Impact of the COVID-19 Pandemic on New England Homeowners and Renters

| Key Facts | |

| More than 1 million NE households are at risk of missing their rent or mortgage payment due to coronavirus-related job loss. | |

| The CARES Act could prevent 694,400 to 836,200 NE households from missing monthly housing payments. | |

| Under the best-case scenario, $1.42 billion in lost housing payments is likely to accrue in NE from April through July 2020. | |

|

|

Summary

Job losses and likely layoffs related to the COVID-19 pandemic will put many New England residents at risk of not being able to pay their mortgage or rent and needing financial assistance and state-government safeguards to remain in their homes. Economic interventions from Congress, primarily through the federal CARES Act, include direct payments to households and increased unemployment insurance benefits that are expected to provide vital support to many of these households for the next three to four months. Even with these efforts, 2 to 3 percent of New England homeowners and 9 to 13 percent of New England renters may be unable to make their housing payments. Many states have temporarily halted evictions, foreclosures, or both to protect people from losing their homes, at least in the short term. However, once the economy begins to recover, these households will remain responsible for their unpaid rents and mortgages. This report’s findings represent the immediate, three- to four-month impact that the coronavirus outbreak and resulting legislation are likely having on New England households. The ultimate economic consequences of the pandemic, along with the adequacy of economic-policy responses, will be determined largely by how long it takes to stop the spread of the virus.

Sign up for new research and data on the New England economy.

More than one-third of New England households at high risk of layoff due to the pandemic

Homeowners are more insulated than renters from losing their housing as a result of job loss, because compared with renters, a smaller share of this group has a monthly housing payment.1 Table 1 shows the share of homeowner and renter households that have either a monthly mortgage or rent payment.2 In New England as a whole, 66 percent of homeowners and 96 percent of renters have these monthly housing costs. Across the region, the share of homeowners with housing costs ranges from a low of 60 percent in Maine to almost 70 percent in Rhode Island, whereas in any New England state, at least 94 percent of renter households pay rent every month.

Table 1: High-Risk Employment among Homeowners and Renters

New England states and United States

| Share of all homeowners | Share of all renters | |||||

| With a monthly mortgage payment | With at least 1 employed person in high-risk occupation | With all employed persons in high-risk occupations | With a monthly rent payment |

With at least 1 employed person in high-risk occupation | With all employed persons in high-risk occupations | |

| United States | 62 | 35 | 16 | 95 | 40 | 25 |

| New England Region | 66 | 35 | 15 | 96 | 36 | 22 |

| Connecticut | 66 | 34 | 14 | 96 | 38 | 26 |

| Maine | 60 | 37 | 17 | 94 | 34 | 23 |

| Massachusetts | 68 | 33 | 13 | 97 | 34 | 20 |

| New Hampshire | 64 | 39 | 16 | 97 | 40 | 26 |

| Rhode Island | 69 | 36 | 16 | 97 | 33 | 23 |

| Vermont | 63 | 36 | 17 | 94 | 43 | 26 |

| Note(s): Households with housing costs include only homeowners with a first or second mortgage and renters paying cash rent. Workers are at high risk of unemployment if their job is nonessential, cannot be done from home, and is paid hourly. The definition used here is based on one used in Gascon (2020), with adjustments made to essential occupations that better match Massachusetts’s state-level policy.

Source(s): 2018 American Community Survey one-year estimates |

||||||

To determine the impact that pandemic-related job losses could have on households, this report identifies occupations that are at high risk for layoff or furlough under public shutdown orders. Workers employed in occupations that are determined to be nonessential, cannot be done at home, and are paid hourly are defined as at high risk for unemployment.3 According to American Community Survey (ACS) data, some 35 percent of all homeowners and approximately 36 percent of all renters in New England had at least one person in their household who was employed in a job that was at high risk for unemployment under this definition.4 The high-risk job definition represents a worst-case scenario for unemployment in that not all high-risk workers will actually be laid off. Some employers will continue operating under a reduced capacity, others will reduce hours or wages to preserve their workers’ positions, and still others will receive federal loans requiring that employees be kept on the payroll.5 The total number of workers actually laid off in the region, however, is approaching the numbers of high-risk workers used in this analysis.6 For the weeks ending March 21, 2020, through May 9, 2020, the total number of people in New England who filed initial unemployment insurance claims was 61 percent of the total number employed in high-risk jobs in the region.7

In New England as a whole, 35 percent of all homeowners and 36 percent of all renters had at least one person employed in a high-risk occupation. Among the region’s six states, the largest difference between the two groups was in Vermont, where about 43 percent of all renters had someone in their household employed in a high-risk job, compared with about 36 percent of homeowners. Thus, for most of New England, and nationally, homeowners and renters are exposed to coronavirus-related job losses at roughly the same rate. In renter households, however, it is more likely that all the wage earners are employed in high-risk jobs, and so these households are more likely to rely entirely on earnings from such occupations. In more than 20 percent of renter households and 15 percent of homeowner households in New England, all the working members were employed in jobs at high risk for layoff or furlough.

Some households will continue to make ends meet even if a household member loses a job, because they include multiple working adults or have non-earnings sources of income.8 On average, a homeowner household includes slightly more wage-earning adults compared with a renter household.9 Homeowners are also more likely to have other financial resources available to them. In New England, 60 percent of homeowners and 48 percent of renters had non-earnings income, which averaged about $41,100 and $20,000 per year, respectively.10 Renter households also tend to have lower incomes in general compared with homeowners, and they can expect to lose a larger share of their income due to layoffs.11 In New England, about 20 percent of total household income for homeowners was earned in high-risk jobs, compared with 25 percent for renters. Among households in which all working members were employed in high-risk occupations, 77 percent of total homeowner household income was at risk of loss, compared with 87 percent of total renter household income.12

More than 1 million households in New England at risk of missing housing payments

Households are likely to miss their mortgage or rent payments if they do not have enough monthly income to pay for both their housing and other necessities. This report includes food costs in addition to monthly housing costs to assess whether a household likely will be able to meet their monthly housing payment. Other necessary expenses certainly factor into a household’s ability to make ends meet; these include utilities, health insurance, and debt payments. However, for the purposes of this report’s analysis, only food costs are included. This report also does not consider whether households have savings they could use to cover monthly housing payments. Most households, especially renters, do not have adequate savings to cover their housing costs in the event of job loss.13 The length of time that people in high-risk jobs may be unemployed also plays a role in determining how many housing payments they may miss. Households whose monthly income after job loss is less than their monthly housing costs plus a monthly low-cost food budget are likely unable to afford to both feed their families and pay for housing.14

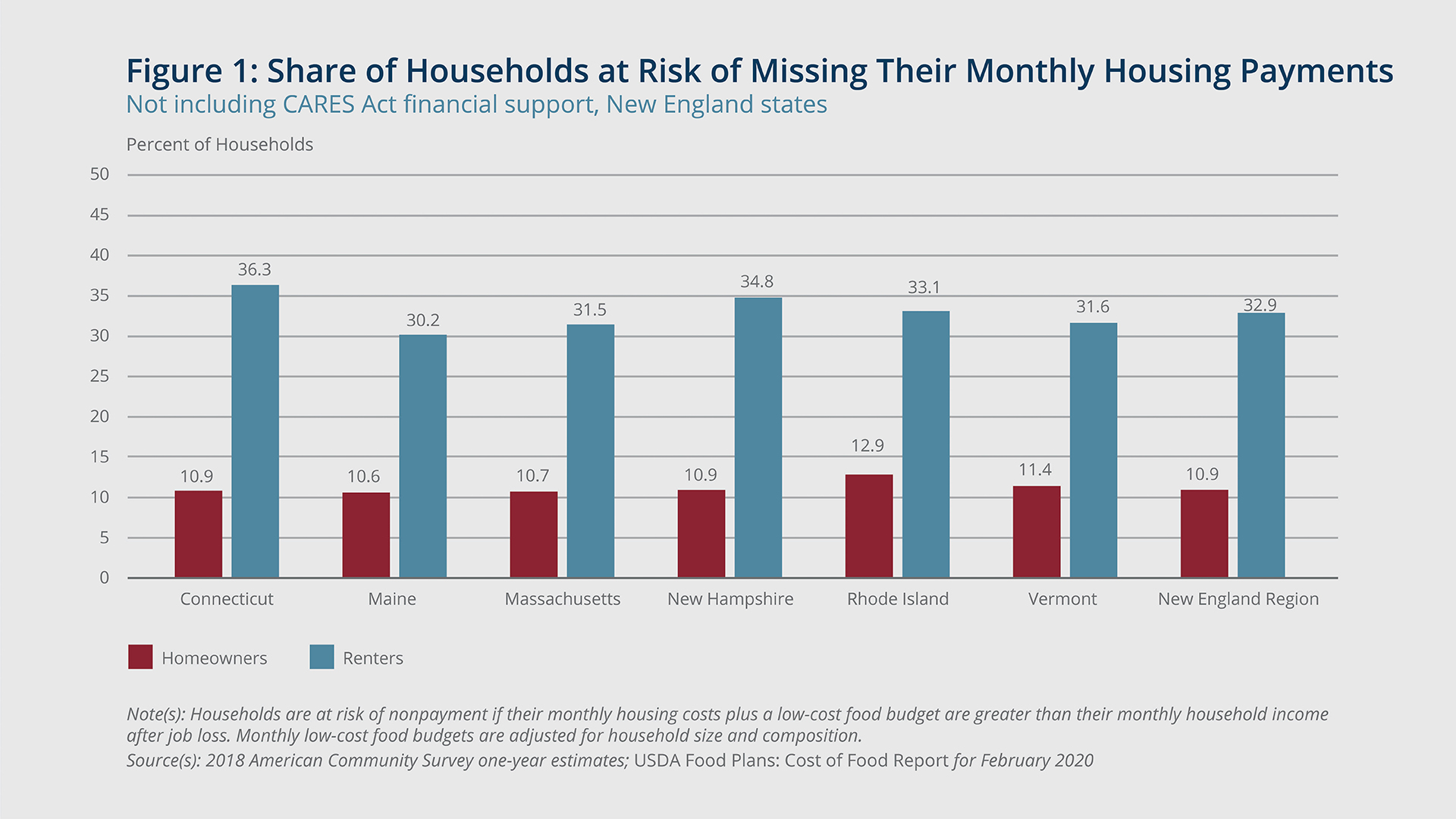

Figure 1 shows the share of all households who could not afford their monthly rent or mortgage payments if all members working in high-risk jobs became unemployed, based on their monthly housing and food costs. About 11 percent of New England homeowners and 33 percent of New England renters would be unable to afford their housing costs, according to this measure. Across the New England states and nationally, renters would be more likely than homeowners to miss their monthly housing payments due to job loss.15 The share of homeowners at risk of missing housing payments would reach almost 13 percent in Rhode Island, while the share of renters who would be at risk ranges from a low of 30 percent in Maine to just over 36 percent in Connecticut.

{kind=link}

Meghan Smith/Federal Reserve Bank of Boston

Compared with renters, a much smaller share of homeowners in New England would likely miss making housing payments, but the total number of each type of household that would be at risk is comparable in most of the region’s states. As Table 2 shows, in Maine and Vermont nearly as many homeowner households as renter households would be at risk of nonpayment. In Maine, about 48,900 renter households would be at risk of missing their monthly housing payment, which equates to about 30 percent of the state’s renter households. The 11 percent of the state’s homeowners who would be at risk equals about 43,300 households. Approximately 23,500 renter households and 21,300 homeowner households would be at risk in Vermont, and in New Hampshire, about 53,800 renters and 41,100 homeowners would be at risk. In southern New England (Connecticut, Massachusetts, and Rhode Island), where there is a greater share of renter households compared with northern New England, the total number of renter households at risk of nonpayment would likely be higher than the number of at-risk homeowner households. Across all of New England, more than 1 million households would be at risk of missing their monthly rent or mortgage payments. About two-thirds of these households are renters, and the rest are homeowners.

Table 2: Total Number of Households at Risk of Missing Housing Payments

Not including CARES Act financial support, New England states

| Homeowners | Renters | |

| New England Region | 410,800 | 664,143 |

| Connecticut | 98,603 | 170,594 |

| Maine | 43,364 | 48,968 |

| Massachusetts | 173,985 | 315,814 |

| New Hampshire | 41,173 | 53,846 |

| Rhode Island | 32,324 | 51,360 |

| Vermont | 21,351 | 23,561 |

| Note(s): Households are at risk of nonpayment if their monthly housing costs plus a low-cost food budget are greater than their monthly household income after job loss. Monthly low-cost food budgets are adjusted for household size and composition.

Source(s): 2018 American Community Survey one-year estimates; USDA Food Plans: Cost of Food Report for February 2020 |

||

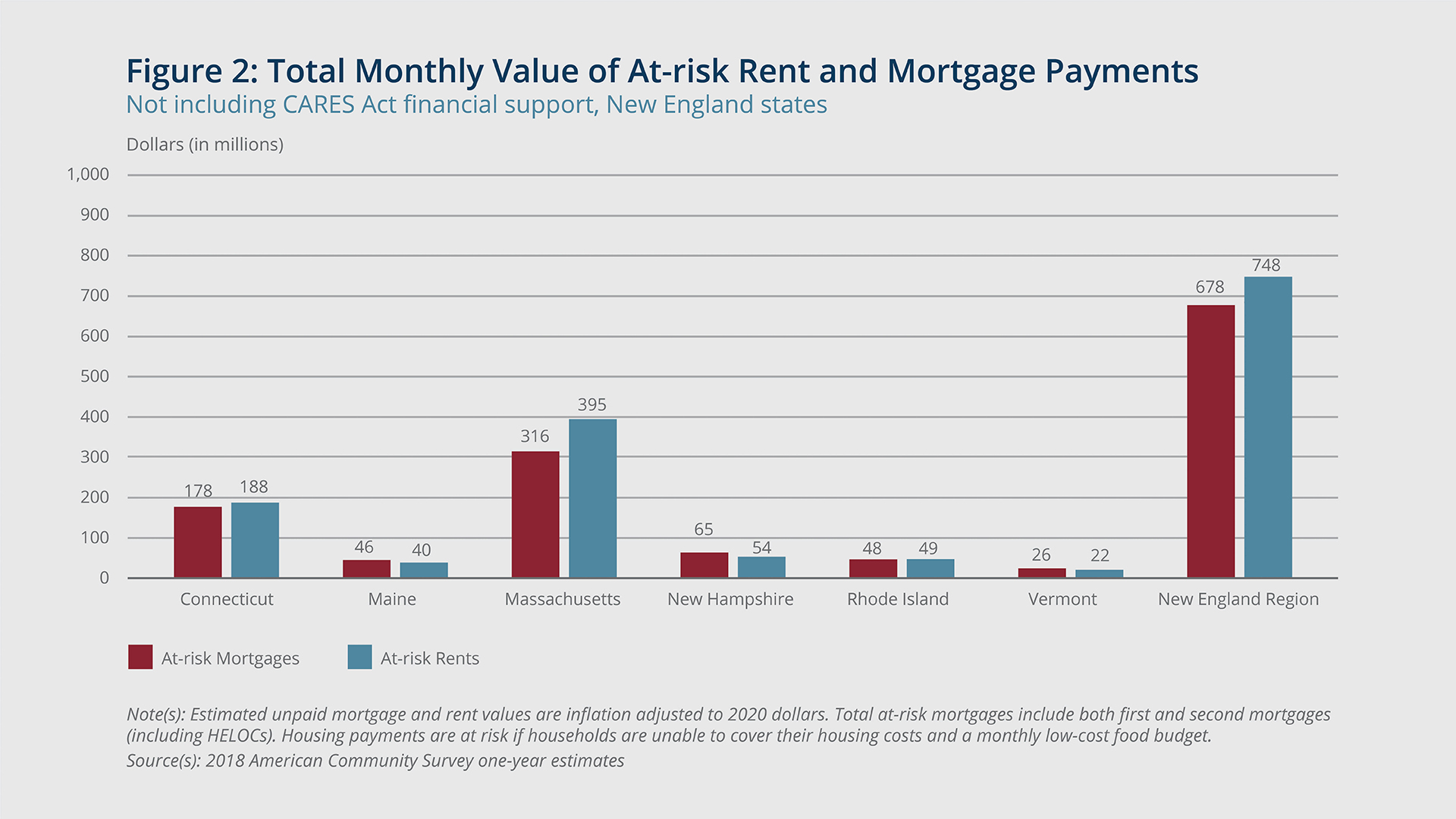

Although fewer homeowners than renters would be at risk of not making housing payments, their housing costs are higher, and so the total value of at-risk mortgage payments in New England would be comparable to that of at-risk rent payments.16 Figure 2 shows the total monthly value of potentially missed payments for renters and homeowners in New England. A total of about $1.43 billion in rents and mortgages would be at risk of nonpayment every month in New England due to coronavirus-related job losses.17 Just over half of this sum would be missed rent payments; the remainder would be missed mortgage payments.18 In Maine, New Hampshire, and Vermont the total value of missed mortgage payments would be greater than that of missed rent payments. The two values would be about equal in Rhode Island. In Massachusetts and Connecticut, missed rents would outpace missed mortgage payments. About $395 million per month in rents would be at risk of nonpayment in Massachusetts, compared with $316 million in monthly mortgages. Connecticut’s missed rents would be about $188 million per month, and missed mortgages would total $178 million per month. While homeowners comprise a smaller share of at-risk households overall, missed mortgage payments would have an outsized impact on the local economy in states where these payments rival or even outstrip those from renter households.

{kind=link}

Meghan Smith/Federal Reserve Bank of Boston

The magnitude of these missed housing payments, which translate into missed income for rental-property owners and mortgage lenders, has the potential to escalate what is an immediate crisis in household finances into a broader problem for the housing market in New England. Rental-property owners who depend on income from tenants would be at risk of missing their own mortgage payments. The combination of those losses and as much as $678 million in missed mortgage payments from homeowner households in New England could create a burden on local housing markets. While current state- and local-level policies help prevent immediate evictions and foreclosures, and in some cases they help pay housing costs, they do not cover the value of missed housing payments that likely would accrue.

Due to the CARES Act, far fewer New England households at risk of missing housing payments

In response to the economic consequences of the pandemic, New England state governments have instituted moratoriums on evictions 19 and provided rental rebates to households who cannot make payments.20 One state, Massachusetts, passed legislation that halts both evictions and foreclosures for the duration of the public health emergency.21 These policies almost certainly safeguard the ability of residents to remain in their homes in the short term, but they do not address the longer-term prospect of many households exiting this crisis with overdue housing payments. However, the federal CARES Act passed in late March 2020 is likely to greatly reduce the total value of outstanding rent and mortgage payments that accrues over the next three to four months, although it will not cover the missed payments entirely, and it is not guaranteed to remain in effect for the longer term. In addition, the total amount of missing housing payments will largely depend on how long the pandemic and resulting business closures last.

The CARES Act provides households with a one-time direct payment of as much as $1,200 per eligible adult and $500 per eligible child, depending on the adult’s adjusted gross income. 22 In addition, the CARES Act extends unemployment insurance (UI) for workers who are currently unemployed and for those laid off at a later date to 39 weeks, and it provides an additional $600 per week on top of any state UI benefit.23 Also, eligibility for benefits has been expanded to include contract and gig workers, who typically are not covered by UI, and those who are ineligible for state UI benefits due to low earnings. This report provides monthly estimates that are likely to persist for three months, until late July 2020, at which point the additional UI benefits will expire.24 Should current economic conditions continue beyond that point, the number of at-risk households (and the value of missed housing payments) will likely increase if no other financial intervention is in place.

To estimate the CARES Act’s impact on New England, this report first assumes those working in high-risk jobs are unemployed and then adds a household’s total direct payments and UI benefits to their estimated household income.25 The total UI benefits received by households are estimated based on each New England state’s UI policies and whether a person is unemployed or currently employed in a high-risk job.26 As in the previous section, this analysis does not account for any savings households might tap to cover their housing costs.

Not everyone who is eligible for UI will apply, nor will all eligible households receive their direct payments promptly. This report presents findings based on two different scenarios to provide a range of what the likely impact of the CARES Act will be in New England.27 The first scenario is based on 95 percent of eligible unemployed workers applying for and receiving their UI benefits. In this scenario, essentially everyone who is eligible for UI applies for and receives the benefits. Nationally, this has not been the case even during periods of severe economic downturn and unemployment.28 The second scenario assumes 75 percent of eligible unemployed workers will claim their UI benefits. This participation rate is also higher than estimates for previous downturns, but it takes into account that, because the total value of the UI benefits is greater today than in the past, the incentive to apply and receive them is also greater. Finally, both scenarios assume that 80 percent of households are signed up for direct deposit and therefore receive their direct payments promptly.29 For filers without direct deposit, the wait may be several months; therefore, in its analysis of the impact of the CARES Act, this report assumes these households do not receive the checks.30

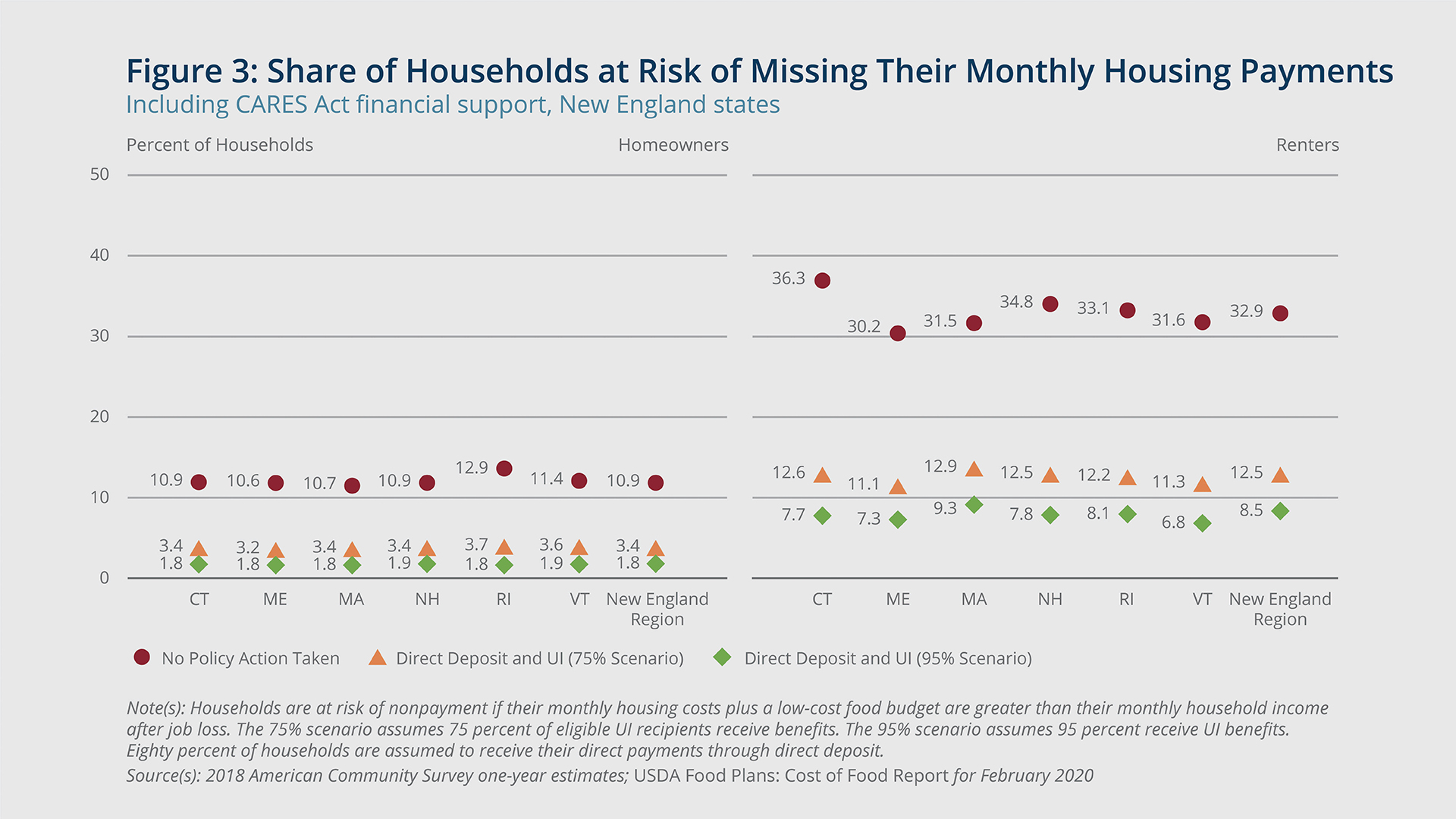

The expanded UI benefits and direct payments to households provided by the CARES Act are likely to improve households’ ability to meet their monthly housing payments.31 It could prevent 694,400 to 836,200 households in New England from missing payments. Figure 3 shows the impact of the CARES Act on the share of households in the region that would be at risk of nonpayment. After UI benefits and direct payments are taken into account, far fewer households are at risk of missing either monthly mortgage or rent payments. Under the more modest scenario where 75 percent of UI-eligible workers apply for benefits, about 3 percent of homeowners and 13 percent of renters are at risk of nonpayment. Under the best-case scenario of 95 percent participation, 2 percent of homeowners and 9 percent of renters remain at risk.32 With no policy intervention, 11 percent of homeowners and 33 percent of renters would be at risk of missing monthly housing payments.

{kind=link}

Meghan Smith/Federal Reserve Bank of Boston

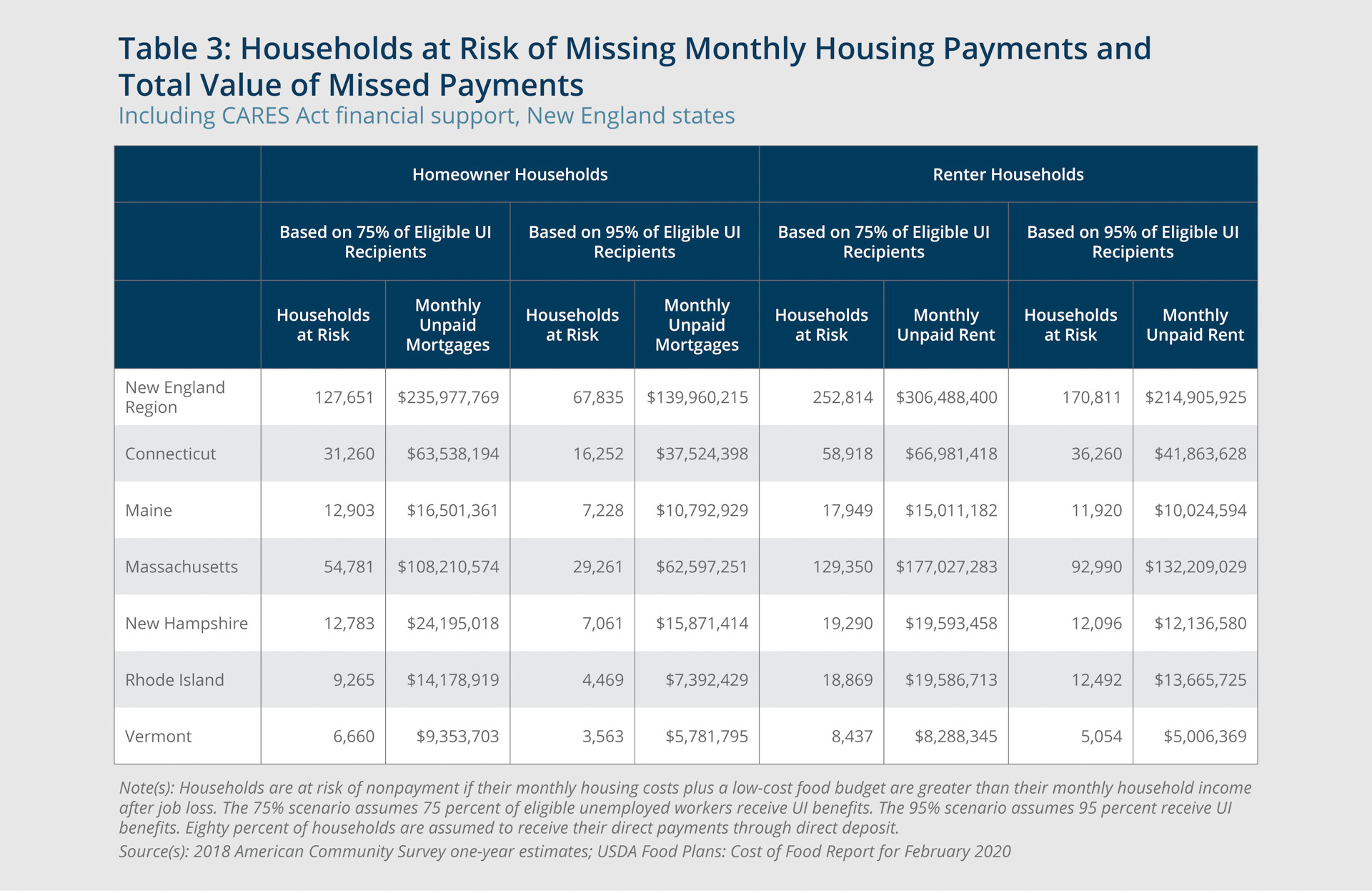

The beneficial effects of the CARES Act are likely to be stronger for homeowners than for renters. Even though more renter households would be at risk of nonpayment, a smaller share would see their situation improve as a result of added UI benefits and direct payments. Renter households have lower incomes, on average, compared with homeowners, and so the financial gap between housing costs and income after job loss is wider. Table 3 shows the number of homeowner and renter households that would remain at risk under the two scenarios used in this report. Across New England, 69 to 83 percent fewer homeowners and 62 to 74 percent fewer renters would be at risk of missing their housing payments as a result of the CARES Act.33 Based on the best-case scenario, in which 95 percent of those eligible for UI receive benefits, 67,800 homeowners and 170,800 renters in New England would still be at risk of nonpayment of housing costs, but in the absence of any intervention, more than 800,000 additional households potentially would be at risk. Under the 75 percent scenario, about 127,600 homeowners and 252,800 renters would be at risk of missing their monthly housing payments.

{kind=link}

Alex Cronin/Federal Reserve Bank of Boston

The impact of the CARES Act is not likely to be even across New England due to differences in the cost of housing, incomes, and existing state UI policies. Under the 95 percent scenario, the number of at-risk households in the region could fall 77 percent after the CARES Act benefits have been received. However, Massachusetts would see a smaller reduction, of 75 percent, while the other New England states would experience 79 to 81 percent reductions in the number of at-risk households. The CARES Act’s additional federal UI benefit does not account for local differences in cost of living, such as housing, which would result in higher-cost areas seeing less of an impact. In 2018, Massachusetts’s median monthly housing costs were 8 percent higher than those of Connecticut, the next costliest state in New England, and they were 65 percent higher than in Maine, the state with the lowest median housing costs.34 Housing costs are not the only factor, however, as Connecticut’s median housing costs are also substantially higher than those of other states in the region; the structure of each state’s UI program is also likely to play a role. In Massachusetts, the average UI benefit before the CARES Act replaced a smaller share of the state’s average wage compared with the average UI benefit in every other New England state except New Hampshire.35 Also in Massachusetts, the additional $600 per week from the CARES Act results in the smallest increase in the share of the average wage replaced with UI.

A decrease in the number of at-risk households reduces the total value of rents and mortgages that are at risk of not being paid. Whereas without any financial assistance to households, missed mortgage and rent payments could total more than $1.43 billion per month across New England, under the moderate 75 percent scenario, the value of missed payments would drop to $542 million per month, as shown in Table 3. Under the best-case, 95 percent scenario, the value of missed payments would be $355 million per month. These decreases are substantial, however, the value of missed payments is a monthly estimate that would accrue if widespread unemployment persists. Given that the additional $600 federal UI benefit expires at the end of July 2020, under the best-case scenario, a total of $1.42 billion in lost housing payments is likely to accrue in New England from April 2020 through July 2020. After July, without further intervention, and if current economic conditions persist, missed housing payments will accrue faster every month. State and local interventions likely have helped to reduce the number of missed payments, but the real impact to households has come from federally provided benefits.

Conclusion

Restricting broad swaths of economic activity is the public health action required to prevent further spread of COVID-19, but the restrictions have additional consequences that are important to recognize. The resulting hits to employment and household finances are likewise far reaching. This report estimates that without any intervention, 11 percent of all homeowners and 33 percent of all renters in New England would be at risk of falling behind on their monthly housing payments. Without any policy intervention, the total value of these missed payments could reach upwards of $1.43 billion per month in the region, which would have a profound impact on the broader housing market due to the effect on property owners and lenders.

Intervention in the form of the federal CARES Act has provided households with direct payments and expanded UI benefits for the unemployed. The effect of these measures is substantial. This report estimates that 694,400 to 836,200 fewer households in New England—homeowners and renters combined—may be at risk of missing their rent or mortgage payments as a result of the CARES Act. However, 9 to 13 percent of renters and 2 to 3 percent of homeowners are likely still at risk of nonpayment. While this report has accounted for some of the delay in households receiving direct payments, it does not take into account the myriad issues and delays New England states are experiencing with issuing UI benefits. These delays likely prevented many households from receiving support during their first month of unemployment. The CARES Acts benefits include an additional $600 weekly unemployment payment that will end by mid-summer. If economic conditions have not improved by then, more intervention may be required.

The federal policy response has likely averted an immediate financial disaster for households. The state-level responses have helped guarantee that those who fall through the cracks can remain in their homes, at least in the short term. Every New England state has responded with a moratorium on evictions; Connecticut, in partnership with local credit unions, has instituted broad forbearance programs for homeowners. Additional interventions, such as those from Maine’s state housing agency, provide direct payments to households that are behind on rent. All these policies help keep families in their homes. However, these measures do not prevent households from continuing to miss housing payments entirely. Even under a best-case scenario, the total value of these missed payments could rise higher than $355 million per month. If these payments continue to accrue, they could reach more than $1.42 billion by the time federal benefits expire. Addressing these secondary impacts of the pandemic crisis could become more important as the immediate effects are resolved. The missed mortgage and rent payments that will likely accrue have the potential to create a burden on the broader housing market.

Data Sources

2018 American Community Survey one-year estimates provided by Steven Ruggles, Sarah Flood, Ronald Goeken, Josiah Grover, Erin Meyer, Jose Pacas, and Matthew Sobek. IPUMS USA: Version 10.0 (data set). Minneapolis, MN: IPUMS, 2020. https://doi.org/10.18128/D010.V10.0

US Department of Agriculture’s USDA Food Plans: Cost of Food Report (monthly report)for February 2020

Internal Revenue Service’s (IRS) 2019 Filing Season Statistics: Cumulative statistics comparing 12/28/2018 and 12/27/2019

Endnotes

- References to homeowners and renters in this report refer to households, not individual people. For homeowners, housing payments include both first and second mortgages as well as home equity lines of credit (HELOCs). For renters, housing costs include their contract rent. Utilities are not included in either group’s housing costs estimates. Other large housing expenses such as property taxes are excluded from this analysis, although missing these payments can put a household’s housing at risk of loss if they are unpaid for a prolonged period of time.

- Nationally, 62 percent of all homeowners and 95 percent of all renters pay either mortgage or rent every month, according to 2018 American Community Survey (ACS) data. In this report, homeowners who have paid off their mortgage will not have any monthly housing payment. Renters may also not pay any cash rent if their housing is provided through their place of work, if they are in school and the university is providing housing outside of a dormitory setting, if it is provided by friends or family who do not charge rent, or if they are providing some other service in exchange for housing. This report excludes households living in group quarters, which generally includes those living in institutional housing settings such as prisons, dorms, or on military bases.

- Occupations at high risk of unemployment are those that are deemed nonessential, cannot be performed from home, and are paid hourly. The definition used here is based on one used in Gascon (2020), with adjustments made to essential occupations that better match Massachusetts’s state-level policy. To determine whether an occupation is essential, a random sample of 323 detailed Standard Occupation Classification (SOC) occupation codes (from a total of 808) was reviewed in relation to Massachusetts’s list of essential services. An occupation’s status was denoted as essential if the occupation reasonably fell under a Massachusetts-listed essential service. While essential businesses may differ from state to state, the relative size of Massachusetts’s labor market means that the state’s policy decisions will have the greatest impact on households in the region. Before these adjustments, 367 of the 808 occupation codes were at high risk of unemployment; these jobs employ 41 percent of workers in New England, based on 2018 ACS one-year estimates. After adjustment, 324 of the 808 SOC codes were high risk; these jobs employ 36 percent of workers in New England. For the original definition that this report is based on, see Charles Gascon, “COVID-19: Which Workers Face the Highest Unemployment Risk?” On the Economy Blog, March 24, 2020, Federal Reserve Bank of Saint Louis. St. Louis, MO.

- The 2018 ACS uses an occupation-coding system that is different from the one used in Gascon (2020). A crosswalk between the two coding systems was constructed. When an ACS occupation code had more than one risk classification (either high-risk or low-risk), the status with the largest share of employment within that ACS occupation code was used.

- The Paycheck Protection Program was established by the federal CARES Act, and provides small businesses with forgivable loans as long as 75 percent of the loan amount is used to pay employee salaries and wages.

- While recent initial unemployment insurance claims are heavily represented by workers in those occupations we have identified as being high-risk, they also include workers in occupations that are not considered high-risk in our analysis.

- Estimates are based on initial unemployment insurance claims from the Bureau of Labor Statistics for the weeks ending March 21, 2020, through May 9, 2020. Compared with the number of people employed in high-risk jobs in each state, 49 percent have applied for unemployment in Connecticut, 51 percent have applied in Maine, 67 percent in Massachusetts, 64 percent in New Hampshire, 76 percent in Rhode Island, and 48 percent in Vermont. These numbers do not include any additional new claims that were filed after May 9, 2020.

- Earned income includes only income from wages or businesses (including the self-employed). Non-earned income includes Social Security, welfare, retirement, investment income, and other sources.

- The average homeowner household in New England had 1.3 working adults, whereas the average renter household had 1.0 working adult, according to 2018 ACS one-year estimates.

- Estimates are in 2020 dollars, based on 2018 ACS one-year estimates, and include only households with positive non-earnings. Nationally, 60 percent of homeowners had some form of non-earnings income, compared with 40 percent of renters. Of those households with positive non-earnings income, homeowners had an average of about $40,600 annually, while renter households had about $19,400 annually.

- The median household income for homeowners was $78,800 nationally and $95,800 in New England. For renters, it was about $41,000 both nationally and in New England. Estimates are in 2020 dollars and based on 2018 ACS one-year estimates.

- This excludes households with negative household income. Nationally, 19 percent of homeowner household income was at risk of loss, while nearly 30 percent of renter household income was at risk. For US households with all employed persons in high-risk jobs, 81 percent of homeowner income was at risk, compared with 89 percent of renter household income.

- The presence of savings could help households make ends meeting during a layoff, but the ACS does not include data on savings or other types of financial or nonfinancial assets. Analysis of the Survey of Consumer Finances (SCF) indicates that the groups identified as most at risk in this analysis—those whose loss of earnings (proxied by working in a service or sales occupation) leaves their income below housing costs plus a moderate food budget—have very little savings in practice. Analysis of 2016 SCF data finds that renters at risk of not making their housing payments had median liquid wealth (savings and checking accounts, money market and call accounts, and pre-paid cards) of just $921, while at-risk homeowners had $3,200. Renters not at risk of missing their housing payments had median liquid wealth of $1,300, compared with $9,000 for homeowners not at risk.

- Households are unable to pay their monthly housing costs if those costs plus a low-cost food budget for their household are greater than their household income after subtracting wage and business income earned in high-risk occupations. A low-cost food budget was estimated for households based on their size and composition using the USDA Food Plans: Cost of Food Report for February 2020. Housing costs for homeowners include any first and second mortgages (including HELOCs). Only those households with a mortgage or cash rent are included. Housing costs for renters include only contract rent. Utilities, maintenance, and taxes are not included.

- In the United States, 11 percent of homeowners and 36 percent of renters were at risk of missing their monthly housing payments. This equates to about 24.5 million households nationally.

- The median homeowner household paid $1,536 per month in mortgage alone, compared with $1,003 per month in rent for the median renter household. Estimates are in 2020 dollars and based on 2018 ACS one-year estimates.

- Estimates are in 2020 dollars and based on 2018 ACS one-year estimates. Nationally, missed rent and mortgage payments could total about $27.9 billion per month; 57 percent of that amount would be missed rent payments, and the remainder would be missed mortgage payments.

- In this report, missed rent and mortgage payments are not equivalent to the amount of financial assistance that households would need to afford their housing costs. In most cases, the amount of assistance needed is less than a household’s total housing payment, as most have some income remaining even after job loss. For an analysis of the level of financial assistance Massachusetts households may need, see Philbrick, Sarah, Timothy Reardon, and Seleeke Flingai. 2020. The COVID-19 Layoff Household Gap. Metropolitan Area Planning Council. Boston, MA.

For an analysis of the level of financial assistance renter households may need nationally see Whitney Airgood-Obrycki, “How Much Assistance Would It Take to Help Renters Affected by COVID-10?” Housing Perspectives, April 28, 2020, Joint Center for Housing Studies of Harvard University. Cambridge, MA. - Every New England state has a moratorium on evictions; most were instituted by state housing courts. In the case of New Hampshire, the moratorium was instituted through executive order.

- Maine Housing, the state’s housing agency, is providing a one-time payment of $500 to renters who fall behind on their rent payments through the state’s COVID-19 Rental Relief Program.

- The Massachusetts Housing Security Bill (H 4647) stops all evictions and foreclosures until 45 days after the state of emergency ends, or 120 days from the date the law was passed, which was April 20, 2020.

- The CARES Act’s direct payments are administered through the Internal Revenue Service (IRS) as a tax refund and are based on either 2018 or 2019 tax returns, depending on the most recent filing.

- See Coronavirus Aid, Relief, and Economic Security (CARES) Act of 2020, II USC § 2102-2201.

- Under the CARES Act, the total number of weeks a person is eligible to receive UI was extended to 39 weeks. The additional $600 in federal benefits, however, are available only until July 31, 2020 (CARES Act 2020). Previously, states had their own policies regarding how many weeks a person could receive benefits; the duration typically was 26 weeks, but it ranged from 12 to 28 weeks depending on the state. See Center on Budget and Policy Priorities (CBPP). 2020. “How Many Weeks of Unemployment Compensation Are Available?” Washington, DC.

- The amount of the direct payment that a household receives is estimated using their adjusted gross income for 2018. TAXSIM Version 9, provided by the National Bureau of Economic Research, was used to estimate the adjusted gross income of households in 2018. Assumptions were made based on sub-family structure in the ACS to account for multiple tax filers within one household. Dependent filers are not eligible to receive the CARES Act direct payments (CARES Act 2020). See Feenberg, Daniel R., and Elizabeth Coutts. 1993. “An Introduction to the TAXSIM Model.” Journal of Policy Analysis and Management 12(1): 189–194.

- Persons eligible to receive UI are assumed to be those who are unemployed or employed in high-risk occupations, regardless of how many weeks they worked during the previous year. State UI income eligibility is based on income earned in the past year. If a household is ineligible to receive state UI, they could still receive the additional $600 in federal UI benefits. State level UI policies were retrieved from state labor department websites.

- This report does not account for the specific timing of UI benefits receipt, which can vary by state and has been delayed, especially in recent months, as states incorporate the new federal eligibility and benefits into their UI systems. Several news outlets have reported state-level delays in issuing UI benefits. Concerns over federal data collection requirements have delayed the issuance of UI benefits for some workers in Rhode Island. See Patrick Anderson, “Thousands of Unemployed Rhode Islanders Will Have to Wait a Little Longer,” Providence Journal, April 19, 2020. In Connecticut, Governor Lamont cited a delay of as long as five weeks in UI checks being received as a result of issues with the state’s UI processing system. See Alexander Soule, “Governor Cites Five-Week Delay for Unemployment,” Stamford Advocate, March 31, 2020.

- There are many reasons people who are eligible for UI do not apply including fear of retaliation by employers, lack of understanding about the process or confusion filling out paperwork, belief they will quickly find employment, or incorrectly assuming they are not covered by state unemployment insurance programs. During the depths of the Great Recession only about 50 percent of eligible unemployed workers claimed their UI benefits. It was not until several years after the end of the recession, while unemployment was still high, that the uptake in UI claims reached 95 percent of eligible unemployed workers. See Fuller, David L., B. Ravikumar, and Yuzhe Zhuang. 2012. “Unemployment Insurance: Payments, Overpayments and Unclaimed Benefits.” Regional Economist. Federal Reserve Bank of Saint Louis. St. Louis, MO.

- According to Internal Revenue Service data, roughly 80 percent of tax refunds are through direct deposit, as opposed to a paper check. See Internal Revenue Service. 2019. Filing Season Statistics for the Week Ending December 27, 2019. Washington, DC.

This report assumes that households spend only one-fourth of their direct payment per month over a period of four months to align with the length of time increased UI benefits will last and to account for households that budget these payments to meet multiple necessary expenses. Given state moratoriums on evictions and foreclosures, housing payments represent a less pressing expense relative to others, such as food and health care, and so additional income may be saved if future income is expected to be low. Evidence from past stimulus-payment programs indicates that half of recipients use the extra money to pay off outstanding debts, one-third save the additional money, and one-fifth spend it on new purchases. See Shapiro, Matthew, and Joel Slemrod. 2012. “Did the 2008 Tax Rebates Stimulate Spending?” American Economic Review 99(2): 374–379.

A recent survey by Gallup found that 35 percent of respondents plan to spend their direct payments on bills, and 16 percent plan to spend it on basic necessities, such as food and gas. See Jeffery M. Jones, “Half in the U.S. Plan to Spend Relief Money on Bills, Essentials,” Gallup News, April 14, 2020. Washington, DC. - The US Treasury Department has stated that about 5 million paper checks can be issued per week beginning in late April, delaying the receipt of these checks by several months for non-direct-deposit filers. See Richard Rubin, “Next Wave of IRS Stimulus Payments Set to Hit Bank Accounts in Coming Days,” Wall Street Journal, April 24, 2020.

- ACS household weights were adjusted to estimate the two different scenarios. In the first scenario, household weights were multiplied by the 95 percent UI uptake rate and the 80 percent direct-deposit rate. For the second scenario, household weights were multiplied by 75 percent and 80 percent.

- Using administrative data, this report estimates that laid-off workers in New England were receiving a total of $1.8 billion per week in UI benefits as of May 9, 2020. This estimate is based on total weekly UI claims from March 21, 2020, through May 9, 2020; the average February UI benefit for the region ($481); and $600 in additional federal benefit. This report, based on analysis of the American Community Survey (ACS), estimates that UI spending will reach $1.8 billion to $2.4 billion per week. The range is based on the 75 percent and 95 percent unemployment insurance uptake scenarios and estimates of high-risk employment.

- The range in the number of households is based on the 75 percent and 95 percent UI uptake rates, representing the low and high estimates, respectively.

- Based on 2018 ACS one-year estimates.

- See Ella Koeze, “The $600 Unemployment Booster Shot, State by State,” New York Times, April 23 2020.

About the Authors

About the Authors

Nicholas Chiumenti

Acknowledgments

The author thanks Jeffrey Thompson and Melissa Gentry, Osborne Jackson, and Thu Tran for contributing analysis to this report.

Resources

Site Topics

Keywords

- Coronavirus ,

- COVID-19 ,

- employment ,

- housing ,

- mortgage ,

- rent ,

- New England ,

- NEPPC