The Federal Reserve's Main Street Lending Program

Business loans to help eligible small and medium-sized for-profit businesses and nonprofit organizations through the COVID-19 pandemic.

{kind=link}

What it is

The program was designed to help credit flow to small and medium-sized for-profit businesses and nonprofit organizations that were in sound financial condition before the onset of the COVID-19 crisis, but needed loans to help maintain their operations until they recovered from, or adapted to, the impacts of the pandemic.

Loans originated under the program had several features that will help borrowers facing challenges. The program offered 5-year loans, with floating rates, and principal and interest payments deferred as indicated in the charts below to assist those experiencing temporary cash flow interruptions.

To support a broad set of employers, loan size started at $100,000 and ranged up to $300 million for some loan types.

What it isn't

Main Street loans are not grants and cannot be forgiven.

How it works

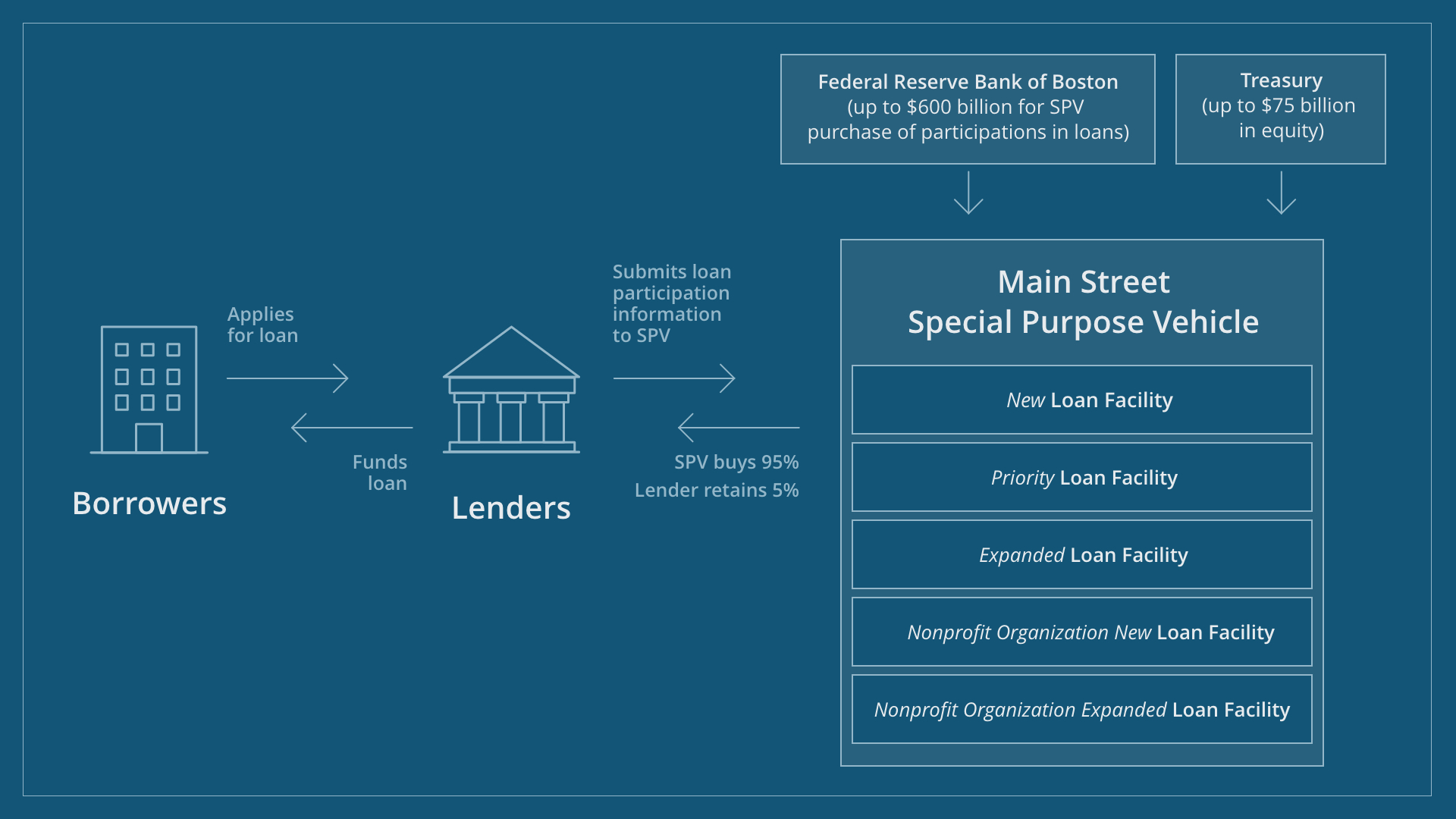

To assist a broad range of borrowers, the program offered three different for-profit business loan types, and two types of loans for nonprofits, each with somewhat different characteristics – as indicated in the charts. Refer to the diagram at the end of the document for a schematic on how the program worked.

| Characteristics of Main Street For-Profit Business Loan Types | |||

| New Loan Facility | Priority Loan Facility | Expanded Loan Facility | |

| Loan Term | 5 years | ||

| Principal Payments | Principal deferred for two years. Years 3-5: 15%, 15%, 70% | ||

| Interest Payments | Deferred for one year | ||

| Interest Rate | LIBOR + 3% | ||

| Loan Size | $100,000 to $35 million |

$100,000 to $50 million |

$10 million to $300 million |

| Maximum Combined Debt to Adjusted 2019 EBITDA | 4 times | 6 times | 6 times |

| Lender Participation Rate | 5% | ||

| Fed Participation Rate | 95% | ||

| Prepayment Allowed | Yes, without penalty | ||

| Business Size Limits | 15,000 employees or fewer, or 2019 revenues of $5 billion or less | ||

| Fees | Origination and transaction fees may apply | ||

| Characteristics of Main Street Nonprofit Organization Loan Types | ||

| Nonprofit New Loans | Nonprofit Expanded Loans | |

| Loan Term | 5 years | |

| Minimum Loan Size | $100,000 | $10 million |

| Endowment Cap | $3 billion | |

| Years in Operation | At least 5 years | |

| Eligibility Criteria (See Term Sheets for More Detail) |

|

|

| Maximum Loan Size | The lesser of $35 million, or the borrower’s average 2019 quarterly revenue | The lesser of $300 million, or the borrower’s average 2019 quarterly revenue |

| Risk Retention | 5% | |

| Principal Repayment | Principal deferred for two years; years 3-5: 15%, 15%, 70% | |

| Interest Payments | Deferred for one year | |

| Interest Rate | LIBOR + 3% | |

Other resources

The Main Street program aimed to assist entities that employ a major share of the American workforce. For smaller businesses, it may be useful to consult the Small Business Administration’s Coronavirus Small Business Guidance & Loan Resources and the Treasury’s Community Development Financial Institutions Fund - Tools and Resources, which has a list of current certified CDFIs, many of which make loans to small businesses and provide technical assistance.*

Administration

The Main Street Lending Program is administered by the Federal Reserve Bank of Boston, which established a special purpose vehicle to purchase loan participations from eligible lenders across the U.S.

{kind=link}

Federal Reserve Bank of Boston

*Please note, information about these lenders is provided as a convenience and for informational purposes only. This does not constitute an endorsement or an approval by the Federal Reserve Bank of Boston or Federal Reserve System.