Rental Affordability and COVID-19 in Rural New England

| Key Facts | |

| Although rents in rural New England in 2019 were, on average, 29 percent less than rents in the region’s urban areas, rural and urban renters both spent, on average, more than one-third of their household income on housing costs. | |

| The region’s rural areas had 2,839 total coronavirus cases per 100,000 residents as of January 2021, yet the number of jobs in those places had decreased 6.1 percent compared with one year earlier. Nationally, rural areas had seen 8,204 total cases per 100,000 residents and lost only 3.1 percent of jobs over the same period. | |

|

|

Although a shortage of affordable rental housing is often framed as an urban-area issue, rural communities also suffer from this problem. On average, rural and urban renters spend similar shares of their income on rent and have comparable rates of housing-cost burden. Years of slow income growth and skyrocketing rents, particularly during the 2000–2010 period, have eroded slack in household budgets that may have gone toward other expenses or toward savings. The coronavirus pandemic likely has exacerbated affordability problems by putting many rural residents out of work. The share of jobs lost in rural New England communities has been large, even though these areas have seen far fewer cases of COVID-19 (relative to their population size and overall) compared with the region’s urban areas. This is in contrast with the experience in much of the rest of the country, where, as of January, rural areas nationally had seen far more COVID-19 cases but had lost a smaller share of jobs. Due to the economic conditions in the region’s rural areas, many renters could find it increasingly difficult to afford their housing costs. Even after the pandemic ends and the negative economic impact subsides, rural New England households likely will still face considerable affordability challenges.

Sign up for new research and data on the New England economy.

COVID-19 and Rental Affordability across New England

Renter households in rural New England face many of the same affordability challenges as renters in the region’s urban areas.1 The average cost of renting an apartment in rural communities is less than the average cost in urban communities due to greater availability of land and less demand for housing;2 however, incomes are lower in rural areas, in part because higher-paying jobs are less abundant.3 As a result, though there are fewer renter households in rural New England than in urban areas, a comparable share of the rural renters are housing-cost burdened; that is, they spend more than 30 percent of their annual household income on rent and utilities.4

According to data from the American Community Survey (ACS), rural New England’s 2019 average gross rent, which includes tenant-paid utilities, was $854 per month, about 28 percent less than the $1,204 average spent per month on rent and utilities in the region’s urban areas.5 But while rents may be lower in rural parts of New England, so are incomes, which negates some of the advantages that these areas’ lower housing costs would offer renters. In 2019, the average household income for renters was about 25 percent less in rural New England relative to the region’s urban areas.6 Consequently, renters in rural New England spent an average of 34 percent of their household income on housing costs that year, while in urban areas the average share was only slightly higher at 37 percent.7 That same year, 38 percent of rural renters were housing-cost burdened, compared with 41 percent of urban renters.8

Each New England state sees this same pattern of rural renters facing financial pressures comparable to those of their urban counterparts. Table 1 shows the average rent, the average share of household income spent on rent, and the rates of housing-cost burden among rural and urban renters in each New England state in 2019. Across the region, the average share of income that rural renters spent on rent ranged from about 2 to 5 percentage points less than the average share that urban renters spent. Massachusetts was the exception; rural renters and urban renters on average spent equivalent amount on rent as a share of income. In each state in 2019, the rate of housing-cost burden among rural renters also was similar to that of urban renters.

Table 1: Affordability for Renter Households in New England

By urban and rural areas (PUMAs) in New England, 2019

| Rural Areas | Urban Areas | |||||

| Average Monthly Rent | Average Share of Income Spent on Rent | Share of Households Cost Burdened | Average Monthly Rent | Average Share of Income Spent on Rent | Share of Households Cost Burdened | |

| Connecticut | $1,025 | 35% | 43% | $1,175 | 39% | 43% |

| Maine | $643 | 33% | 37% | $903 | 35% | 39% |

| Massachusetts | $1,102 | 37% | 39% | $1,295 | 37% | 41% |

| New Hampshire | $927 | 34% | 37% | $1,169 | 36% | 40% |

| Rhode Island | n/a | n/a | n/a | $968 | 36% | 39% |

| Vermont | $822 | 34% | 40% | $1,129 | 39% | 41% |

| Note(s): Rent estimates include tenant-paid utilities. Households with zero or negative income and those in which the head is a student are assumed not to be housing-cost burdened, even if they spend more than 30 percent of their annual household income on rent. In some cases, this report uses microdata that do not identify all counties in New England. In these cases, Public Use Microdata Areas (PUMAs) are used as a substitute. A PUMA is classified as urban if the majority of its population lives within a metropolitan statistical area (MSA), and rural if the majority of its population lives outside of an MSA. Rhode Island is the only New England state without a rural area, and so this report excludes it from the discussion of rural rental affordability.

Source(s): 2015–2019 American Community Survey 5-year microdata. |

||||||

The financial constraints many rural renters face make them—like their urban counterparts—susceptible to economic shocks such as the coronavirus pandemic. This is particularly true for housing-cost-burdened households, which already are at greater risk of missing a housing payment and being evicted compared with households that spend less than 30 percent of their income on rent. The demographic profile of rural America indicates that the residents of these communities are, on average, older and in poorer health. People with such characteristics are considered to be at higher risk of suffering complications from contracting COVID-19.9 As of January 2021, however, the cumulative number of confirmed COVID-19 cases per 100,000 residents in rural New England was substantially lower than the number in the region’s urban areas, as shown in Figure 1. In contrast, rural areas in the United States as a whole have had far more COVID-19 cases relative to their population size; the share of the rural population that had been infected as of January 2021 was more than the share that had been infected in urban areas across the country.10 But while the pandemic may not be having as large a health impact on New England’s rural areas relative to urban areas, it is having a similar economic impact due to businesses closures and restrictions on economic activity aimed at limiting the spread of the virus.

{kind=link}

Meghan Smith/Federal Reserve Bank of Boston

Beginning in March 2020 and accelerating in April, many businesses around the country—in urban and rural communities—chose or were required to cease operating due to the pandemic, causing a spike in unemployment. Subsequent business re-openings have allowed people to return to work, but as shown in Figure 1, rural New England areas still had 6.1 percent fewer employed workers in January 2021 compared with one year earlier. Urban New England areas had 7.4 percent fewer employed workers in January 2021 compared with January 2020. Nationally, rural areas experienced a 3.1 percent decline in employment over last year, while urban areas overall saw a 5.8 percent decline. The greater loss of jobs in the region’s rural areas relative to rural areas in the rest of the country is likely due to a combination of differences in the policy response to the pandemic and the composition of the regional economy. Some of the industries most heavily affected by shutdown orders and social-distancing requirements account for a disproportionately large share of employment in rural areas. These include leisure and hospitality, which was New England’s hardest-hit industry; total employment in this sector fell by more than 50 percent between February and May 2020. Other hard-hit industries include education and health services, and trade (which includes retail establishments), transportation, and utilities. In New England, those two industries saw employment decline 13 percent and 17 percent, respectively, between February and May 2020.11 Widespread job losses could mean rural renters, like their urban counterparts, are equally at risk of missing housing payments and consequently facing eviction or even homelessness.12

Rural Area Affordability within New England States

The disparity between the health and economic impacts of the coronavirus pandemic in rural New England is most evident at the county level. As Figure 2 shows, as of January 2021 most of the region’s 33 rural counties had 1,000 to 3,000 confirmed COVID-19 cases for every 100,000 residents. In comparison, that same month only five of the region’s 34 urban counties had 1,000 to 3,000 confirmed cases per 100,000 residents, with the majority having more than 5,000 cases. However, many rural counties have experienced rates of job loss in the last year that are comparable to those of urban areas. In one rural county, Lamoille County, Vermont, the number of employed workers declined more than 12 percent between January 2020 and January 2021.

{kind=link}

Meghan Smith/Federal Reserve Bank of Boston

Some rural areas that have seen large-scale job loss as a result of the pandemic are also ones where renter households spend a relatively large amount on housing costs. Of the 19 rural counties that experienced a greater than 5 percent decline in total employment between January 2020 and January 2021, 12 had average rents that were higher than the statewide rural-area average. However, as discussed earlier, even where rents are lower, households do not necessarily experience less financial pressure, not if lower incomes negate the benefits of low rents. In 2019, for example, the rural communities in Western Massachusetts had above-average rates of housing-cost burden despite that area’s average rent being about 15 percent less that the state’s rural-area average.

{kind=link}

Meghan Smith/Federal Reserve Bank of Boston

Figure 3 displays the affordability threshold in rural areas of New England relative to their home state’s median household income. The affordability threshold is the annual household income above which a household has access to a surplus of available apartments; that is, the household likely can find apartments on the market that won’t render it housing-cost burdened.13 For example, in the rural area encompassing Litchfield County, Connecticut, the affordability threshold was $41,000 per year in 2019. Households earning more than this amount are more likely to find an apartment they can afford, while those making less than this amount are more likely to pay more than 30 percent of their income toward rent. While the affordability threshold in Litchfield County is higher than that of almost every other rural area in New England, it is equivalent to only 52 percent of Connecticut’s median household income. Relative to what the median household earns in the state, the rents charged in the rural areas are as affordable to Connecticut residents as rents in rural parts of Maine, New Hampshire, and Vermont are to residents of those states.

In northern New England’s rural counties (in Maine, New Hampshire, and Vermont), rents are generally more affordable, even after differences in income across the states are taken into account. In 2019, the affordability thresholds in rural northern New England ranged from 43 percent to 58 percent of the respective state median incomes. In the three rural areas of southern New England, the thresholds were 52 percent (Connecticut), 57 percent (Massachusetts), and 68 percent (Massachusetts) of the respective state median incomes. However, in 2019, housing costs in at least one rural northern New England rental market were as high as those in southern New England, relative to the state median income. Renters living in Vermont’s southeastern rural area had to earn 58 percent of the state median income to have access to a surplus of affordable units, which is comparable to the affordability threshold in rural Western Massachusetts, where renters needed to earn 57 percent of the state median income.

Long-term Affordability Trends

The coronavirus pandemic has highlighted the economic danger looming over households that struggle to pay rent. A permanent or even temporary job loss puts these households at risk of losing their homes. But the pandemic has only exacerbated the affordability crisis in rural New England; it didn’t cause it. Long-term stagnant or declining incomes have, in part, led to a shortage of affordable apartments. Years of increasing rents also have eroded affordability for rural renters and are likely the result of many different factors. The high cost of housing in neighboring urban areas has driven up demand for less expensive housing options in rural communities. Many of New England’s rural places are also popular vacation destinations, and the purchase of existing housing stock for second homes or vacation rental properties restricts the supply of housing for year-around residents, driving up prices. Also, low rents historically have meant less incentive to build new rental housing stock because the returns on investment are lower, and so while the demand for housing has increased, the supply has not kept pace.

Rural rents and incomes have consistently been lower than those in urban areas. In 2000, the average rent in rural New England was 30 percent less than that of urban areas, while the average rural renter household income was 21 percent less. After 2000, incomes declined in the rural areas of two New England states and lagged far behind rising rents in the rural areas of the other three states. Figure 4 shows the change in the rent-to-income ratio for rural renters in each New England state. Between 2000 and 2019, the rent-to-income ratio increased in both rural and urban parts of New England, meaning that rental costs increased as a share of household income. However, they increased more in rural areas than in urban ones, and thus rural renters saw a greater loss of rental affordability during this period than their urban counterparts. Between 2000 and 2019, the average renter household income across rural New England increased 4.1 percent (adjusted for inflation), while the average rent increased 27.3 percent.14 In urban areas during this period, the average income increased 11 percent, while the average rent increased 31.1 percent. Renters in some New England rural areas fared slightly better than others in terms of income growth. In Vermont, for example, household incomes increased 6.7 percent on average between 2000 and 2019; however, rents in rural Vermont increased 31 percent on average, the largest rural-area rent increase in the region.

{kind=link}

Meghan Smith/Federal Reserve Bank of Boston

Much of the decline in rural housing affordability occurred between 2000 and 2010.15 During this period, average incomes of renter households declined in the rural areas of Connecticut, Maine, and New Hampshire, and they increased less than 1 percent in Massachusetts and Vermont.16 Meanwhile, average rents across rural New England increased at rates of 16 percent to 28 percent, depending on the state. This trend mostly reversed during the 2010–2019 period.17 The growth in average income outpaced rent increases overall, although in two states, Maine and Massachusetts, the difference was less than 1 percentage point. Nevertheless, the finances of rural renters did not improve enough between 2010 and 2019 to close the gap that had widened during the previous 10 years.18

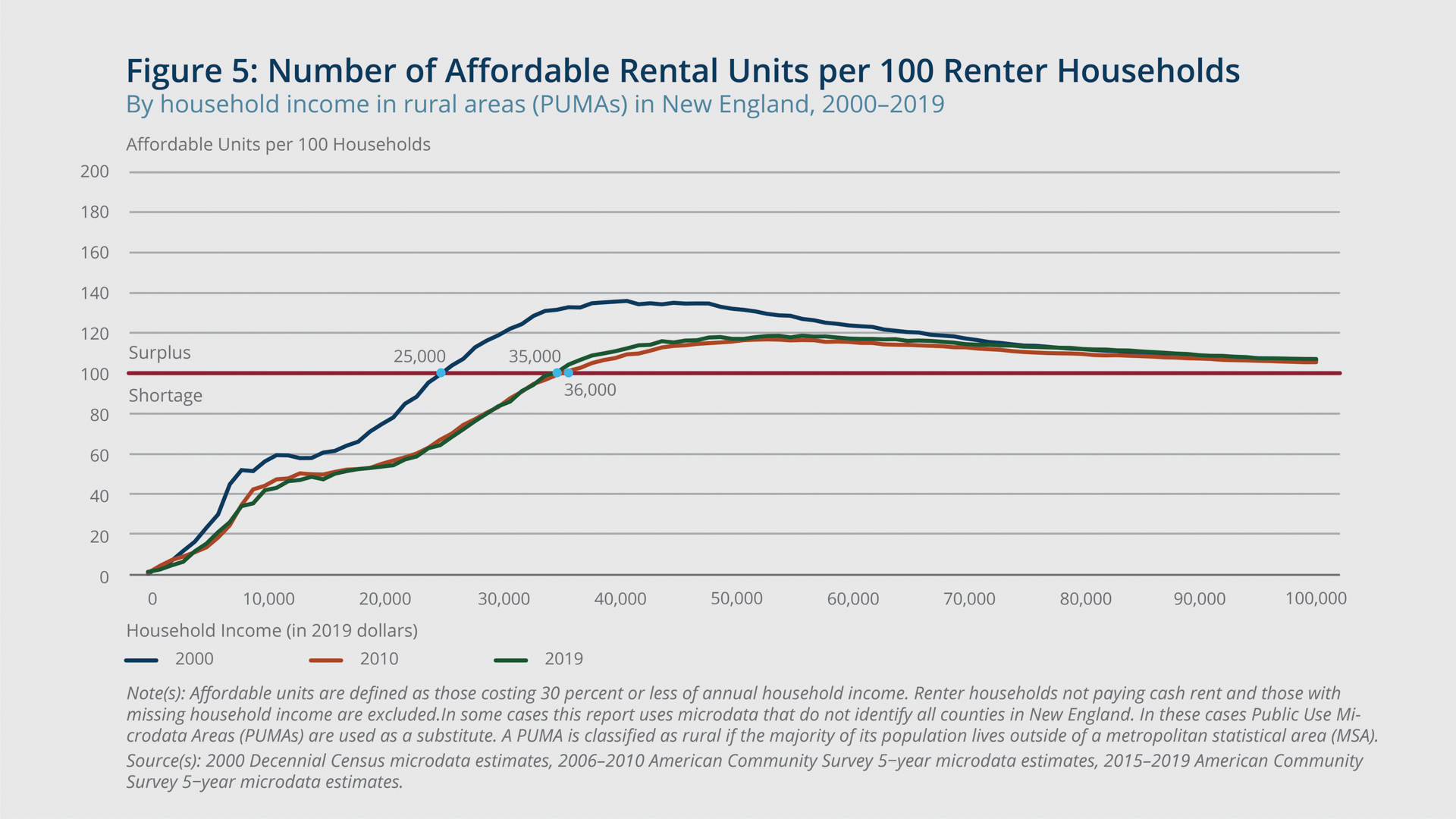

Figure 5 shows the number of rental units per 100 households in all of rural New England that were affordable at a given level of income. In 2000, the affordability threshold across the region’s rural areas was $25,000 (in 2019 dollars), meaning that renter households earning less than this amount per year experienced a shortage of affordable apartments. Households earning this amount or more per year were more likely to be able to find a rental unit they could afford, while those below this income level were more likely to have to spend at least 30 percent of their income on rent—a share that is commonly regarded as a housing-cost burden.

{kind=link}

Meghan Smith/Federal Reserve Bank of Boston

After 2000, the number of affordable apartments in rural New England declined substantially, particularly for households earning $30,000 to $40,000 annually. In 2000, for every 100 households earning $40,000 (in 2019 dollars), the market included about 135 affordable apartments. By 2010 this supply had fallen to 108 apartments, a decline of 20 percent. In 2019, this supply had increased slightly to 110 apartments. Between 2000 and 2019, households earning $30,000 (in 2019 dollars) went from seeing about 120 affordable apartments for every 100 households in rural New England to only 83 per 100 households. The affordability threshold (100 affordable apartments for every 100 households) went from about $25,000 (in 2019 dollars) in 2000 to about $35,000 in 2018, an increase of 40 percent.

Support for Renters in Response to COVID-19

The long-term decline in rural rental affordability, coupled with the economic distress brought on by the pandemic, poses unique challenges for policymakers. Renters today are likely less capable of withstanding a financial shock, such as job loss, than in the past. The coronavirus pandemic induced just such a shock by causing businesses to close and economic activity to slow. Previous research by the New England Public Policy Center finds that as a result of pandemic-related unemployment, about 30 percent of renter households in New England were at risk of missing a housing payment if they did not receive any financial assistance.19 Given the comparable rates of housing-cost burden, shares of income spent on rent, and job losses, it is likely that the region’s rural renters are just as at risk as urban renters of being unable to afford their monthly rent payments.

Since the start of the COVID-19 pandemic in March 2020, Congress has passed various federal stimulus bills providing financial assistance to households. The federal Coronavirus Aid, Relief, and Economic Security (CARES) Act, enacted in March 2020, alleviated some of the financial pressures on many households by providing individuals with an additional $600 per week in Pandemic Unemployment Assistance (PUA) and/or a direct payment of as much as $1,200. However, the PUA program expired at the end of July.20 The replacement Lost Wages Assistance (LWA) program followed the expiration of PUA and provided individuals with an additional $300 per week in unemployment insurance benefits for six weeks. In most states, the LWA assistance came during August and September.21 An appropriations bill passed at the end of 2020 (H.R. 133) extended many of these additional $300 payments through March of 2021 and allowed those on unemployment to receive benefits for as long as 50 weeks total.22 More recently, the American Rescue Plan Act (ARPA) extended both regular unemployment benefits and the additional $300 benefit to a total of 79 weeks, until September 2021. The ARPA also included a direct payment of as much as $1,400 per individual. As long as the unemployment rate continues to decline, the financial support provided by the ARPA should help prevent further economic hardship among those who are still without work.

Historically, the federal government has been an important source of funding for affordable housing in both rural and urban communities. The US Department of Agriculture (USDA) administers programs specifically for rural areas, but funding for these programs has diminished over time.23 Some policymakers advocated unsuccessfully for additional funding of USDA rental assistance programs during negotiations over the CARES Act and subsequent legislation.24 While USDA rental assistance remains an important source of financial support for rural renters, it is less important now than in the past. In 2019, 22 percent of units receiving federal rental assistance in rural New England were subsidized through USDA programs; the rest were subsidized through programs administered by the US Department of Housing and Urban Development (HUD).25

The CARES Act, H.R. 133, and the ARPA all provided additional funding for rental assistance both through HUD26 and through the federal Emergency Rental Assistance Program. While the funding is not explicitly targeted to rural areas, many rural residents will benefit either because they participate in HUD-administered programs or because states have set up their own rental-assistance programs open to all renters using federal and state dollars. As of the writing of this report, every New England state had in place a rental-relief program funded at least partially by federal stimulus dollars. The total amount of funding allocated varies and is a mix of federal and state sources. The ARPA was the most recent and largest appropriation of rental-assistance funding, with the New England states receiving $200 million to $450 million for rental assistance alone.27 State-level eviction moratoriums also helped to prevent renters from becoming homeless, but these moratoriums had ended in all but two New England states as of this report’s writing.28 A nationwide moratorium remains in effect until the end of June 2021, but it likely covers fewer renters than the state-level moratoriums did.29 Regardless of their reach, eviction moratoriums only postpone an inevitable loss of housing unless back rent is paid.

Conclusion

Renter households in rural New England communities face housing affordability issues that in many ways resemble those of renters in the region’s urban areas. Across New England, the share of renter households in rural areas that are housing-cost burdened is similar to the share in urban areas. In both rural and urban areas of the region, renter households on average spent more than one-third of their income on rent in 2019. Even though rents in rural communities are lower than urban-area rents, so are incomes. As in urban areas, housing affordability for renters in New England’s rural communities has declined in recent decades. To access the portion of the local rental market that is not plagued by supply shortages, renter households in rural New England needed to earn 40 percent more income in 2019 than in 2000.

The coronavirus pandemic has the potential to further reduce housing affordability in rural New England. Previous research by the New England Public Policy Center (NEPPC) shows that pandemic-related job losses have increased the likelihood of renter households missing rent payments. The financial constraints that rural renter households face make them just as likely as urban renter households to fall behind on rent. If unemployment persists, many more rural renters will pay a greater share of income toward rent.

States and the federal government have responded to this crisis by funding rental- and mortgage-relief programs aimed at enabling at-risk households to remain in their homes. Every New England state has launched a rental-assistance program using money from federal stimulus packages. However, the decline in rural rental affordability took place over decades, and the economic pressures causing it (low wages, limited housing stock) will likely continue even after the pandemic subsides.

Data Sources

The 2000 Decennial Census, 2010 Decennial Census, and 2015–2019 American Community Survey five-year microdata estimates were provided by Steven Ruggles, Sarah Flood, Sophia Foster, Ronald Goeken, Jose Pacas, Megan Schouweiler, and Matthew Sobek. IPUMS USA: Version 11.0 [dataset]. Minneapolis, MN: IPUMS, 2021. https://doi.org/10.18128/D010.V11.0

The 2000 Decennial Census, 2010 Decennial Census, and 2015–2019 American Community Survey five-year aggregate estimates were provided by Steven Manson, Jonathan Schroeder, David Van Riper, Tracy Kugler, and Steven Ruggles. IPUMS National Historical Geographic Information System: Version 15.0 [data set]. Minneapolis, MN: IPUMS. 2020. http://doi.org/10.18128/D050.V15.0

Johns Hopkins University Coronavirus Resource Center COVID-19 Dashboard. See Dong, Ensheng, Hongru Dum, Lauren Gardner. 2020. “An Interatictive Web-based Dashboard to Track COVID-19 in Real Time.” The Lancet Infectious Diseases 20(5): 533–534.

US Bureau of Labor Statistics (BLS) 2020 and 2021 Local Area Unemployment statistics by county.

Endnotes

- Rhode Island is the only New England state without rural areas, and so this report excludes it from the discussion of rural rental affordability, although the state is included in the analysis of the region’s urban areas overall. By this regional brief’s definitions, urban counties fall within a metropolitan statistical area (MSA) and rural counties fall outside of MSA boundaries. An MSA encompasses counties that share close economic ties and have relatively high population densities. In some cases, this report uses microdata that do not identify all counties in New England. In these cases, Public Use Microdata Areas (PUMAs) are used as a substitute. In this report, a PUMA is classified as rural if the majority of its population lives outside of an MSA. The exception to this definition involves the PUMA that includes Dukes, Nantucket, and parts of Barnstable counties in Massachusetts. It is classified as rural even though the majority of its population lives in an MSA. This part of Massachusetts is generally considered rural, even though it meets the criteria for a metro area.

- Scally, Corianne, Brandi Gilbert, Carl Hedman, Amanda Gold, and Lily Posey. 2018. “Rental Housing for the 21st Century Rural America.” The Urban Institute. Washington, DC.

- US Department of Agriculture (USDA). 2016. “Rural America at a Glance, 2016 Edition.” Washington, DC.

- About one-quarter of households in rural New England rented in 2019 as opposed to owning their own home. The share of renters has remained essentially unchanged since at least 2000. In comparison, 36 percent of New England’s urban-area households rented their home in 2019.

- Unless otherwise specified, references to rent in this report refer to gross rent, which includes tenant-paid utilities.

- The average renter household income in rural New England was $44,004 in 2019; in the region’s urban areas, it was $58,589. Household income includes income from all sources, such as wages, investments, businesses, retirement benefits, and Social Security and other government programs.

- In some cases, households in the ACS are estimated as spending more than 100 percent of their income on gross rent. This report assumes such households spend a maximum of 100 percent on gross rent.

- In this report, households with zero or negative income and those in which the head is a student are assumed not to be housing-cost burdened, even if they spend more than 30 percent of their annual household income on rent. This is to account for a temporary reduction in income that a household may experience from, for example, the sale of a large investment at a loss. Such a reduction would classify the household as housing-cost burdened even though it can afford its housing costs month to month. This adjustment is similar to one in the US Department of Housing and Urban Development’s “Worst Case Needs” series of reports. See US Department of Housing and Urban Development (HUD), 2020, “Worst Case Housing Needs: 2019 Report to Congress,” Washington, DC. Student-led households are also assumed to have other sources of financial support they can rely on that are not captured in the ACS, such as savings or familial support.

- Peters, David J. 2020. “Community Susceptibility and Resiliency to COVID-19.” The Journal of Rural Health 36(3): 446–456.

- As of January 2021, there were 8,204 cumulative confirmed COVID-19 cases per 100,000 residents across all rural counties in the United States and 7,837 cumulative confirmed cases per 100,000 residents across all US urban counties. These numbers are based on data from the Johns Hopkins University COVID-19 Dashboard Cases by US County.

- Based on data from the Bureau of Labor Statistics’ Establishment Survey, in 2019, about 16 percent of employed workers in rural New England worked in leisure and hospitality compared with about 12 percent in urban areas. The trade, transportation, and utilities industry employed almost 20 percent of workers in rural New England and 18 percent in the region’s urban areas. Education and health services employed about 25 percent of workers in both rural and urban areas.

- Chiumenti, Nicholas. 2020. “Impact of the COVID-19 Pandemic on New England Homeowners and Renters.” New England Public Policy Center Regional Briefs No. 20-2. Federal Reserve Bank of Boston.

- Affordability here is defined as costing 30 percent or less of household income per year.

- Average incomes and rents were adjusted for inflation to 2019 dollars using the Personal Consumption Expenditure (PCE) price index.

- Likely reasons why household income grew more slowly between 2000 and 2010 than it did between 2010 and 2018 include the 2007–2008 recession, which caused unemployment to spike in many communities across the nation and the average household income to decline. Thus, it is unclear if the decline in income in some states was due to declines in wages or a decline in earnings overall.

- Between 2000 and 2010, renter household incomes declined 10.5 percent in Connecticut, 2.2 percent in Maine, and 2.9 percent in New Hampshire. During this period, renter household incomes grew 0.6 percent in Massachusetts and 0.2 percent in Vermont.

- Between 2010 and 2019, incomes grew 12.4 percent in rural Connecticut while rents increased 6.1 percent. In rural Maine, incomes grew 5.2 percent while rents increased 4.7 percent. In rural Massachusetts, incomes grew 4.6 percent while rents increased 4.5 percent. In rural New Hampshire, incomes grew 7.6 percent while rents increased just 1.4 percent. In rural Vermont, incomes grew 6.4 percent, while rents increased 3.1 percent.

- Urban areas faired similarly to rural areas between 2000 and 2019. Urban renter household incomes increased an average of 11 percent during this period, while rents rose 31.1 percent on average. As with rural areas, much of this gap grew between 2000 and 2010, when incomes decreased about 5 percent in urban areas and rents increased 19.3 percent. In the subsequent eight years, incomes grew 15.8 percent while rents grew 9.8 percent.

- Chiumenti, Nicholas. 2020. “Impact of the COVID-19 Pandemic on New England Homeowners and Renters.” New England Public Policy Center Regional Briefs No. 20-2. Federal Reserve Bank of Boston.

- In April 2020, the US Congress passed the CARES Act in response to the coronavirus pandemic. This legislation extended the amount of time unemployed workers can receive state unemployment insurance (UI) benefits and provided an additional $600 per week in Pandemic Unemployment Assistance (PUA) until no later than July 31, 2020. The CARES Act also gave many individuals a one-time stimulus payment of as much as $1,200. See Coronavirus Aid, Relief, and Economic Security (CARES) Act of 2020, II USC § 2102-2201.

- The LWA program is funded through grants from the Federal Emergency Management Agency (FEMA). Ostensibly this program is in place until December 27, 2020, but the application period and limited funding available means that most states spent the additional assistance during August and September, leaving many renters without financial support during the remaining months of 2020. See the Federal Emergency Management Agency Lost Wages Supplemental Payment Assistance Guidelines website, https://www.fema.gov/disasters/coronavirus/governments/supplemental-payments-lost-wages-guidelines.

- See H.R. 133 Consolidated Appropriations Act, 2021

- Since the late 1980s, the amount of money allocated to USDA’s rental housing programs has declined 97 percent. These programs include Section 515, which provides loans to developers that build affordable housing, and the companion Section 521, which provides rental assistance to residents who live in Section 515 units. No new units have been created under these programs since 2012. See National Rural Housing Coalition, 2017, “A Review of Federal Rural Rental Housing Programs, Policy and Practices,”Washington, DC.

- See “Shaheen & Hassan Call for Rural Housing Assistance amid Economic Fallout from Pandemic,” April 19, 2020, press release, office of US Sen. Maggie Hassan (New Hampshire), https://www.hassan.senate.gov/news/press-releases/shaheen-and-hassan-call-for-rural-housing-assistance-amid-economic-fallout-from-pandemic.

- Based on data from the National Housing Preservation Database (NHPD), updated April 2020, and HUD’s 2019 Picture of Subsidized Households.

- The ARPA also included nearly $5 billion in homeless prevention grants for providing rental assistance, developing affordable housing, and other services for people experiencing or at-risk of homelessness.

- According to the US Treasury Department, the maximum amount of new funding available to New England states through the federal Emergency Rental Assistance Program includes $235 million for Connecticut, $457 million for Massachusetts, and $200 million each for Maine, New Hampshire, Rhode Island, and Vermont. See US Department of the Treasury website, https://home.treasury.gov/policy-issues/cares/emergency-rental-assistance-program.

- Connecticut and Vermont are the only two remaining New England states with eviction moratoriums. Connecticut’s moratorium is set to end on April 19, 2021. Vermont’s moratorium lasts until 30 days after the end of the state’s declared emergency (currently set to end on April 15, 2021).

- The Centers for Disease Control and Prevention enacted a nationwide moratorium on evictions to last until the end of June 2021. However, it differs distinctly from state-level moratoriums, as it does not prevent a landlord from beginning an eviction process in a housing court. In order to be covered by the moratorium, a tenant must provide a declaration to their landlord and the housing court judge that they meet certain criteria. See Centers for Disease Control and Prevention, 2020, “Temporary Halt in Residential Evictions to Prevent the Further Spread of COVID-19,” Federal Register Vo. 85, No. 173, September 4, 2020, Notices.

About the Authors

About the Authors

Nicholas Chiumenti

Resources

Site Topics

Keywords

- New England ,

- NEPPC ,

- Affordable Housing ,

- COVID-19 ,

- Coronavirus ,

- rural areas ,

- housing-cost burden

Related Content

The Housing Bust and Housing Affordability in New England

New England Study Group Past Meetings

Economic Fallout of the COVID-19 Pandemic in New England

New Boston Fed analyses outline grim economic consequences of COVID-19 pandemic in New England