Predicting Recessions Using the Yield Curve: The Role of the Stance of Monetary Policy

FGorgun/Getty Images

{kind=link}

The yield curve is often viewed as a leading indicator of recessions. While the yield curve’s predictive power is not without controversy, its ability to anticipate economic downturns endures across specifications and time periods. This note examines the predictive power of the yield curve after accounting for the current stance of monetary policy—a relevant issue given that monetary policy was unusually accommodative during the most recent yield curve inversion, in the third quarter of 2019. The results show that a yield curve inversion likely overstates the probability of a recession when the stance of monetary policy, judged relative to a time-varying neutral federal funds rate, is accommodative.

Introduction

Numerous studies document the ability of the slope of the yield curve (often measured as the difference between the yields on a long-term US Treasury bond and a short-term US Treasury bill) to predict future recessions.1 Importantly, the predictive power of the yield curve seems to endure across many studies, even if the specific measure of the yield curve and other conditioning variables differ. Indeed, with each new episode of “yield curve inversion”—when long-term interest rates fall below short-term interest rates—recession probability models are dusted off and re-estimated. A notable recent episode occurred in 2019, lasting from May through early October and leading to temporary but widespread concern about an impending recession.

As we will discuss below, most yield curve inversions arise because the central bank raises the short-term interest rate above the long-term rate in reaction to a rise in inflation and/or inflation expectations that often is associated with an overheated economy. Such rate increases are typically expected to be temporary, and thus investors in long-term bonds accept yields that are a bit lower than the temporarily elevated short-term rate. The yield curve inversion of 2019 is notable because it can be traced largely to a decline in long-term yields rather than to an increase in the short-term policy rate. In fact, the Federal Reserve twice cut the policy rate by 25 basis points in the third quarter of 2019. The level of the policy rate is as important as any change in the policy rate when it is judged relative to an estimate of the “neutral” rate, the rate that is consistent with the economy remaining at its long-run sustainable level. The difference between the policy rate and the neutral rate is taken as an indication of the overall stance of monetary policy: Rates above neutral exert a contractionary force on the economy, while rates below neutral stimulate the economy, all else being equal. This note assesses the reliability of the slope of the yield curve as a recession predictor, taking into account the stance of monetary policy measured in this way. It also estimates the probability of recession as of the third quarter of 2019 implied by an array of models that include the stance of monetary policy as an explanatory variable.

The relationship between the slope of the yield curve and the stance of monetary policy in predicting recessions has been examined in the literature with mixed results.2 We show that it is important to gauge the stance of monetary policy as the difference between the policy rate and a time-varying, rather than constant, neutral rate. Previous studies have largely abstracted from time variation in the neutral rate. There is evidence, however, that both the real and the nominal components of the neutral short-term policy rate have changed over time. By accounting for time variation in the estimated neutral rate, our measured stance of monetary policy becomes a more reliable indicator of future recessions. It does not, however, completely displace the role of the yield curve. In other words, the slope of the yield curve still holds information for future economic activity after the monetary policy stance has been taken into account.

Our findings are relevant for evaluating the probability of an impending recession following a yield curve inversion such as the one that occurred in 2019, when monetary policy was, by most measures, relatively accommodative. Recession fears at the time were quite high, as many yield-curve-based models were predicting elevated probabilities of a downturn. While the yield curve inversion disappeared in late 2019, how much solace to take from such a development is debatable.3 In the past, there have been instances when yield curve inversions retraced but recessions nevertheless materialized. Our results show that predictions relying on only the signal from the yield curve in 2019 likely overstated the probability of a recession, because the stance of monetary policy remained relatively accommodative. This conclusion appears robust along several dimensions, including the definition of the monetary policy stance variable, the stage of the recession that the probability model is trying to predict, and the inclusion of other explanatory variables. Overall, our findings suggest that it is important to consider the stance of monetary policy when using the yield curve to assess recession probabilities.

The rest of this article proceeds as follows. Section 2 reviews the different channels that can explain the predictive power of the yield curve for future recessions. Section 3 assesses empirically the role played by the current stance of monetary policy in the yield curve’s predictive power. Section 4 discusses the robustness of this finding. Section 5 concludes.

2. Background: The Yield Curve, Monetary Policy, and Recessions

Recessions are difficult to predict, in part because they occur rarely, but also because the factors that drive the economy into a recession most likely differ across episodes. As a consequence, a factor that may drive one recession may fare poorly in predicting other downturns. Using many explanatory variables to estimate the probability of recessions will likely result in a very limited ability to predict recessions outside the estimation sample. In contrast, the slope of the yield curve has proven a promising parsimonious indicator of downturns, possibly because a variety of factors, some of them complementary, can drive a yield curve inversion and at the same time carry information about a future recession.

The Relationship between the Yield Curve and Future Recessions

The slope of the yield curve is typically measured by the “term spread,” that is, by the difference between the yields on long- and short-term Treasury securities. A common measure of the term spread, and the one we focus on here, is the difference between the 10-year Treasury bond yield and the 3-month Treasury bill yield. A yield curve inversion occurs when the spread is negative—when the long-term yield is less than the short-term yield.

Several factors can drive a yield curve inversion. Most common is when the central bank temporarily increases the short-term interest rate and the long-term rate rises less than proportionately (because it embeds expectations that future short-term rates will eventually revert to lower levels). Thus as tighter policy works its way through the economy, the restrictive monetary policy stance can generate an inverted yield curve today and weaker activity in the future. This does not imply that monetary policy is necessarily the sole or primary cause for a recession. For example, forecasts from the Federal Reserve Board staff before the onset of the three most recent recessions, as dated by the National Bureau of Economic Research (NBER), show that actions taken to tighten the stance of monetary policy were intended to slow the economy to a more sustainable pace of growth, not to purposely tip the economy into a recession.4 This does not rule out that the Board staff could have misjudged the effect of policy tightening on economic activity, or the underlying resilience of the economy. It is also possible, however, that a policy action meant to slow the pace of growth to a more sustainable level was exacerbated by exogenous and unanticipated adverse factors. While this implies systematic bad luck striking precisely at the time of tight monetary policy, it is also true that slower growth makes the economy more vulnerable to adverse shocks, thus raising the likelihood of a recessionary event.

A yield curve inversion can also emerge due to a decline in longer-term interest rates. Investors’ expectations about future economic activity, and the associated expectations about future monetary policy, will drive movements at the longer end of the curve. For example, an anticipated slowdown in the pace of economic activity will put downward pressure on long-term yields, because they are driven by expectations of future short-term rates, and investors recognize that the central bank will have to lower rates eventually if the slowdown materializes. Such a decline in long-term yields can generate a yield curve inversion that is correlated with a future recession to the extent that investors correctly anticipate the downturn. Needless to say, theses dynamics could also occur in the context of the previously described monetary policy tightening scenario.

Changes in risk assessments of the future state of economic activity can also affect long-term rates and lead to an inverted yield curve. Indeed, long-term Treasury bonds are an effective hedge against states of the world with low economic activity, as (long-term) interest rates tend to be depressed when activity is low, and so bond prices appreciate when activity is depressed (recall that the price of a bond is inversely related to its yield). When risks of a future downturn increase, even with an unchanged modal path for the future course of monetary policy, there can be a “flight to quality” that bids up the price of long-term Treasury bonds and lowers their yield.5 Thus if a recession materializes, it will be correlated with the inverted yield curve.

In sum, many non-mutually exclusive channels could rationalize why the yield curve has predictive power for future economic activity. In particular, the yield curve aggregates information from a host of sources and captures investors’ expectations about the economy’s future prospects, which are driven by factors that can change over time. Importantly, the yield curve also incorporates information about the stance of monetary policy, which is tied to where the economy stands in the business cycle and could be informative about the likelihood of a future downturn. Relative to other financial market indicators, such as broad stock market indices, that the literature shows to have, at times, predictive power for future economic activity, the yield curve has the advantage of more readily providing additional information about investors’ perceptions of risks.

Evaluating the Yield Curve’s Predictive Power

It is certainly debatable whether the aforementioned reasons for the predictive power of the yield curve are compelling. After all, investors can be wrong about future economic developments, and monetary policy tightening that inverts the yield curve should not necessarily translate into an economic downturn. Indeed, the yield curve is frequently used to predict recessions in large part because it seems to work in practice. While the literature reaches different conclusions about which segment of the yield curve has the greatest predictive power (see Miller 2019), there is much less debate about the general usefulness of the yield curve as an indicator of future US recessions.6

There is much less consensus, however, on what role monetary policy plays in the yield curve’s predictive power. Wright (2006), for example, finds that the term spread, as a summary measure of the yield curve, owes its predictive power for future recessions, at least in part, to the stance of monetary policy. Bauer and Mertens (2018) argue the opposite—that the ability of the yield curve to predict recessions has little to do with the stance of monetary policy. These and other studies, however, do not gauge the stance of monetary policy vis-à-vis a time-varying neutral federal funds rate (neutral rate)—the rate that, absent any shocks, will keep the economy at equilibrium.7 Their implicit assumption of a constant neutral funds rate runs against evidence by Laubach and Williams (2003 and subsequent updates), which shows that the estimates of the neutral (or natural) short-term real rate of interest, while imprecise, tend to exhibit significant variation over time. Moreover, Fuhrer et al. (2018) document that the Federal Open Market Committee’s implicit inflation target, which affects estimates of the neutral rate, was also time-varying until 1996, when the FOMC implicitly adopted a 2 percent target; the committee explicitly adopted the 2 percent target in 2012.

In principle, changes to the real and inflation components of the neutral federal funds rate could offset each other and result in a constant (nominal) neutral rate. However, there is little reason to expect that this is the case in practice. In the next section we define our measure of the time-varying neutral rate and show how the predictive power of the yield curve for future recessions is affected by the relative stance of monetary policy measured in a way that takes into account time-variation in the real neutral rate and in the FOMC’s inflation target.

3. Predicting Recessions Taking into Account the Stance of Monetary Policy

The Stance of Monetary Policy Defined

We measure the stance of monetary policy (MP) as the difference between the nominal federal funds rate (FF) and an estimate of the (nominal) neutral rate (FF*).

![]()

We calculate ![]() as the sum of the Laubach and Williams neutral real rate of interest (

as the sum of the Laubach and Williams neutral real rate of interest (![]() ) and a proxy of the FOMC’s inflation target based on the Hoey-Philadelphia Fed Survey of Professional Forecasters (SPF) 10-year inflation expectations, as reported in the FRB/US data set.8 We take a two-sided smoothed estimate of

) and a proxy of the FOMC’s inflation target based on the Hoey-Philadelphia Fed Survey of Professional Forecasters (SPF) 10-year inflation expectations, as reported in the FRB/US data set.8 We take a two-sided smoothed estimate of ![]() that contains information not available in real time. However, for the purposes of in-sample estimation, we are interested in a measure of

that contains information not available in real time. However, for the purposes of in-sample estimation, we are interested in a measure of ![]() that best approximates its true underlying value, rather than policymakers’ perceptions in real time. Of course in practice, difficulty estimating the neutral rate presents challenges in using such a measure to calculate recession probabilities in real time. As a robustness check, we consider alternative measures of the stance of monetary policy, including one-sided measures, in the next section.

that best approximates its true underlying value, rather than policymakers’ perceptions in real time. Of course in practice, difficulty estimating the neutral rate presents challenges in using such a measure to calculate recession probabilities in real time. As a robustness check, we consider alternative measures of the stance of monetary policy, including one-sided measures, in the next section.

{kind=link}

Alex Cronin/Federal Reserve Bank of Boston

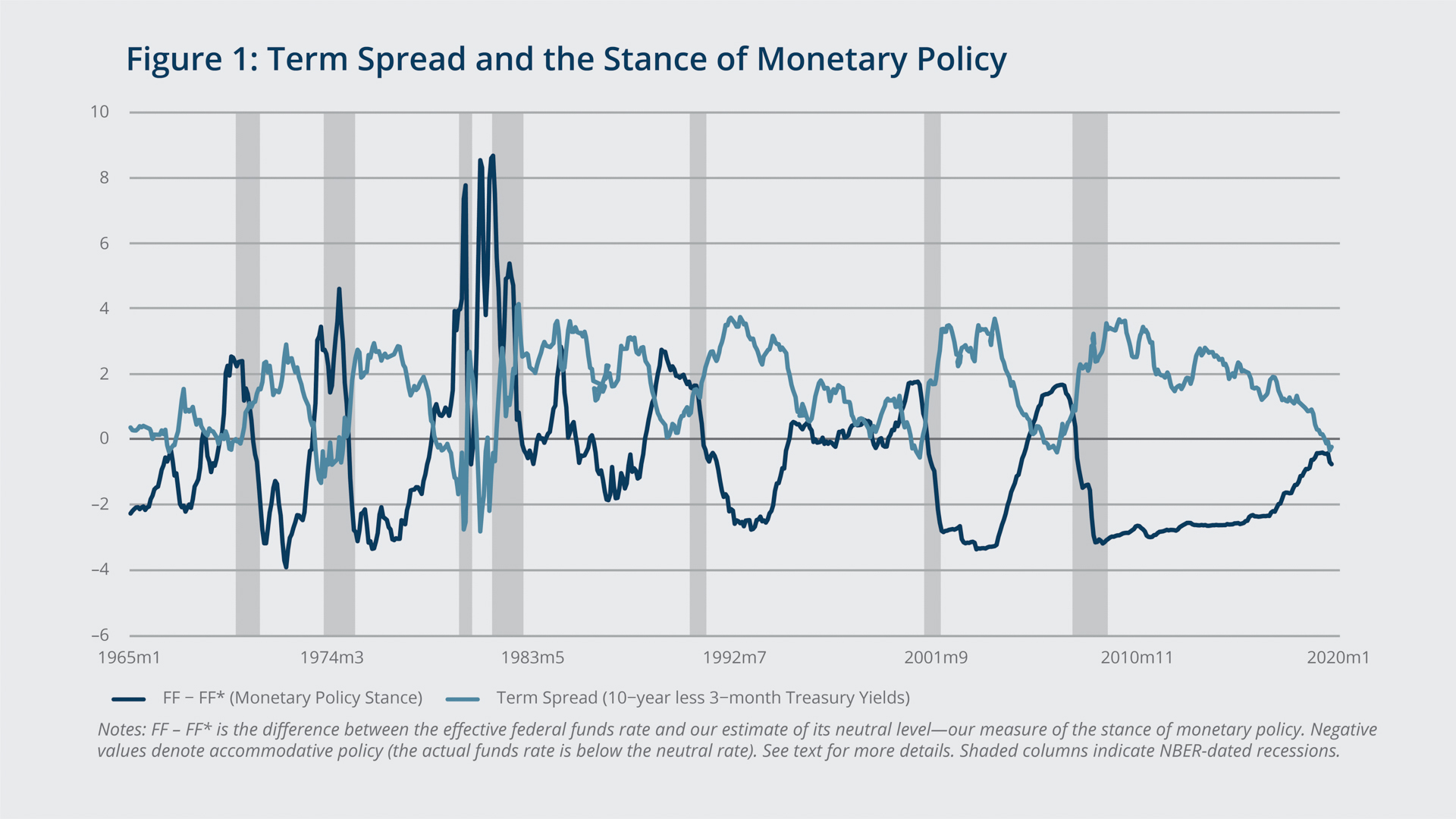

Figure 1 depicts the relative stance of monetary policy (solid line)—the difference between the effective federal funds rate and our time-varying measure of ![]() —from 1965 through the end of 2019. The figure also plots the term spread (dashed line), which we define as the difference between the 10-year and 3-month Treasury yields. As noted earlier, this summary measure of the yield curve is standard in the literature and has been shown to have robust predictive power for future recessions.

—from 1965 through the end of 2019. The figure also plots the term spread (dashed line), which we define as the difference between the 10-year and 3-month Treasury yields. As noted earlier, this summary measure of the yield curve is standard in the literature and has been shown to have robust predictive power for future recessions.

The figure highlights a couple of interesting patterns. First, a tight stance of monetary policy—that is, a policy rate that exceeds the neutral rate by 200 basis points or more—has preceded each recession since 1965. There was one false signal, in 1984, when policy tightening to counter a pickup in inflation was reversed fairly quickly without an ensuing recession. Second, in the past the term spread declined and turned negative as monetary policy tightened, suggesting that the stance of monetary policy was an important factor in previous yield curve inversions. In contrast, the most recent yield curve inversion was not associated with tight monetary policy. Indeed, the figure shows that monetary policy has been relatively accommodative over the past few years despite rising interest rates, and had in fact become somewhat more accommodative when the term spread turned negative mainly during the third quarter of 2019. This yield curve inversion when policy was accommodative rather than tight, as in the past, highlights the potential role of monetary policy in the yield curve’s signal for future recessions.

Empirical Specification

To assess the independent contributions of monetary policy and the yield curve for predicting recessions, we estimate the following probit model:

The model, which is specified at a monthly frequency, assesses the probability of being in a recession, as defined by the National Bureau of Economic Research (NBER), 12 months in the future. The indicator variable ![]() takes the value of one if there is an NBER-defined recession in month t + 12 and is zero otherwise.9 The variable

takes the value of one if there is an NBER-defined recession in month t + 12 and is zero otherwise.9 The variable ![]() is the term spread, which captures the shape of the yield curve based on the difference between the 10-year and 3-month Treasury yields.

is the term spread, which captures the shape of the yield curve based on the difference between the 10-year and 3-month Treasury yields.  is the nominal effective federal funds rate, while

is the nominal effective federal funds rate, while ![]() is its estimated time-varying (nominal) neutral value.10

is its estimated time-varying (nominal) neutral value.10 ![]() is the cumulative normal distribution.

is the cumulative normal distribution.

As specified, the model predicts the likelihood 12 months into the future of any period being identified by the NBER as between the peak and trough of the business cycle (recession). Importantly, there is no distinction here between the early and late stages of a recession—a topic we will return to as part of our robustness analysis.

For our baseline analysis, we estimate equation (1) from January 1966 through December 2009. We stop the sample at the end of 2009—which means that the explanatory variables go through the end of 2008—to include the Great Recession but exclude the years that followed, when the federal funds rate was constrained by the effective lower bound (ELB). With the funds rate at the ELB, the FOMC resorted to other tools to ease credit conditions, and as a result ![]() lost some of its meaning as a gauge of monetary accommodation.11 We also estimate equation (1) splitting the sample in 1987 to test the stability of our findings over time.

lost some of its meaning as a gauge of monetary accommodation.11 We also estimate equation (1) splitting the sample in 1987 to test the stability of our findings over time.

4. Results

4.1 Baseline Estimates

Table 1: Predicted Probability of Being in a Recession 12 Months Ahead

| 1966 to 2009 | 1966 to 1986 | 1987 to 2009 | ||||

| (1) | (2) | (3) | (4) | (5) | (6) | |

| -0.79* | -0.53* | -0.78* | -0.55* | -0.77* | -0.34 | |

| 0.08 | 0.09 | 0.10 | 0.11 | 0.14 | 0.21 | |

| 0.26* | 0.24* | 0.40* | ||||

| 0.05 | 0.05 | 0.15 | ||||

| N | 528 | 528 | 252 | 252 | 276 | 276 |

|

0.31 | 0.37 | 0.34 | 0.42 | 0.24 | 0.27 |

Notes: Standard errors for the estimated coefficients are reported in italics. The superscript * indicates that the estimated coefficient is significantly different from zero at the 99 percent confidence level.

Table 1 reports estimates of equation (1) over the full sample as well as before and after 1987. We also include estimates in which we predict the likelihood of a recession with just the term spread (columns 1, 3, and 5). These estimates yield several relevant results. First, the predictive power of the term spread when only the term spread is included in the estimate is remarkably stable over time, as the estimates from splitting the sample into pre- and post-1987 observations show. This finding fits with earlier literature that documents the yield spread’s predictive power for future recessions.12 Introducing the stance of monetary policy as an additional recession predictor, however, noticeably reduces the absolute size of the coefficient on the term spread (columns 2, 4, and 6). The sum of the two coefficients, in absolute value, tends to be close to the absolute value of the estimated coefficient on the term spread when it is the only predictor.

In addition, over the most recent subsample (column 6), the estimated effect of the term spread is not significantly different from zero at standard confidence levels when we also include the stance of monetary policy. This lack of predictive power for the term spread in the post-1987 sample is due, in part, to the relatively higher correlation between the term spread and the stance of monetary policy over this period. Indeed, the correlation between the two series over this later period is –0.85, compared with a correlation of –0.55 in the pre-1987 sample. This finding is consistent with the important role played by monetary policy in inverting the yield curve before the three most recent recession episodes. In the pre-1987 sample, the statistical significance and economic relevance of the stance of monetary policy vis-à-vis the term spread is somewhat diminished by the aforementioned false signal in 1984. Still, monetary policy played some role in predicting downturns before 1984 given the significant amount of policy tightening associated with the early 1980s recessions.

{kind=link}

Alex Cronin/Federal Reserve Bank of Boston

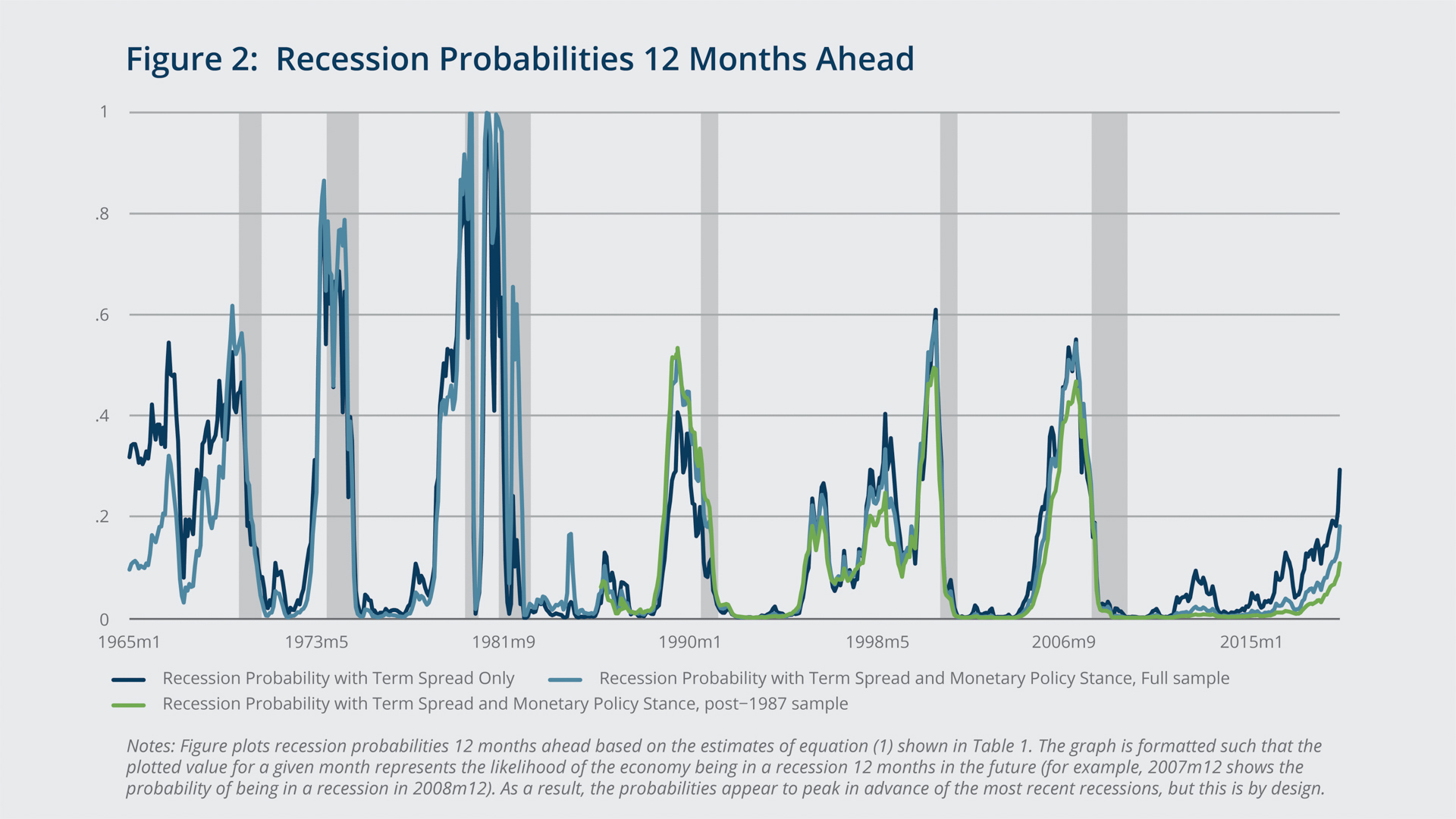

Figure 2 shows predicted recession probabilities based on the estimated coefficients in Table 1, with out-of-sample predictions shown for the January 2010–September 2020 period. (Note that the graph is formatted such that a given date shows the predicted value of a recession 12 months ahead; so, for example, the 2019:M09 point represents the likelihood of the economy being in a recession in September 2020).13 The red line shows the prediction based on the estimates in column (1) that use only the term spread, while the green lines show predictions based on estimates that use both the term spread and the stance of monetary policy (solid line for full sample estimates, dashed line for post-1987 estimates).14 The figure shows that for most of the sample period the predictions using either estimation approach tend to be fairly similar, though the predictions that include the stance of monetary policy provide a better in-sample fit (as captured by the McFadden R2). However, the two approaches provide noticeably different (out-of-sample) predictions of the probability of a recession a year ahead about the time of the yield curve inversion in 2019. When only the yield curve is used as an indicator, the probability of a recession is elevated by historical standards. Adding information from the stance of monetary policy, however, reduces the probability noticeably, given that the stance of monetary policy remains accommodative. In particular, the probability of a recession 12 months ahead in August and September 2019 is roughly 55 percent when just the term spread is used as an indicator, but only 30 percent after the (relatively accommodative) stance of monetary policy is also taken into account.

To summarize, an inverted yield curve’s predictive power for future recessions comes in part from the current stance of monetary policy after time variation in the neutral value of the federal funds rate is considered.15 Indeed, in the sample period from 1987 on, most of the predictive power appears to come from the stance of monetary policy. Nevertheless, even after monetary accommodation is taken into account, the yield curve remains a relevant indicator for assessing the probability of a future economic downturn.

4.2 Robustness

We assess the robustness of our results along several dimensions. In particular, we run numerous recession probability models that vary along the following dimensions.

- The definition of the monetary policy stance variable, which takes four forms:

- our baseline measure,

, where the time varying nominal neutral rate (

, where the time varying nominal neutral rate ( ) is computed as the sum of the Laubach and Williams (2003) estimate of the neutral real rate and 10-year inflation expectations from the SPF

) is computed as the sum of the Laubach and Williams (2003) estimate of the neutral real rate and 10-year inflation expectations from the SPF - the difference between the nominal funds rate and a neutral rate computed as the sum of the Holston, Laubach, and Williams (2017) estimate of the neutral real rate and 10-year inflation expectations from the SPF

- the difference between the real federal funds rate (nominal funds rate less the trailing 12-month core personal consumption expenditures [PCE] inflation rate) and Laubach and Williams (2003) estimate of the neutral real rate

- same as (iii) but instead using the Holston, Laubach, and Williams (2017) estimate of the neutral real rate

- our baseline measure,

- The inclusion of the monetary policy stance variable as well as other variables, such as different term spread measures, stock prices, oil prices, and the change in the unemployment rate.

- The part of the recession that the probit model tries to predict:

- baseline (any of the dates identified by the NBER as between the business cycle peak and trough, as above)

- the first month of the recession only

- the first 3, 6, or 12 months (if it lasts that long) of the recession

- The estimation sample. We consider a long sample running from 1961 through 2019, a sample that ends in 2009, and a sample that starts in 1987.

{kind=link}

Alex Cronin/Federal Reserve Bank of Boston

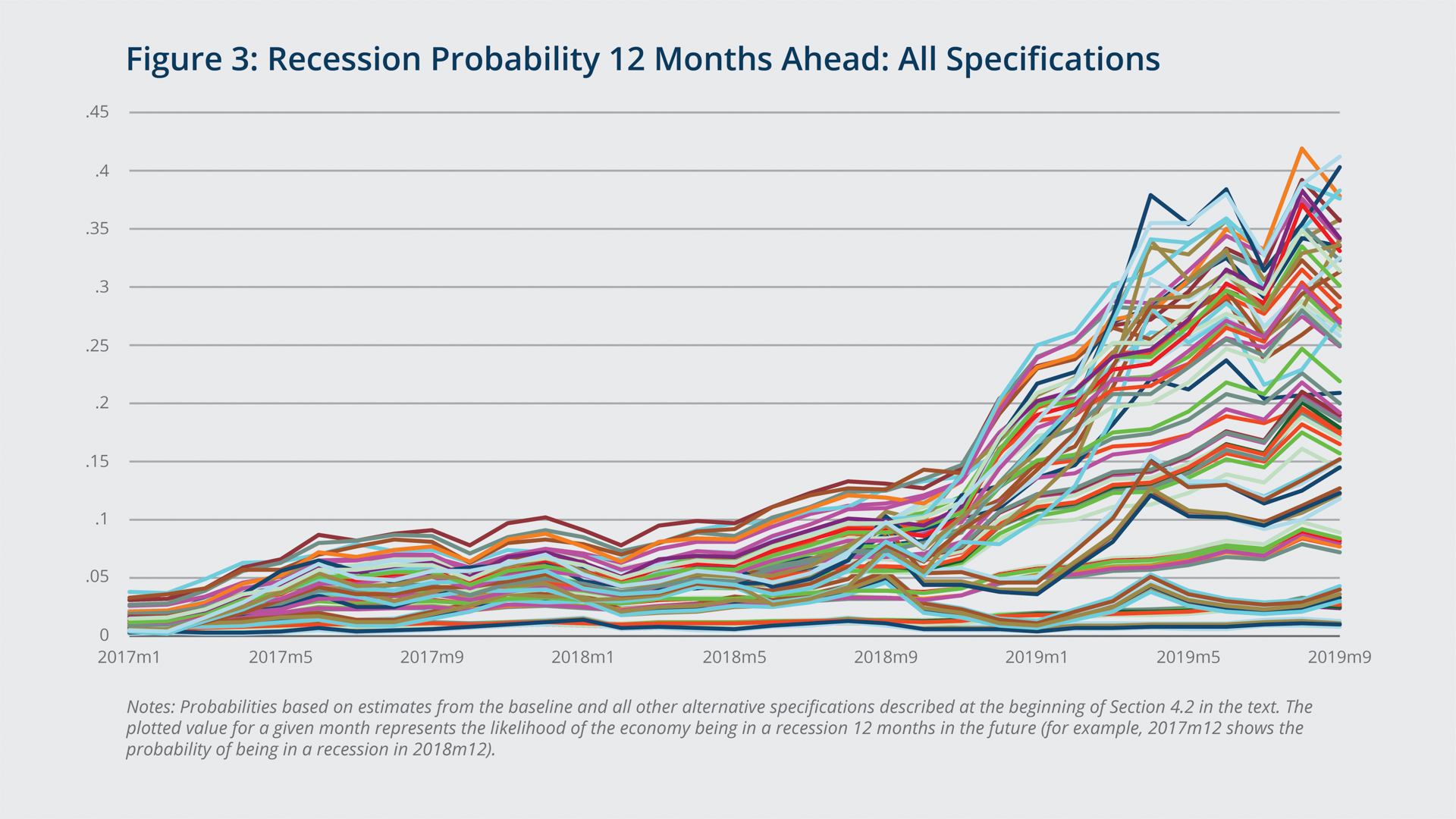

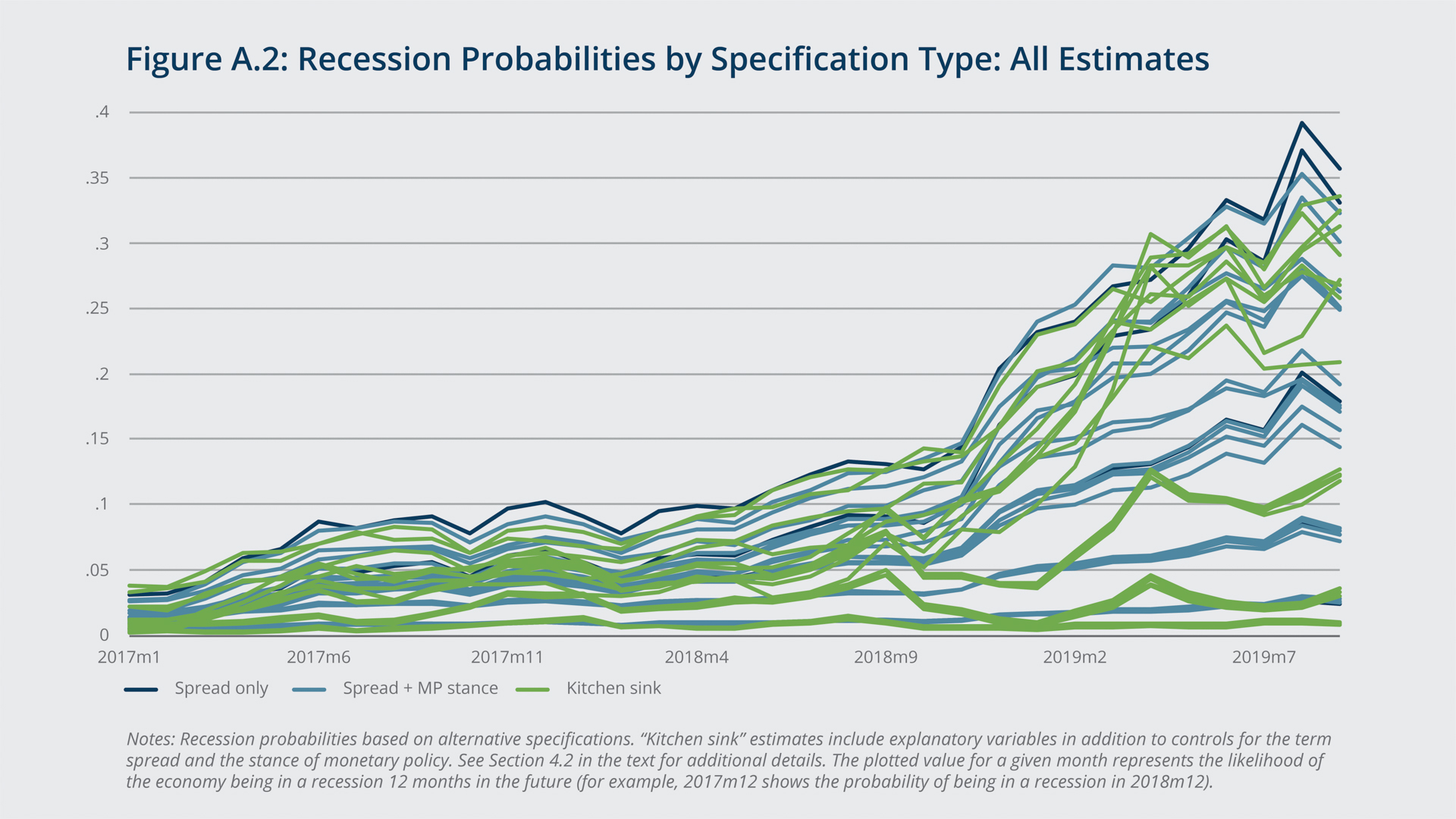

Figure 3 depicts the predicted recession probabilities 12 months in the future in recent years through the fall of 2019 based on the estimates from all of these different specifications that include the stance of monetary policy in addition to the term spread. The results show considerable dispersion in the predicted recession probabilities, with the readings for the third quarter of 2019 ranging from nearly 0 percent to greater than 40 percent.

{kind=link}

Alex Cronin/Federal Reserve Bank of Boston

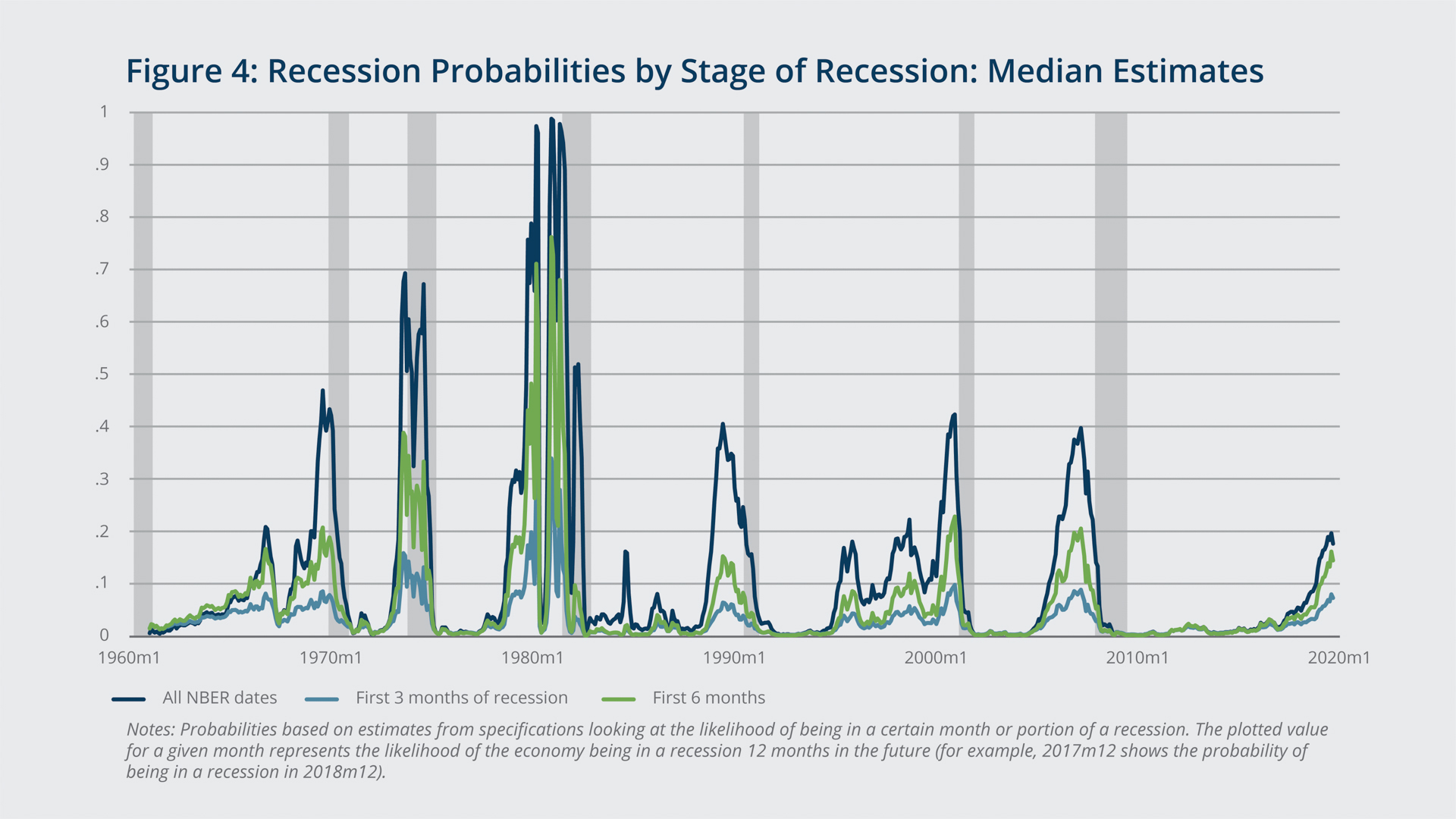

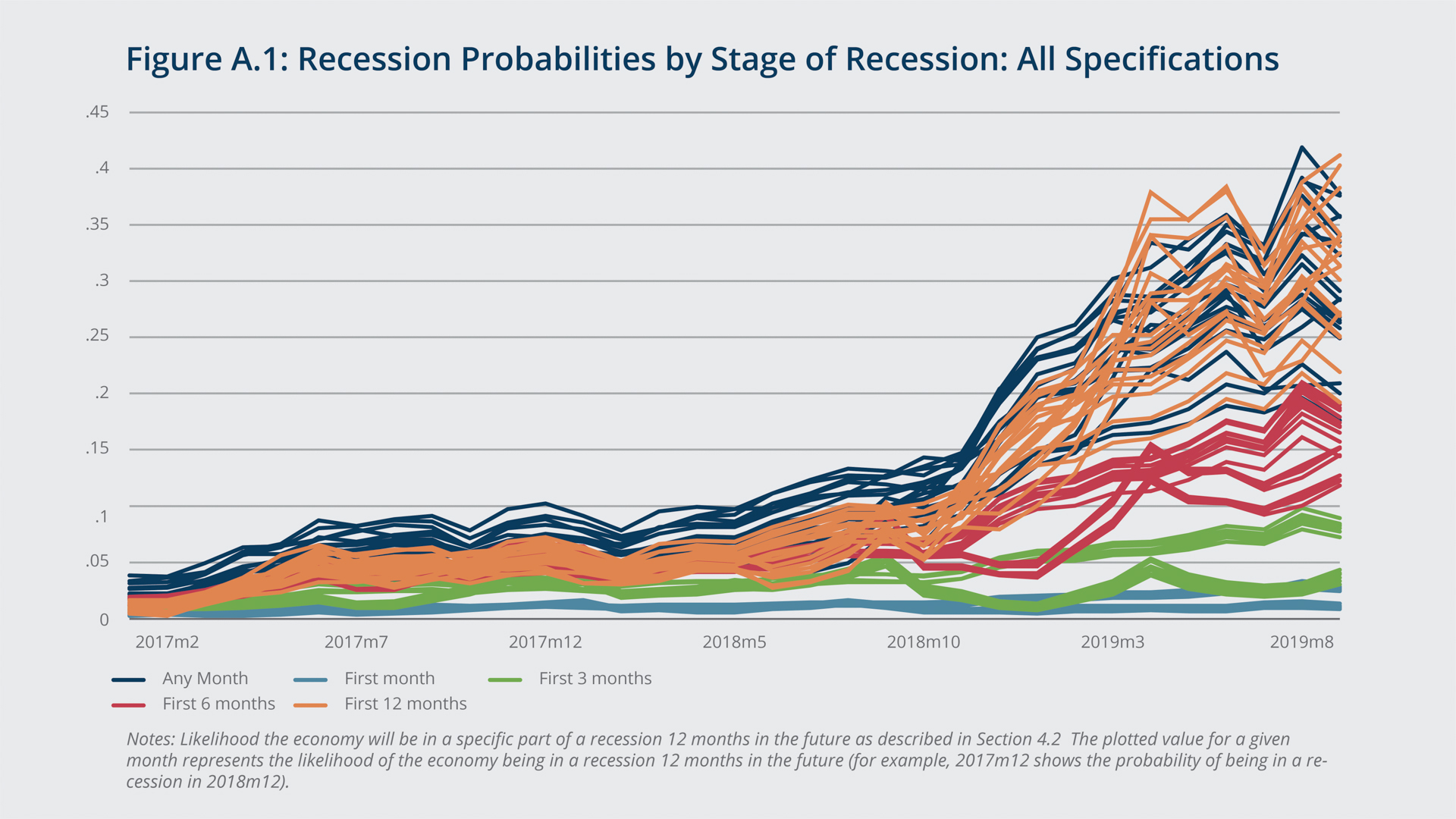

Focusing in particular on the portion of the recession that the probability model is trying to predict (any month [baseline], the first month, the first 3 months, the first 6 months, and the first 12 months [where applicable]), we find that these simple probability models typically work better at predicting the middle or the end of recessions 12 months in the future—a point that is not often discussed in the literature. In particular, Figure 4 plots the median estimate across all the specifications that predict a given part of the recession.16 The figure highlights the models’ limited ability to predict the early stages of a recession (green line [first three months of a recession]) especially compared with the predictions for the first six months (blue line) or any month (red line). The figure also shows the probability of being in the early stages of a recession 12 months ahead was quite low when the yield curve was inverted in 2019. The results also highlight that the probability models have more information content—they provide stronger indications of an impending recession—when any month of a recession period is included in the estimation.

Finally, we consider alternative model specifications to test the robustness of our finding that the stance of monetary policy provides statistically significant and economically relevant information for gauging the probability of future recessions.

{kind=link}

Alex Cronin/Federal Reserve Bank of Boston

Conclusions

The slope of the yield curve, measured as the spread between the long and short Treasury yields, features predictive power for future recessions. This so-called term spread gauges where long-term yields stand relative to short-term yields, regardless of the level of the short-term yields. An outstanding question, however, is the extent to which the information in the term spread—specifically when the term spread turns negative (a yield curve inversion)—for predicting future recessions is a reflection of tight monetary policy. The question is relevant because yield curve inversions tend to happen when monetary policy is tight, that is, when short-term interest rates are high relative to the neutral rate. We have shown that it is possible to obtain a more robust answer to the question of the predictive power of the term spread given monetary policy accommodation when the federal funds rate is measured relative to a time-varying estimate of its equilibrium (neutral) value. Indeed, the FOMC inflation target has changed over time, and the available evidence also points to noticeable changes in the real portion of the neutral rate. As a result, considering explicitly a time-varying neutral federal funds rate should yield a more accurate assessment of the stance of monetary policy. When doing so, it becomes clearer that a nontrivial portion of the information content of the term spread for predicting future recessions is driven by the stance of monetary policy. However, some information for future recessions in the term spread is still associated with movements at the long end of the yield curve, though their contribution seems to have diminished somewhat since 1987.

These findings are relevant for assessing the implications of the 2019 yield curve inversion. The inversion, which occurred primarily during the third quarter of the year, was different from previous ones in that it happened when monetary policy was still accommodative and just after the FOMC twice had lowered the federal funds rate. Our findings imply that such a distinction in monetary policy conditions matters. After the stance of monetary policy is taken into account, the probability of a future recession as of the third quarter of 2019 is lower, often noticeably so, than the signal obtained by relying exclusively on the yield curve.

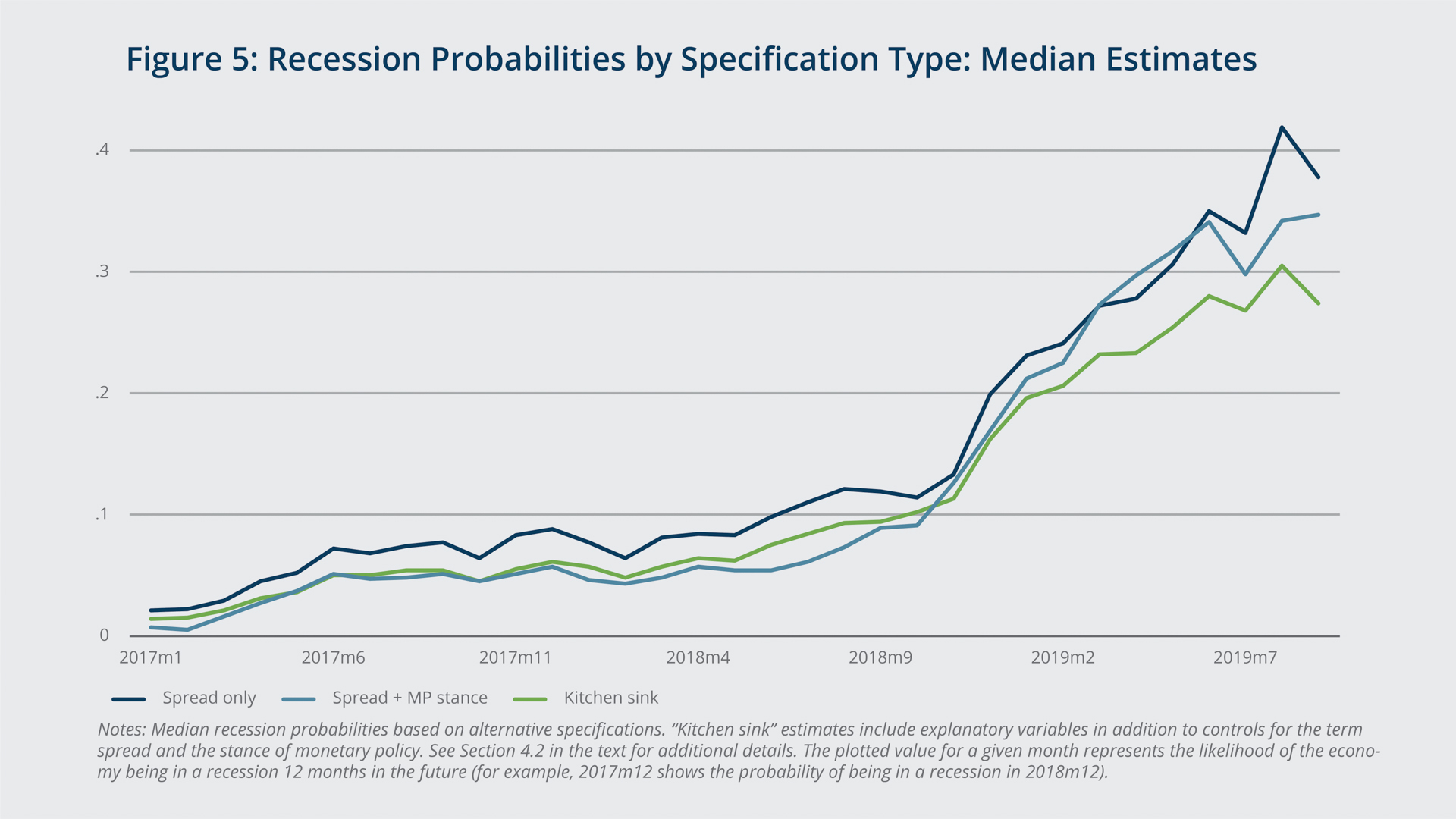

Here we return to predicting any month of a recession 12 months ahead, and we consider models that use only the spread variable, models that add different measures of the policy stance, and so-called kitchen sink models with all the additional explanatory variables mentioned above. Figure 5 shows the median recession probability predictions from each of the three model types, while Figure A.2 in the appendix plots the predictions from each individual specification. Overall, the results tend to support the importance of explicitly taking into account the stance of monetary policy. Indeed, given that monetary policy has remained accommodative over the recent period, the median specification that takes into account the policy stance period (purple line) lies below the medians from the two alternative specifications (term spread only [orange] and kitchen sink [teal]). Adding explanatory variables in addition to the monetary policy stance reduces the recession probabilities somewhat relative to the predictions with the term spread alone; however, the probabilities are generally lowest with the more parsimonious specification that includes just the policy stance and term spread predictors. Finally, estimating these alternative specifications starting in 1987 (not shown) tends to reduce the importance of the term spread relative to the stance of monetary policy, as we found with our baseline estimates (Table 1, column 6).

Appendix

{kind=link}

Alex Cronin/Federal Reserve Bank of Boston

{kind=link}

Alex Cronin/Federal Reserve Bank of Boston

Endnotes

- Harvey (1989), Stock and Watson (1989), and Estrella and Hardouvelis (1991) document the predictive power of the yield curve for future economic activity. A number of subsequent papers focus on the yield curve’s predictive power for recessions. Recent work on this topic (with references to earlier work) includes Bauer and Mertens (2018), Engstrom and Sharpe (2018), and Johansson and Meldrum (2018).

- We review some of this literature in Section 2 of the text.

- The yield curve, as measured by the difference in the 10-year and 3-month yields, was inverted for two days in late January and early February 2020 when fears regarding the coronavirus outbreak initially spiked.

- See Fuhrer et al. (2018).

- Technically speaking, this demand for insurance compresses the so-called term premium, which is the component of long-term Treasury yields not associated with expectations about future short-term interest rates.

- An important caveat, however, is that inference related to the yield curve is typically made on a sample that features few recession episodes.

- Bauer and Mertens (2018) consider a time-varying neutral real rate as an additional explanatory variable, but their specification does not fully capture the stance of monetary policy.

- Up-to-date estimates of the Laubach and Williams neutral real rate of interest are maintained by the Federal Reserve Bank of New York (see https://www.newyorkfed.org/research/policy/rstar). Ten-year inflation expectations data from the FRB/US data set can be found at https://www.federalreserve.gov/econres/us-models-package.htm (series “PTR”).

- Since there are only 12 months between the end of the recession in 1980 and the beginning of the next recession in 1981, we treat the February 1980–November 1982 period as a single recession. Estimation results are not sensitive to this modification vis-à-vis the actual NBER recession dating.

- The variables used to construct , namely Laubach and Williams’ estimate of the natural real rate of interest and FRB/US long-run inflation expectations, are available at quarterly frequency. We interpolate both variables at monthly frequency and sum them to obtain the monthly series.

- Our sample begins in 1966 because it was not until the second half of the 1960s that the FOMC began targeting a short-term interest rate—the Treasury bill rate first and the federal funds rate later (see Friedman 2000). Moreover, long-term inflation expectations data from FRB/US are currently available from only the first quarter of 1968 onward. We assume that expectations were constant at 1.68 percent—the 1968:Q1 value—before then. Given this assumption, we are reluctant to use too many observations from before 1968 in our baseline estimation. Nevertheless, the next section will show that our findings are robust to starting the estimation sample earlier.

- See, for example, Estrella, and Mishkin (1998), Wright (2006), and Rudebusch and Williams (2009).

- We chose this reporting approach for ease of presentation across specifications as well as our robustness checks. If instead we plotted the probability of a recession associated with a specific date, then the high probabilities of a recession before the three most recent economic downturns would more closely align with the start of the NBER’s recession periods (gray bars in the graph).

- We report predicted values from 1987 on only for the post-1987 estimation period.

- The simple analysis presented here abstracts from important issues associated with the fact that the neutral federal funds rate is a generated regressor, which complicates inference. However, we are concerned mainly with the predicted probabilities based on the point estimates, which are consistent. It is also likely that this neutral value is measured with error. Such measurement error could attenuate the estimated role of the monetary policy stance in predicting future downturns.

- Figure A.1 in the appendix shows the full set of recession probability predictions for three of the different stages of a recession that we consider.

References

Bauer, Michael D., and Thomas M. Mertens. 2018. “Economic Forecasts with the Yield Curve.” FRBSF Economic Letter 2018-07, March 5.

Engstrom, Eric, and Steven A. Sharpe. 2018. “The Near-Term Forward Yield Spread as a Leading Indicator: A Less Distorted Mirror.” Finance and Economics Discussion Series 2018-055, Board of Governors of the Federal Reserve System.

Estrella, Arturo, and Gikas A. Hardouvelis. 1991. “The Term Structure as a Predictor of Real Economic Activity.” The Journal of Finance 46(2): 555–576.

Estrella, Arturo, and Frederic S. Mishkin. 1998. “Predicting U.S. Recessions: Financial Variables as Leading Indicators.” Review of Economics and Statistics 80(1): 45–61.

Estrella, Arturo, and Mary R. Trubin. 2006. “The Yield Curve as a Leading Indicator: Some Practical Issues.” Current Issues in Economics and Finance (12)5: 1–7.

Friedman, Benjamin M. 2000. “The Role of Interest Rates in Federal Reserve Policymaking.” In The Evolution of Monetary Policy and the Role of the Federal Reserve in the Last Third of the Twentieth Century, edited by Richard W. Kopcke and Lynn E. Browne, 43–66. Boston, MA: Federal Reserve Bank of Boston.

Fuhrer, Jeffrey, Giovanni Olivei, Eric Rosengren, and Geoffrey Tootell. 2018. “Should the Fed Regularly Evaluate Its Monetary Policy Framework?” Brookings Papers on Economic Activity. Fall: 443–497.

Harvey, Campbell R. 1989. “Forecasts of Economic Growth from the Bond and Stock Markets.” Financial Analysts Journal 45(5): 38–45.

Holston, Kathryn, Thomas Laubach, and John C. Williams. 2017. “Measuring the Natural Rate of Interest: International Trends and Determinants.” Journal of International Economics 108(S1): 59—75.

Johansson, Peter, and Andrew Meldrum. 2018. “Predicting Recession Probabilities Using the Slope of the Yield Curve.” FEDS Notes, Board of Governors of the Federal Reserve System, March 1.

Laubach, Thomas, and John C. Williams. 2003. “Measuring the Natural Rate of Interest.” The Review of Economics and Statistics 85(4): 1063–1070.

Miller, David S. 2019. “There Is No Single Best Predictor of Recessions.” FEDS Notes, Board of Governors of the Federal Reserve System, May 21.

Rudebusch, Glenn, and John Williams. 2009. “Forecasting Recessions: The Puzzle of the Enduring Power of the Yield Curve.” Journal of Business & Economic Statistics 27(4): 492–503.

Stock, James H., and Mark W. Watson. 1989. “New Indices of Coincident and Leading Indicators,” in NBER Macroeconomic Annual 4, edited by Olivier J. Blanchard and Stanley Fischer, 351–394. Cambridge, MA: MIT Press.

Wright, Jonathan H. 2006. “The Yield Curve and Predicting Recessions.” Finance and Economics Discussion Series 2006-07, Board of Governors of the Federal Reserve System.

The views expressed herein are those of the authors and do not indicate concurrence by the Federal Reserve Bank of Boston, the principals of the Board of Governors, or the Federal Reserve System.

About the Authors

About the Authors

Daniel H. Cooper,

Federal Reserve Bank of Boston

Daniel H. Cooper is a vice president and economist in the research department at the Federal Reserve Bank of Boston.

Email: Daniel.Cooper@bos.frb.org

Jeff Fuhrer is an executive vice president and senior policy advisor at the Federal Reserve Bank of Boston. His email is Jeffrey-Fuhrer@hks.harvard.edu.

Giovanni P. Olivei,

Federal Reserve Bank of Boston

Giovanni P. Olivei is a senior vice president and deputy director of research at the Federal Reserve Bank of Boston.

Email: Giovanni.Olivei@bos.frb.org

Acknowledgments

The authors thank Hannah Rhodenhiser for help producing the figures.

Resources

Site Topics

Keywords

- term spread ,

- yield curve inversion ,

- recession probabilities

JEL Codes

- E43 ,

- E44