2015 Series • No. 15–16

Research Department Working Papers

Exchange Rates and Monetary Policy

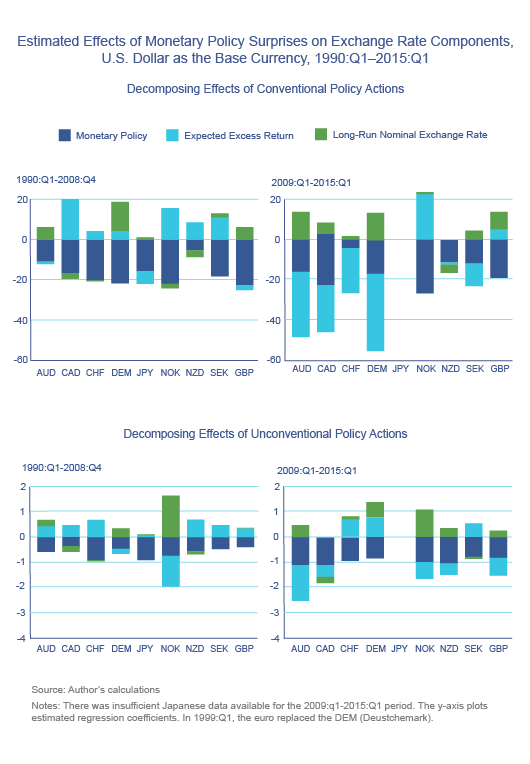

Financial markets regard exchange rate movements as conveying information about future expected policy rates. This paper explores the empirical link between conventional and unconventional monetary policy surprises and exchange rate fluctuations at a quarterly frequency. It examines these links using the currencies of ten developed economies calculated against four base currencies: the U.S. dollar, the British pound, the Deutschmark/euro, and the Japanese yen. Two periods are studied: 1990:Q1–2008:Q4, when the U.S. dollar hit the zero lower bound (ZLB) in December 2008, and the ZLB period between 2009:Q1 and 2015:Q1. The authors decompose exchange rate movements using a standard no-arbitrage asset pricing equation and two alternate interest rate forecasting models—a standard Taylor rule and a yield factor model. This decomposition reveals how contemporaneous unanticipated monetary policy surprises and changes in the expected future paths of policy are linked to exchange rate changes directly through relative interest rates as well as indirectly through expected excess returns and expected long-run exchange rate levels. The authors also use this decomposition to measure the fractions of the estimated effects of conventional and unconventional monetary policy surprises on exchange rate changes that are due to each component of the exchange rate change.

Key Findings

Key Findings

- Monetary policy can explain a sizable fraction of the volatility of exchange rate changes for some currency pairs, primarily the ones for which the British pound serves as the base currency.

- Changes in expectations over long-run nominal exchange rates and lagged relative interest rates play negligible roles in these movements.

- Variation in current and future expected excess returns, which capture currency risk premia and financial frictions, account for most of the fluctuations in exchange rate changes.

- The overall importance of contemporaneous monetary policy surprises for explaining exchange rate volatility decreased after the U.S. dollar hit the ZLB - despite the fact that the correlation between exchange rate changes and relative monetary policy surprises became stronger during this period. A lower variance of relative monetary policy surprises over this period reconciles these two facts, a result that is consistent with interest rate policy being infeasible and a heavier reliance on quantitative easing and forward guidance.

Exhibits

Implications

The paper's results confirm the financial-market folk wisdom which holds that a country's currency tends to appreciate when there are higher current and expected future monetary policy rates in that country relative to others. Prior to the ZLB period, the dynamics of expected excess returns dampened the effect of monetary policy, but during the ZLB period, the dynamics of expected excess returns now amplify the effect of monetary policy for most major currency pairs . As a result, a surprise increase in a country's short-term interest rate relative to that of other countries now tends to be associated with a larger appreciation of that country's currency.

Abstract

In this paper we confront the data with the financial -market folk wisdom that monetary policy is one of the key drivers of nominal exchange rates. Focusing on measures of conventional and unconventional monetary policy, we find that monetary policy surprises and changes in expectations about future monetary policy can explain a sizable fraction of the variation in exchange rate changes for certain currency pairs. However, our results show that expected excess returns account for most of this variation. We also find that the importance unconventional onetary policy plays for explaining exchange rate changes is larger in the period since the United States hit the zero lower bound in December 2008. In contrast, the importance of conventional monetary policy is lower during this period due to a decrease in the volatility of monetary policy surprises. Meanwhile, the marginal response of exchange rate changes relative to conventional policy surprises actually has trengthened due to a change in the relationship between these surprises and expected excess returns.