Credit Card Delinquencies: Are New England Consumers Better Off?

{kind=link}

Federal Reserve Bank of Boston

The views expressed herein are solely those of the author and should not be reported as representing the views of the Federal Reserve Bank of Boston, the principals of the Board of Governors, or the Federal Reserve System.

Credit card spending and borrowing in the United States declined rapidly at the start of the COVID-19 pandemic in 2020. As a result, credit card revolving (carrying debt) and credit card delinquencies (loans at least 30 days past due) declined shortly thereafter. Those trends reversed in early 2021, when US consumers started to increase their credit card borrowing and credit card default rates rose again (Stavins 2023).

Even though credit card transactions constitute only about one-third of the total number of consumer transactions (Foster, Greene, and Stavins 2024), credit cards are the only payment method that allows cardholders to take unsecured loans. Borrowing on credit cards is very common; nearly half of US cardholders revolve credit card debt. Among cardholders who revolve, the average debt combined across all their credit card accounts is $6,481, and the median is $3,000.1 Therefore, credit card borrowing, particularly delinquent credit card loans, provides an important signal that consumers may be experiencing financial stress.

Sign up for new research and data on the New England economy.

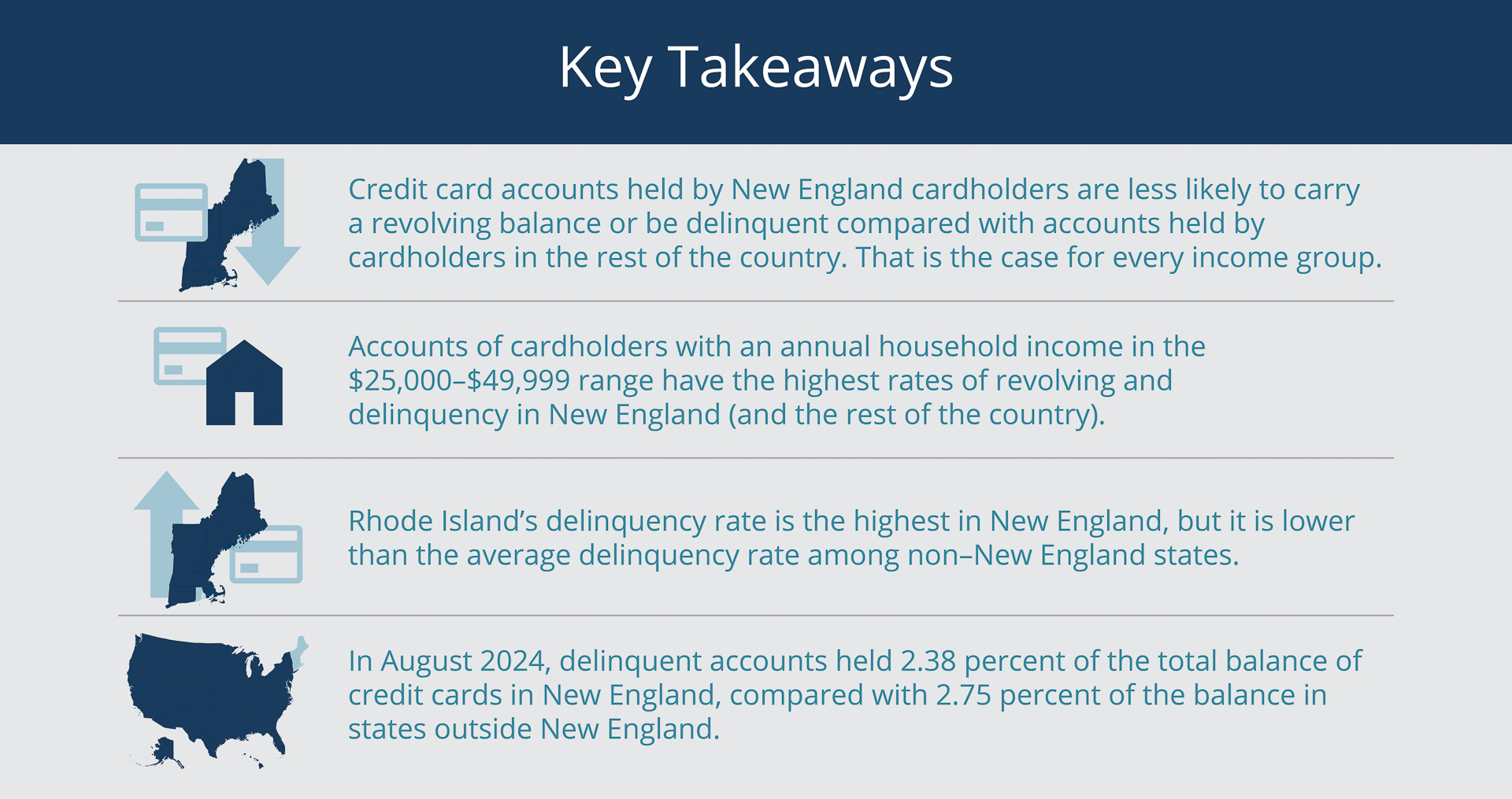

This Regional Brief looks at how credit card spending and borrowing in New England and in each of the region’s states in recent years compare with such consumer behavior in the rest of the country. It finds that in general, New England consumers are better off than those living in other regions: They are more likely to have credit cards, they use credit cards more intensively, and they are less likely to revolve, which is consistent with New Englanders, on average, being wealthier and more educated than other US residents.2

In addition, the share of New England credit card accounts that are delinquent is slightly smaller relative to the rest of the country, and although Rhode Island and Connecticut have higher rates of delinquent accounts compared with other New England states, particularly among lower-income cardholders, those rates are lower than the average among states outside the region.

Less Than One-Third of New England Credit Cardholders Revolve Debt

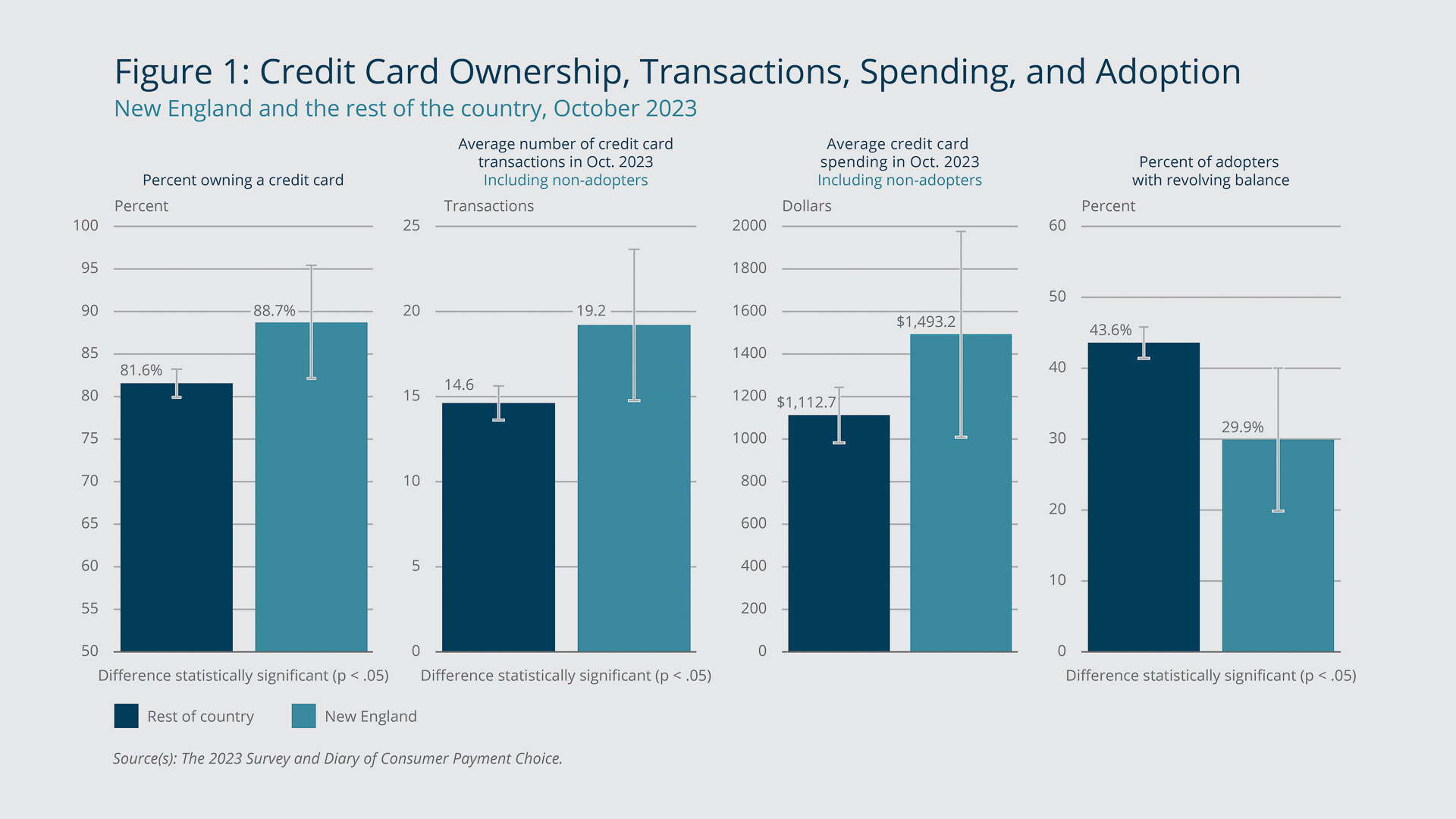

According to data collected from the Survey and Diary of Consumer Payment Choice (SDCPC) in October 2023,3 about 89 percent of New Englanders owned at least one credit card, compared with less than 82 percent of consumers outside the region (Figure 1). On average, New England consumers conducted 19 credit card transactions in a month, charging a total of $1,500, compared with fewer than 15 transactions and about $1,100 for non–New Englanders. Among credit cardholders in New England, only 30 percent revolved their credit card debt, compared with 44 percent outside the region.

{kind=link}

Federal Reserve Bank of Boston

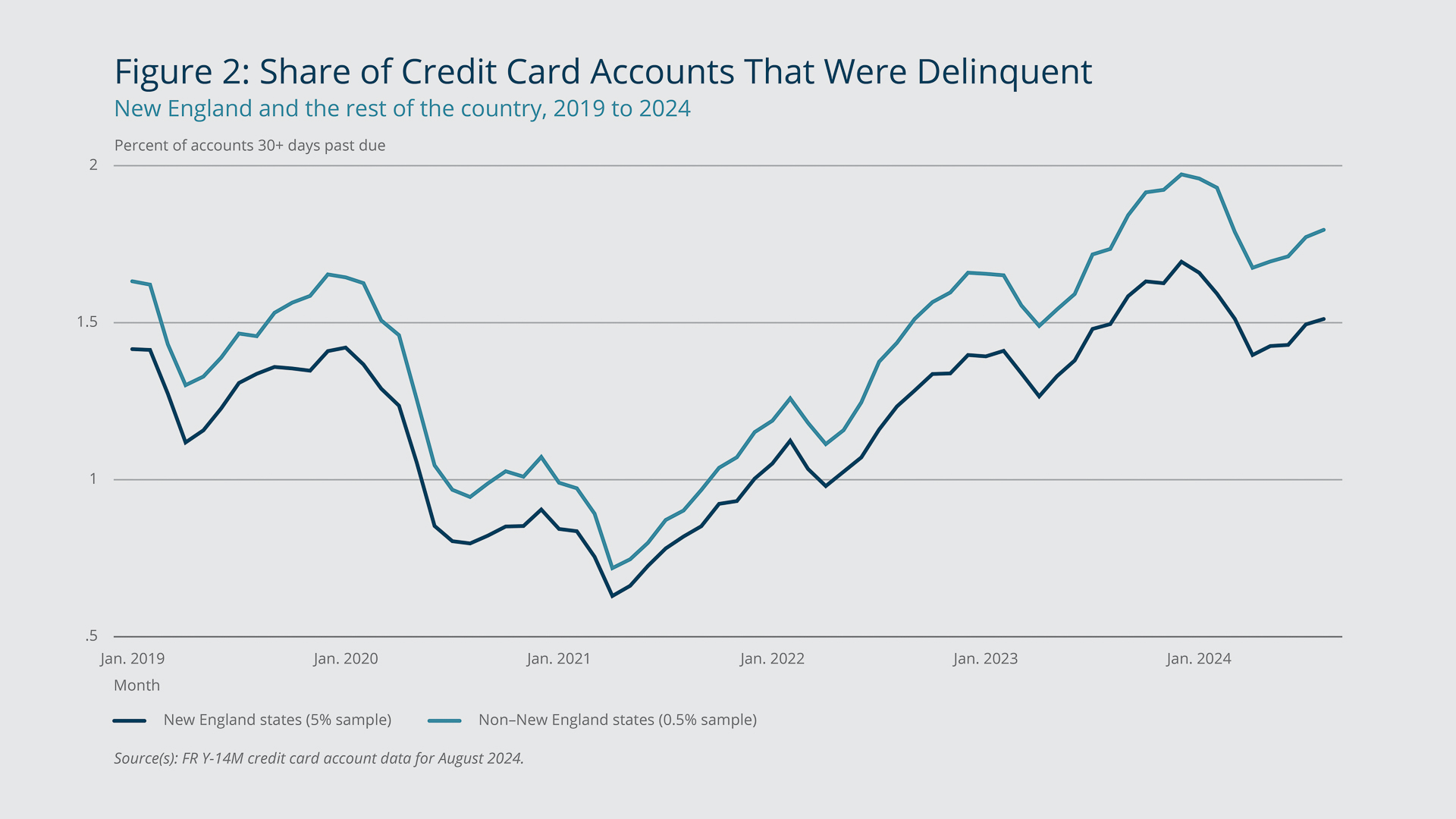

Each month, the Federal Reserve Board collects what are known as FR Y-14M data from bank holding companies (BHCs) to use in supervisory capital assessments and stress testing.4 The data include information on all the credit card accounts that the BHCs have on file. TheFR Y-14M data for August 2024 show that the share of credit card accounts that were delinquent was slightly smaller in New England than in the rest of the country (Figure 2). The gap has persisted since before the COVID-19 pandemic, although it increased somewhat over the last two years. The trend in New England is very similar to the trend outside the region (as indicated by the nearly parallel lines in Figure 2), with credit card delinquencies declining in 2020 and starting to rise again in April 2021.

{kind=link}

Federal Reserve Bank of Boston

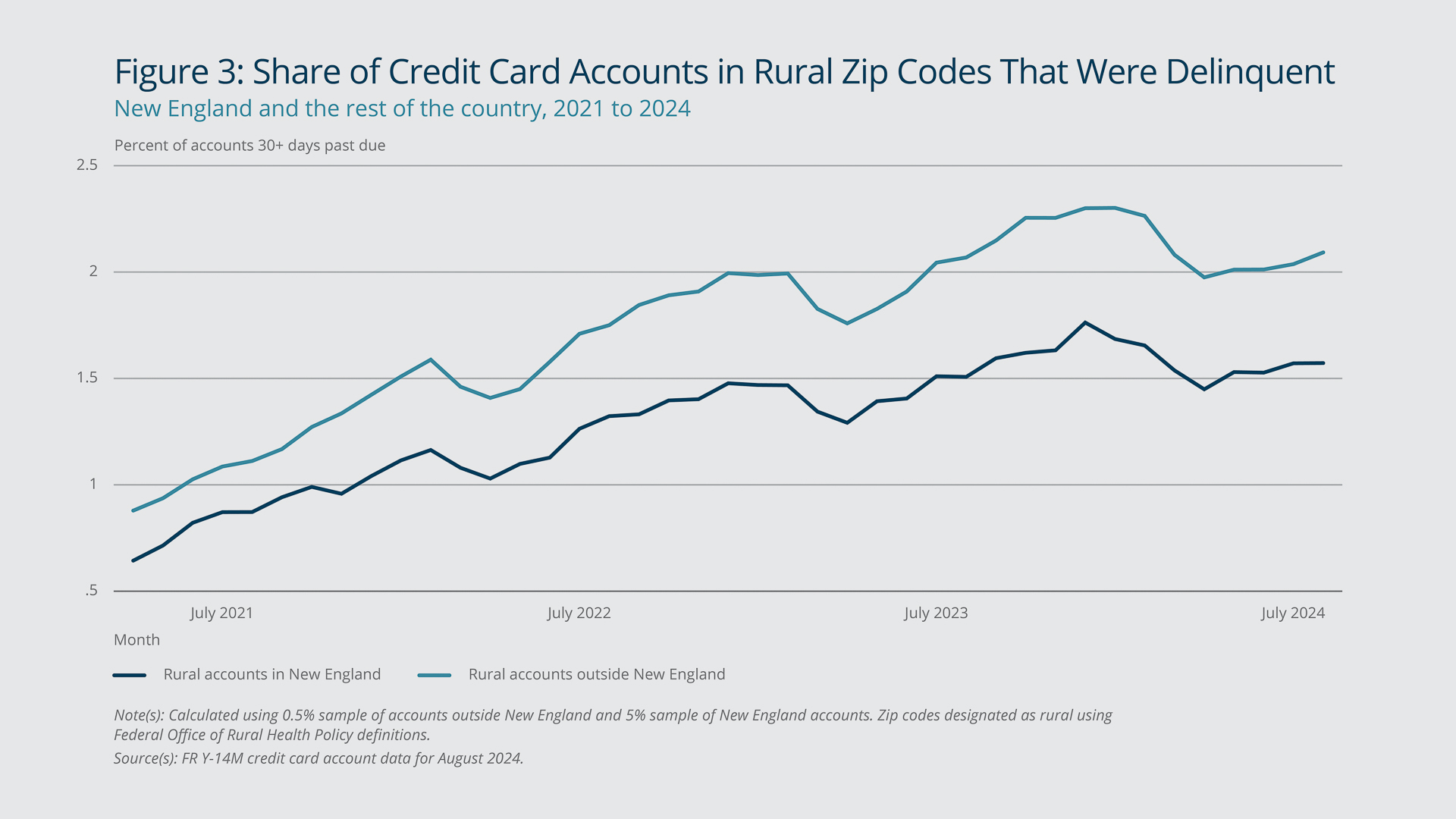

The delinquency gap between rural5 accounts in New England and rural accounts in the rest of the country is similar to the overall delinquency gap between New England and the rest of the country (Figure 3). In other words, the gap persists regardless of whether we compare accounts in all Zip codes, only rural Zip codes, or only nonrural Zip codes. In New England, accounts in rural and nonrural Zip codes have similar delinquency rates, but spending levels are lower for rural accounts.

{kind=link}

Federal Reserve Bank of Boston

Lower-income Consumers Experience More Financial Stress

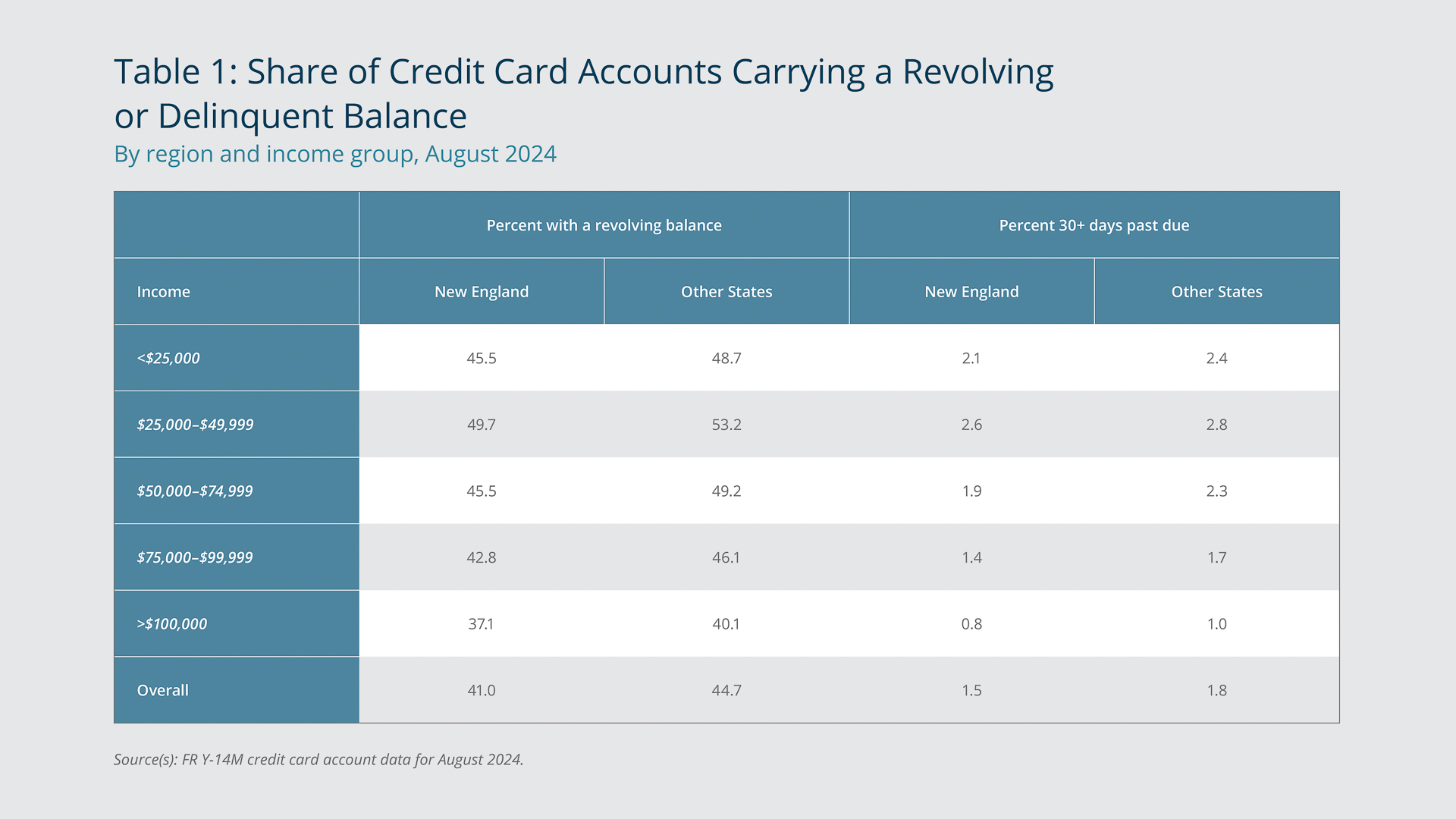

Whereas Figure 1 shows the shares of consumers who have a revolving balance, based on a self-reported consumer survey (the SDCPC), Table 1 shows the percentage of credit card accounts with a revolving balance and the percentage of accounts that are delinquent, in New England and outside New England, by income group. Overall, New England has a smaller share of accounts with a revolving balance (41.0 percent versus 44.7 percent as of August 2024) and a smaller share of accounts that are delinquent compared with the rest of the country (1.5 percent versus 1.8 percent). The New England shares also are smaller for every income group.

{kind=link}

Federal Reserve Bank of Boston

Nevertheless, in the region—and the rest of the country—lower-income cardholders appear to be experiencing more financial stress relative to other income groups. As Table 1 shows, their delinquency and revolving rates are higher than those of cardholders in higher income groups. Accounts of cardholders with an annual household income in the $25,000–$49,999 range have the highest rates of revolving and delinquency, and the average balance on delinquent cards is slightly higher in New England than in the rest of the country.

In addition, the average balance on delinquent accounts has risen much faster for accounts held by lower-income cardholders. This is consistent with lower-income consumers depleting the excess savings accumulated early in the pandemic faster than other consumers.

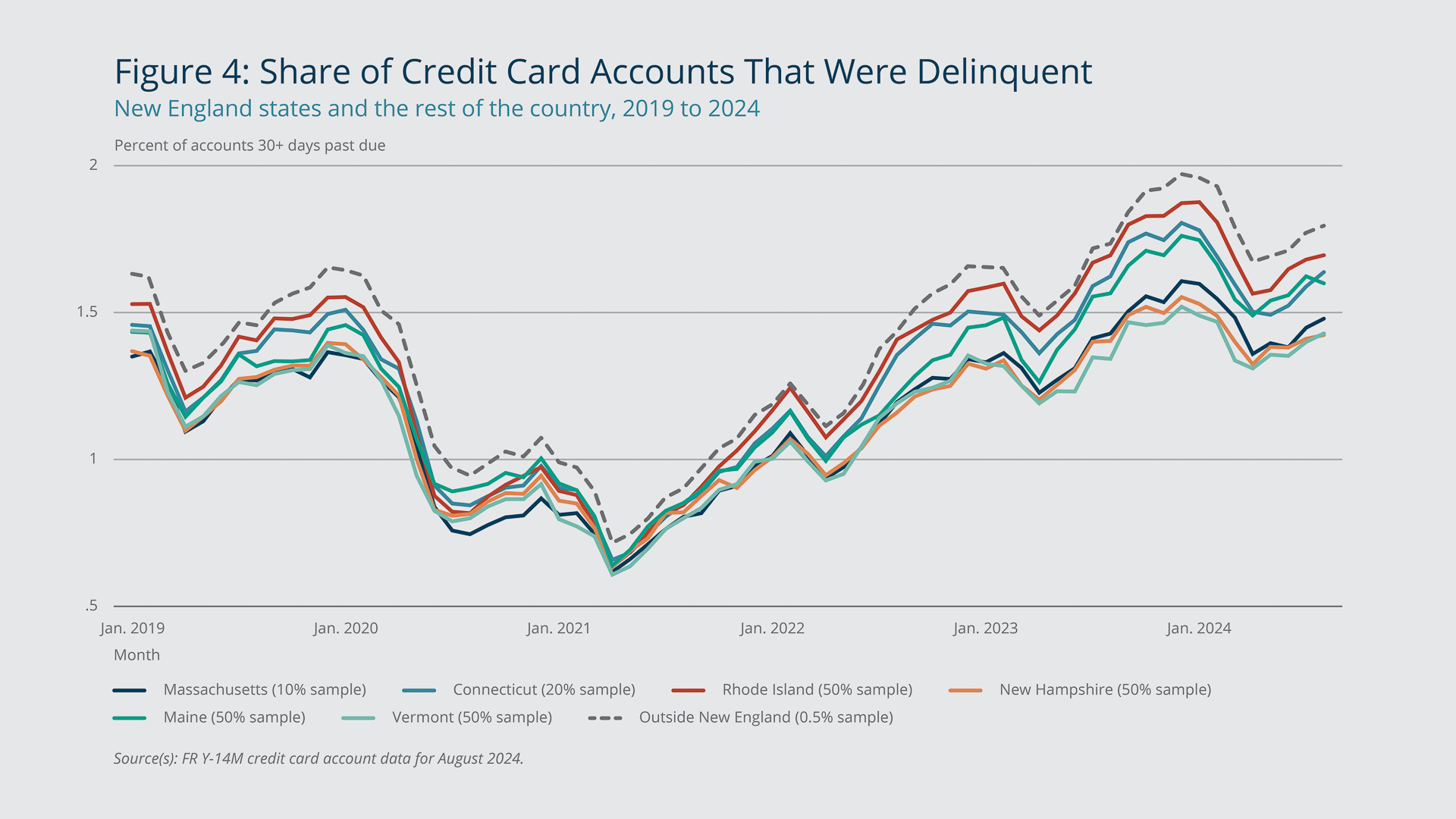

States’ Delinquency Rates Are Similar, but They Have Diverged

Delinquency rates are similar across the six New England states (Figure 4), though not as similar as they were in March 2021, when each reached its lowest point in the observable data (which begin in 2015). Since mid-2022, Rhode Island, Connecticut, and Maine have had higher delinquency rates than Massachusetts, New Hampshire, and Vermont. However, as the dashed line in Figure 4 shows, even Rhode Island—the state with the highest delinquency rate in the region—has had a delinquency rate that is lower than the average for non–New England states.

{kind=link}

Federal Reserve Bank of Boston

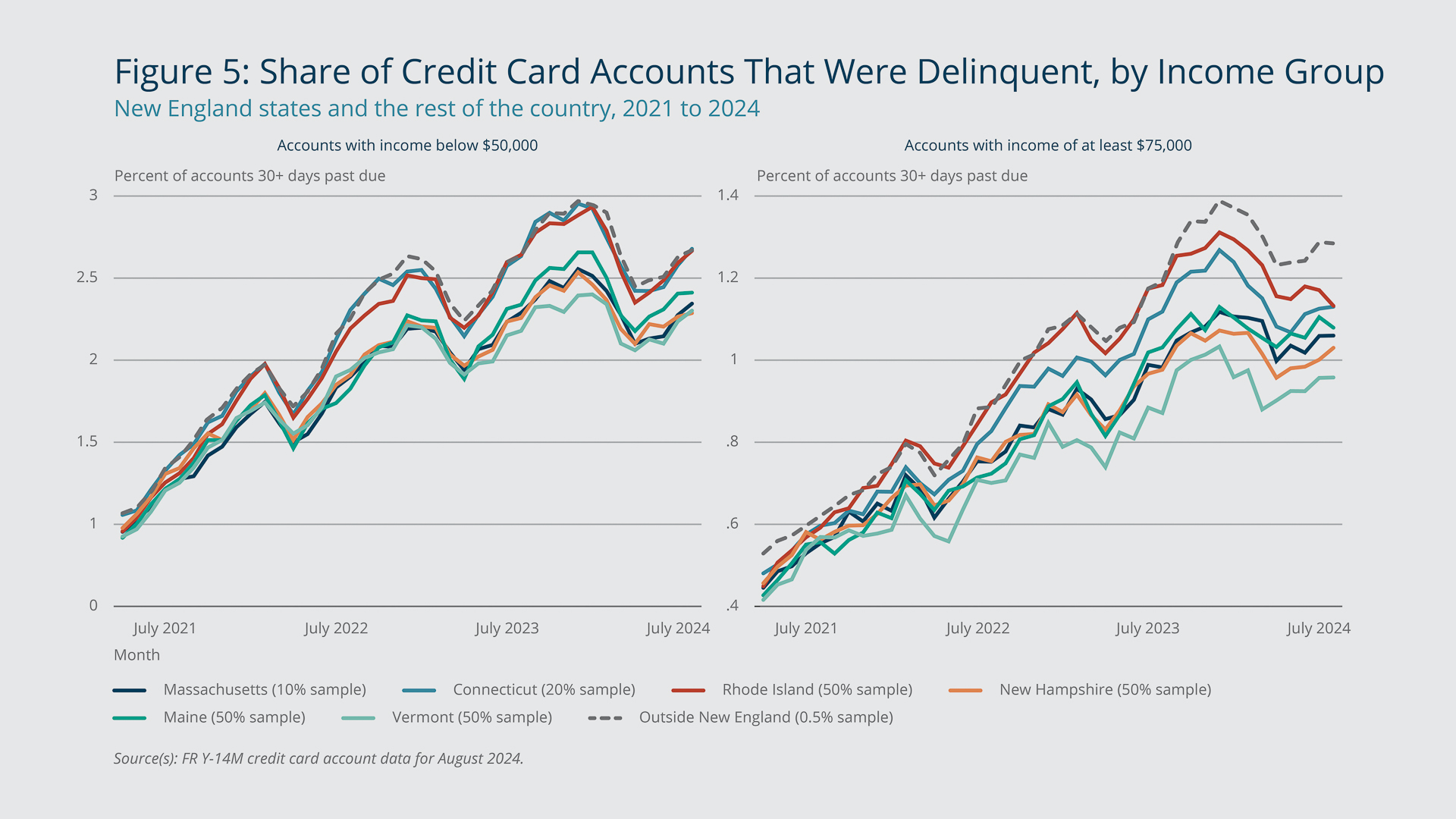

The gaps between the delinquency rates for Rhode Island and Connecticut and the rates for the other New England states are especially pronounced for cardholders with annual household income of less than $50,000, but they are also apparent for cardholders with annual household income of more than $75,000 (Figure 5). Although Rhode Island, Connecticut, and Maine have higher delinquency rates compared with the rest of the region, delinquent cardholders living in those states have, on average, a slightly lower cycle-ending balance compared with delinquent cardholders living in Massachusetts, New Hampshire, or Vermont.

{kind=link}

Federal Reserve Bank of Boston

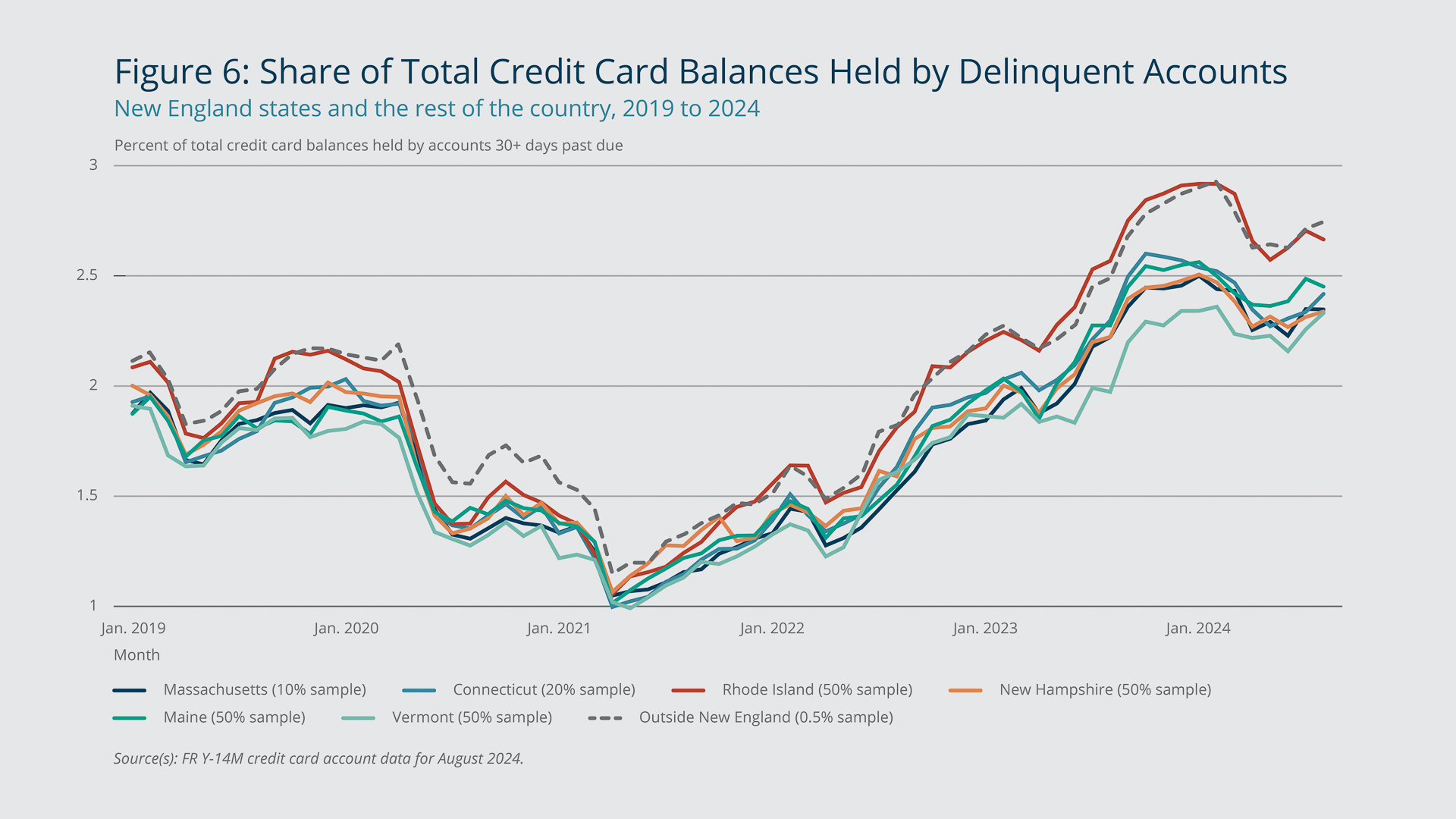

In addition to looking at the rates of delinquency and the average balances on delinquent accounts, we compare total delinquent balances across New England states. Total delinquent balances are calculated by adding the outstanding balances on all delinquent accounts in the sample. The amounts differ substantially across states partly because total credit card balances differ substantially. Therefore, Figure 6 presents total delinquent balances as a share of total credit card balances.

{kind=link}

Federal Reserve Bank of Boston

The figure shows, for each New England state and for non–New England states, the percentage of total credit card account balances held by delinquent accounts. The shares of total balances that are delinquent has changed over time at similar rates across the states, although they have been largest in Rhode Island, especially in 2023 and 2024. As of August 2024, delinquent accounts held 2.38 percent of the total balance of credit cards in New England, compared with 2.75 percent of the balance in states outside the region, another sign that New England credit cardholders are doing better than cardholders in the rest of the country.

Endnotes

- These estimates are per person and are based on self-reported balances from the 2023 Survey and Diary of Consumer Payment Choice (see endnote 3), with nationally representative weights. In the FR Y-14M credit card account data (see endnote 4), the average revolving balance per account (among cards with a positive revolving balance) was $3,083 in October 2023, and the median was $1,495.

- The average per capita personal income in New England in 2023 was $84,340, compared with $69,815 nationwide. See FRED Economic Data, Federal Reserve Bank of St. Louis, “Per Capita Personal Income in the New England BEA Region” (accessed November 15, 2024), https://fred.stlouisfed.org/series/BEANEPCPI, and FRED Economic Data, Federal Reserve Bank of St. Louis, “Personal Income Per Capita” (accessed November 15, 2024), https://fred.stlouisfed.org/series/A792RC0A052NBEA, respectively. Educational attainment in New England is higher than in the other US regions (US Census Bureau 2023).

- The SDCPC is a representative survey of US adults (aged 18 and older) conducted annually by the Federal Reserve Banks of Atlanta and Boston and Federal Reserve Financial Services. See Foster, Greene, and Stavins (2024) for details about the data.

- The Federal Reserve Board collects FR Y-14M data monthly from BHCs with total consolidated assets of $100 billion or more. BHCs are required to report information on all their credit card accounts. The accounts reported in the FR Y-14M data represent about three-quarters of the total bank credit card balances in the United States.

- We classify an account as rural if the Zip code of the account holder is defined as such by the Federal Office of Rural Health Policy; for details, see Health Resources and Services Administration, Federal Office of Rural Health Policy Data Files (accessed November 15, 2024), https://www.hrsa.gov/rural-health/about-us/what-is-rural/data-files. In August 2024, 13.5 percent of FR Y-14M accounts held by consumers outside New England were classified as rural, compared with 12.0 percent of accounts in New England.

References

Foster, Kevin, Claire Greene, and Joanna Stavins. 2024. “2023 Survey and Diary of Consumer Payment Choice: Summary Results.” Federal Reserve Bank of Atlanta Research Data Report No. 24-1.

Stavins, Joanna. 2023. “Credit Card Spending and Borrowing since the Start of the COVID-19 Pandemic.” Federal Reserve Bank of Boston Current Policy Perspectives.

US Census Bureau, U.S. Department of Commerce. 2023. “Educational Attainment,” American Community Survey, ACS 1-Year Estimates Subject Tables, Table S1501, 2023. Accessed November 5, 2024.

About the Authors

About the Authors

Joanna Stavins,

Federal Reserve Bank of Boston

Joanna Stavins is a former principal economist and policy advisor in the Federal Reserve Bank of Boston Research Department.

Acknowledgments

Resources

Keywords

- New England ,

- NEPPC Regional Brief ,

- credit card borrowing ,

- credit card delinquencies ,

- credit card revolving