Statement of Eric S. Rosengren, Commenting on Dissenting Vote at the Meeting of the Federal Open Market Committee

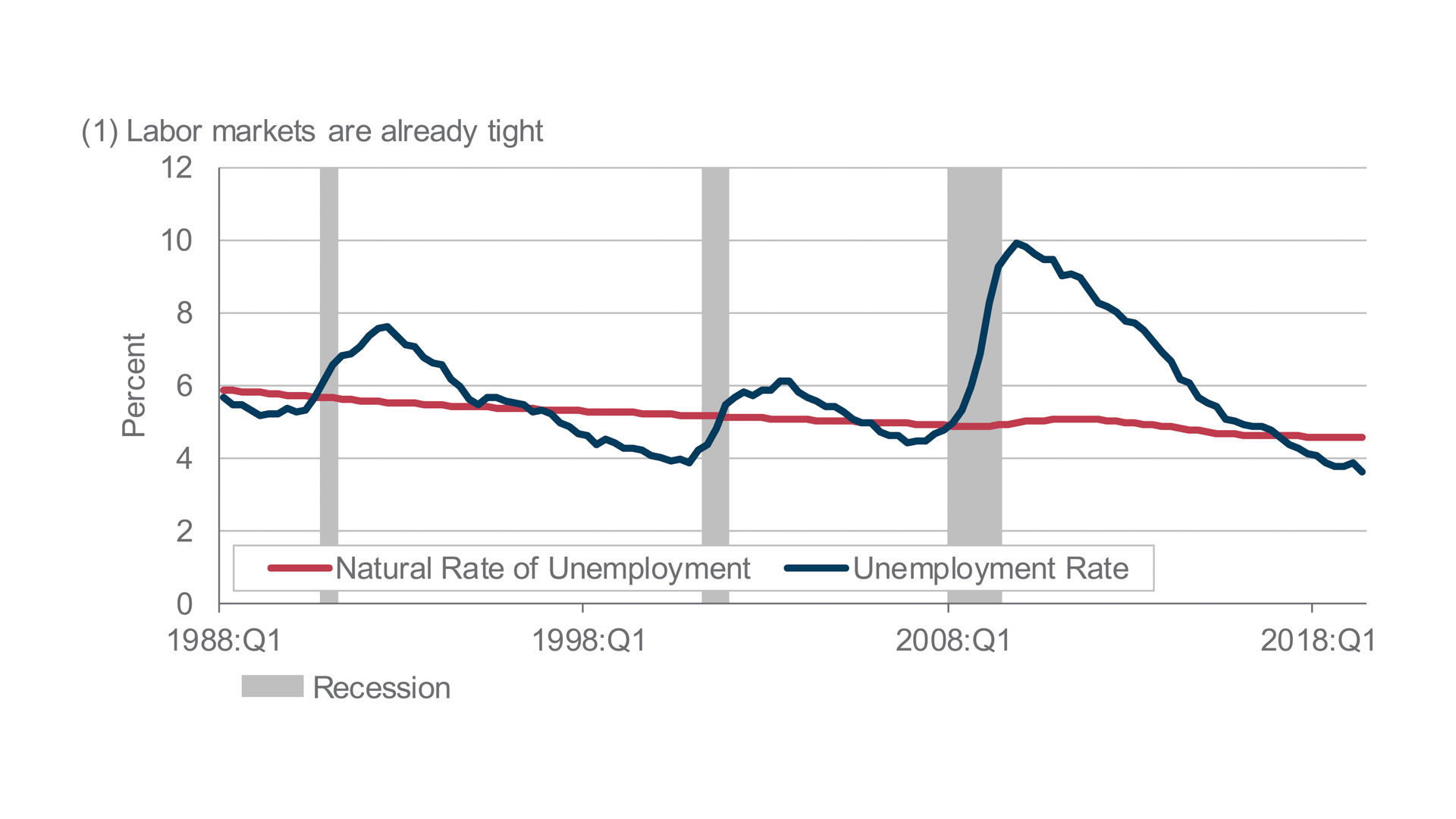

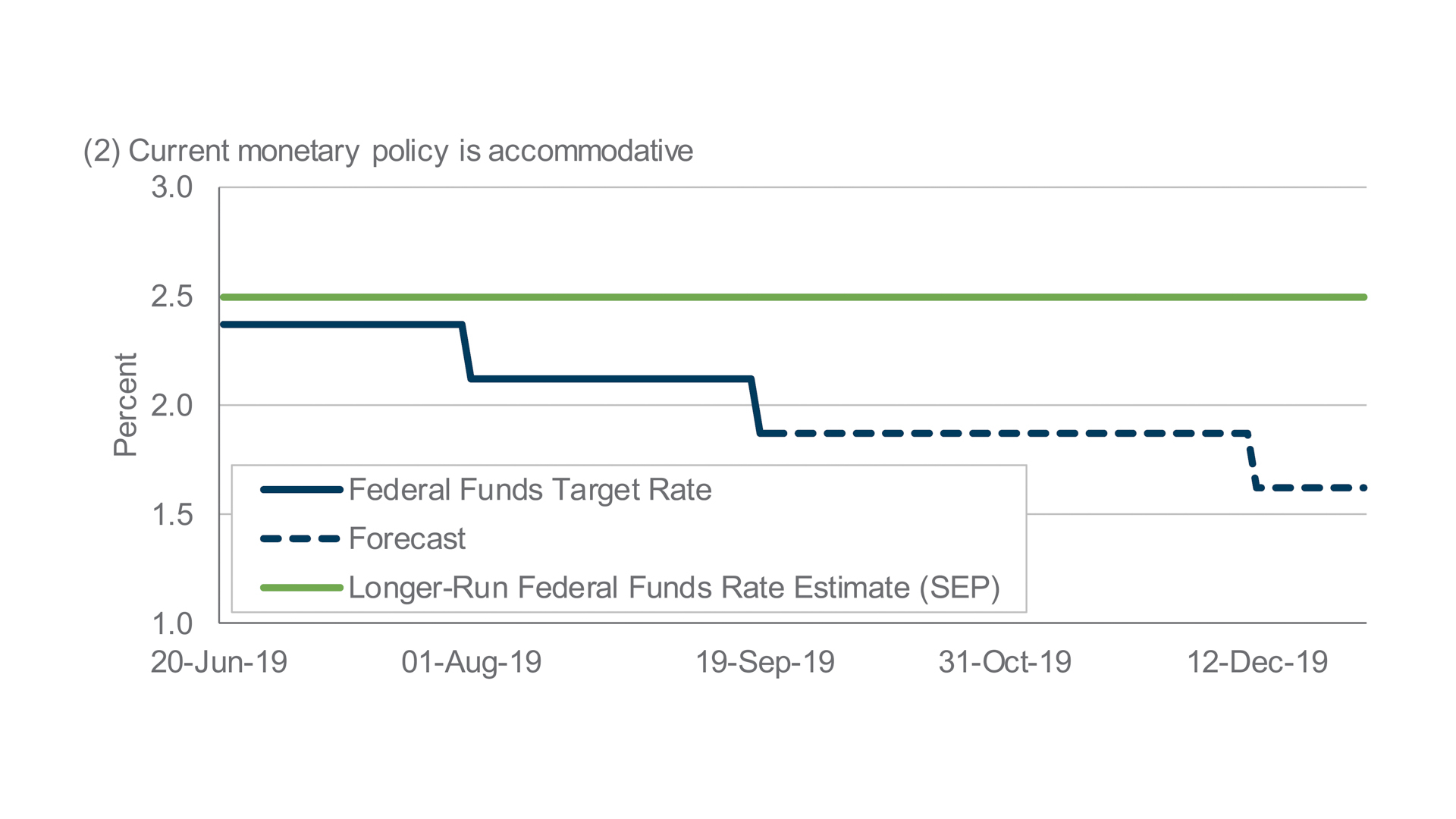

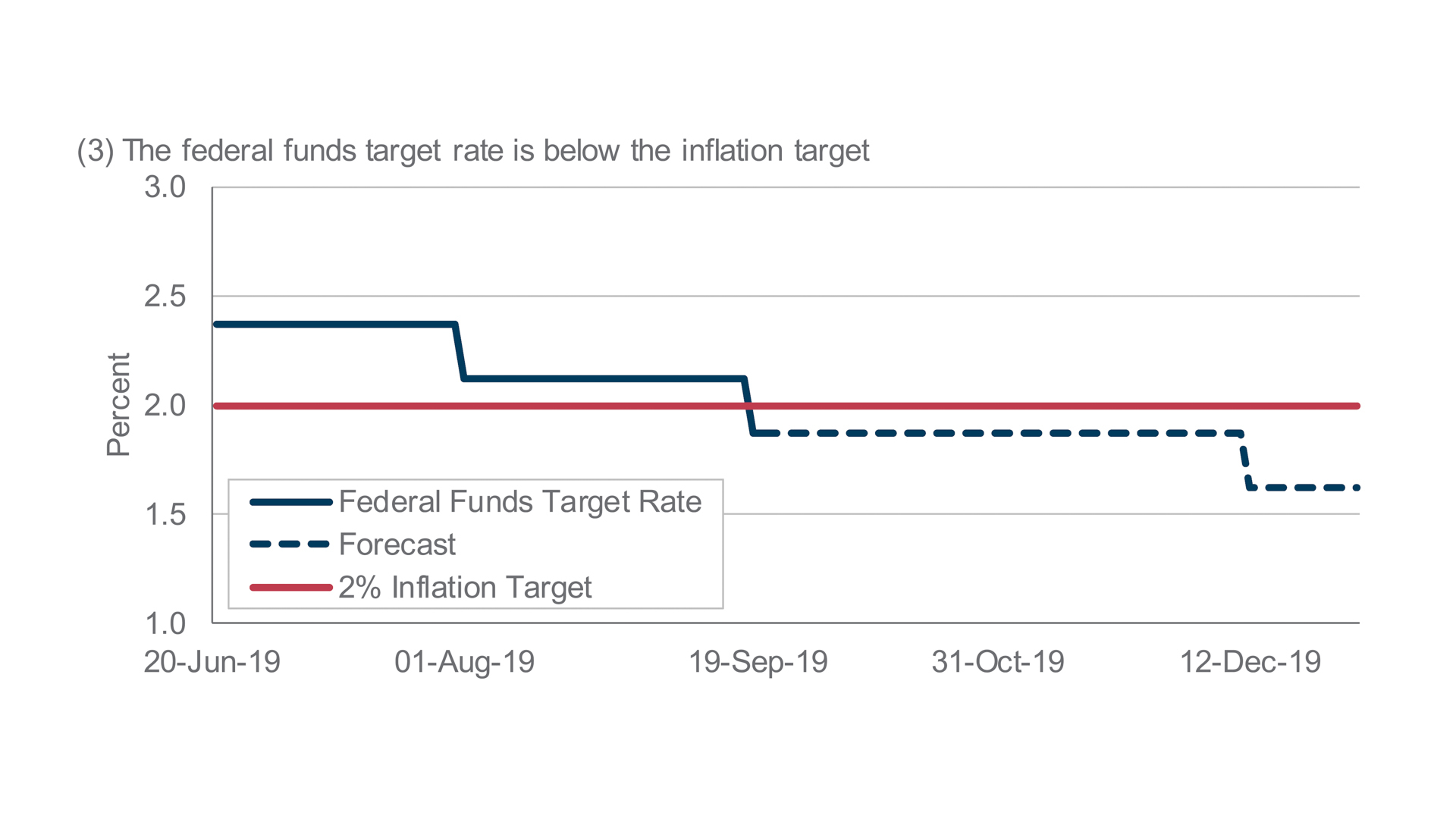

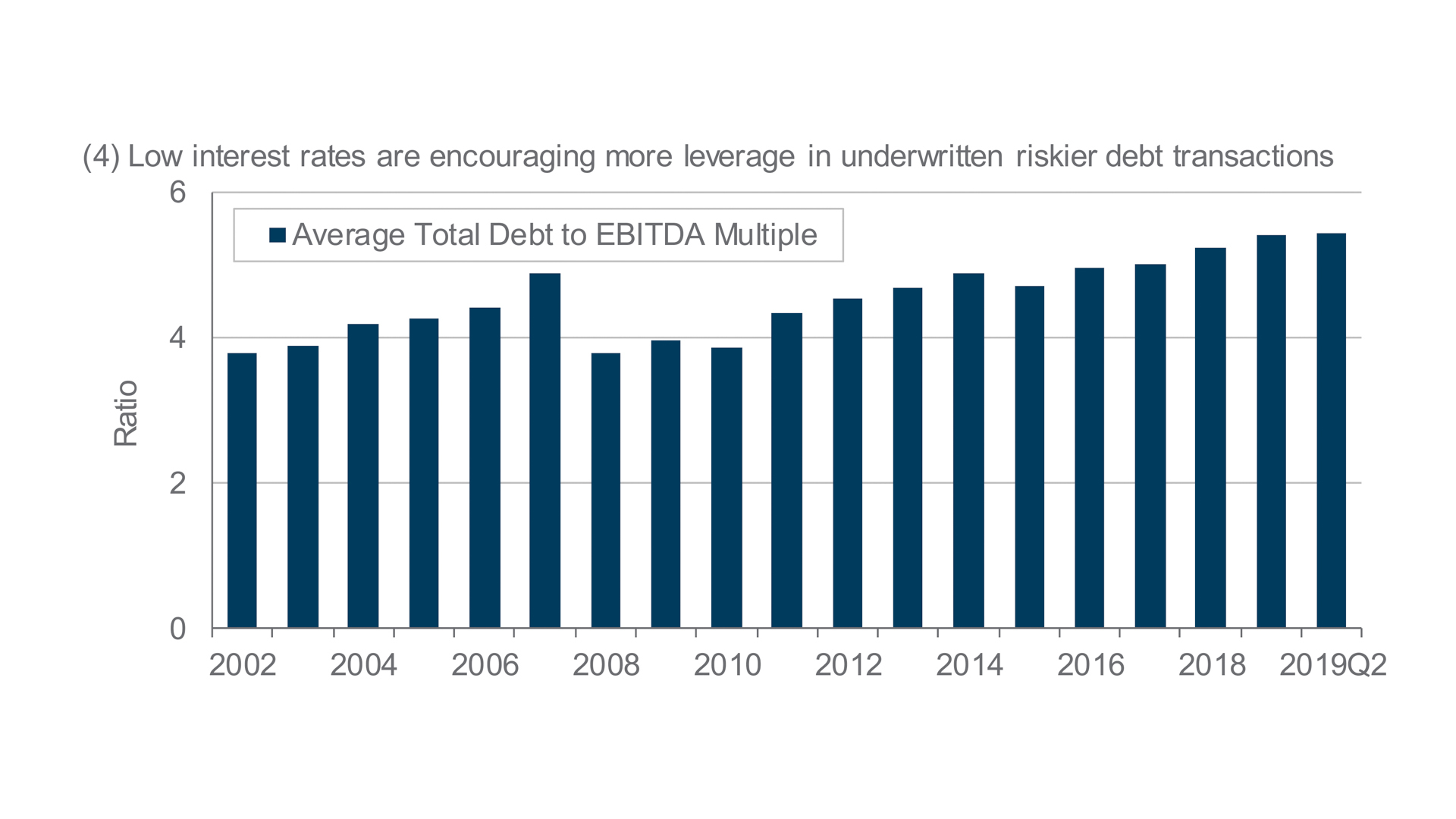

The stance of monetary policy is accommodative. Additional monetary stimulus is not needed for an economy where labor markets are already tight, and risks further inflating the prices of risky assets and encouraging households and firms to take on too much leverage. While risks clearly exist related to trade and geopolitical concerns, lowering rates to address uncertainty is not costless.

The following four charts reflect the key data on which I base this view, with each chart’s title summarizing a key point. Also, I describe my views in more detail in a speech entitled Assessing Economic Conditions and Risks to Financial Stability.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Notes: (2-3) The forecast for the federal funds target rate is calculated using the CME Group probability for the most likely outcome for the target range. Pictured in the charts is the midpoint of the actual and forecast target ranges. (2) The longer-run federal funds rate estimate is the median of the SEP estimates for the federal funds rate in the longer run. (4) Includes loan deals that are syndicated in the U.S. market. Includes transactions with loans priced at Libor+225 and higher. Total debt includes loans and bonds. Excludes the media and telecom industry deals prior to 2011. EBITDA is earnings before interest, taxes, depreciation and amortization.

Sources: (1) BLS, CBO, NBER, (2) Federal Reserve Board, CME Group, FOMC - Summary of Economic Projections, (3) Federal Reserve Board, CME Group, (4) LCD, S&P Global Market Intelligence, (1-3) Haver Analytics

Resources

Resources

Keywords

- Dissent Statement