Land Installment Contracts: The Newest Wave of Predatory Home Lending Threatening Communities of Color

iStock/CatLane

Designed to fail, land installment contracts exploit low-income would-be homeowners, especially in communities of color, draining them of resources and often leaving them homeless. Regulation can change that.

{kind=link}

Land installment contracts are not new, but they are historically predatory. In these home purchase transactions, also known as contracts for deed, the buyer makes payments directly to the seller over a period of time—often 30 years—and the seller promises to convey legal title to the home only when the full purchase price has been paid. If the buyer defaults at any time, the seller can cancel the contract through a process known as forfeiture, keep all payments, and evict the buyer.

In the decades between 1930 and the late 1960s the systemic exclusion of African Americans from the conventional mortgage market facilitated the peddling of land contracts with inflated prices and harsh terms to residents of credit-starved communities of color, and in impoverished rural areas.

Until recently, the sellers of land installment contracts were primarily individuals with one or two investment properties. Now, in the wake of the foreclosure crisis, large companies with private equity backing are buying up large numbers of foreclosed homes, many from Fannie Mae and Freddie Mac bulk sales, and selling them to would-be homeowners through land contracts.[1] Companies like Harbour Portfolio, Vision Property Management, and Battery Point Financial are just some of the significant players using this business model.[2]

In mid-2016, the National Consumer Law Center (NCLC) conducted a series of interviews with attorneys across the nation about their cases related to land installment contracts.[3] This article describes the lessons of those interviews, including the problems with land contracts and their impact on communities of color, and proposes a regulatory fix.

The Illusion of Homeownership

While land contracts are marketed as an alternative path to homeownership, contract buyers almost never end up achieving ownership. The contracts are designed to fail. Successive cancellations allow the sellers to churn more would-be homeowners through the same property, creating more profit with each new contract.

Land contracts are structurally unfair and deceptive because they shift all the burdens and obligations of homeownership to the buyers with none of the attendant rights or protections. Land contract buyers are typically obligated to make substantial repairs, which often include overhauls of essential systems like plumbing and heating or adding a new roof. Would-be homeowners invest considerable sums just into making their homes habitable, only to be evicted and lose everything after a default on payments.

Independent appraisals and inspections are seldom performed, and the contracts often require buyers to pay grossly inflated purchase prices.[4] Preexisting liens and mortgages are rarely disclosed, and, as land contracts are infrequently recorded, contract buyers' interests are unprotected.

{kind=link}

Impact on Communities of Color

Advocates report that the buyers in these transactions are almost exclusively people of color: African American or Latino homebuyers.[5] Marketing schemes appear to target African American and Spanish-speaking consumers for these toxic transactions. Specifically, companies advertise through signs in front of houses located in majority-minority neighborhoods and rely heavily on word-of-mouth referrals.[6] One company paid a kickback to a pastor of a primarily Spanish-speaking congregation each time he referred a buyer.[7] An NCLC report notes, "One attorney reported that certain land contract sellers exploit homebuyers' vulnerable immigration status: Instead of evicting them through a court of law, which would allow them to raise defenses, the seller threatens to report them to immigration officials if they do not move out of the home."[8].

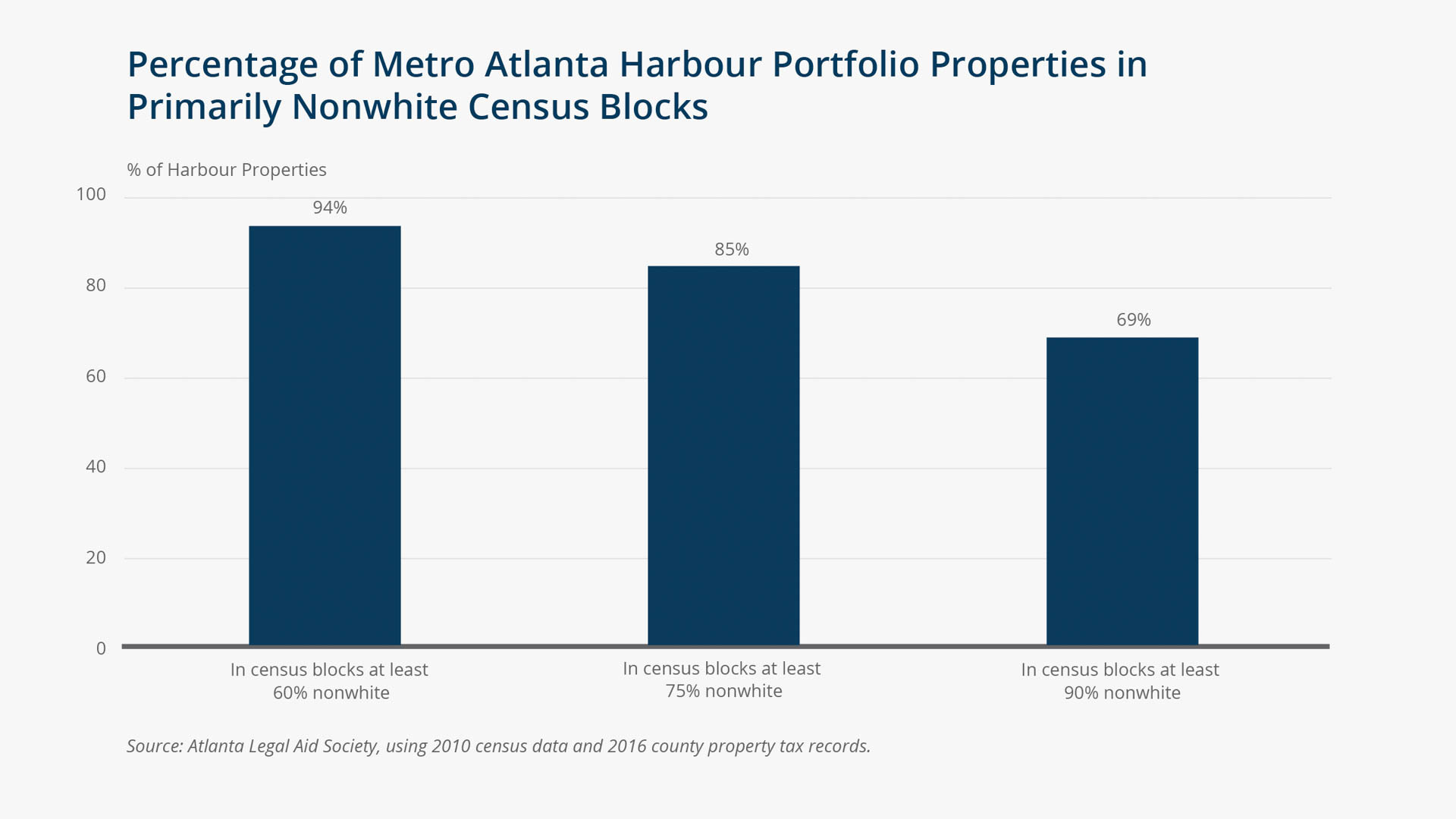

Atlanta Legal Aid attorneys conducted a search of property tax records in six metro Atlanta counties and found 94 properties currently held by Harbour Portfolio in the Atlanta area; most of these homes were likely being sold through land installment contracts as that is Harbour's business model.[9] Nearly all those properties (approximately 93 percent) were located in census blocks that are at least 60 percent nonwhite, and a significant majority were in census blocks that are at least 90 percent nonwhite. (See "Percentage of Metro Atlanta Harbour Portfolio Properties in Primarily Nonwhite Census Blocks.")

The Atlanta case study is representative of a national trend. The same communities that were drained of wealth by subprime lending and the subsequent foreclosure crisis are now being victimized anew by land contract sales. While hopeful homeowners struggle to regain homeownership in minority communities, land contracts are siphoning away precious savings and sweat equity and postponing communities' recoveries from the housing crash through inflated prices and unfair contract terms.

A Regulatory Fix

A comprehensive set of rules is needed to govern the transaction and eliminate the destructive and unfair features in these contracts. Most states provide little regulation of these instruments, but some, including Maine, have regulated them.[10] Oklahoma and Texas have been the most aggressive in addressing the issue and treat these contracts like mortgages. States have the power to ban these transactions altogether. That is the cleanest and most effective way to eradicate land contract abuses.

Federal regulation would provide the most efficient way to protect consumers in states that permit land installment contracts. The Truth in Lending Act (TILA) applies to land contracts to the same extent that it does to other home-secured loans, requiring disclosures and barring certain abusive conduct, but these limited protections cannot curtail other abusive features of land contracts. However, TILA does require the Consumer Financial Protection Bureau (CFPB) to issue regulations addressing mortgage lending practices that are unfair or deceptive, or that seek to evade TILA's regulations. Furthermore, TILA gives buyers the right to sue in the case of injury caused by the seller's noncompliance with the law. Here, we outline a comprehensive regulation the CFPB could put in place to protect buyers in land contracts:

- Require independent inspections, appraisals, and disclosure of the true cost of credit. A licensed, independent inspector should identify any work necessary to make the home habitable and the estimated cost for that work. An independent appraisal should identify the fair market value of the home as well as the fair rental value in its current condition. The amount by which the contract sale price exceeds the fair market value should be treated as a finance charge. These steps would address the deceptive practice of understating the cost of credit in grossly inflated purchase prices.

- Require settlement of property taxes and liens at sale. Sellers should be required to pay all past due assessments prior to signing the contract.

- Require recordation. The seller should be required to record the land contract in the real property records within a short time frame. If the seller fails to record the contract, then the buyer should be entitled to do so.

- Provide protections upon default. All parties should be treated fairly if the transaction falls apart.

- If the buyer defaults and the seller attempts to cancel the contract based on the default, the buyer should have the option to demand the return of all amounts paid under the contract, plus amounts expended for necessary repairs, property taxes, and insurance, minus the fair market rental value of the home for the period of occupancy. This provision avoids the punitive forfeiture of all amounts paid, in favor of an unwinding of the transaction.

- If the seller fails to comply with its obligations (for example by failing to convey title, record the contract in a timely fashion, or pay off preexisting liens), the buyer should be entitled to a full refund of all payments made, without owing the seller the fair rental value. This provision creates strong incentives for compliance.

The rules described above would go a long way toward eliminating the abusive characteristics of land contracts. The harms inflicted on communities of color by these contracts are potentially devastating if left unchecked. Already, tens of thousands of would-be homeowners have invested thousands of dollars in repairs to homes they will likely never own. The CFPB and state lawmakers have the tools to stop predatory land contract practices before they drain further wealth from communities of color—the same communities that were hit hardest by the foreclosure crisis. Swift action is needed to limit the revival of this form of financial exploitation, which threatens to trap more consumers in a mirage of homeownership—one that carries all of the burdens but offers none of the rewards.

Articles may be reprinted if Communities & Banking and the author are credited and the following disclaimer is used: "The views expressed are not necessarily those of the Federal Reserve Bank of Boston or the Federal Reserve System. Information about organizations and upcoming events is strictly informational and not an endorsement."

About the Authors

About the Authors

Sarah Mancini,

National Consumer Law Center

Sarah Mancini is an attorney with expertise in foreclosures and bankruptcy who works half-time for the National Consumer Law Center (NCLC).

Email: smancini@nclc.org

Margot Saunders,

National Consumer Law Center

Margot Saunders is of counsel to NCLC and served as the managing attorney at NCLC’s Washington office from 1991 to 2005.

Endnotes

- Matthew Goldstein and Alexandra Stevenson, "Market for Fixer-Uppers Traps Low-Income Buyers," New York Times, February 21, 2016, A1.

- Alexandra Stevenson and Matthew Goldstein, "Rent-to-Own Homes: A Win-Win for Landlords, a Risk for Struggling Tenants," New York Times, August 21, 2016; Heather Perlberg, "Apollo's Push into a Business That Others Call Predatory," Bloomberg, April 7, 2016, http://www.bloomberg.com/news/articles/2016-04-07/apollo-s-push-into-a-lending-business-that-others-call-predatory.

- Since 1969, the nonprofit National Consumer Law Center has worked for consumer justice and economic security for low-income and other disadvantaged people. The authors thank Jeremiah Battle, Jr., and Odette Williamson for their research, writing, and editorial contributions to this piece.

- Jeremiah Battle, Jr., et al., "Toxic Transactions: How Land Installment Contracts Once Again Threaten Communities of Color" (report, National Consumer Law Center, July 2016), http://www.nclc.org/images/pdf/pr-reports/report-land-contracts.pdf; Heather K. Way and Lucy Wood, "Contracts for Deed: Charting Risks and New Paths for Advocacy," Journal of Affordable Housing and Community Development Law 23, no. 1 (2014).

- Battle, Jr., et al., "Toxic Transactions," 4 (citing interviews with consumer attorneys from around the country).

- Interview with Kristen Tullos (June 22, 2016).

- Phone interview with Luke Grundman and James E. Wilkinson (March 31, 2016).

- Battle, Jr., et al., "Toxic Transactions," 4.

- Ibid., 4–5.

- See Maine's Revised Statutes, Title 33, Property, Chapter 8, Land Installment Contracts, § 482, Minimum Contents of Land Installment Contracts; Recordation.