Nursing Home Closures in New England: Impact on Long-term Care, Labor Markets

{kind=link}

Federal Reserve Bank of Boston

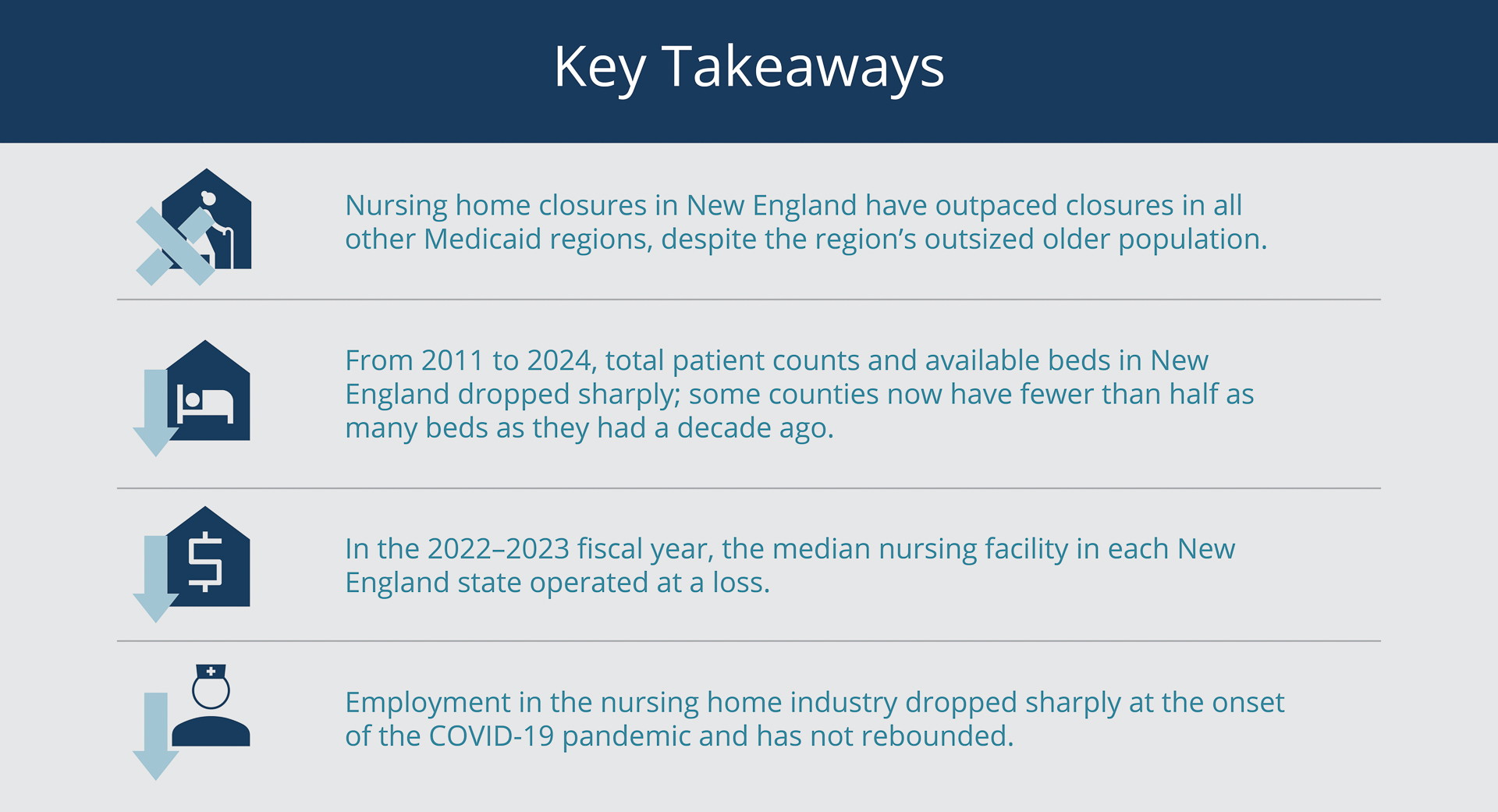

The US population, particularly in New England, is aging rapidly—both the median age and the share of the population aged 85 and older have increased and are projected to continue rising. This group of older adults is the segment of the population most likely to require long-term care, which encompasses a variety of formal and informal care options. The most intensive of these care options is provided in residential nursing facilities, better known as nursing homes. New England has seen a pattern of nursing home closures since at least 2011, and in some counties, the number of available beds has plummeted to less than half of what it was a decade ago.

Due in part to increasing longevity, improvements in the health of older adults, and personal and family preferences, more older residents are remaining in their homes, or “aging in place.” Informal care and state programs designed to keep residents in their homes longer are also contributing to this trend. In recent years, nursing homes’ limitations on visitors and elevated rates of fatalities during the height of the COVID-19 pandemic may have played a role as well, though the trend predates the pandemic.

Sign up for new research and data on the New England economy.

The number of older adults aging in place may be increasing in the region, nevertheless nearly one-third of the New England states’ combined Medicaid spending is devoted to funding long-term care. In 2023, low reimbursement rates from Medicaid and Medicare and high operating costs resulted in most nursing homes in New England losing money, suggesting the region could see more closures unless significant changes occur.

An Older Population That Is Aging Rapidly

In the United States and New England, the 85-and-older cohort is the fastest growing segment of the population. This group is also the most likely to rely on long-term care options, including nursing homes (Gruber and McCrary 2023). The economic implications of an aging population range from reduced labor force productivity to increased spending on entitlement programs, including those that support long-term care.

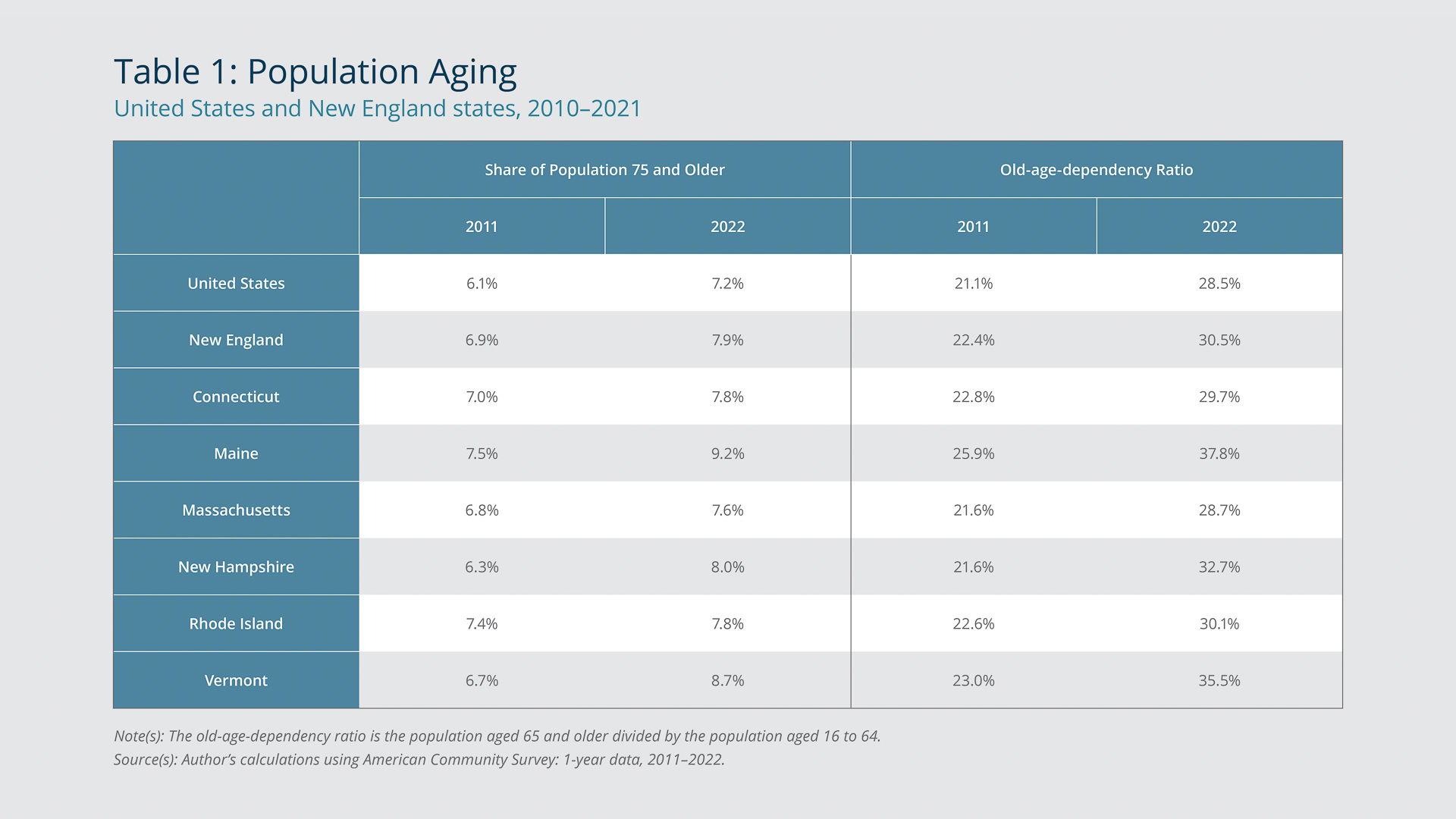

In each New England state, the share of the population that is aged 75 and older is greater than the 75-and-older share of the US population (Table 1). From 2011 to 2022, the growth of this share was especially accelerated in the northern New England states of Maine, New Hampshire, and Vermont, which now have the three oldest median ages in the United States. Over the same period, the old-age-dependency ratio for New England grew even more rapidly, from 22.4 percent to 30.5 percent. This ratio measures the size of the population at or older than the typical retirement age (65) against the size of the typically working-age population (16 to 64). The increase in this ratio indicates that the number of working-age residents in the region is declining relative to the number of older residents. These younger residents often bear the responsibility of providing informal care to aging family members who require care but are not in nursing homes. As the older population continues to grow, pressures on informal caregivers and the region’s long-term-care infrastructure will continue to increase.

{kind=link}

Federal Reserve Bank of Boston

Number of Nursing Homes Is Falling Fastest in New England

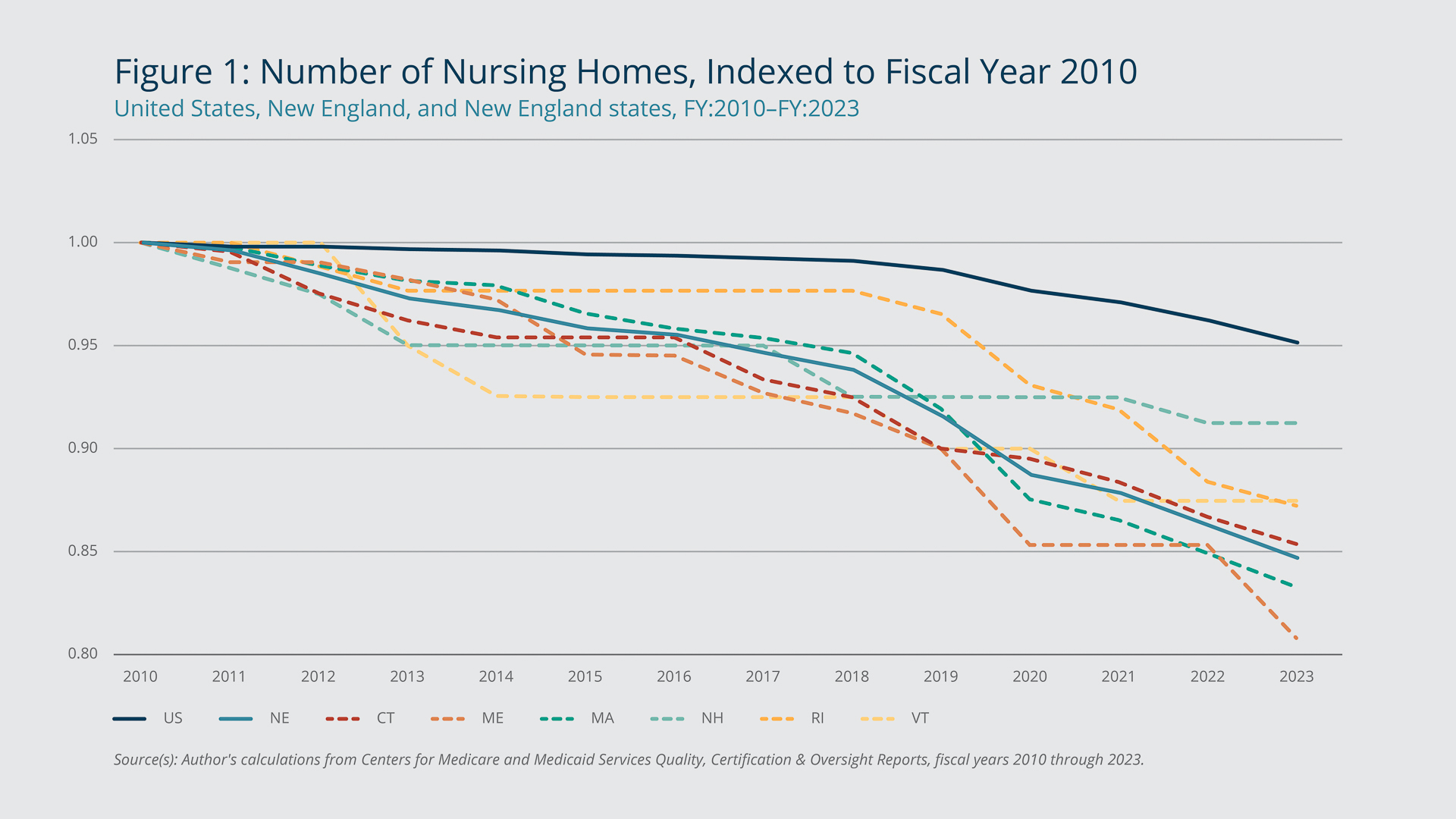

Nursing facilities across the country have garnered significant attention in recent years, particularly during the COVID-19 pandemic, for both quality and cost of care. Nationally, closures have accelerated, but this trend predated the pandemic, particularly in New England (Figure 1). From the start of fiscal year 2010 through the end of fiscal 2023, the number of nursing homes in New England decreased 15 percent. The six New England states each experienced declines greater than the national rate. The region has seen a net loss of more than 150 nursing facilities over the period considered. Maine, the state with the oldest population according to the metrics in Table 1, experienced the greatest decline in the number of nursing homes: 19 percent. Considered jointly, the demographic and nursing home trends indicate that, compared with a decade ago, New England has more older residents and fewer facilities to provide care.

{kind=link}

Federal Reserve Bank of Boston

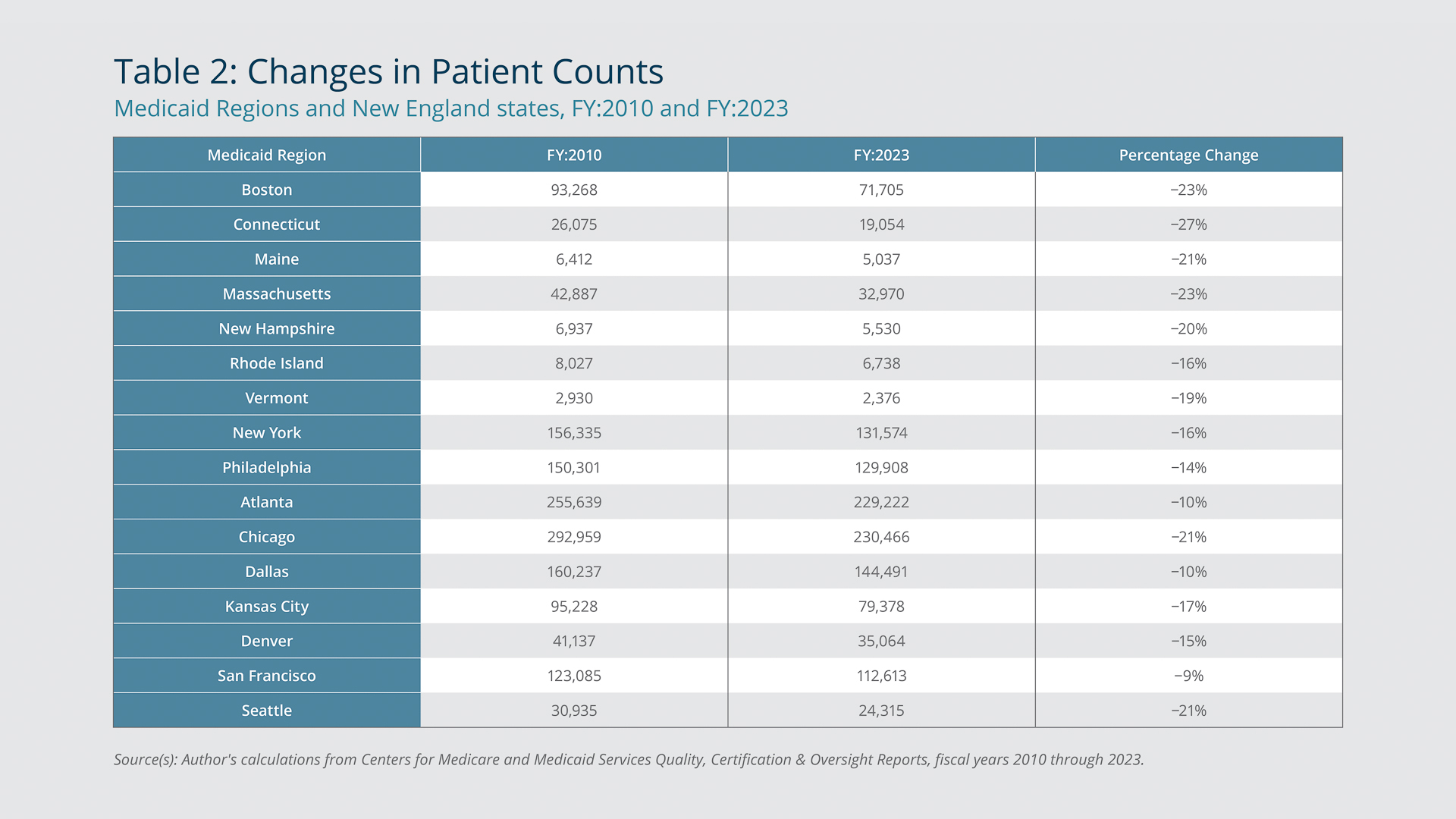

As the number of nursing facilities in New England has declined, so have patient counts. The Boston Medicaid Region, which encompasses the six New England states, saw a 23 percent decline in its patient count from fiscal years 2010 through 2023. This was the steepest drop among the country’s 10 Medicaid Regions (Table 2). Informal care, home health care, and state programs to assist residents aging in their homes have plausibly provided alternatives to nursing facilities and contributed to the declining patient count. However, these alternatives can come with costs. For example, providing informal care may prevent prime-age workers from participating fully in the labor market. More broadly, older adults staying in the homes they may have otherwise left affects the region’s already-tight housing market.

{kind=link}

Federal Reserve Bank of Boston

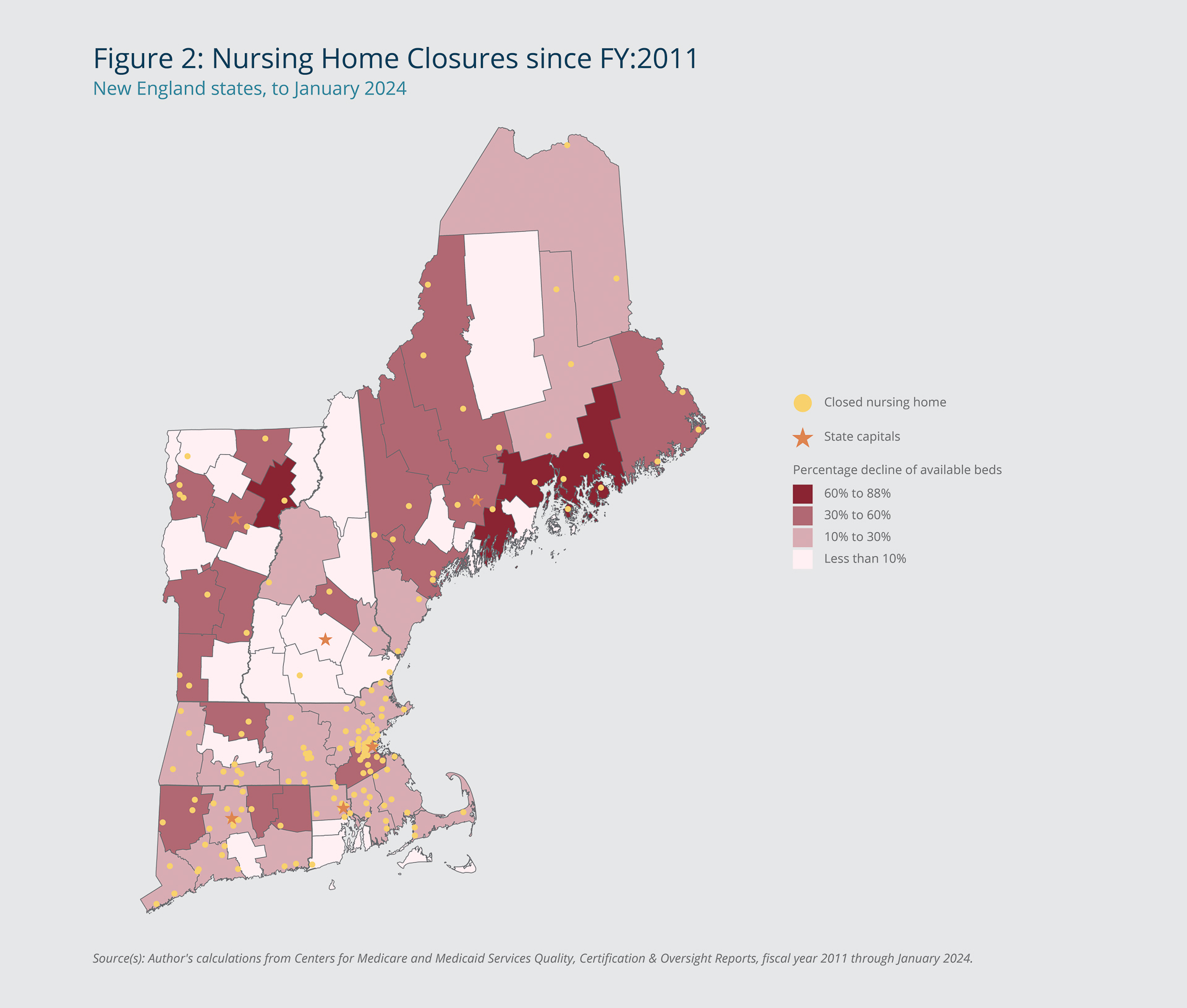

Changes in the number of nursing homes can have differing effects on patient counts due to the wide variation in the number of beds at each facility and in the length of patients’ stays. Figure 2 illustrates the locations of closures across the region and the change in the number of beds in each county. Some counties had less than half the number of beds in January 2024 than they had in fiscal year 2011. While Greater Boston was the area with the most closures, the counties that saw the greatest percentage declines in bed quantities were concentrated in Vermont, Connecticut, and Maine. This is because those counties had fewer facilities in 2011, and a substantial share of the facilities that closed were large.

Many counties have thus far avoided closures; however, nursing homes continue to face challenges, as indicated by the industry profitability trends examined in the next section.

{kind=link}

Federal Reserve Bank of Boston

Medicaid Pays the Largest Share of Costs for Long-term Care

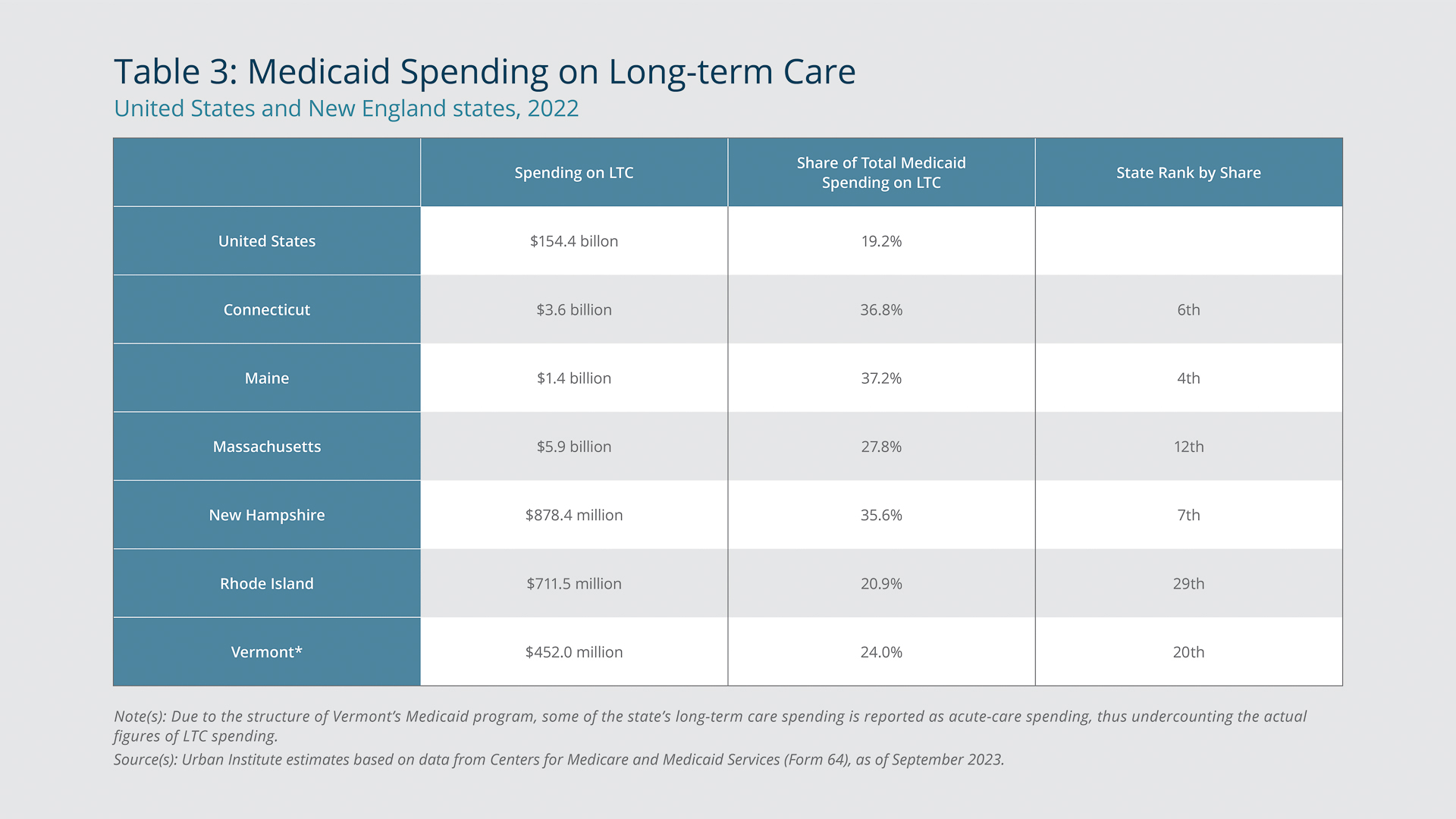

Long-term care (LTC) in the United States is funded through a mix of Medicaid, Medicare, private insurance, veterans’ benefits, and out-of-pocket expenditures, but Medicaid provides the largest share of funding.1 Although Medicare covers most of older adults’ health-care expenses, it typically covers only short-term stays in LTC facilities following hospitalizations. For eligible patients, Medicaid is the designated funder of longer-term care. Many patients who do not have private LTC insurance must exhaust their personal savings through out-of-pocket spending before they become eligible for Medicaid.

Private LTC insurance premiums vary widely based an individual’s age, health status, level of coverage, and other factors. Policies provide coverage for expenses such as nursing home care, assisted living, and home-health services. Even though an estimated 70 percent of Americans 65 and older will need critical services before they die, only 3 to 4 percent of Americans aged 50 and older have LTC policies (Johnson 2019).

Due to this low rate of private insurance, the burden of financing long-term care falls primarily on individuals and their families, who have to pay out of pocket, or the government. Medicaid programs support long-term care for those who have minimal financial resources or who deplete their resources through paying for long-term care. Medicaid plans and coverage vary by state. Table 3 illustrates the annual amount of funding that was dedicated to long-term care in the United States and in each New England state in 2022. Nationally, Medicaid programs spent more than $154 billion on long-term care, and in New England, one-third of the states’ combined annual Medicaid spending went to funding LTC.

{kind=link}

Federal Reserve Bank of Boston

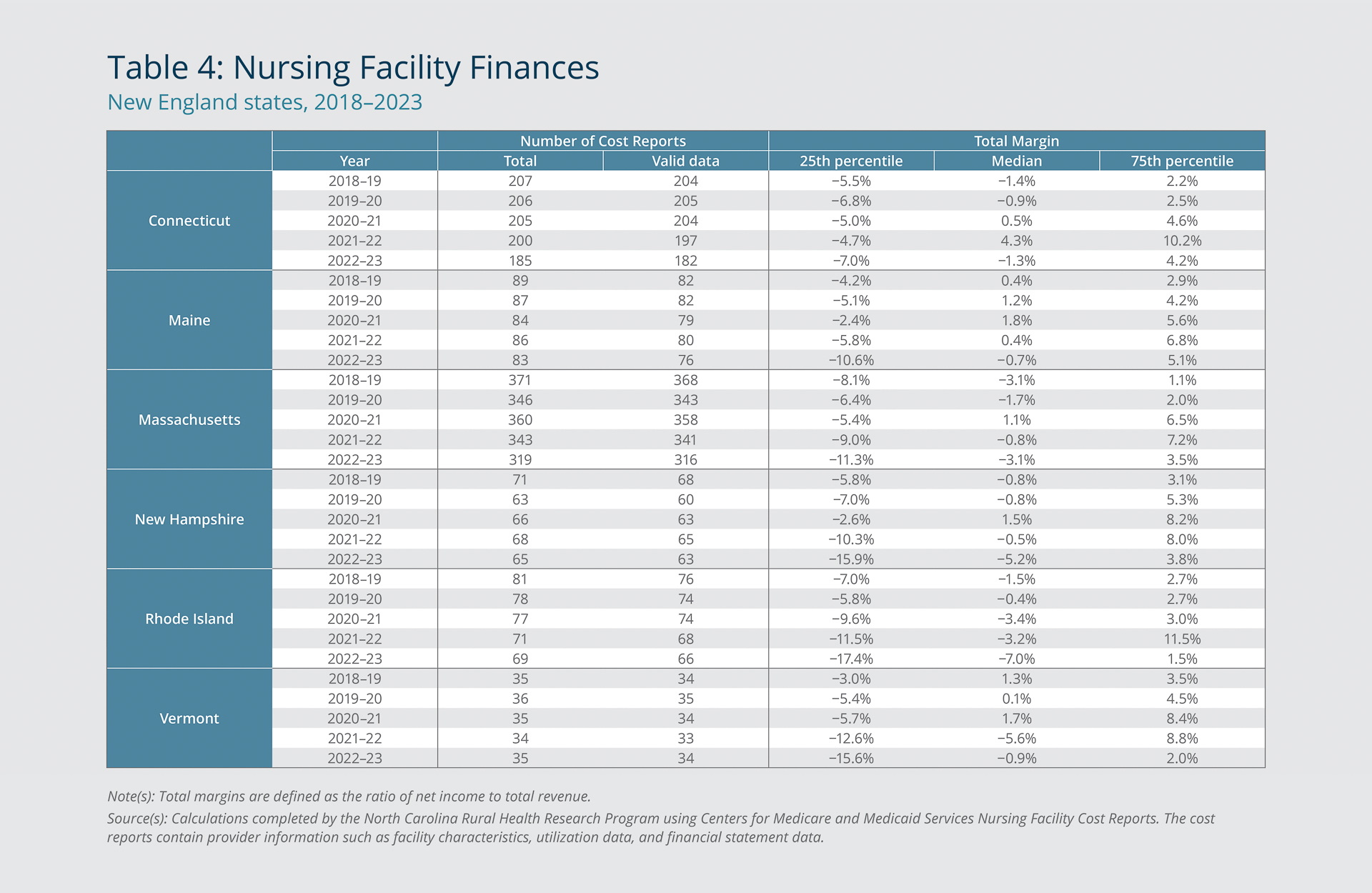

Despite these large expenditures, nursing homes’ operating costs often exceed their Medicaid receipts. Table 4 shows the precarious financial position of most Medicaid-certified nursing facilities in the region. At the end of fiscal year 2023, the most recent year for which data are available, the median facility in each New England state was operating at a loss. If this trend continues, it is likely that more nursing homes will close. During the COVID-19 pandemic, the federal government provided financial support to nursing facilities to help offset revenue losses and high costs related to the crisis.2 This Public Health Emergency (PHE) funding came from Provider Relief Funds (PRF), the Paycheck Protection Program (PPP), and other sources (Ochieng et al. 2022). While these infusions of funds for the 2020–2021 and 2021–2022 reporting periods yielded greater profitability for most facilities, by the most recent period, profitability had dipped back to or below the pre-pandemic levels (in the 2018–2019 and 2019–2020 periods).

{kind=link}

Federal Reserve Bank of Boston

Nursing Homes Facilitate Labor Force Participation

Nursing homes have a twofold impact on the labor market. Directly, they are major employers in some communities, providing jobs for more than 200,000 workers across New England. They also facilitate labor force participation by patients’ family members who would otherwise need to forgo work or reduce their hours to care for their aging relatives.

The role of nursing homes in facilitating labor force participation is particularly important among women (Lily, Laporte, and Coyte 2007) because older adults’ informal caregivers are twice as likely to be female, typically a wife or daughter. The cost of this informal care, when measured as foregone wages, is estimated to be about one-third of the nearly 2 percent of US GDP that is spent on formal LTC (Gruber and McCrary 2023).

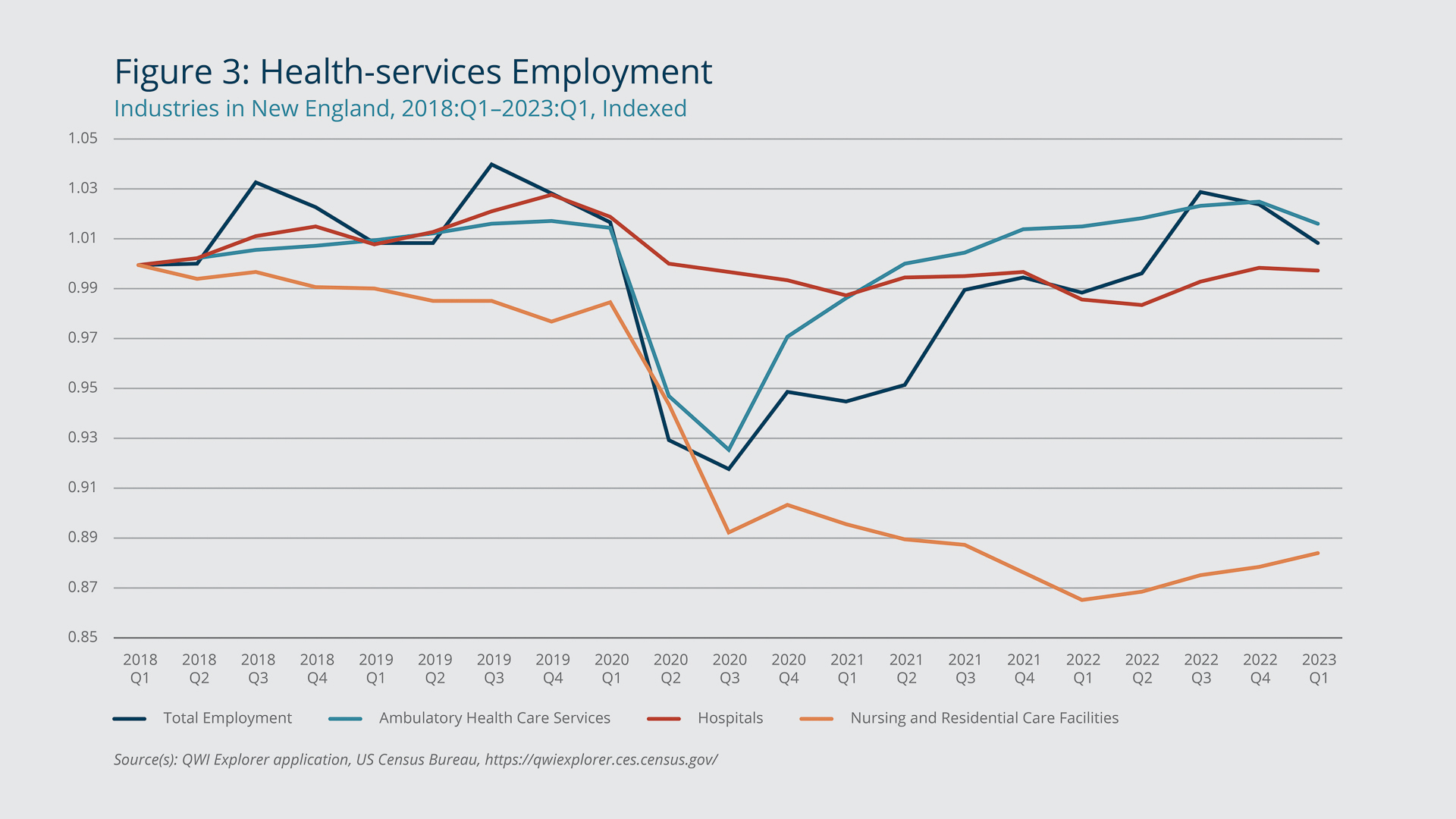

Nursing home closures can also have a direct impact on employment. Whereas most industries rebounded quickly from the spike in job losses at the onset of the COVID-19 pandemic, employment in nursing homes and residential care facilities has still not recovered. Figure 3 disaggregates the three industries comprising health services in New England. It shows that employment in nursing homes and residential care facilities was falling before the pandemic and has continued to flounder, while total employment in New England and in the region’s other two health-services industries has returned to 2018 levels. From the first quarter of 2018 through the first quarter of 2023, the number of workers employed in nursing homes in New England declined by 27,000. Nursing home employment fell in each New England state, ranging from a 7 percent drop in New Hampshire to a 19 percent drop in Rhode Island.3

{kind=link}

Federal Reserve Bank of Boston

Changes to Operations or Reimbursement of Nursing Homes May Be Needed

The current system for funding long-term care faces several challenges. These include the high cost of LTC, which can be a financial burden for individuals and families; the lack of affordable and accessible LTC insurance options; and the growing number of older adults who will need LTC services in the future.

Policymakers are exploring various options for addressing these challenges. In Rhode Island, for example, nursing homes are no longer fined when their staffing falls below the required levels. This policy change, which went into effect in December 2023, is intended to reduce facilities’ cost burden and prevent additional closures.4 However, on April 22, 2024, the Centers for Medicare and Medicaid Services (the federal agency that administers Medicare, Medicaid, and other health services) announced new minimum staffing standards, which will be phased in starting in two years. Interim staffing changes will go into effect in urban facilities by May 2026 and in rural facilities May 2027. At their current staffing levels, less than one-fifth of facilities throughout the country would meet the new standards, meaning most facilities will be required to increase staffing in the coming years.5

States also have launched or continue to operate programs that support residents’ ability to age in their homes. The Home Care Program in Massachusetts provides care management and in-home support services to residents. The cost of these services to the recipient is based on their income.6 Other programs in Massachusetts include the Home Modification Loan Program, which provides loans with 0 percent interest and deferred payment options to homeowners who want to accommodate an older adult living in the home by, for example, installing a ramp or adapting a bathroom.7

Reduced capacity at nursing facilities spills over to the rest of the health-care system. Older patients who receive inpatient care at hospitals are often meant to receive further care at skilled nursing facilities, a subset of nursing facilities that are staffed by medical professionals and intended for shorter stays. In Massachusetts, 1,200 people a day on average are lying in hospital beds instead of recovering at skilled nursing facilities due to closures and staffing shortages.8 Hospital stays tend to be much more expensive than nursing home stays, and devoting resources to patients who would otherwise be in skilled nursing facilities could drive up a hospital’s wait times and reduce its capacity to provide necessary treatments to other patients. In April 2024, Massachusetts committed to spending $1 billion over the next eight years on new housing and community-support programs that could enable 2,400 or more Medicaid recipients who require less intensive medical care to move out of nursing homes.9

The LTC industry’s long-term challenges include the mismatch between Medicaid reimbursement rates and patient-related costs. In 2019, the median Medicaid reimbursement rate was 86 percent of facilities’ reported patient costs. For 29 percent of facilities, the reimbursement rate fell below 80 percent (Medicaid and CHIP Payment and Access Commission 2023). Due to the outsized role of Medicaid as the largest payer for nursing home services, this shortfall contributed, in most cases, to the operating losses that the region’s facilities experienced last year. On April 17, 2024, Maine passed a budget allowing the state to issue one-time grants totaling more than $26 million to help nursing homes cover the gaps between reimbursement rates and care costs until higher reimbursement rates take effect. The higher rates will be phased in from 2025 to 2027.10

This report’s analysis indicates that substantial changes to either how facilities operate or the level of reimbursement they receive will be necessary to stop the trend of nursing home closures. Alternatively, policymakers could innovate and expand programs that support aging in place, though such informal LTC solutions can have a negative effect on labor and housing markets. Other options may include promoting increased enrollments in LTC insurance, which may increase individuals’ ability to fund long-term care at the full cost of the services to nursing facilities, without exhausting their resources.

The views expressed herein are solely those of the author and should not be reported as representing the views of the Federal Reserve Bank of Boston, the principals of the Board of Governors, or the Federal Reserve System.

Endnotes

- See “Paying for Long-term Care,” National Institutes of Health, National Institute on Aging (accessed April 21, 2024). https://www.nia.nih.gov/health/long-term-care/paying-long-term-care

- The North Carolina Rural Health Program, which completed the analysis in Table 4 on our behalf, has found in previous studies that timing differences in recognition of PHE revenue versus PHE expenses on Medicare cost reports could distort reported profitability during the COVID-19 years. For this reason, it is important to clearly separate years without PHE funds (pre–COVID-19 years) and years with PHE funds (COVID-19 years). Therefore, the data include the profitability of nursing facilities during two pre–COVID-19 years and three COVID-19 years.

- As of the first quarter of 2023, employment in the nursing home and residential care facilities industry stood at 88.4 percent of the 2018:Q1 level for New England. It was at 81.1 percent in Rhode Island, 87.1 percent in Connecticut, 89.2 percent in Massachusetts, 90 percent in Maine, 91 percent in Vermont, and 92.9 percent in New Hampshire.

- See Antonia Noori Farzan, “RI Mandated the Highest Nursing Home Staffing in the US. Why the Governor Suspended Penalties,” Providence Journal, December 29, 2023. https://www.providencejournal.com/story/news/politics/2023/12/29/fines-suspended-indefinitely-for-rhode-island-nursing-homes-that-violate-minimum-staffing-law/72061342007/

- See Priya Chidambaram, Alice Burns, Tricia Neuman, and Robin Rudowitz, “With Current Staffing Levels, About 1 in 5 Nursing Facilities Would Meet Fully Implemented Minimum Staffing Standards in the Final Rule,” KFF, April 22, 2024. https://www.kff.org/policy-watch/nursing-facilities-staffing-levels-standards-final-rule/

- For more details, see In-Home Services, Executive Office of Elder Affairs. https://www.mass.gov/in-home-services

- For more details, see Home Modification Loan Program (HMLP), Massachusetts Rehabilitation Commission. https://www.mass.gov/home-modification-loan-program-hmlp

- See Jessica Bartless, “Over a Thousand Patients Have Been ‘Stuck’ in Hospitals Beds as Discharge Problems Persist,” Boston Globe, June 12, 2023. https://www.bostonglobe.com/2023/06/12/metro/over-thousand-patients-stuck-hospital-beds-discharge-problems-persist/

- See Jason Laughlin, “Massachusetts Commits $1 Billion to Move Thousands out of Nursing Homes in Wake of Lawsuit Settlement,” Boston Globe, April 21, 2024 https://www.bostonglobe.com/2024/04/21/metro/nursing-home-settlement-disabled-massachusetts/

- See Billy Kobin, “Maine Legislature Passes Budget Addition Again without Republican Support,” Bangor Daily News, April 17, 2024 https://www.bangordailynews.com/2024/04/17/politics/state-politics/maine-house-2-year-budget-lacks-republican-support/

Data Sources and Acknowledgments

Data on patient counts and nursing facility closures come from the Centers for Medicare and Medicaid Services (CMS). Data on profit margins come from analysis completed by Dr. George H. Pink, senior research fellow at the Cecil G. Sheps Center for Health Services Research and deputy director of the North Carolina Rural Health Research Program at the University of North Carolina at Chapel Hill. Dr. Pink’s analysis uses the CMS 2540-10 Cost Report files. We are grateful to Dr. Pink for completing this analysis for this report.

Data on industry employment come from the Quarterly Workforce Indicators (QWI). The QWI is a set of 32 economic indicators including employment, job creation/destruction, wages, hires, and other measures of employment flows.

References

Gruber, Jonathan, and Kathleen M. McGarry. 2023. “Long-term Care in the United States.” National Bureau of Economic Research Working Paper 31881.

Lilly, Meredith B., Audrey Laporte, and Peter C. Coyte. 2007. “Labor Market Work and Home Care’s Unpaid Caregivers: A Systematic Review of Labor Force Participation Rates, Predictors of Labor Market Withdrawal, and Hours of Work.” The Milbank Quarterly 85(4): 641–690.

Johnson, Richard W. 2019. “What Is the Lifetime Risk of Needing and Receiving Long-term Services and Supports?” US Department of Health and Human Services, Office of the Assistant Secretary for Planning and Evaluation. https://aspe.hhs.gov/reports/what-lifetime-risk-needing-receiving-long-term-services-supports-0

Medicaid and CHIP Payment and Access Commission. 2023. “Estimates of Medicaid Nursing Facility Payments Relative to Cost.” MACPAC Issue Brief. January. https://www.macpac.gov/wp-content/uploads/2023/01/Estimates-of-Medicaid-Nursing-Facility-Payments-Relative-to-Costs-1-6-23.pdf

Ochieng, Nancy, Jeannie Fuglesten Biniek, Mary Beth Musumei, and Tricia Neuman. 2022. “Funding for Health Care Providers during the Pandemic: An Update.” KFF. https://www.kff.org/coronavirus-covid-19/issue-brief/funding-for-health-care-providers-during-the-pandemic-an-update/

About the Authors

About the Authors

Riley Sullivan,

Federal Reserve Bank of Boston

Riley Sullivan is a senior policy analyst with the New England Public Policy Center in the Federal Reserve Bank of Boston Research Department.

Email: riley.sullivan@bos.frb.org

Resources

Keywords

- New England ,

- NEPPC Regional Brief ,

- nursing homes ,

- long-term care ,

- Medicaid ,

- Labor markets