The Color of Wealth in Boston

A Joint Publication of Duke University, The New School, and the Federal Reserve Bank of Boston

Ken Dubrowski

{kind=link}

The widening wealth gap in the United States is a worrisome sign that millions of families nationwide do not have enough in assets to offer better opportunities for future generations. Wealth allows families to make investments in homes, in education, and in business creation. On the basis of data collected using the National Asset Scorecard for Communities of Color (NASCC) survey, we report that, when analyzed by race, wealth accumulation is vastly unequal. By means of the NASCC survey, researchers have collected, for the first time, detailed data on assets and debts among subpopulations, according to race, ethnicity, and country of origin—granular detail ordinarily unavailable in public datasets. In this analysis we focus on estimates for U.S. born blacks, Caribbean blacks, Cape Verdeans, Puerto Ricans, and Dominicans in the Boston Metropolitan Statistical Area (MSA). Our analysis shows that with respect to types and size of assets and debt held, the data collected on white households and nonwhite households exhibit large differences. The result is that the net worth of whites as compared with nonwhites is staggeringly divergent.

Key Findings

- The typical white household in Boston is more likely than nonwhite households to own every type of liquid asset. For example, close to half of Puerto Ricans and a quarter of U.S. blacks don't have either a savings or checking account, compared to only 7% of whites.

- Whites and nonwhites also exhibit important differences in assets that associated with homeownership, basic transportation, and retirement. Close to 80% of whites own a home, whereas only one-third of U.S. blacks, less than one-fifth of Dominicans and Puerto Ricans, and only half of Caribbean blacks are homeowners. And while most white households (56 percent) own retirement accounts, only one-fifth of U.S and Caribbean blacks, and 8 percent of Dominicans have them.

- Although members of communities of color are less likely to own homes, among homeowners they are more likely to have mortgage debt. Nonwhite households are more likely than whites to have student loans and medical debt.

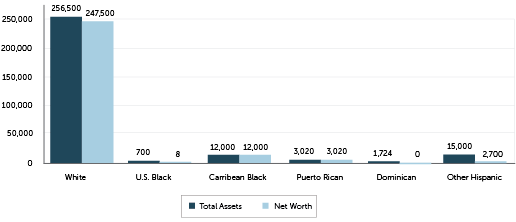

- Nonwhite households have only a fraction of the net worth attributed to white households. While white households have a median wealth of $247,500, Dominicans and U.S. blacks have a median wealth of close to zero. Of all nonwhite groups for which estimates could be made, Caribbean black households have the highest median wealth with $12,000, which is only 5 percent of the wealth attributed to white households in the Boston MSA.

Exhibit

{kind=link}

Implications

Population growth in the Boston MSA is already driven by the nonwhite population increase. Thus, the financial well-being of communities of color is central to ensuring the inclusive long-term growth and prosperity of the Boston MSA. Unless net worth outcomes in communities of color improve, the aggregate magnitude of the wealth disparity will increase. This is a first-order public policy problem requiring immediate attention. Policies aimed at bridging the wealth gap should also consider the wide diversity among nonwhite populations and be targeted or adapted accordingly. Policy solutions are complex and need to use a multifaceted approach that includes input from practitioners who are familiar with the unique needs and challenges different communities of color face.

About the Authors

About the Authors

Ana Patricia Muñoz

Marlene Kim

Mariko Chang

Regine O. Jackson

Darrick Hamilton

William A. Darity Jr.

Resources

Site Topics

Keywords

- financial wealth