, and utilities has slowed overall employment growth in the region.

New England continued to exceed its pre-pandemic payroll employment benchmark in July 2024, though these employment gains were diminished by a loss of 1,300 jobs during the month (Exhibit 1). Employment growth from February 2020 to July 2024 remained markedly slower in the region (0.8 percent) than in the nation as a whole (4.2 percent). New England exhibited more robust employment growth over the past year, although this recent growth is still below the corresponding year-over-year growth rate in the United States (1.2 percent versus 1.6 percent) (Exhibit 2). Employment in each New England state has grown beyond pre-pandemic benchmarks, led by the rates in Maine and New Hampshire (3.0 percent and 2.6 percent above February 2020 levels, respectively). However, even the growth rates in those two states are below the corresponding national rate.1

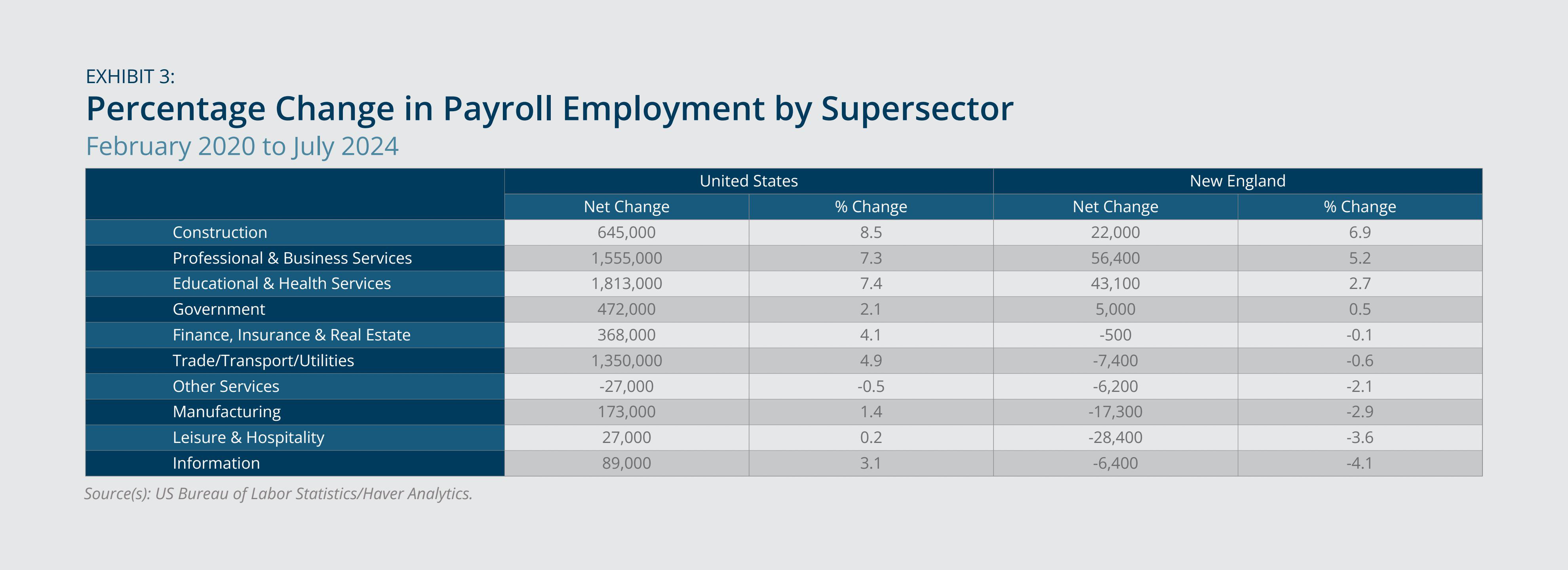

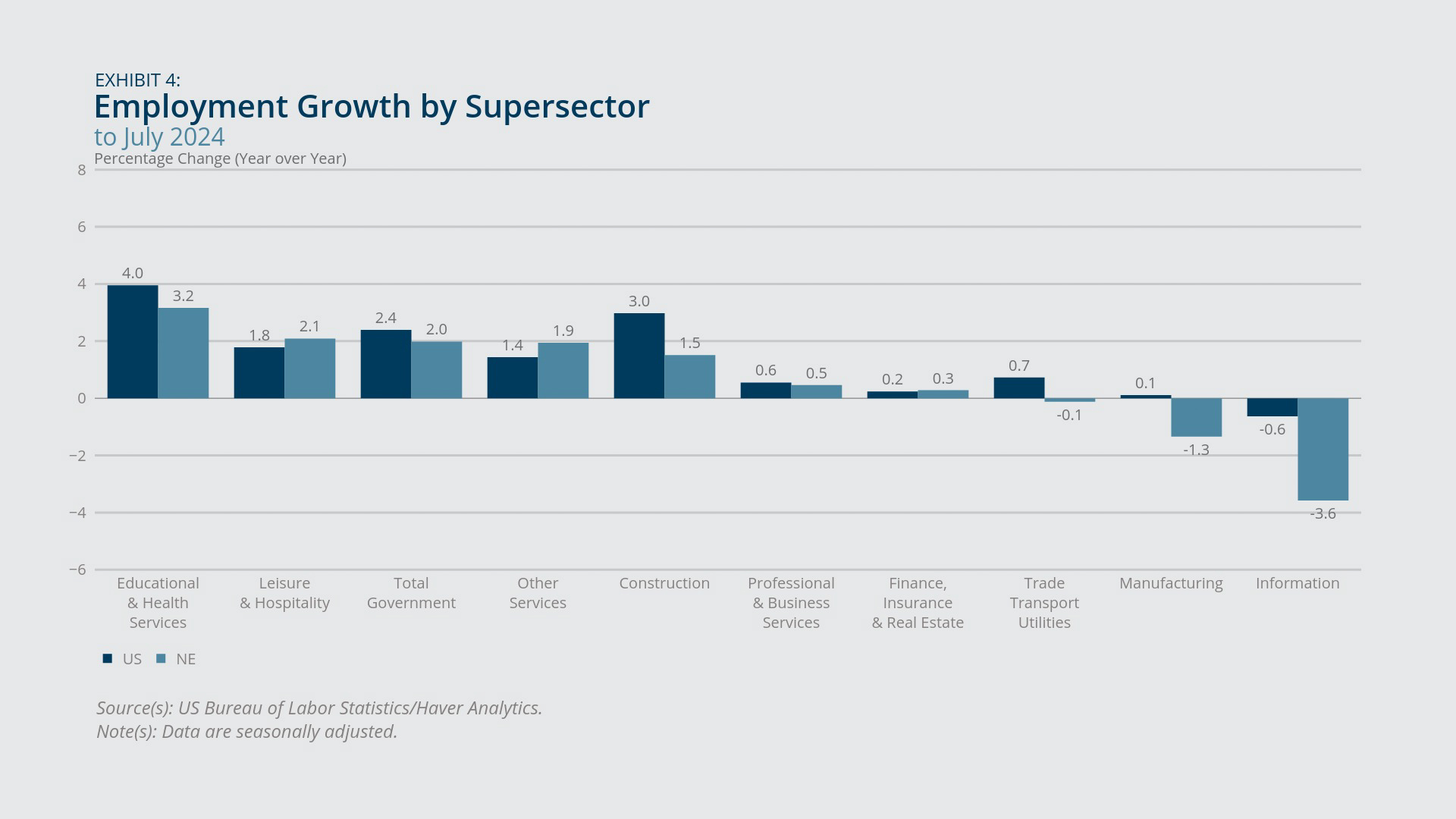

Employment growth in New England also varied across sectors. From the start of the pandemic through July 2024, the construction sector experienced the fastest job growth (6.9 percent), followed by professional and business services and educational and health services (5.2 percent and 2.7 percent, respectively) (Exhibit 3). By contrast, employment in the information sector remained 4.1 percent below its February 2020 level, reflecting the largest growth shortfall in the region. The leisure and hospitality (3.6 percent lower), manufacturing (2.9 percent lower), and trade, transportation, and utilities (0.6 percent lower) sectors similarly exhibited post-pandemic employment declines, mitigating overall employment growth in the region. In terms of year-over-year job growth, educational and health services exhibited the largest increase in the region (3.2 percent) in July 2024, while information; manufacturing; and trade, transportation, and utilities once again displayed negative employment growth (year-over-year declines of 3.6 percent, 1.3 percent, and 0.1 percent, respectively) (Exhibit 4).2

Preliminary Benchmark Revisions

On August 21, 2024, the Bureau of Labor Statistics released a preliminary estimate of its annual benchmark revision to the payroll employment data. The preliminary estimate, available only for the United States, indicated that 818,000 fewer jobs were added in the nation over the 12-month period ending in March 2024.3 This estimate suggests employers added roughly 174,000 jobs per month, on average, during the noted one-year period. Given existing data that indicate approximately 242,000 jobs per month were added from April 2023 through March 2024 on average, the preliminary adjustment reflects a downward revision of 28 percent. Final benchmark revisions for all payroll survey data, for the country as a whole and for each US state, will not be available until early 2025. However, applying the same 28 percent downward revision to New England would suggest roughly 17,200 fewer jobs were added in the region over the 12-month period ending in March 2024. That calculation suggests New England employers added about 3,600 jobs per month from April 2023 through March 2024, on average, compared with existing data that indicate roughly 5,100 jobs per month, on average, were added during that period.4

{kind=link}

Federal Reserve Bank of Boston

{kind=link}

Federal Reserve Bank of Boston

{kind=link}

Federal Reserve Bank of Boston

{kind=link}

Federal Reserve Bank of Boston

Unemployment and Labor Force Participation

- The unemployment rate in New England was below the US rate and experienced a modest year-over-year increase.

- Unemployment rates throughout the region remained the same or rose year-over-year, including Rhode Island’s rate, which increased notably due at least partly to an elevated labor force participation rate.

Unemployment in New England was 3.4 percent in July 2024 based on household surveys, reflecting a year-over-year increase of 0.3 percentage point. It fell below the corresponding national rate, which grew 0.8 percentage point year-over-year to 4.3 percent (Exhibit 5). Among the New England states, unemployment rates ranged from a low of 2.1 percent in Vermont to a high of 4.5 percent in Rhode Island. Most states in the region experienced a year-over-year increase in the unemployment rate, while Connecticut and Maine experienced no change. Notably for Rhode Island, the unemployment rate increased by 1.8 percentage points from July 2023 to July 2024. That state has seen unemployment remain the same or rise every month since May 2023, when it was 2.6 percent.

Labor force participation rates (Exhibit 6) and rates of layoffs and discharges (Exhibit 7) help identify factors likely contributing to the observed changes in unemployment rates throughout New England, including Rhode Island. In the region, the participation rate increased year-over-year by 0.8 percentage point in July 2024 to 65.0 percent, exceeding the corresponding 0.1 percentage point rise in the national rate to 62.7 percent. Participation rates rose over this period for every state in the region, led by an increase of 1.7 percentage points in Rhode Island that resulted in a July 2024 rate of 65.2 percent. The observed changes in participation rates, combined with rates of layoffs and discharges in June 2024, which remained the same or increased slightly, suggest both mechanisms likely help explain recent trends in unemployment rates.5

{kind=link}

Federal Reserve Bank of Boston

{kind=link}

Federal Reserve Bank of Boston

{kind=link}

Federal Reserve Bank of Boston

Labor Costs

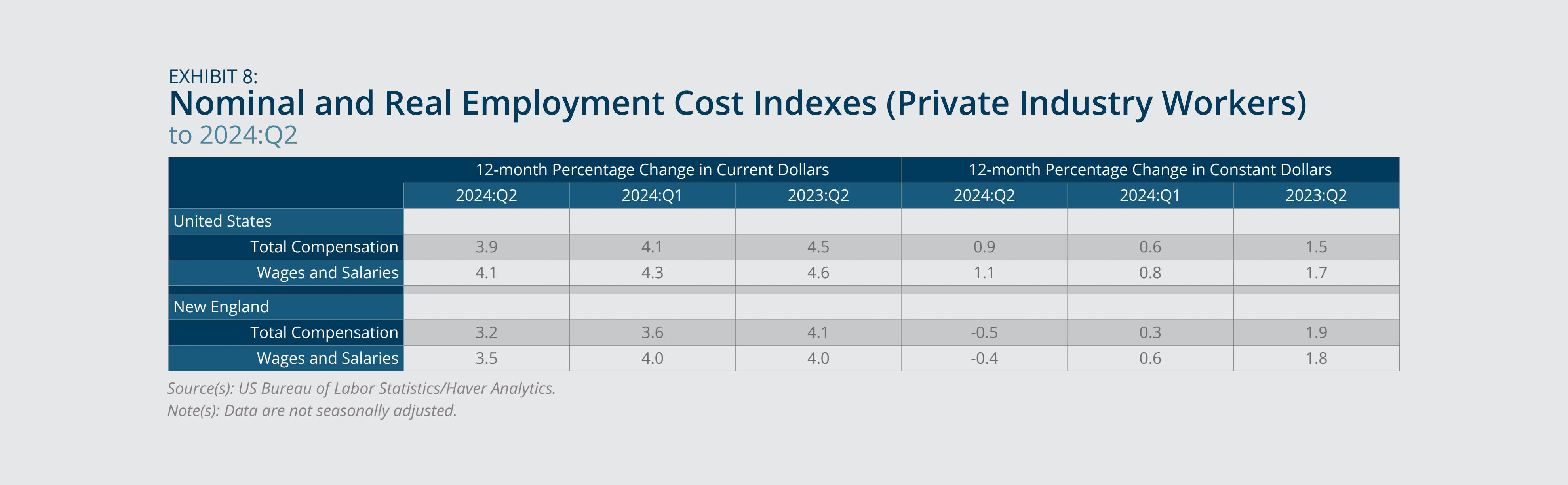

- Real labor costs fell for private-industry workers in New England, while such costs rose in the United States.

In the second quarter of 2024, New England experienced year-over-year growth in nominal labor costs for private-industry workers, although this growth rate was lower than the rate for the first quarter of 2024 (Exhibit 8). While the region saw nominal growth in wages and salaries (3.5 percent) and total compensation (3.2 percent), accounting for inflation results in year-over-year decreases in those measures for the region’s private-industry workers (–0.4 percent for wages and salaries and –0.5 percent for total compensation). This slight decline in real labor costs contrasts with a small rise for the first quarter of 2024, reflecting diminished nominal growth in labor costs as well as elevated inflation rates. In the nation, real labor costs showed positive growth in the second quarter of 2024 (1.1 percent for wages and salaries and 0.9 percent for total compensation). Similar metrics measured more recently also indicate positive growth.6

{kind=link}

Federal Reserve Bank of Boston

Inflation

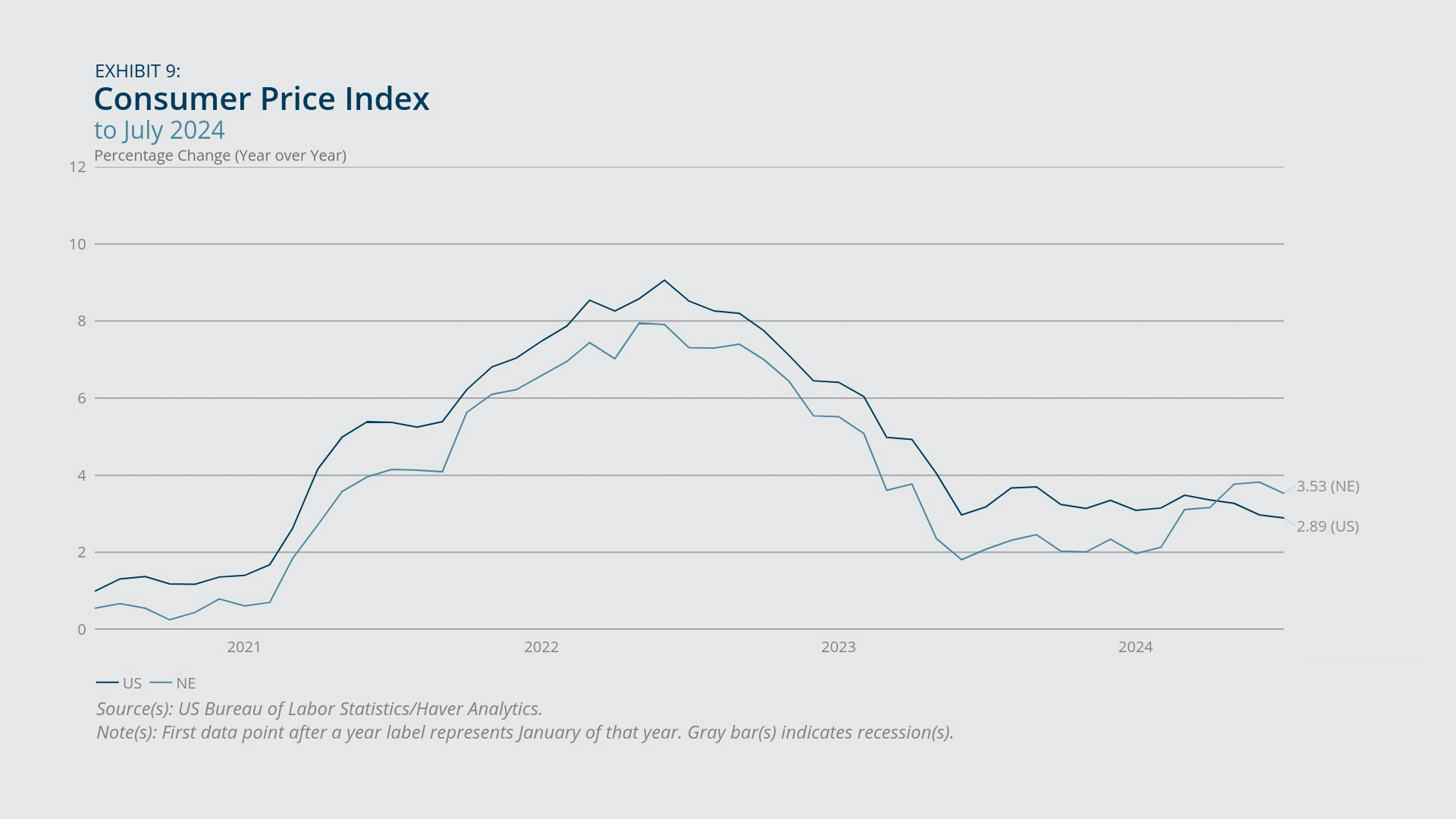

- New England inflation exceeded price growth in the United States, and it was higher than it was in the region in the second half of 2023 and early 2024.

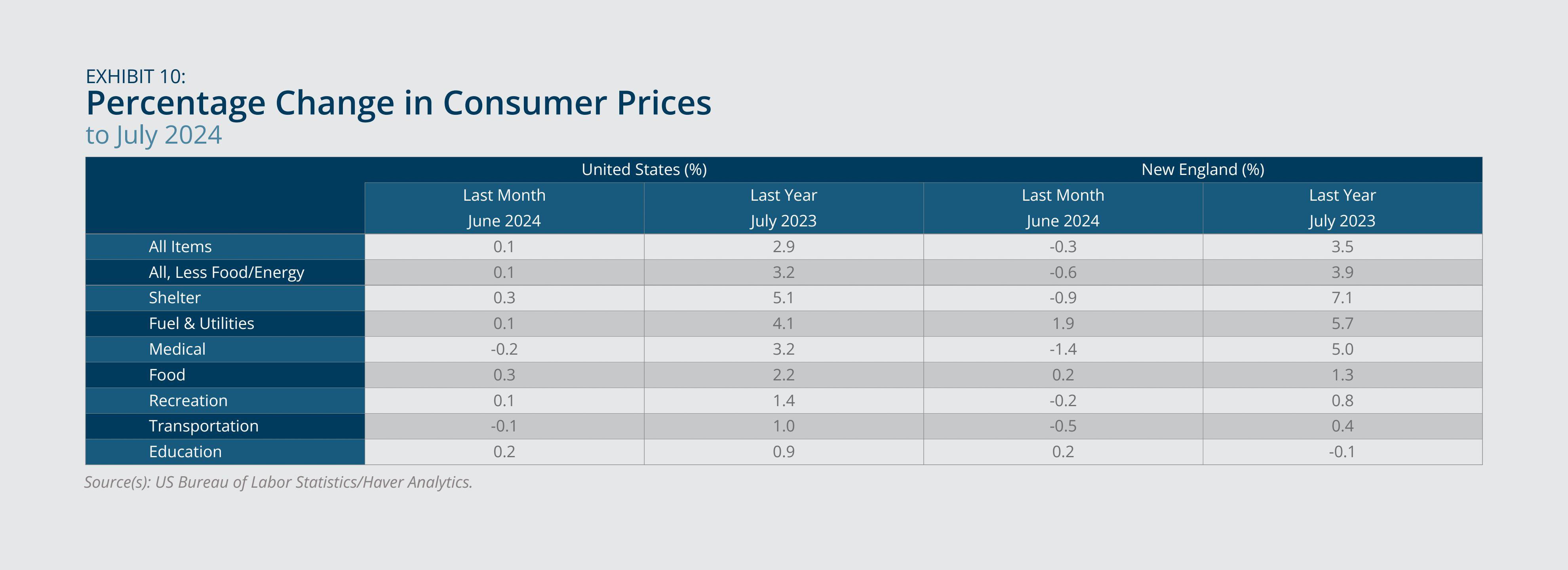

- The shelter, fuel and utilities, and medical expenditure categories experienced the largest price growth in the region.

In July 2024, the inflation rate for New England was roughly 0.6 percentage point above the US rate, based on the Consumer Price Index: 3.5 percent versus 2.9 percent (Exhibit 9). These annual growth rates reflect a slight drop for the region (0.3 percentage point) and the nation (0.1 percentage point) compared with annual growth in the previous month. However, the current inflation rate in the region is still elevated compared with the second half of 2023 and start of 2024, when the rate typically hovered near 2.0 percent.

The shelter, fuel and utilities, and medical expenditure categories experienced the fastest price growth in the region, while education was the sole category that experienced a year-over-year decline (Exhibit 10). At the national level, all expenditure categories displayed positive annual price growth. Core inflation (which excludes food and energy prices) in New England (3.9 percent) exceeded the overall inflation rate in the region, reflecting in part the noted rise in shelter prices (7.1 percent).

{kind=link}

Federal Reserve Bank of Boston

{kind=link}

Federal Reserve Bank of Boston

House Prices

- New England experienced higher annual house-price growth compared with the nation.

- Vermont’s house-price growth was the fastest in the nation, and Rhode Island’s ranked third.

House prices, as measured by the Federal Housing Finance Agency House Price Index, increased year-over-year for New England in the second quarter of 2024 (7.9 percent), surpassing the concurrent national rate (5.7 percent) (Exhibit 11). Among the region’s states, Vermont (13.3 percent) and Rhode Island (10.0 percent) saw the fastest house-price growth, and Maine (6.3 percent) saw the slowest. Indeed, Vermont’s house-price growth was the fastest in the country, and Rhode Island’s ranked third.7 House prices in Maine had been growing more rapidly than their current rate, but the growth slowed due likely in part to reduced demand.8

Additional variation in house-price growth occurred across metropolitan areas within states (Exhibit 12). For instance, in Maine, house-price growth ranged from 4.2 percent in the Lewiston–Auburn metropolitan area to 8.2 percent in the Portland–South Portland–Biddeford metropolitan area.

{kind=link}

Federal Reserve Bank of Boston

{kind=link}

Federal Reserve Bank of Boston

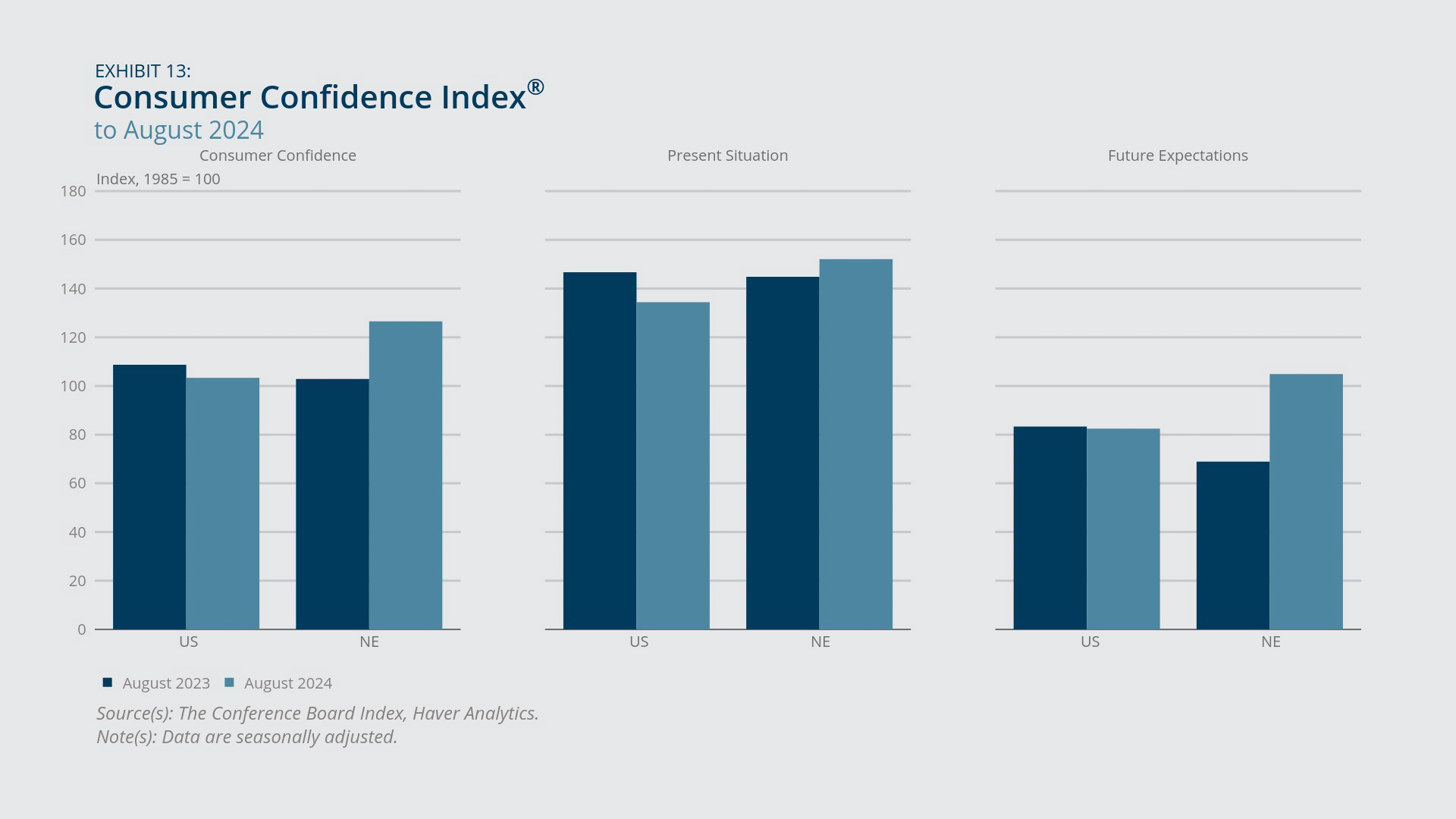

Consumer Confidence

- Consumers in New England were more confident in August 2024 than they were a year earlier, while nationally, confidence fell slightly over that period.

Consumer confidence in August 2024, as measured by the Conference Board’s Consumer Confidence Index, experienced a year-over-year increase in New England but a slight decrease in the United States (Exhibit 13). In the region, the increase was largely driven by improved future expectations, as consumer sentiment about the present rose more modestly. By contrast, the national decrease in consumer confidence resulted primarily from a less positive outlook about the present, as consumer expectations about the future declined minimally. Relative to how they felt the preceding month, consumers in August were more positive about business conditions, but they also were more worried about the labor market, especially the market’s future.9

{kind=link}

Federal Reserve Bank of Boston

Endnotes

- By contrast, since February 2020, employment-to-population ratios among New England states have fallen the most in New Hampshire and Maine (declines of 2.6 percentage points and 1.9 percentage points on February 2020 ratios of 66.5 percent and 60.0 percent, respectively). Rhode Island is the only state in the region with positive growth in its employment-to-population ratio since the onset of the pandemic (an increase of 0.4 percentage point on a February 2020 ratio of 61.9 percent), although all New England states exhibited such growth in the previous year from July 2023 to July 2024.

- Further disaggregating, year-over-year employment growth in New England in July 2024 was lower for educational services (0.5 percent) than it was for health care and social assistance (3.9 percent).

- See “CES Preliminary Benchmark Announcement,” Bureau of Labor Statistics, August 21, 2024. Each year, the payroll survey (formally, Current Employment Statistics, or CES) employment estimates are “benchmarked to comprehensive counts of employment for the month of March. These counts are derived from state unemployment insurance (UI) tax records that nearly all employers are required to file. For National CES employment series, the annual benchmark revisions over the last 10 years have averaged plus or minus one-tenth of one percent of total nonfarm employment. The preliminary estimate of the benchmark revision indicates an adjustment to March 2024 total nonfarm employment of –818,000 (–0.5 percent).”

- Note that (5,100 jobs – 3,600 jobs) x 12 months = 18,000 jobs over a one-year period, which differs from the stated 17,200 jobs. This difference is due to rounding, as the precise calculation is (5,075 jobs – 3,644 jobs) x 12 months = 17,172 jobs over a one-year period.

- See Omar Mohammed, “Rhode Island’s Unemployment Rate Is Up, But That May Not Be Bad,“ Boston Globe, August 23, 2024. Additionally, July 2024 rates of layoffs and discharges will not be available until the corresponding data from the Job Openings and Labor Turnover Survey are released by the Bureau of Labor Statistics in early September 2024.

- Seasonally adjusted real average hourly earnings in the United States increased 0.7 percent year-over-year for July 2024. See Bureau of Labor Statistics, “Real Earnings Summary,” Economic News Release, August 14, 2024.

- See “US House Prices Rise 5.7 Percent over the Last Year; Up 0.9 Percent from the First Quarter of 2024,” Federal Housing Finance Agency press release, August 27, 2024.

- See Zara Norman, “The Conflicting Clues That Maine’s Housing Market Is Leveling Off,“ Bangor Daily News, April 11, 2024. Additionally, for example, Maine experienced year-over-year house-price growth of 11.7 percent for the third quarter of 2023, which ranks second in the region behind corresponding growth for that quarter in Vermont.

- See “US Consumer Confidence Rises Slightly in August,” Conference Board press release, August 27, 2024.

About the Authors

About the Authors

Osborne Jackson,

Federal Reserve Bank of Boston

Osborne Jackson is a principal economist with the New England Public Policy Center in the Federal Reserve Bank of Boston Research Department.

Email: Osborne.Jackson@bos.frb.org

Acknowledgments

Kelly Jackson, Federal Reserve Bank of Boston

Resources

Keywords

- Regional economy ,

- Economic Conditions ,

- New England