College Towns and COVID-19: The Impact on New England

| Key Facts | |

| In New England cities and towns whose economies are heavily reliant on higher education, 45 percent of wages and 38 percent of jobs come directly from the local colleges and universities. | |

| There are 71 financially vulnerable higher education institutions in New England; each has experienced enrollment decline for the last decade and has a limited endowment. | |

| There are 19 cities and towns in New England that are heavily reliant on a financially vulnerable college or university. | |

|

|

Summary

The abrupt closing of college campuses this spring due to the spread of COVID-19 upended the lives of students and their families and disrupted the higher education sector. The impact of these closures and the questions of whether and how to reopen campuses this fall have been widely discussed. Less attention has been paid to the potential consequences for the local economies of the cities and towns that depend heavily on higher education. This issue is particularly important in New England, where in many communities, colleges and universities are among the largest employers and make an outsized contribution to the local economy. The absence of students and campus activities is a major blow to local businesses. And while New England schools generally have avoided large-scale layoffs so far, extended campus shutdowns and pandemic-induced enrollment declines could force some institutions that already are on shaky financial ground to close altogether.1 Continued disruption to the higher education sector could threaten even financially strong institutions. This brief examines the number of cities and towns in the region that are highly dependent on employment and commerce from institutions whose declining enrollments and low endowments make them particularly vulnerable during this period. These are the communities that are most at risk of economic harm due to major pandemic-related disruptions to higher education.

Sign up for new research and data on the New England economy.

Campus closures under COVID-19

As the seriousness of the COVID-19 pandemic became increasingly apparent, almost all higher education institutions in New England (and the United States) closed their campuses and emptied their dorms in March and quickly transitioned to online teaching. Many institutions experienced an immediate hit to their budgets when they issued refunds for room and board. The University of Massachusetts system alone faced $70 million in refunds to students.2 Schools kept faculty on the payroll to complete the semester online, but they differed in the degree to which they continued paying staff responsible for student services, from cooks to coaches.3

With business shutdowns continuing and stay-at-home orders or recommendations remaining in effect in the New England states into April and beyond, institutions moved their summer education programs online or cancelled them. Now the immediate question is, what happens with the fall semester? The options being considered range from fully reopening campuses to canceling the fall semester and restarting with the spring semester in January 2021. Any plans are heavily contingent on the course of the pandemic.4 Depending on which option an institution chooses, some of its incoming students may delay enrollment or reconsider their choice of school. Continuing students are raising questions about the value of online education as compared with the “full experience” of campus life. 5 The American Council on Education predicts that at the national level, college enrollment will drop a total of 15 percent for the 2020–2021 school year.6 Beyond this question there is discussion about the prospect of major pandemic-related disruptions to higher education that would be longer lasting. These could include massive declines in the enrollment of foreign students and large shifts to online learning.7

Enrollment declines would lead to revenue losses for institutions that could result in layoffs. Job losses, coupled with a decreased number of students, likely would cause economic harm to the communities where these colleges and universities are located. Some schools have already begun laying off employees ranging from custodial staff to faculty.8

Higher education employment in New England

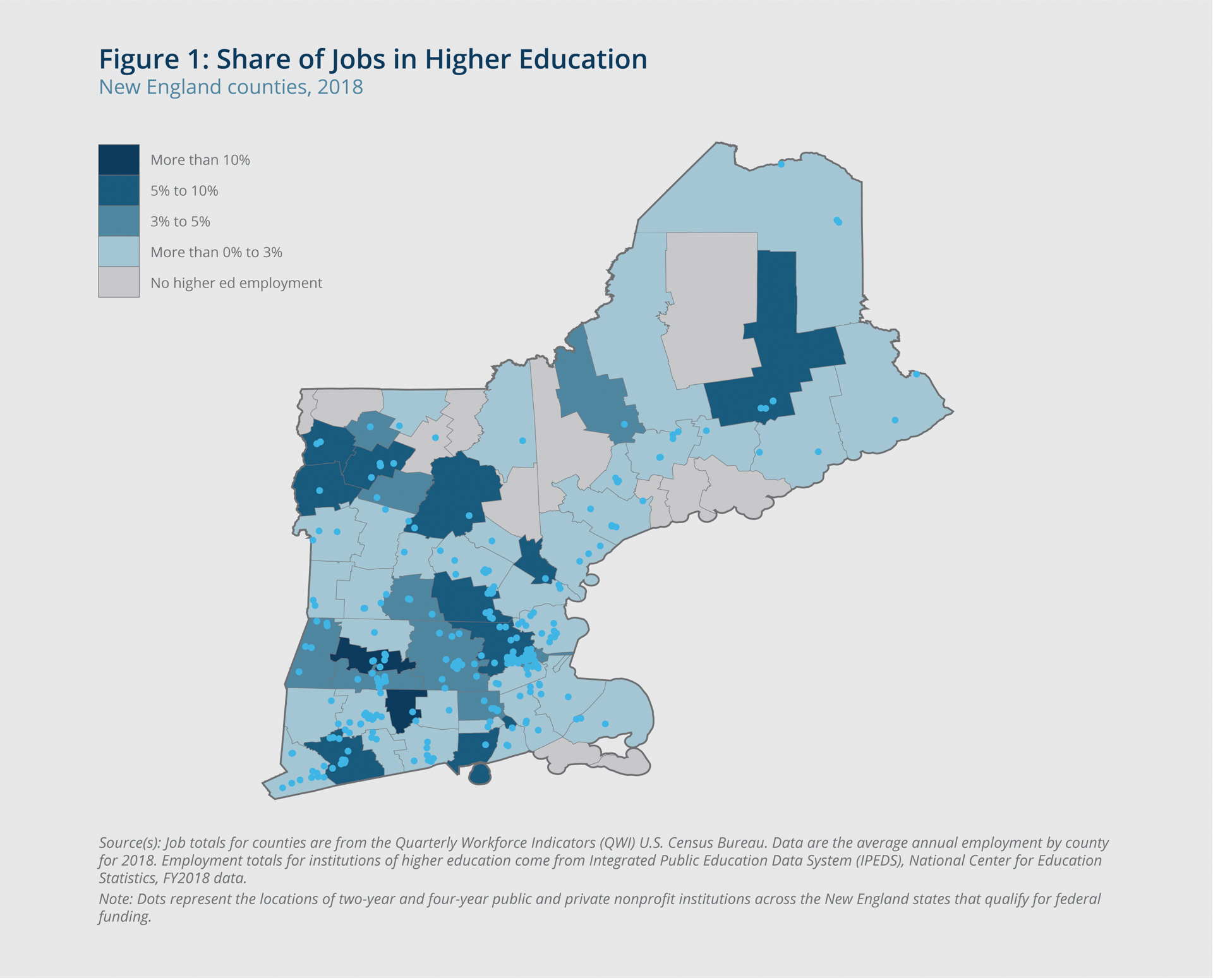

In New England, higher education has above-average importance for the regional economy, accounting for 3.4 percent of total employment compared with 2.5 percent nationwide. Some communities are heavily dependent on higher education as a share of employment, including Durham, New Hampshire; Cambridge, Massachusetts; and South Kingstown, Rhode Island. Figure 1 illustrates the share of jobs that public and private nonprofit colleges and universities provide in each New England county. In two New England counties, such schools account for more than 10 percent of all employment, and in another 11 counties, the sector employs more than 5 percent of all workers.

{kind=link}

Federal Reserve Bank of Boston

Employment, wages, and enrollment in the cities and towns most reliant on higher education

New England is home to 208 public and private nonprofit colleges and universities, which are located in 119 different cities and towns across the region. In some of these communities, higher education accounts for only a small share of total employment, but in others, the sector accounts for a major share of local economic activity. Table 1 groups these cities and towns into quintiles based on the higher education share of total employment. In the municipalities that are most dependent on higher education (the top 20 percent), the local college or university provides nearly 38 percent of total employment, on average. The communities most dependent on higher education tend to be smaller towns; the average population of the highest-dependency quintile is fewer than 23,000 residents. In many of these top-quintile towns, the higher education institution is the largest local employer. Even in the cities and towns in the middle quintile, which have an average population of more than 56,000, 6.2 percent of jobs, on average, come directly from the local college or university.

Table 1: Employment, Wage, and Enrollment Impact of Higher Education

New England cities and towns with higher education institutions

| Quintile | Higher Ed. Share of Employment (Mean) | Higher Ed. Share of Wages (Mean) | Enrollment to Population (Mean) | Average Population |

| Highest Dependency | 37.9% | 44.8% | 0.47 | 22,642 |

| Second | 12.3% | 12.7% | 0.21 | 41,890 |

| Third | 6.2% | 6.4% | 0.15 | 56,246 |

| Fourth | 3.4% | 3.0% | 0.12 | 51,047 |

| Lowest Dependency | 1.4% | 1.4% | 0.05 | 49,988 |

| Source(s): The job totals for cities and towns are from each state’s department of labor as part of its ES-202 program. Job totals for institutions of higher education and enrollment data come from Integrated Postsecondary Education Data System (IPEDS), National Center for Education Statistics, FY2018 data. Note(s): The sample of cities and towns is limited to those that are locations of higher education institutions. The location reflects where workers are employed and not necessarily where they live. Except for those pertaining to cities and towns in Connecticut, the percentages reflect 2018 annual averages. The latest available data for Connecticut is 2016, which this brief uses. Each quintile includes 24 cities and towns, except for the top quintile, which includes 23. Outliers do not drive the values in the top quintile, and the medians for each quintiles are close to the means. |

||||

In addition to providing a large number of jobs in some communities, colleges and universities tend to pay above-average wages. Among the cities and towns most reliant on higher education employment, the share of wages that come directly from colleges and universities is greater than the share of jobs: 44.8 percent versus 37.9 percent, on average.

In many cities and towns that are home to higher education institutions, the students are a crucial component of the local consumer base. Among the communities in the quintile most dependent on higher education, the average ratio of enrolled students (excluding online-only students) to the local population is 0.47.9 The average ratio of students to the local population is relatively high in most New England communities where colleges and universities are located; it falls below 0.10 in only the least-dependent quintile, and in 25 communities, there is at least one post-secondary student for every three residents. The departure of students when campuses closed early in the spring semester has had a major impact on the volume of goods and services consumed in New England’s college towns. This is particularly true for communities that are home to residential schools, but it is also the case in the cities and towns of commuter schools, as traffic to local businesses declines when students do not attend classes in person.

Higher education permeates many aspects of the communities beyond direct employment, wages, and student-driven consumption; it extends to conferences, athletic events, and more. However, this report is not an economic impact statement intended to identify all the benefits of the sector as a whole or the benefits of a school to a community.10 The goal of this report is to help better understand the number of New England communities that could be at risk of economic harm from major disruptions to the higher education sector due to the COVID-19 pandemic.

For some institutions, financial strain may be too great

If the pandemic leads to a more dramatic disruption in higher education, such as sharp declines in enrollment or increased reliance on distance learning, the impact could vary substantially across the cities and towns where institutions are located.11 Some colleges and universities have a strong foundation, with a stable enrollment and a large endowment. Others are in a much more precarious situation, with a declining enrollment and little, if any, endowment. Major disruptions could push such fragile institutions toward permanent closure, which could have profound consequences for their cities and towns.

Data show the number of higher education closures rising steeply in recent years across the United States, with private for-profit institutions accounting for most of them.12 The pandemic could force more nonprofit schools to close. Moody’s Investors Service recently declared that due to the pandemic, the outlook for the higher education sector is changing from stable to negative.13 By one college advising company’s estimate, before the COVID-19 outbreak, 13 institutions across New England were at risk of closing within the next six years; the company has since increased the count to 25.14 Many of these institutions were making changes to improve their financial footing, but it is unclear now how they will address the revenue losses from refunds for the spring semester and the losses they could incur if enrollment declines or if the fall semester is canceled or moved online.

Schools that rely largely on tuition revenue could be particularly vulnerable to enrollment declines in the fall semester. In contrast, institutions with larger endowments have greater flexibility for meeting the challenges of the pandemic, even though endowments often have restrictions on much of their funds.15

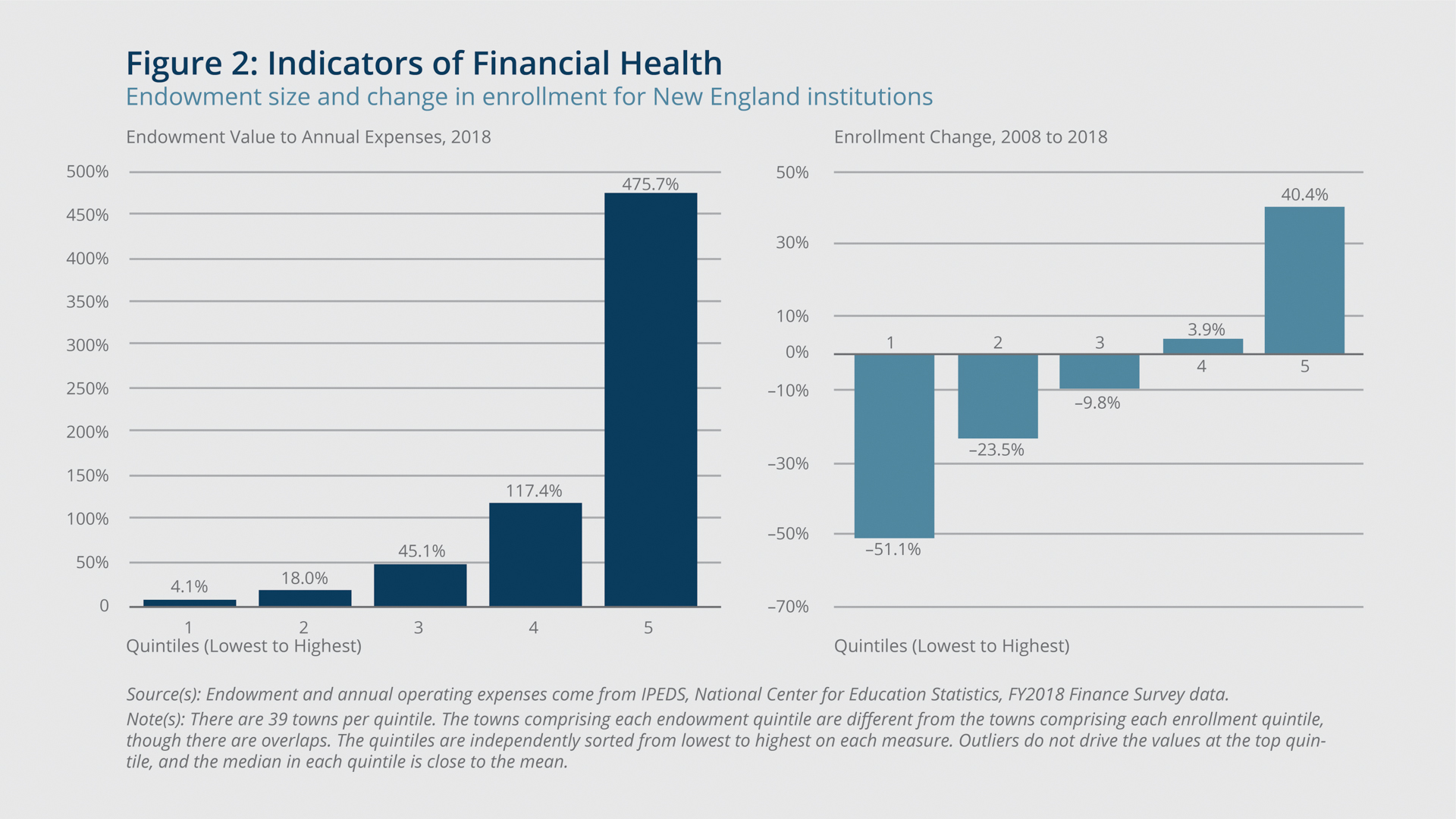

The size of the endowments held by colleges and universities in New England varies dramatically. The left-hand panel of Figure 2 shows that fewer than half of the schools have endowments valued at more than half the amount of their annual expenses. Some of the institutions with the lowest ratios of endowment to expenses are public two-year institutions, which tend to have much smaller endowments than other schools but are the recipients of state and federal appropriations. As the fallout from the pandemic continues, projections for state tax revenues in New England have fallen substantially,16 which could jeopardize some of the funding for these and other public institutions unless policymakers prioritize higher education.

Enrollment trends can be another important factor in a school’s long-term viability. Many of the institutions that have closed in recent years had experienced steep drops in enrollment. The right-hand panel of Figure 2 shows the changes in enrollment for colleges and universities across New England between 2008 and 2018. More than half of the institutions saw their enrollment decline during this period.

{kind=link}

Federal Reserve Bank of Boston

Some schools that were attempting to improve their enrollment and financial situation have lost revenue this fiscal year due to room and board refunds, event postponements and cancellations, donors deferring gifts due to market instability, and increased student financial need.17 In Vermont, a plan was announced to close three state schools partly in response to pandemic-related declining state tax revenue and declining enrollment, but the plan has been shelved, temporarily at least. Governor Scott of Vermont has emphasized that the schools’ financial challenges pre-date the COVID-19 outbreak, and that changes will be necessary if they are to remain open.18

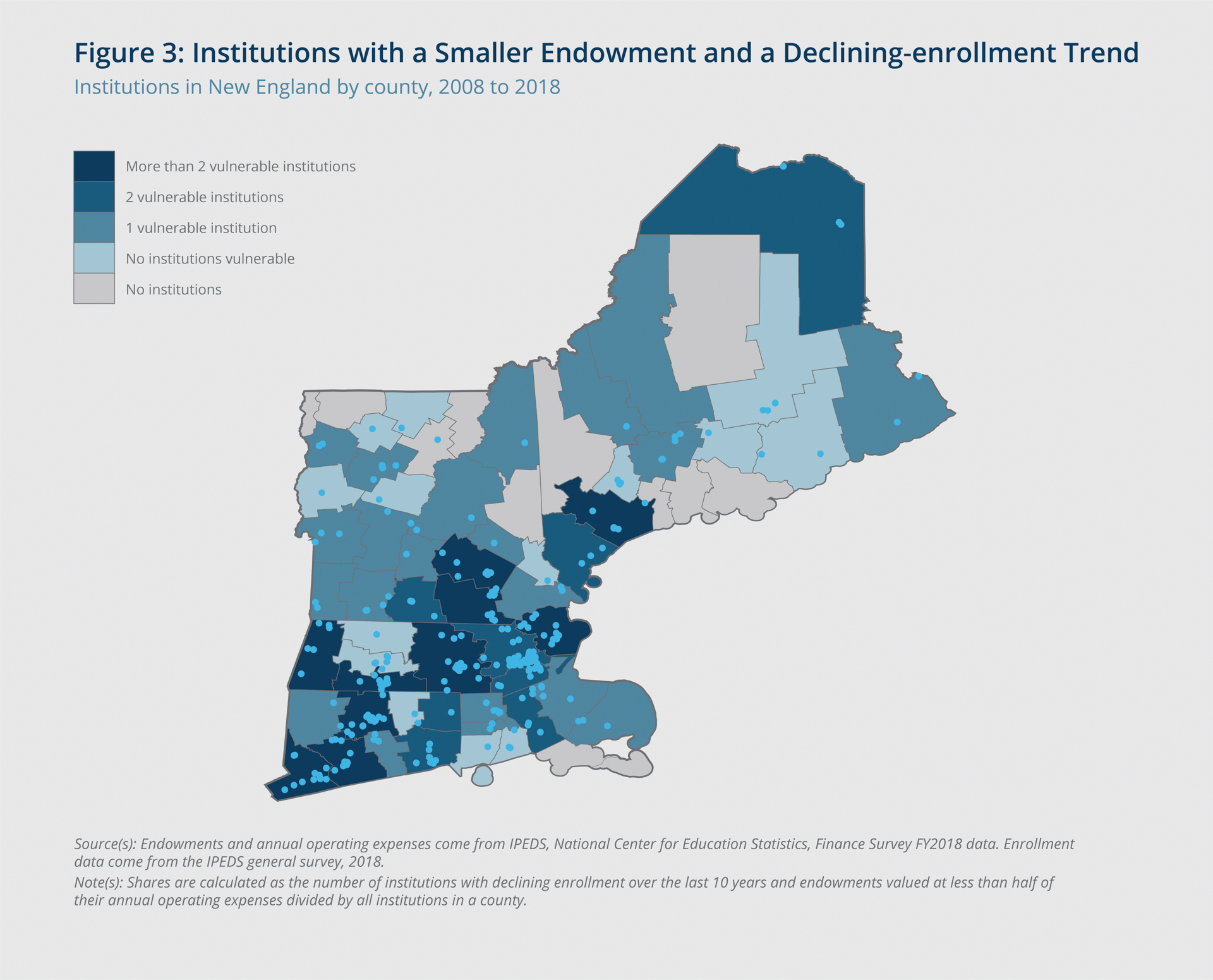

Seventy-one institutions across New England exhibit both declining enrollment over the last decade and a low endowment (a sum that is less than half of their annual operating expenses). Though several additional factors can contribute to the financial vulnerability of an institution, schools with minimal endowments and declining enrollments could be particularly susceptible to potential fallout from the pandemic.19

Figure 3 maps the county-level prevalence of institutions that exhibit both of these signs of financial vulnerability. In 10 counties, more than two institutions could be at risk of closing, based on these criteria.

{kind=link}

Federal Reserve Bank of Boston

Communities that are heavily dependent on higher education and home to an institution at risk of closing are the most vulnerable to a major disruption to the higher education sector. Across New England, 57 cities and towns are heavily dependent on higher education; that is, at least 10 percent of their jobs come directly from the local colleges and universities or the number of enrolled student-to-population ratio of 0.2 (Table 2). Of these cities and towns, 19 are home to an institution that is more financially vulnerable due to its endowment-to-expenses ratio and its enrollment trend. In Massachusetts, half of the higher education dependent communities are home to vulnerable institutions. Maine, with six, has the greatest number of such cities and towns in the region. While both short-term and long-term disruptions to higher education could affect the entire region, these communities likely would feel the largest impact, because the local economies rely so heavily on these schools that may be less equipped to withstand the potential obstacles ahead. Of the 19 cities and towns, two in Massachusetts and one in Vermont are home to multiple institutions, and only one of the institutions in each community meets the higher-risk criteria. These places would still be severely impacted by a closure, but they are not in the same position as cities and towns where the closing of one institution could jeopardize the entirety of the local economic activity associated with higher education.

Table 2: Higher Education Dependent Towns and Higher-Risk Institutions

New England cities and towns with higher education institutions

| State | Number of Heavily Dependent Cities and Towns | Number of Heavily Dependent Cities and Towns with a Higher-Risk Institution | Number of Heavily Dependent Cities and Towns with a Higher-Risk Private Institution |

| New England | 57 | 19 | 10 |

| Connecticut | 6 | 1 | 0 |

| Maine | 19 | 6 | 1 |

| Massachusetts | 10 | 5 | 3 |

| New Hampshire | 7 | 3 | 2 |

| Rhode Island | 2 | 1 | 1 |

| Vermont | 13 | 3 | 3 |

| Source(s): Endowments and annual operating expenses come from IPEDS, National Center for Education Statistics, Finance Survey FY2018 data. Enrollments and higher education jobs data come from the IPEDS general survey, 2018. Total number of jobs in a city or town are from each state’s department of labor as part of its ES-202 programs. Note(s): Heavily dependent cities and towns are defined as those for which at least 10 percent of jobs come directly from colleges and universities, or those where the number of enrolled students (excluding online-only students) equates to a student-to-population ratio of 0.2. Higher-risk institutions are defined as those with a declining enrollment between 2008 and 2018 and an endowment valued at less than half of their annual operating expenses. Of the heavily dependent cities and towns with a higher-risk institution, one community in Vermont and two in Massachusetts are home to multiple institutions, including schools that do not meet the threshold for being financially vulnerable. Therefore, not all higher education related economic activity in those communities would be threatened with the closure of the vulnerable schools. |

|||

Financially vulnerable colleges and universities include two-year, four-year, public, and private institutions. Of the 71 colleges and universities that meet our criteria for financial vulnerability, 18 are private and 53 are public. However, of the 19 at-risk schools in heavily dependent towns, 10 are private and 9 are public.

Maine is an outlier among the New England states in that of the six financially vulnerable institutions in heavily dependent municipalities, five are public and only one is private. The possible policy responses differ when considering the options of a public school versus those of a private school. In particular, state appropriations can become a key factor in the long-term viability of a public institution.

School responses and concerns heading into fall

This past spring semester, colleges and universities across the region rose to the challenge of quickly moving students off campus and setting up online courses in a matter of weeks. Summer courses have similarly been moved to distance-education models, but the status of an on-campus fall semester remains unclear.

The CARES Act authorized more than $14 billion in emergency relief for institutions of higher education to respond to the pandemic. At least 50 percent of the funds that a school receives must be used for emergency financial aid grants that help students cover such matriculation-related expenses as food, housing, course materials, technology, health care, and childcare. Remaining funds may be used to address shortfalls from room and board reimbursements and other lost revenues.20 By late April, the financial costs of the pandemic to colleges and universities at the national level had surpassed the CARES Act appropriations.

As they weigh their options for the fall semester, school officials must consider that, because tuition payments are not due until the beginning of a semester, pushing back the start date for fall classes would be untenable if an institution could not afford to maintain operations without that money. The California State University system made a relatively quick decision about the fall semester, announcing on May 12 that classes will be conducted primarily online. Advocates of in-person classes claim that testing, tracing, and separating students are essential elements to any opening plans. They concede that opening campuses and then sending students home if there is another outbreak would not be feasible, and allowing normal dormitory living, crowded lecture halls, and large social gatherings would be irresponsible, and likely prohibited in many states. Also, testing only those students, faculty, and staff with symptoms would not be sufficient. Regular testing of all students and employees is the only way to prevent the disease from being spread by those who are asymptomatic.

Changes will be necessary, and many of the possible requirements for reopening safely would involve additional expenses. In addition to universal testing, these requirement could include renting hotel space to reduce the number of students living in campus dorms. The well-being of the students is the priority for school officials, but some also note that local economies depend on these institutions.21

The total economic toll of the COVID-19 pandemic has yet to be determined, including how severely it will affect New England’s colleges and universities and the communities where they are located. The potential for long-term disruptions to higher education remains a concern, and the question of how to resume normal operations safely and successfully has not yet been answered. As of late May, roughly two-thirds of the schools that had released fall 2020 plans indicated that their campuses will be open.22 In the absence of a COVID-19 vaccine, life in college towns across New England and the country will be different, but just how different remains unclear.

Data Sources

This report uses the Integrated Postsecondary Education Data System (IPEDS), Quarterly Workforce Indicators (QWI) data from the Census Bureau, county subdivision population data from the Census Bureau, and data on city and town employment from each New England state’s departments of labor.

IPEDS data are submitted at the aggregate level from postsecondary institutions and do not have student-level information. IPEDS is administered by the National Center for Education Statistics (NCES). The submission of data to IPEDS is mandatory for any institution that participates in or is an applicant for participation in any federal financial assistance program authorized by Title IV of the Higher Education Act. The mandatory submission consequently results in a nearly 100 percent response rate for each IPEDS survey component.

QWI provides local labor market statistics by industry, worker demographics, and employer characteristics. The source data for the QWI are the Longitudinal Employer-Household Dynamics (LEHD) linked employer-employee microdata. The LEHD is a massive longitudinal database covering more than 95 percent of US private sector jobs. QWI data are available each quarter from 1995 for Rhode Island, from 1996 for Connecticut and Maine, from 2000 for Vermont, from 2003 for New Hampshire, and from 2010 for Massachusetts.

Endnotes

- “There will probably be some institutions that will not survive. It's an existential threat. Smaller colleges that are tuition-driven, they have little or no endowment, if they lost 15 to 20 percent of their class, that is a huge budget crisis," said Steven Bloom, the director of government relations at the American Council on Education, in an interview with ABC News. See Catherine Thorbecke, “Why Coronavirus-battered Universities May Not Be Able to Use Their Endowments,” ABC News, April 25, 2020. https://abcnews.go.com/US/coronavirus-battered-universities-endowments/story?id=70305591

- See Hillary Burns, “UMass to Lose $70M in Revenue to Student Refunds,” Boston Business Journal, March 27, 2020. https://www.bizjournals.com/boston/news/2020/03/27/umass-to-lose-70m-in-revenue-to-student-refunds.html

- See Michael T. Nietzel, “College Furloughs Have Begun,” Forbes, April 19, 2020. https://www.forbes.com/sites/michaeltnietzel/2020/04/19/college-furloughs-have-begun/#3fd5c0a623cd

- See Joey Hadden, “What the Top 25 Colleges and Universities in the US Have Said about Their Plans to Reopen in Fall 2020, from Postponing the Semester to Offering More Remote Coursework,” Business Insider, May 13, 2020. https://www.businessinsider.com/how-major-us-colleges-plan-reopen-for-fall-2020-semester-2020-5#tufts-university-1

- See Susan Svrugla, “With Colleges Shuttered, More Students Consider Gap Year. But Those May Be Disrupted, Too,” Washington Post, May 13, 2020. https://www.washingtonpost.com/education/2020/05/13/gap-years-college-covid/

- See “Higher Education Community Requests $46.6 Billion for Students and Institutions in Fourth Supplemental Package, Proposes Tax Changes,” American Council on Education, April 10, 2020. https://www.acenet.edu/News-Room/Pages/Higher-Education-Community-Requests-$47-Billion-for-Students-and-Institutions-Proposes-Tax-Changes.aspx

- See Andrew DePietro, “Here’s a Look at the Impact of Coronavirus (COVID-19) on Colleges and Universities in the US,” Forbes, April 30, 2020, https://www.forbes.com/sites/andrewdepietro/2020/04/30/impact-coronavirus-covid-19-colleges-universities/#8aee6b61a681; and Douglas N. Harris, “How Will COVID-19 Change Our Schools in the Long Run?” Brown Center Chalkboard blog, Brookings Institute, April 24, 2020. https://www.brookings.edu/blog/brown-center-chalkboard/2020/04/24/how-will-covid-19-change-our-schools-in-the-long-run/

- See Emma Pettit, “Faculty Cuts Begin, with Warnings of More to Come,” Chronicle of Higher Education, May 15, 2020. https://www.chronicle.com/article/Faculty-Cuts-Begin-With/248795

- The reason that students are represented here as a ratio to population instead of as a share is that we don’t know whether the students are included as part of the local population. In some instances, students are living in dormitories and return to their homes when the academic year is not in session. In other cases, students, such as those attending community college, live year-round in the city or town where the school is located and are part of the population.

- A college or university’s economic impact can span many categories beyond direct employment, including the purchasing of local goods and services; institutional donations to the community; and staff, student, and visitor spending. After direct expenses have been determined, the indirect effect that an institution has on the local economy is determined by applying an expenditure multiplier. Expenditure multipliers in 19 studies range from 1.34 to 2.54, with a median of 1.7 of spending for every $1 spending by the university. Many of these studies also incorporate a jobs multiplier to estimate the number of jobs created outside of the university or college in response to an institution’s expenditures. These studies have wide ranges, and it is clear that not all institutions affect each local economy in the same way, but it is also clear that job and spending benefits extend beyond the campus to local economies. Source: Siegfried, John J., Allen R. Sanderson, and Peter McHenry. 2007. “The Economic Impact of Colleges and Universities.” Economics of Education Review 26(5): 542–558. https://doi.org/10.1016/j.econedurev.2006.07.010

- For examples of predictions about the future of higher education, see Jon Marcus, “Will the Coronavirus Forever Alter the College Experience,” New York Times, April 23, 2020, https://www.nytimes.com/2020/04/23/education/learning/coronavirus-online-education-college.html; Jeffrey Aaron Snyder, “Higher Education in the Age of Coronavirus,” The Boston Review, April 30, 2020, http://bostonreview.net/forum/jeffrey-aaron-snyder-higher-education-age-coronavirus; and James D. Walsh, “The Coming Disruption,” New York Magazine, May 11, 2020, https://nymag.com/intelligencer/2020/05/scott-galloway-future-of-college.html; among others.

- For example, the number of all-institution closures during the last five years (2014–15 through 2018–19) was more than six times higher than during the previous five years (2009–10 through 2013–14). The number of closures decreased for public institutions, while it rose from 26 to 80 for private nonprofit institutions, and from 56 to 473 for private for-profit institutions (two-year and four-year). Source: NCES IPEDS Digest Table 317.50. Degree-granting postsecondary institutions that have closed their doors, by control and level of institution: 1969–70 through 2018–19.

- See Hilary Burns, “Small Colleges 'Could Be the Lehman Brothers of this Recession,' Says Economist,” Boston Business Journal, April 9, 2020. https://www.bizjournals.com/boston/news/2020/04/09/small-colleges-could-be-the-lehman-brothers-of.html

- See Deirdre Fernandes, “Amid Pandemic, a Growing List of Colleges in Financial Peril,” Boston Globe, May 8, 2020. https://www.bostonglobe.com/2020/05/08/metro/amid-pandemic-growing-list-colleges-financial-peril/

- Massachusetts Attorney General Maura Healey's office has received an increasing number of inquiries from colleges about tapping into restricted pools of money in their endowments. The office issued guidance in late April about when and how institutions can access money that has been set aside for specific uses, such as scholarships. See Deirdre Fernandes, “Amid Pandemic, a Growing List of Colleges in Financial Peril,” Boston Globe, May 8, 2020. https://www.bostonglobe.com/2020/05/08/metro/amid-pandemic-growing-list-colleges-financial-peril/

- See Bo Zhao, “Forecasting the New England States’ Tax Revenues in the Time of the COVID-19 Pandemic,” Current Policy Perspectives, Federal Reserve Bank of Boston Research Department, forthcoming. https://www.bostonfed.org/publications/current-policy-perspectives.aspx

- See Hilary Burns, “Small Colleges ‘Could Be the Lehman Brothers of this Recession,’ Says Economist,” Boston Business Journal, April 9, 2020. https://www.bizjournals.com/boston/news/2020/04/09/small-colleges-could-be-the-lehman-brothers-of.html

- See Austin Danforth, “Vermont State College Board Announces Delay Campus Closure Vote,” Burlington Free Press, April 19, 2020. https://www.burlingtonfreepress.com/story/news/2020/04/19/coronavirus-vermont-state-college-campus-closure-vote/5162033002/

- Students from foreign countries who attend schools across New England could be particularly sensitive to the lack of clarity surrounding the fall semester. In some cases, international travel currently has added restrictions, and while returning home during a second wave of an outbreak would be inconvenient and costly for all students, these issues would be exacerbated for students who are farther from home and could affect their enrollment decisions. At 20 of the 71 institutions that meet the higher-risk endowment and enrollment criteria, at least 5 percent of the students are international. At a time when domestic enrollment is likely to decline, a sharp decline in the number of foreign students would worsen the financial footing of colleges and universities and the communities where they are located.

- See “COVID-19 Stimulus Bill: What It Means for States,” National Conference of State Legislators, April 2, 2020. https://www.ncsl.org/ncsl-in-dc/publications-and-resources/coronavirus-stimulus-bill-states.aspx

- See Christina Paxson, “College Campus Must Reopen in the Fall. Here’s How We Do It,” The New York Times, April 26, 2020. https://www.nytimes.com/2020/04/26/opinion/coronavirus-colleges-universities.html

- See “Here’s a List of Colleges’ Plans for Reopening in the Fall,” Chronicle of Higher Education, May 21, 2020. https://www.chronicle.com/article/Here-s-a-List-of-Colleges-/248626

About the Authors

About the Authors

Riley Sullivan,

Federal Reserve Bank of Boston

Riley Sullivan is a senior policy analyst with the New England Public Policy Center in the Federal Reserve Bank of Boston Research Department.

Email: riley.sullivan@bos.frb.org

Acknowledgments

The author thanks Morgan Klaeser for her excellent research assistance and Katharine Bradbury and Jeffrey Thompson for their guidance in producing this brief.

Resources

Site Topics

Keywords

- COVID-19 ,

- Higher Education ,

- economy ,

- New England ,

- NEPPC ,

- college