New report: Main Street added substantially to credit supply to small and medium-sized borrowers

Most of Boston Fed–run program’s 1,830 loans went to smaller firms impacted by the pandemic

{kind=link}

The Main Street Lending Program was intended to foster the flow of credit to small and medium-sized businesses and nonprofit organizations so that they could continue to operate during the COVID-19 outbreak. The program was conceived early in the pandemic, when states were imposing closures, businesses were drawing down their credit lines, and the credit market was growing ever tighter. According to a new report from the Federal Reserve Bank of Boston and the Board of Governors of the Federal Reserve System, Main Street successfully served its purpose, especially with respect to smaller businesses, even though the program used only a small fraction – $17.5 billion – of its capacity to facilitate $600 billion in loans.

“Uptake of the Main Street Lending Program,” by Boston Fed Senior Economist and Policy Advisor Falk Bräuning and Board of Governors Principal Economist Teodora Paligorova, notes that Main Street's 1,830 loans went to 2,453 borrowers, 99% of which were smaller businesses; that is, they reported an EBIDTA of less than $50 million in 2019. (EBITDA stands for earnings before interest, taxes, depreciation, and amortization.) These loans were generally concentrated among the industries hurt most by the COVID-19 pandemic: accommodation and food services; manufacturing; real estate and rental and leasing; and mining, oil and gas extraction.

In fact, more than 70% of all Main Street lending went to COVID-19–affected industries, and the loans tended to support businesses in locations that were particularly hard-hit by the pandemic. The authors show that Main Street uptake by state in any month was positively correlated with the state’s COVID-19 testing positivity rate in the preceding month.

“We find that a range of different borrowers used the program, with disproportionate uptake by firms that faced pandemic-related business disruptions,” the authors write.

Main Street, which the Boston Fed operated from July 6, 2020, to Jan. 8, 2021, made loans available to borrowers with as many as 15,000 employees or up to $5 billion in annual revenue. The program could purchase 95% of a loan from the lending bank, with the bank retaining the remaining 5% of the balance. Different loan types were available, and the maximum loan amounts available depended on, among other factors, the financial condition of the business at the end of 2019, as measured by its adjusted debt-to-EBITDA ratio (adjusted to account for extraordinary expenses, for example). The adjusted debt-to-EBITDA ratio is also known as the leverage ratio.

Depending on the size and type of loan, Main Street’s leverage ratio limit was either 4 or 6, meaning a borrower could have a maximum of four or six times as much debt to earnings. That may explain why the program did not facilitate more loans than it did: The criteria may have been too strict for firms that otherwise would have obtained a loan through the program. “A large share of participating firms’ loans were constrained by the program’s maximum leverage ratio(s)…rather than by the unconditional maximum loan size limit or the maximum firm size limit, suggestive of unmet credit demand from small firms,” the authors write.

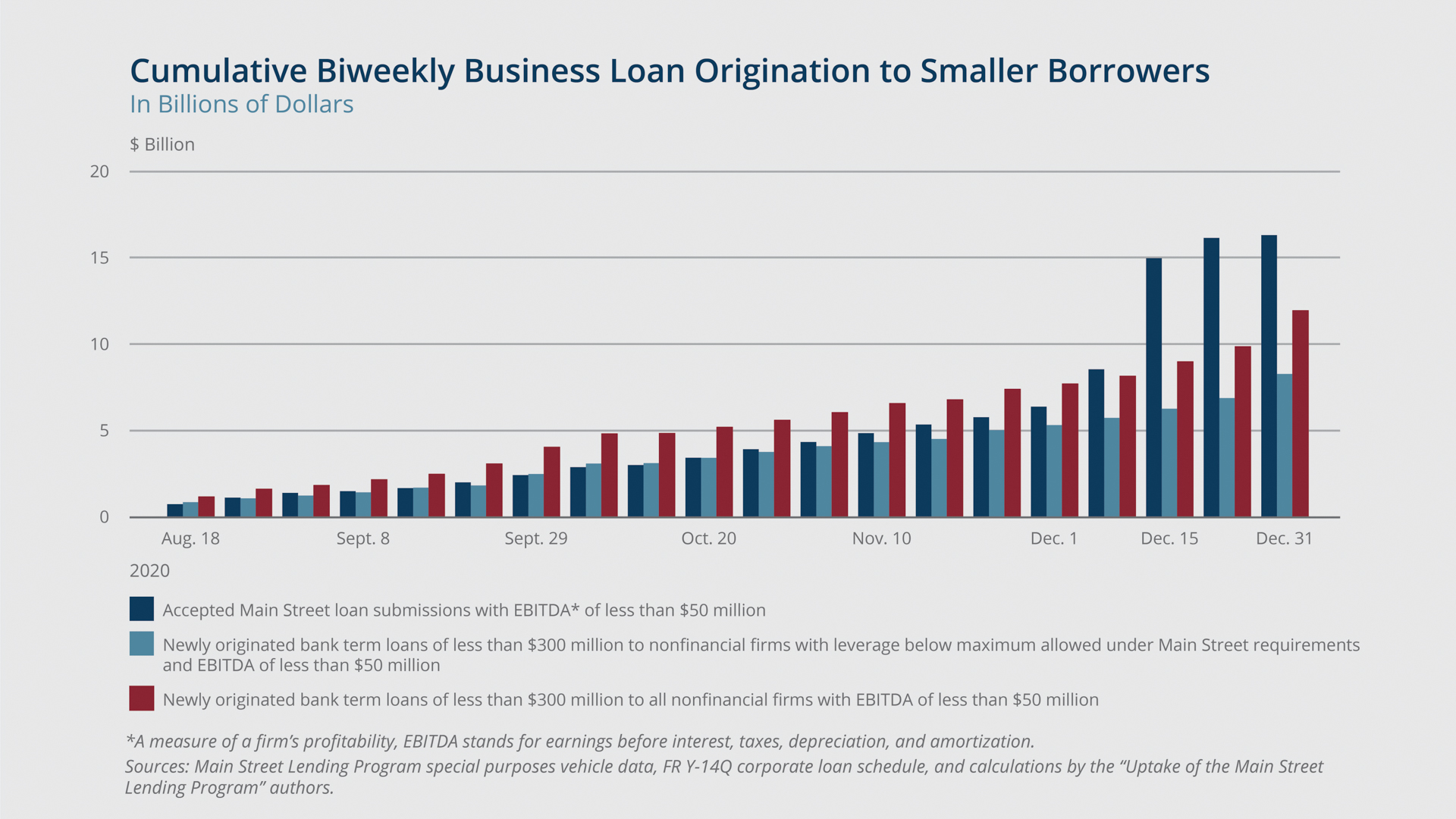

The authors compare lending through Main Street with the volume of loans originated by large banks that were not sold to the program but did meet its main qualifying criteria. These were term loans for less than $300 million obtained by nonfinancial firms with a leverage ratio of less than 6. The authors find that by the end of December 2020, the total Main Street volume had risen to roughly 60% of the volume of comparable loans made outside the program.

{kind=link}

Meghan Smith/Federal Reserve Bank of Boston

When they compare the volume of Main Street loans with the volume of similar loans made outside the program to only smaller businesses (EBITDA of less than $50 million) with leverage ratios of less than 6, the Main Street volume is twice as large as the large banks’ volume. (See figure.) Relative to the volume of large bank loans to all small firms regardless of their leverage ratio, the Main Street volume was about 50% larger.

“Overall, our comparison highlights that the uptake of the Main Street program was very similar to the uptake from (large) banks, especially for borrowers with less than $50 million EBITDA,” the authors write. “This finding suggests that Main Street added substantially to the supply of credit to the smallest firms.”

About the Authors

About the Authors

Larry Bean is the executive editor in the Research department at the Federal Reserve Bank of Boston.

Email: Lawrence.Bean@bos.frb.org

Keywords

- Main Street Lending Program