Forecasting the New England States’ Tax Revenues in the Time of the COVID-19 Pandemic

FGorgun/Getty Images

State governments across the United States face the prospect of sharply declining tax revenues due to the COVID-19 pandemic. They need reliable and up-to-date revenue forecasts to make financially sound policy decisions during this public health and economic crisis. This paper proposes an objective, transparent, simple, and efficient method to forecast state tax revenues in this time of the COVID-19 pandemic. The model is based on only two input factors: the state unemployment rate and an empirically determined time trend. The predictions from the model closely track the actual values of tax revenues for the New England states over the past 25 years. Using this method, this paper forecasts state tax revenues for fiscal year 2021 and suggests large decreases in the New England states. The paper discusses policy options to address the expected declines in revenues and highlights the urgent need for more federal grants without tight strings attached.

Sign up for new research and data on the New England economy.

1. Introduction

The United States is currently in both a public health and economic crisis caused by the COVID-19 pandemic. Starting in March 2020, state and local governments implemented stay-at-home advisories, ordered the closure of nonessential businesses, and recommended against nonessential travel in order to slow the spread of the coronavirus and flatten the infection curve. These government actions reduced the threat of the coronavirus to public health. However, they also brought about substantially decreased economic activity and skyrocketing unemployment. Although states have reopened to varying degrees, economic activity is generally not expected to return quickly to the pre-pandemic level in the absence of a successful coronavirus vaccine.

State governments face the prospect of sharply declining tax revenues related to the COVID-19 pandemic. Collections from individual income taxes will likely fall significantly now that tens of millions of workers across the country have lost their jobs. Because fewer people are making taxable purchases, driving to work, dining out, or traveling, states will collect less sales tax, gasoline tax, meals tax, and hotel tax. The Tax Policy Center at the Urban Institute and the Brookings Institution reports that total state taxes among the 46 states with available data dropped 20.9 percent in May 2020 compared with a year earlier.1 In particular, personal income taxes, sales taxes, and corporate income taxes declined 10.6 percent, 27.8 percent, and 50.7 percent, respectively.

States need reliable and up-to-date revenue forecasts to make financially sound policy decisions during this public health and economic crisis. With the knowledge of how much tax revenue they can expect, governments can plan accordingly to minimize the disruption of crucial public services and balance their budgets as required by state law. At this particular moment, states need new revenue forecasts to remake their fiscal year 2021 budgets. Their original FY2021 budget proposals, which were discussed back in December 2019 and January 2020, understandably did not account for the economic impact of the COVID-19 pandemic and therefore have become obsolete.

Several public agencies and research groups recently released forecasts of the revenue shortfalls for the New England states. These forecasters can largely be categorized into four groups: (1) state agencies, such as the Connecticut Office of Policy and Management (OPM), the Maine Department of Administrative and Financial Service, and the Vermont Legislative Joint Fiscal Office; (2) fiscal watchdog and advocacy groups, such as the Massachusetts Taxpayers Foundation and the Massachusetts Budget and Policy Center; (3) university-affiliated research centers, such as the Center for State Policy Analysis at Tufts University and the Beacon Hill Institute at Suffolk University; and (4) private consulting firms, such as Moody’s Analytics and Fitch Ratings. Most of these forecasters have not revealed their methodologies publicly. The Connecticut OPM cites the percentage decline in state tax in the first year of the 2008–2010 financial crisis as the basis of its recent revenue forecasts.2 The Center for State Policy Analysis at Tufts University relied on the US GDP projections and a high correlation between Massachusetts tax revenue and the US GDP since FY2006 to forecast Massachusetts tax shortfalls for FY2020 and FY2021 (Center for State Policy Analysis 2020).

This paper proposes an objective, transparent, simple, and efficient method to forecast state tax revenue. It is based on a regression model requiring only two input factors: the state unemployment rate and the number of years since FY1994. The specification of the model is guided by basic economic intuition and tested by the data. This paper demonstrates the performance of the model by showing that its predictions closely track the actual values of tax revenue for each state over the past 25 years. Using this method, I forecast the FY2021 tax revenues for each New England state under selected low-, mid-, and high-unemployment scenarios related to the COVID-19 pandemic. Finally, I discuss policy options to address the expected tax revenue declines.

2. Method

After exploring more than 50 empirical models, I have chosen a parsimonious method that fits the data the best.3 This method is based on two assumptions. First, I assume that each state’s tax revenue would have followed a simple-form path over time if its economy had not experienced business cycles. This path likely reflects the long-term movement of the state tax bases driven by underlying economic fundamentals. Second, I assume that business cycles, which are approximated by changes in the state unemployment rate, cause each state’s tax revenue to deviate from its given time path. When the state economy is booming with a lower unemployment rate, its tax revenue rises above its given path. But when the state economy sinks into a recession with a higher unemployment rate, its tax revenue dips below its given path. The shape of the time path and the sensitivity of tax revenue to the state unemployment rate are both affected by each state’s tax system. Therefore, they may vary across states and need to be empirically determined.

Following this method, I model each state’s real tax revenue per capita to follow a linear or quadratic time trend and to have a negative relationship with the state unemployment rate. The linear time trend model is

where Yt is realstate tax revenue per capita in year t, t is standardized to equal 1 for the first year in the data, and Ut is the state unemployment rate in year t. Alternatively, the quadratic time trend model is

{kind=link}

I run both models for each state and then let the data dictate which model to choose for that state. The only selection criterion that I apply is that if the estimated coefficient on t2 in equation (2) is significant, with a p-value of 0.1 or less, then I choose the quadratic time trend model for a given state; otherwise, I choose the linear time trend model for that state.

3. Data

I obtain the data on quarterly state tax collections from the US Census Bureau. This data set has several advantages over the tax data published by each state’s department of revenue. First, the Census Bureau applies a uniform definition of taxes across states and over time, which makes the data more comparable between states and across years. Second, the Census Bureau data set is not affected by each state’s accounting practices. For example, some states earmark a portion of their sales tax for special budget funds, such as the transportation fund or the education fund, while depositing the rest in the general fund. In contrast, the Census Bureau collects all the information on the sales tax, regardless of the purpose for which the states use the sales tax. In addition, the Census Bureau data comprehensively cover state tax types.4 For simplicity and generalizability, I analyze total state taxes, rather than each specific tax type, and thereby circumvent each state’s choices for which tax tools it uses to collect revenue.

The Census Bureau data on state taxes have one obvious drawback. They often are released three months behind the state agencies’ publication of the same-period data, and so they are less timely. On June 29, 2020, the latest Census Bureau data on state taxes were for the first quarter of 2020. The earliest Census Bureau data on state taxes that are in an electronic, workable format are for the first quarter of 1994. Thus, the data availability determines that the sample period for my regression analysis is FY1995 through FY2019, with each fiscal year starting from the beginning of the third quarter of the previous calendar year and concluding at the end of the second quarter of the current calendar year.

I make four adjustments to the state tax data to make them more suitable for the regression analysis. First, I remove state property tax (if any), because property tax is relatively stable and typically not sensitive to business cycles. In the New England region, New Hampshire and Vermont are the only two states with significant state property taxes, which are earmarked to finance public schools. Excluding state property tax improves the model fitting, although it could make these states’ total tax revenues look more volatile compared with when all tax revenues are included. Second, I remove revenue changes that were induced by state tax policy changes. If a state raised the tax rate in a year, I remove the resulting revenue increase from that year’s state tax revenue. If a state had a tax cut in a year, I add back the foregone tax to that year’s state tax revenue. Without this adjustment, the regression model would underestimate the impact of the state unemployment rate on state tax revenue, since states often resorted to raising tax rates to mitigate revenue shortfalls and meet the balanced budget requirements during economic recessions. The fall edition of the annual Fiscal Survey of the States, a report produced by the National Association of State Budget Officers (NASBO), provides data on each state’s annual revenue changes due to newly enacted state tax policies. Third, I use the Consumer Price Index for the Northeast region to inflate each year’s state tax revenue to FY2019 dollars so that tax revenue is comparable from year to year. Finally, I divide real adjusted state tax revenue by state population to derive the real per capita term for each state in each year.

4. Regression Results

Table 1 shows the estimations from the linear and quadratic time trend model for each of the six New England states. Based on the pre-set selection criterion, I choose the linear time trend model as the preferred model for Connecticut, Massachusetts, and Vermont, and the quadratic time trend model as the preferred model for Maine, New Hampshire, and Rhode Island.

{kind=link}

Federal Reserve Bank of Boston

These preferred models fit each state’s data well. Each New England state, except Connecticut, has an adjusted R-squared greater than 0.6, meaning that the model can explain most of the variation in the data. In particular, Rhode Island and Vermont have an adjusted R-squared that is even greater than 0.9. Connecticut has a relatively low adjusted R-squared, likely because the state relies more heavily on the volatile capital gains tax, the pattern of which is difficult to capture in a parsimonious model.

As hypothesized, the estimated coefficient on the state unemployment rate is negative and statistically significant in the preferred model for each New England state. In the region, the sensitivity of tax revenue to changes in economic conditions is greatest in Massachusetts, which has the largest coefficient on the state unemployment rate. A 1 percentage point increase in the state unemployment rate, on average, is associated with a decrease of $160 in real adjusted state tax revenue per capita in the FY1995–FY2019 period for Massachusetts. In comparison, New Hampshire’s tax revenue is the least sensitive to changes in economic conditions. A 1 percentage point increase in the state unemployment rate, on average, is associated with a decrease of only $50 in real adjusted state tax revenue per capita in the FY1995–FY2019 period for New Hampshire.

{kind=link}

Meghan Smith/Federal Reserve Bank of Boston

{kind=link}

Meghan Smith/Federal Reserve Bank of Boston

Before using the regression model to forecast future state tax revenue, I first examine the performance of the model’s predictions for the past. In Figure 1, I plot the predicted value of real adjusted state tax revenue per capita for each state in each year during the sample period of FY1995 through FY2019, based on each state’s preferred model. I also add a prediction interval with a 90 percent confidence level for each predicted value. In other words, there is a 90 percent chance that the actual value of real adjusted state tax revenue falls within this prediction interval in each year, if the prediction model is properly specified. Finally, each state’s graph includes the actual value of real adjusted state tax revenue per capita in each year as a “quality-check” comparison.

Figure 1 shows that the model performs well for the past 25 years. The predicted values closely track the actual values and fluctuate along with business cycles. For each state, the prediction interval with the 90 percent confidence level is relatively narrow, except for Connecticut. More importantly, the interval for each state almost always covers the actual values during the sample period. This suggests that the prediction interval with the 90 percent confidence level is a sufficient and valuable tool for policymakers to consider if they want to be more certain about the revenue forecasts during the budget-making process.

5. Revenue Forecasts

I use the preferred regression model for each state to make the predictions for future tax revenues (that is, out-of-sample predictions). Only two inputs have to be fed into the model: (1) time (t), which is certain, and (2) the future unemployment rate, which must be forecast separately. Given the ongoing uncertainty about the labor market, I present revenue forecasts under three scenarios: low unemployment, mid unemployment, and high unemployment.

In order to calculate the year-over-year changes in state tax revenue in FY2021, I first have to forecast the FY2020 tax revenue for each state, because that data are not yet available (as of early July 2020). For simplicity, I base the forecast of the state unemployment rates for the second quarter of 2020 partially on the forecast of the US unemployment rate for the same year-quarter. The Blue Chip Economic Indicators monthly report includes a consensus forecast of the quarterly US unemployment rate, which is an average of the forecasts from more than 50 surveyed US leading business economists. That report also includes averages of the 10 highest and 10 lowest forecasts. I use these three sets of forecasts to set up the three unemployment scenarios: low, mid, and high.

Assuming that the relationship between each state’s unemployment rate and the US unemployment rate does not change substantially in the short term, I use the ratio of each state’s unemployment rate to the US unemployment rate in the most recent period to scale the Blue Chip forecasts for the US unemployment rate in 2020:Q2 and derive the predicted unemployment rate for each state in 2020:Q2. Considering concerns about the accuracy of the recent unemployment estimates by the US Bureau of Labor Statistics (BLS), I use two versions of the state unemployment estimates in the recent period to construct the scaling factor. First, I calculate the ratio of the average of the April and May 2020 unemployment rates for each state to the average of the US unemployment rates for the same two months using the official unemployment estimates by the BLS.5 However, the BLS recognizes a misclassification error that has been large and persistent in its household employment survey since March 2020.6 Many workers who have been unpaid and absent from work due to coronavirus-related business closures have been misclassified in the survey as employed but absent from work, when they should have been classified as unemployed on temporary layoff.7 No states have been immune to this misclassification error, although the impact of the error may have differed from one state to the next. Some states that believe the BLS has severely underestimated their unemployment rates thus have developed their own estimates, largely based on the data on unemployment insurance claims. In the New England region, Connecticut and Maine have published their own unemployment estimates for May 2020, which are about twice as large as the BLS estimates. Therefore, I construct the second version of the scaling factor by calculating the ratio of a state’s own estimated unemployment rate to the BLS reported US unemployment rate in May 2020, if a state’s own estimates are publicly available.

Then, I use the predicted 2020:Q2 state unemployment rate and the reported state unemployment rates in 2019:Q3, 2019:Q4, and 2020:Q1 to calculate the average state unemployment rate for the entire FY2020. After feeding the model with the estimated FY2020 state unemployment rate and a time value of 26 (2020 – 1994 = 26), I obtain the predicted FY2020 real adjusted state tax revenue per capita for each state under each unemployment scenario.8

{kind=link}

Federal Reserve Bank of Boston

Next, I convert that figure into the nominal value of total state tax revenue (with the enacted tax policy changes, if there were any), which policymakers are more familiar with and therefore may find more useful than the real adjusted per capita term. To do this conversion, I first multiply the predicted FY2020 real adjusted state tax revenue per capita by the 2019 state population, assuming that the population has not changed between these two years. Next, I multiply total real adjusted state tax revenue (in FY2019 dollars) by the ratio of the average Consumer Price Index for the Northeast region (CPI-Northeast) in the July 2019–May 2020 period to the average CPI-Northeast in the July 2018–May 2019 period to inflate state tax revenues to FY2020 dollars. Finally, I add any revenue changes due to newly enacted state tax policies in FY2020, which are reported in the NASBO’s fall 2019 Fiscal Survey of the States.

Table 2 shows the amount and percentage changes in the nominal total state tax revenue between FY2019 and FY2020 that are forecast for each New England state. I obtain the FY2019 total state tax revenues directly from the Census Bureau; the only adjustment is the removal of state property tax. When using the first version of the scaling factor, New Hampshire is expected to experience the largest year-over-year percentage change in nominal state tax revenue, a 14.53 to 19.08 percent decline from a year ago under the three unemployment scenarios.9 Connecticut is expected to experience the smallest year-over-year percentage change; its decline in nominal state tax revenue is likely to be 2.15 to 3.63 percent. However, when the second version of the scaling factor is used, the year-over-year percentage changes for Connecticut and Maine are tripled and doubled, respectively, compared with the changes when the first version of the scaling factor is used.

More importantly, I use the regression model to forecast the FY2021 tax revenue for each state. The COVID-19 pandemic has forced states to restart the FY2021 budget-making process, because their original budget proposals were based on the assumption that the economy would continue growing through all of FY2021, which has become increasingly unrealistic. I take the Blue Chip quarterly forecasts of the US unemployment rate—the consensus, the average of the top 10, and the average of the bottom 10—for 2020:Q3 through 2021:Q2 to construct the average US unemployment rate for FY2021 under the three unemployment scenarios. Again, I use the two versions of the scaling factor to scale the FY2021 US unemployment rate and obtain the predicted FY2021 state unemployment rate.

{kind=link}

Federal Reserve Bank of Boston

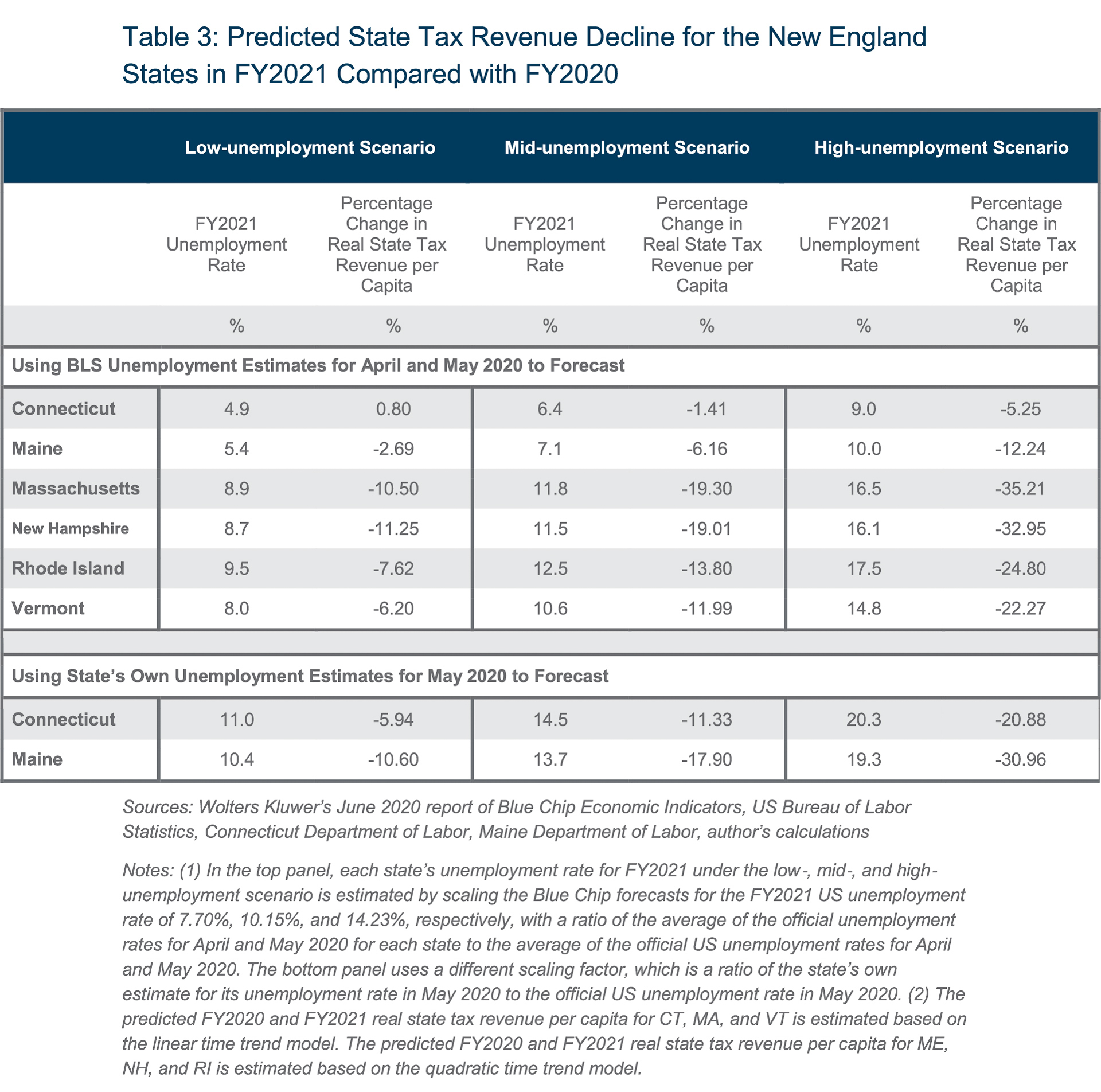

Table 3 shows the year-over-year percentage change in real adjusted state tax revenue per capita for FY2021.10 To be more specific, I compare the predictions under the low-unemployment scenario for FY2021 with the predictions under the low-unemployment scenario for FY2020 as assumed in Table 2. Similarly, I compare the predictions under the mid- and high-unemployment scenarios for FY2021 with the mid- and high-unemployment scenarios, respectively, for FY2020 as assumed in Table 2.

When I use the first version of the scaling factor, the results indicate that all the New England states except Connecticut are expected to experience a decline in real state tax revenue per capita in FY2021, even under the low-unemployment scenario. The decrease is expected to be far greater under the high-unemployment scenario, ranging from 5.25 percent for Connecticut to 35.21 percent for Massachusetts. The expected revenue declines for Connecticut and Maine are even more severe when I use the second version of the scaling factor.

6. Conclusion

This paper proposes a simple, data-driven method that can be used to forecast state tax revenue in this time of the COVID-19 pandemic. The model is based on only the state unemployment rate and an empirically determined time trend. The paper shows that this model performs well, with the predictions closely tracking the actual values for the New England states over the past 25 years. This model is flexible and can be updated easily when additional years’ data become available. It is also sufficiently generalizable to apply to states in other regions.11 However, because this model was developed using historical data, it is uncertain how accurate these predictions are, since this COVID-19-induced economic crisis is rather different from previous, more traditional recessions.

With that caveat noted, this paper suggests that the New England states will experience a decrease in state tax revenues in FY2021. If the economic recovery is slow, the year-over-year real revenue per capita decline in FY2021 could be greater than 20 percent or even 30 percent.

States will need to take a combination of various policy actions to address these large revenue declines. Many states regularly put aside savings in their budget stabilization funds, commonly known as rainy day funds, before the COVID-19 pandemic. For example, Connecticut and Massachusetts have accumulated savings balances of $2.5 billion and $3.5 billion, respectively, which are historically high levels for both states. Withdrawal from the rainy day funds can help states to weather the remainder of FY2020 and maybe even the early part of FY2021. However, those funds may not be sufficient given how large the FY2021 state revenue declines could be.

State budget cuts will be almost unavoidable under the constraints of the balanced budget requirements, and they will carry significant risks and undesirable consequences. These cuts will harm the vulnerable population that depends on public services, and they will destabilize local government finance if they include reductions in local aid. More broadly, they will reduce the aggregate demand and slow the economic recovery.

States may consider increasing borrowing to help smooth out government spending over this business cycle. In particular, they can participate in the Municipal Liquidity Facility, which the Federal Reserve System recently created to purchase as much as $500 billion of short-term municipal debt.

More importantly and urgently, states need more federal aid. The Coronavirus Aid, Relief, and Economic Security (CARES) Act provided $150 billion in federal aid to state and local governments. While this money is helpful, state and local governments are legally bound to use it exclusively to pay for expenses directly related to the COVID-19 pandemic. Based on the current common interpretation of the CARES Act, state and local governments are not allowed to use this federal aid to address revenue shortfalls, even though the pandemic is the ultimate source of the state tax decline. Therefore, states need additional revenue transfers, without tight strings attached, from the federal government, which is not subject to balanced budget requirements like the ones that constrain state and local governments. States need more federal aid for FY2021 and maybe even beyond, because it will likely take several years for state tax revenues to recover from the damage caused by the COVID-19 pandemic.

Endnotes

- Lucy Dadayan, “State Tax Revenues Continued to Decline in May 2020,” TaxVox, the Tax Policy Center blog, July 1, 2020.

- Dan Haar and Ken Dixon, “Lamont: Hit to State in Lost Taxes Could Reach $1.9 Billion,” CT Post, April 2, 2020.

- Boyd, Dadayan, and Ward (2011) present a survey of the revenue forecasting methods used by state budget officers. They suggest that more sophisticated revenue forecasting methods do not necessarily produce more accurate predictions.

- The Census Bureau data include property tax, general sales and gross receipts tax, motor fuel sales tax, alcoholic beverages tax, public utilities tax, insurance tax, tobacco products tax, pari-mutuel tax, amusements tax, other sales and gross receipts tax, beverage licenses tax, motor vehicles tax, motor vehicle operators’ licenses tax, corporations in general tax, hunting and fishing licenses tax, amusement licenses tax, occupation and business licenses tax, other licenses tax, individual income tax, corporate net income tax, death and gift tax, severance tax, document and stock transfer tax, and other miscellaneous tax.

- April and May 2020 are the first two full months with available data reflecting when the US labor market experienced the impact of the COVID-19 pandemic.

- The survey has also suffered a large decline in its response rate; it dropped from about 82 percent in the pre-pandemic period to 67 percent in May. A lower response rate may result in larger estimation errors.

- The BLS estimates that if it had corrected the misclassification error, the true US unemployment rate for May 2020 would have been 3 percentage points higher than reported.

- After the Internal Revenue Service moved the 2019 federal income tax return filling deadline from April 15, 2020, to July 15, 2020, states with the individual income tax also changed their state income tax return filling deadlines to July 15, 2020, which is after the end of FY2020 for states. However, the delayed state income tax collection is still counted as the FY2020 state tax revenue in my forecasts.

- It should be noted that the prediction interval with the 90 percent confidence level for New Hampshire is large, with a spread of 27 to 31 percentage points between the upper bound and the lower bound of the prediction interval.

- Since there are no data yet on revenue changes due to state tax policy changes in FY2021, I am unable to convert the predicted real adjusted state tax revenue per capita to the nominal value of total state tax revenue with the enacted tax policy changes for FY2021.

- I have applied this method to other states and found that the model fits most states’ data well, except for several energy-producing states.

References

Center for State Policy Analysis. 2020. “Estimating the Shortfall in Massachusetts Tax Revenue.”

Boyd, Donald J., Lucy Dadayan, and Robert B. Ward. 2011. States’ Revenue Estimating: Cracks in the Crystal Ball. The Pew Center on the States and the Nelson A. Rockefeller Institute of Government.

About the Authors

About the Authors

Bo Zhao,

Federal Reserve Bank of Boston

Bo Zhao is a principal economist with the New England Public Policy Center in the Federal Reserve Bank of Boston Research Department.

Email: Bo.Zhao@bos.frb.org

Acknowledgments

The author thanks Jeff Thompson for helpful comments and Lan Ha for excellent research assistance.

Resources

Site Topics

Keywords

- revenue forecasting ,

- state tax revenue ,

- COVID-19 ,

- COVID-19 pandemic ,

- NEPPC

JEL Codes

- C22 ,

- C53 ,

- H71