The Create Jobs for USA Program

Lee Bodzioch/Federal Reserve Bank of Boston

Starbucks and Opportunity Finance Network teamed up to stimulate job growth through small-business lending.

{kind=link}

One of the most debilitating legacies of the Great Recession is the very slow job recovery that followed. The United States did not return to prerecession job levels until nearly five years after the recession ended. Even now there are a large number of discouraged workers who are not in the labor force because of lack of job opportunities. Low-wealth, low-income, minority, and otherwise marginalized communities bore the brunt of the recession and were least equipped to deal with it. In late 2009, when unemployment was cracking a record-high 9 percent for whites, unemployment was over 16 percent for blacks and nearly 13 percent for Hispanic and Latino Americans.1 The employment divide was (and still is) similarly stark across education, wealth, and income stratification.

Integral to the story of lagging job growth in the United States are struggling small businesses. Small businesses account for nearly 55 percent of current employment and 66 percent of net new jobs since the 1970s.2 Although they lead in job creation in boom times, they are vulnerable to recessions, when outside sources of financing may dry up. Even during the recovery, many small businesses reported difficulty in securing loans.

Tackling the Challenge

In 2011, Opportunity Finance Network (OFN) and Starbucks Coffee Company teamed up to launch Create Jobs for USA Fund to help alleviate the credit crunch facing community businesses. OFN is a nonprofit network of community development financial institutions (CDFIs)—private financial institutions that focus on community businesses and individuals in distressed and underserved markets. A team that combined OFN's track record of creating jobs through community business financing with the corporate leadership, resources, and branding of Starbucks joined hands to help realign the backbone of America's economy.

From 2011 to 2014, the Create Jobs for USA fund raised more than $15 million in donations from individual and corporate donors. Starbucks donated $5 million and encouraged individual donations through its "Indivisible" campaign, which rewarded customers who donated to the fund with a branded wristband. In addition, Starbucks launched an "Indivisible" line of products—wristbands, mugs, and other items—and made a donation for each item sold to customers.

Funds were distributed as capital grants to 120 CDFIs selected from OFN's lender network for their financial performance and track record of serving community businesses. CDFIs were then able to leverage the grants to provide over $105 million in loans to community businesses. The expectation was that additional jobs would be created as the CDFIs reinvested the repaid loans, resulting in a virtuous cycle of job growth in communities that need it most.

What Was Learned

The Create Jobs for USA Fund provided an excellent opportunity to learn whether and how CDFI lending helps with job creation.

Characteristics of Loans

OFN's network of CDFIs is sprawling, and those awarded grants through Create Jobs for USA made loans to many businesses over a wide range of industries and geographies. Initial reports from the 120 CDFIs who received OFN grants reveal that they made 34,915 loans overall, providing $2.3 billion in funding.3 CDFI loans tend to serve low-income, minority neighborhoods. CDFI loan recipients were located in ZIP-code regions with 70 percent minority population, on average (as opposed to 37 percent national average), and with median household incomes of $45,000 (as opposed to $52,800 national median).4 CDFIs disbursed loans to community businesses in every state and in all industry sectors represented by 20 two-digit North American Industry Classification System categories of the US Census Bureau, in addition to all five types of OFN-defined community businesses. (See "OFN's Five Types of Community Business.")

OFN's Five Types of Community Business

Microenterprises: Community businesses with five or fewer employees (including proprietor), and with a maximum loan/investment of $50,000.

Businesses: Community businesses with more than five employees or with CDFI financing in an amount greater than $50,000.

Commercial Real Estate: Construction, rehabilitation, acquisition, or expansion of nonresidential property used for office, retail, or industrial purposes.

Community Services: Community-service organizations such as human- and social-service agencies, advocacy organizations, cultural and religious organizations, health care providers, and child care or education providers, regardless of tax status.

Housing Development: Predevelopment, acquisition, construction, and renovation to support the creation of rental housing, service-enriched housing, transitional housing, and owner-occupied housing.

Reporting and Results

OFN set up a two-step reporting system on job creation. In addition to details about the loan, such as size and date closed, OFN required CDFIs to gather certain details about job creation from businesses in their portfolios. This initial report included existing full-time-equivalent (FTE) jobs, FTE jobs that would likely have been lost without the loan, projections for FTE jobs that would be created within a year of closing the loan, and FTE jobs that would be created more than a year after the loan. CDFIs were then asked to get a follow-up report of actual job creation from each business within a year of closing a loan.

Of the loans closed within a year of receiving a grant, 1,434 had a follow-up report.5 The report includes information on direct, indirect, and induced job creation and retention (DII jobs) associated with each loan. DII jobs are all jobs created and retained, including not only primary jobs at the recipient business but also secondary jobs created at other establishments as a result of increased activity in the local economy. The measure of DII jobs was generated using IMPLAN Impact software, which uses industry and geographic information to simulate local labor markets and assigns a multiplier to capture the secondary effects of creating jobs on the broader economy, giving a fuller measure of jobs impact.

{kind=link}

Rachel Bissett/Federal Reserve Bank of Boston

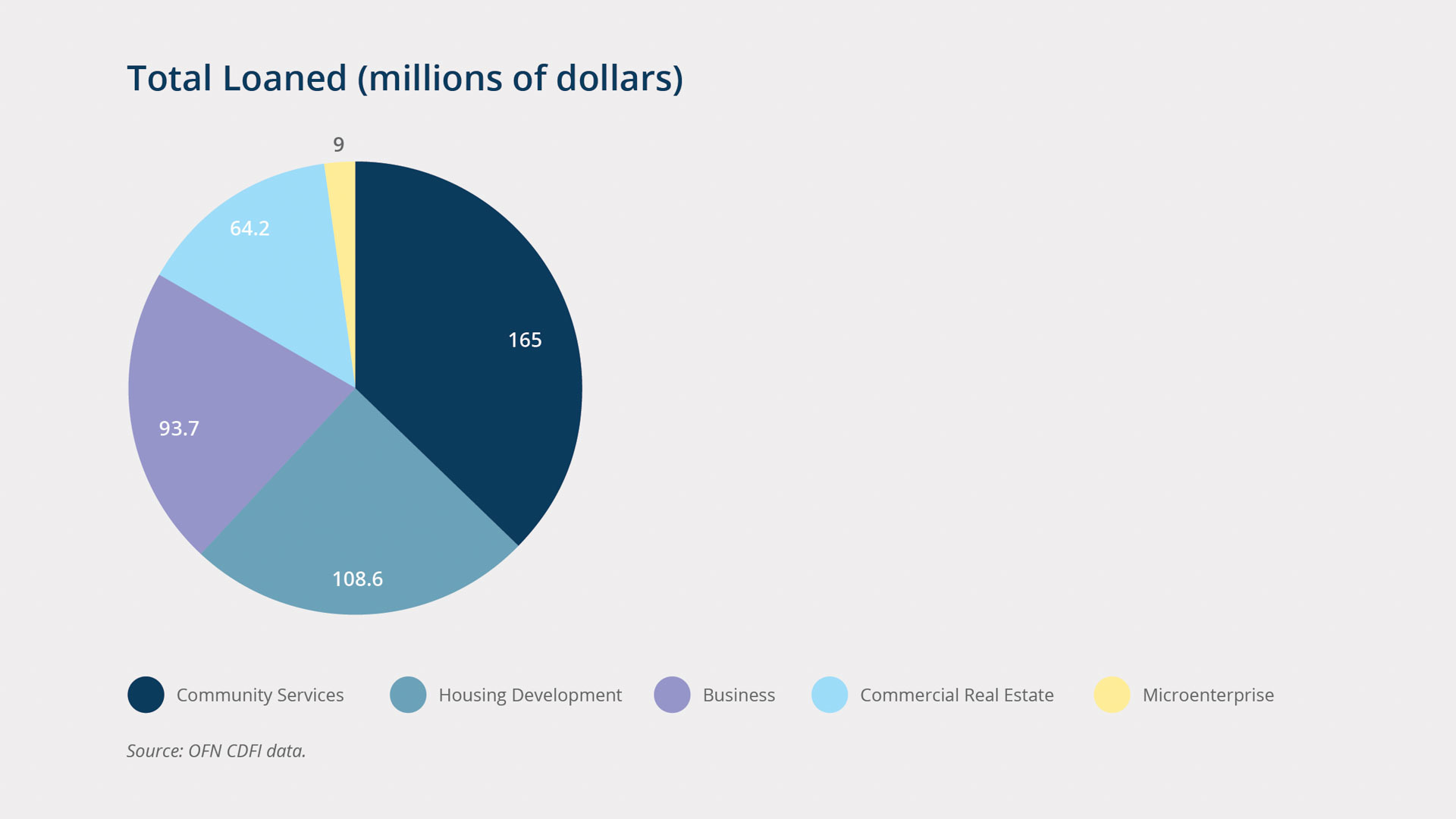

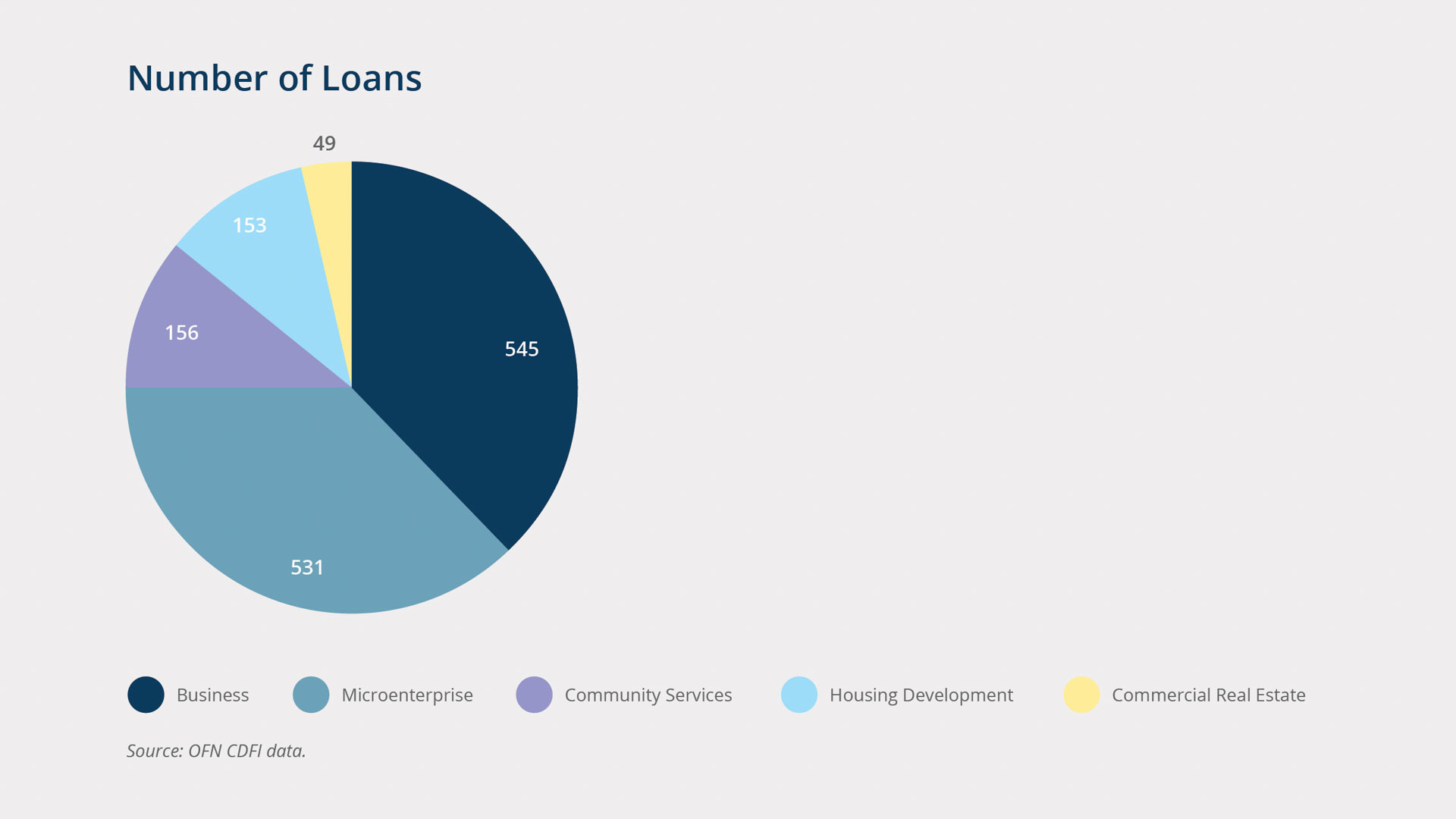

Of loans with follow-up reports, community services received the largest volume of CDFI financing, followed closely by housing development, business, and commercial real estate. (See "Total Loaned.") Microenterprises received only a small fraction of the total value of loans disbursed, despite accounting for the second-largest number of loans (531). (See "Number of Loans.") The business category received the greatest number of loans (545), while housing development, community services, and commercial real estate received far fewer.

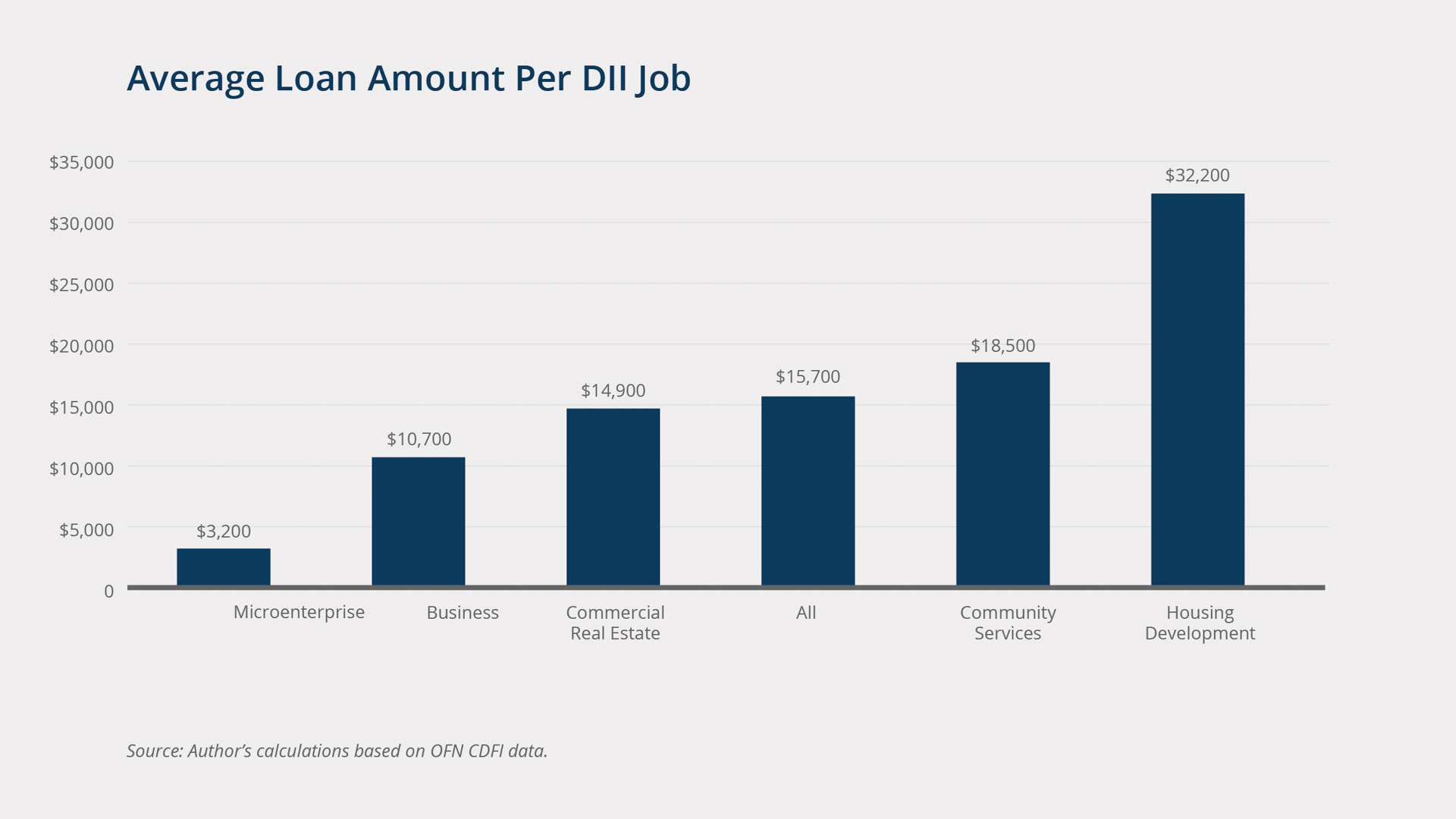

Over all community businesses for which there is a follow-up report, $440 million was lent and 28,100 DII jobs were created or retained, which comes out to $15,700 loaned per DII job. (See "Another Approach to Estimation" for an alternative, though still supportive, set of numbers.) The relationship was found to vary significantly by type of community business. Ratios ranged from $3,200 per DII job (microenterprise) to $32,200 per job (housing development), with higher ratios indicating that lending was less efficient in terms of DII jobs per dollar. (See "Average Loan Amount per DII Job.")

Another Approach to Estimation

Least-squares regression, a more sophisticated method for estimating dollars lent per additional job, gives an estimate of $25,600 over all projects. This technique gives estimates of $11,000, $28,000, $46,000, $9,600, and $128,000 for microenterprise, business, community services, commercial real estate, and housing development, respectively. This article displays descriptive statistics for the sake of simplicity and ease of interpretation.

{kind=link}

Rachel Bissett/Federal Reserve Bank of Boston

The efficacy of microenterprise and business lending supports the notion that small-business and microenterprise financing through CDFIs is a potentially cost-effective lever for promoting job recovery in the United States. This result is consistent with the economic intuition that small businesses are labor intensive and therefore hire more workers per unit capital. More capital-intensive businesses, such as housing development and commercial real estate, create fewer jobs per dollar lent, as we might expect. Regardless of the type of community business receiving the loans, however, lending programs may still have positive value to the communities they are in.

{kind=link}

Rachel Bissett/Federal Reserve Bank of Boston

There are a few important caveats with this analysis. Due to data constraints, I cannot make claims about the quality of jobs across types of community business. There are likely significant and systematic differences in wages, repayment, and other important variables across types of community business, which ideally should be controlled for when comparing the amount loaned per DII job. Notably, it is not possible to determine whether CDFI financing was only a portion of total funding for a project, because the only data available is on the amount of CDFI lending for each project. This influences estimates for some types of community business, like commercial real estate and housing development, which are more likely to have additional outside financing, compared with business and microenterprise. Furthermore, a ratio of dollars lent over jobs is a summary statistic and should not be interpreted as the total "loan cost" of creating or retaining additional jobs. Nevertheless, our evidence suggests that CDFIs are likely to be an effective tool for promoting jobs growth through community business lending. They provided an excellent channel for Create Jobs for USA's grants, which were put to use creating opportunity and changing lives for Americans that needed it most.

Articles may be reprinted if Communities & Banking and the author are credited and the following disclaimer is used: "The views expressed are not necessarily those of the Federal Reserve Bank of Boston or the Federal Reserve System. Information about organizations and upcoming events is strictly informational and not an endorsement."

About the Authors

About the Authors

Sam Richardson,

Federal Reserve Bank of Boston

Email: Samuel.Richardson@bos.frb.org

Acknowledgments

Special thanks to the Boston Fed’s Robert Triest for support and comments along the way and to OFN’s Donna Fabiani, Lance Loethen, and Chris Bell for providing data and valuable insight into the Create Jobs for USA program.

Endnotes

- Data from Haver Analytics/Bureau of Labor Statistics, http://www.bls.gov/cps/demographics.htm.

- See “Small Business Trends” on the US Small Business Administration website, https://www.sba.gov/content/small-business-trends-impact.

- These figures represent the CDFIs’ total number of loans and funds disbursed, not only the loans and funds made possible by Create Jobs for America.

- Author’s calculations. ZIP-code incomes generated using a weighted average of census tract median incomes, from 2009–2013 American Community Survey five-year estimates obtained using the National Historical Geographic Information System, Version 2.0, at the Minnesota Population Center.

- Ambiguity about the true meaning of zero jobs created led to the dropping of reports of zero. Multiple loans sharing CDFI, date, geography, and type of community business were assumed to be on the same project and hence grouped into a single project.