2014 • No. 14–3

Research Data Reports

U.S. Consumers' Holdings and Use of $100 Bills

Conventional wisdom asserts that $100 bills are often associated with crime and foreign cash holdings, leading some commentators to call for their elimination; in light of this proposal, it is useful to examine the legal, domestic use of cash. This report uses new data from the 2012 Diary of Consumer Payment Choice (DCPC) to evaluate consumer use of $100 bills as a means of payment.

Key Findings

Key Findings

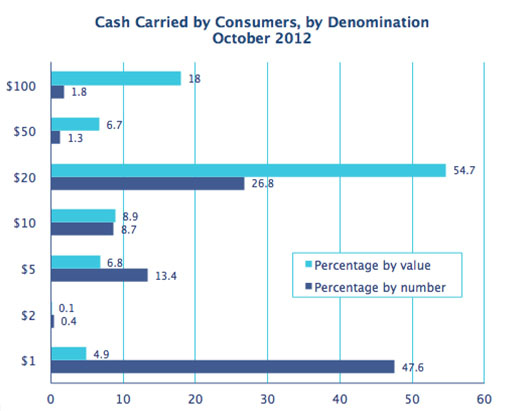

- More than one in five U.S. consumers carries more than $100 in cash in his or her pocket, purse, or wallet, and the more cash the consumer carries the more likely he or she is to carry $100 bills. Consumers may have $100 bills stored on their property as well, but data are not available on this aspect of consumer cash use.

- People who carry $100 bills tend to hold them for a while. On any given day, between 75 percent and 80 percent of respondents to the 2012 DCPC who carried a $100 bill held on to it. There does not appear to be evidence that consumers try to get rid of $100 bills.

- By number of transactions, consumers with $100 bills do not make relatively more payments in cash than consumers with more than $100 in mixed bills, as reported in the 2012 DCPC. Thus, $100 bills do not appear to be more special than other currency denominations as a means of payment; rather, some consumers appear to have a stronger preference than other consumers for $100 bills.

- By value of cash payment, people who carry $100 bills make larger-value cash payments than people who carry more than $100 in mixed bills. Thus, $100 bills appear to help some consumers who prefer to pay in cash make larger cash payments more conveniently.

- Nevertheless, most cash payments are for less than $100, so people are receiving change from their $100 bills. And, for payments of $100 or more, 15.8 percent of purchases were paid in cash, while just 3 percent of bills were paid in cash. So, based on these data, it appears that most consumer payments greater than $100 in value are made using noncash means of payment. Thus, the need for a denomination as large as a $100 bill appears to be modest in the big picture of consumer payments.

Exhibits

Implications

Taken together, these results suggest that cash-intensive consumers place some value on carrying $100 bills for reasons that merit further investigation. Therefore, the largest U.S. currency denomination in circulation today may have value as a means of payment and may be worth retaining in circulation, at least in the United States. Despite the $100 bill's decline in purchasing power since 1969, U.S. consumers do not appear to be demonstrating a need for larger denominations.

Abstract

Conventional wisdom asserts that $100 bills are often associated with crime and foreign cash holdings, leading some commentators to call for their elimination; in light of this view, it is useful to examine the legal, domestic use of cash. This report uses new data from the 2012 Diary of Consumer Payment Choice (DCPC) to evaluate consumer use of $100 bills as a means of payment. On a typical day in the United States, 5.2 percent of consumers have a $100 bill in their pocket, purse, or wallet. But only 22 percent of U.S. consumers have at least $100 in their wallet, pocket, or purse. Of these cash-intensive consumers, the main association with holding a $100 bill is the amount of cash carried. A consumer who carries $400 to $699 has a 64 percent probability of carrying at least one $100 bill.