Firms’ Cash Holdings and Monetary Policy Transmission

Liquidity, particularly cash holdings, may serve as an important cushion for firms to absorb macroeconomic shocks such as interest rate increases so that these shocks have only minimal effects on their operations, at least in the short term. For example, to finance their investments, firms with high levels of cash may not have to tap so deep into debt financing, the cost of which relates closely to interest rates. Understanding the role of corporate cash holdings is therefore paramount to formulating appropriate monetary policy in the current environment. This brief informs the ongoing policy debate by examining the effect of US nonfinancial corporate cash holdings on the transmission of monetary policy, both historically and in the present tightening cycle.1 This brief shows that in the current hiking cycle, firms have used the cash they accumulated in 2020 and 2021 to finance operations, growth, and payouts. Due to this depletion of the accumulated-cash buffer, the effects of interest rate increases to date on corporate investment will likely gain traction in the coming quarters.

Sign up for Research Department Updates.

Similarly to how households amassed excess savings, firms accumulated unprecedented levels of cash and cash equivalents in 2020 and 2021, partly due to the vast public policy support in response to the COVID-19 crisis and a strong economic recovery.2 Importantly, however, recent data show that firms depleted most of this newly accumulated cash buffer in 2022. Historically, changes in the federal funds rate have been a less powerful monetary policy tool in affecting the investment activity of firms with higher levels of cash. We find that firms used the cash accumulated in 2020 and 2021 to increase investment, intangible assets, payouts (dividends and buybacks), and operating expenses during the current tightening cycle without issuing any additional debt.

Given the recent depletion of accumulated corporate cash holdings, however, the effects of the interest rate increases to date on corporate investment will likely gain traction in the coming quarters as costlier external funding becomes more relevant to financing investment and growth (see Bräuning, Joaquim, and Stein 2023 for a related analysis on the transmission of monetary policy to firms' interest expenses).

Firms' Liquid Assets and Cash Holdings

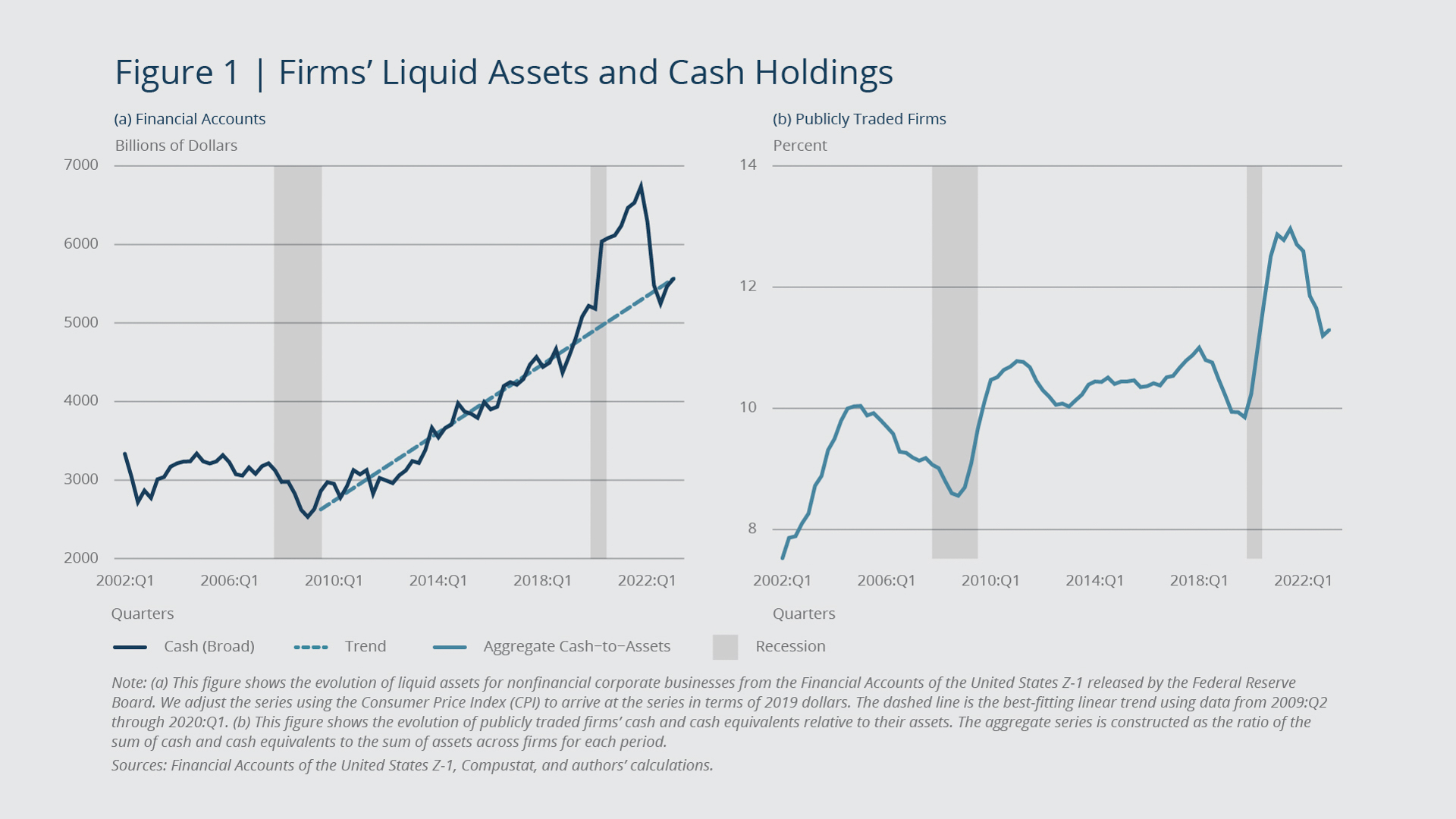

Figure 1a shows the evolution of liquid assets (in 2019 dollars) for nonfinancial corporate businesses, according to the Financial Accounts of the United States. After the financial crisis in 2008 and 2009, firms' cash holdings increased steadily, and then at the onset of the COVID-19 pandemic, they soared. While the initial surge in cash holdings in March 2020 may have been for precautionary reasons, the sharp increase was at least in part also a result of the unprecedented public policy support. Monetary and fiscal policies provided direct and indirect assistance to firms, including through very low interest rates that may have led many firms to front-load funding. The generally strong performance of the US economy in the post-pandemic recovery also contributed to the increase in cash holdings.

{kind=link}

Federal Reserve Bank of Boston

More recently, however, we have seen a large and steep decrease in this additional liquidity buffer accumulated during the COVID-19 period that has brought the nonfinancial corporate sector's cash holdings back to their pre-pandemic trend. We find similar trends when we use detailed financial statement information on publicly traded US firms from Compustat to analyze their cash and cash-equivalent holdings.3 Aggregating across all publicly listed firms, Figure 1b shows that firms' cash-to-assets ratio increased significantly during the immediate aftermath of the pandemic and has been declining since the beginning of the ongoing hiking cycle.

Cash Holdings and the Transmission of Monetary Policy

Given the large accumulation of cash in 2020 and 2021, this brief next studies the transmission of monetary policy to firms depending on their cash levels. First, the analysis focuses on the historical transmission of monetary policy shocks to firm investment. Second, we extend the analysis to the current hiking cycle to determine how the accumulated cash affected firms' balance sheets in 2022.

For the historical analysis, we take the sample of firms in the Compustat database from the first quarter of 1990 through the first quarter of 2008 (before the Global Financial Crisis) and separate them into two groups according to their cash-to-assets ratios.4 We use the monetary shocks from Swanson (2021) to estimate the differential transmission of monetary policy.5 We estimate the monetary policy effects using lag-augmented local projections (Jordà 2005; Montiel Olea and Plagborg-Møller 2021), a method used widely in the empirical macroeconomic literature.

{kind=link}

Federal Reserve Bank of Boston

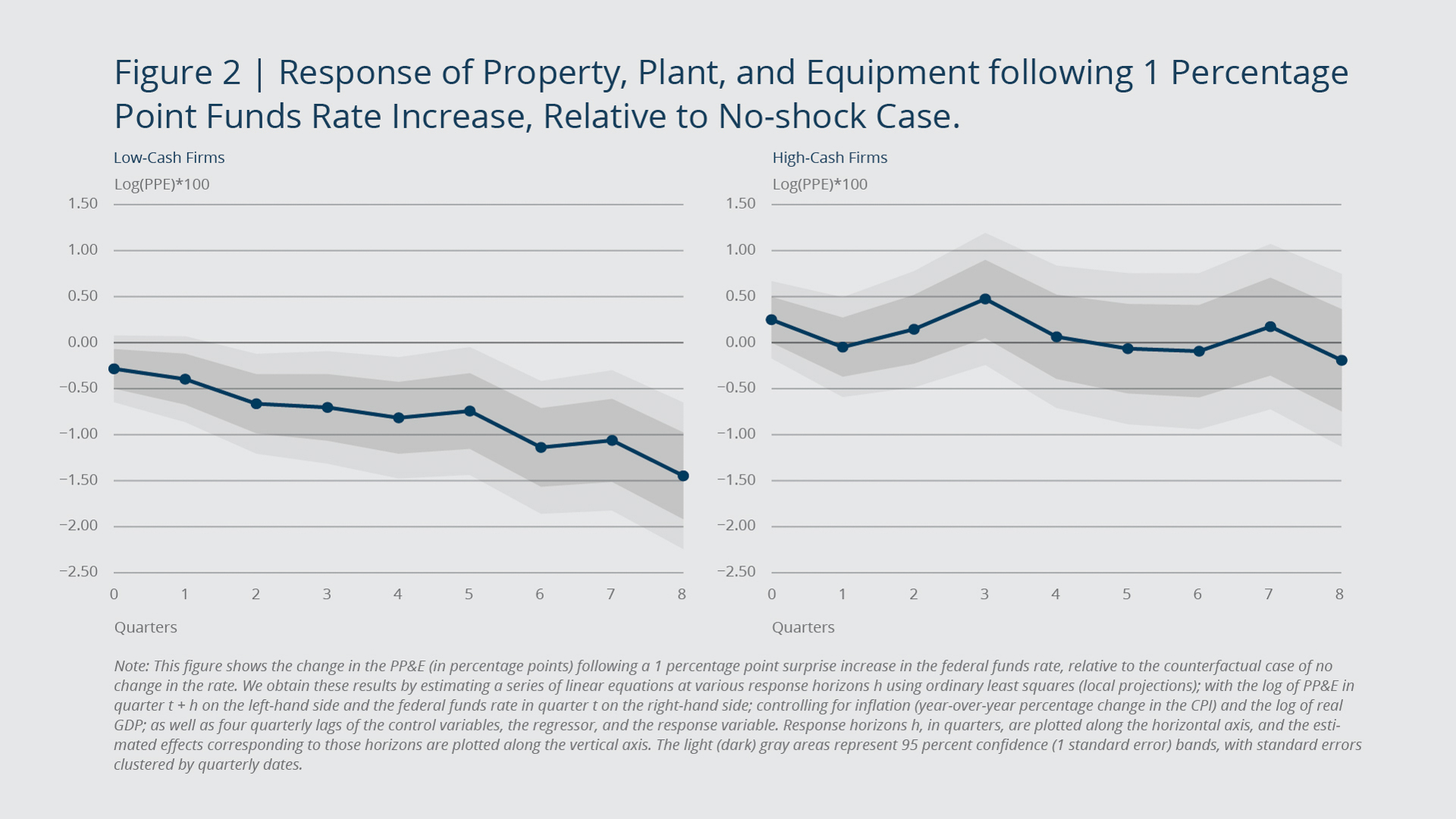

Figure 2 shows the response of property, plant, and equipment (PP&E)—a standard measure of firms' physical capital stock—following a surprise federal funds rate increase of 1 percentage point. We separate the responses of firms with high cash holdings from those of firms with low cash holdings. The left panel shows that the negative effect of monetary policy on low-cash firms' investment is large and significant, reducing investment to such an extent that it does not even cover depreciation and therefore leads to a reduction in the stock of capital. Moreover, the effect builds up gradually, consistent with the well-documented existence of lags in monetary policy transmission. About eight quarters after the rate increase, low-cash firms have a 1.5 percentage point smaller capital stock compared with the no-shock scenario. On the other hand, as the right panel shows, there is no significant effect on high-cash firms. The muted response of high-cash firms to monetary policy shocks is robust to a wide range of specifications, suggesting that the accumulation of cash in 2020 and 2021 may have dampened the transmission of monetary policy to the corporate sector.

To understand the impact that the COVID-19–period cash accumulation is having on firms in the current tightening cycle, we next assess how that accumulation affected key financial indicators across firms. For this analysis, we compute the firm-level growth in cash from the end of 2019 to the end of 2021 and correlate that growth with changes in firm-level variables in 2022. We do so while controlling for firm sector and size.

{kind=link}

Federal Reserve Bank of Boston

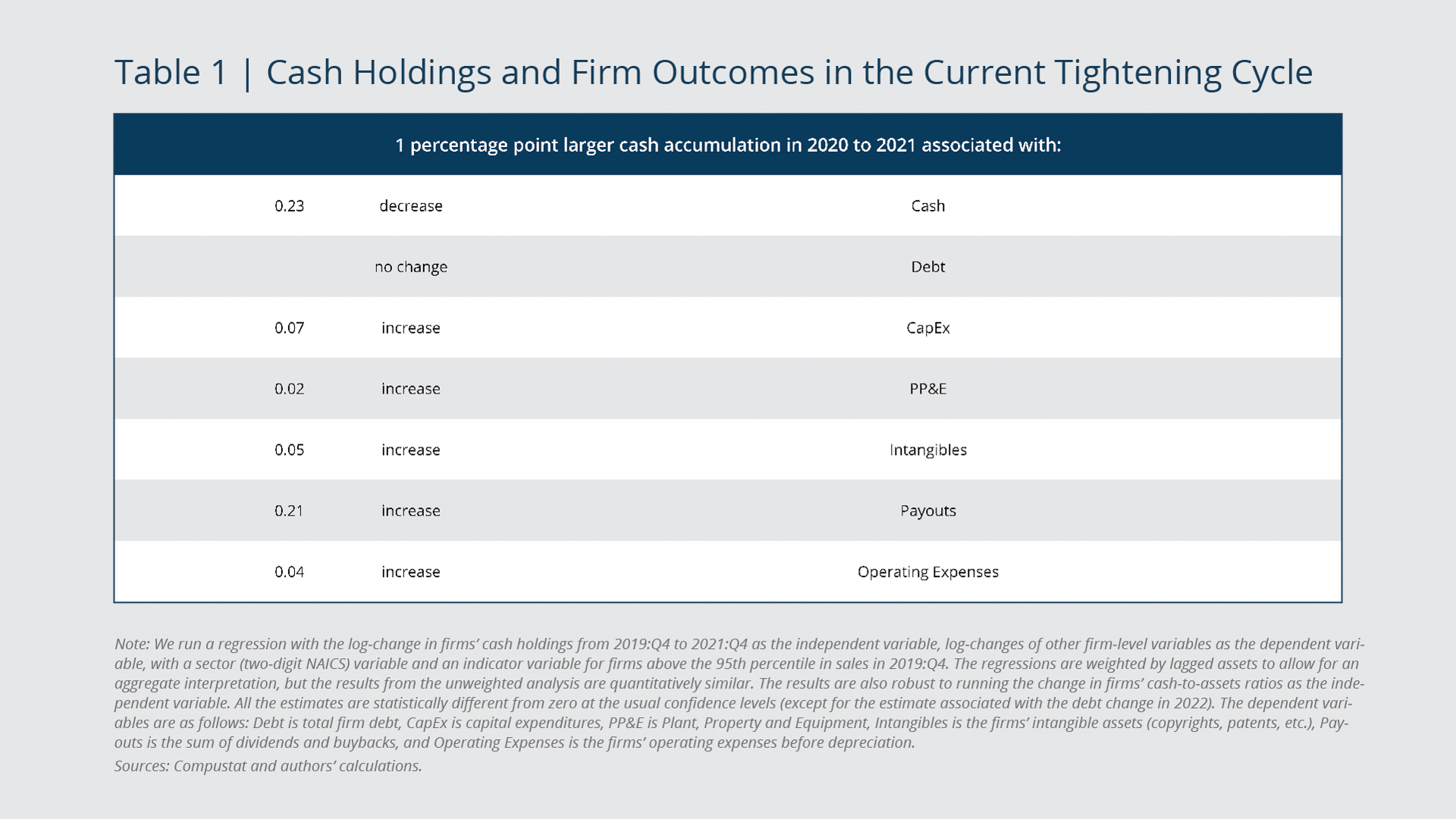

Table 1 shows the percentage point change in each variable resulting from a 1 percentage point greater accumulation of cash from 2019:Q4 to 2021:Q4. For each percentage point of additional cash accumulation in 2020 and 2021, firms saw a 0.23 percentage point larger decrease in their cash in 2022 and no differential change in debt. This finding indicates that firms, in fact, were using their newly accumulated cash in 2022. Moreover, firms used this cash to increase their capital expenditures (CAPEX), their stock of intangibles, payouts (dividends and buybacks), and operating expenses. These results suggest that cash accumulated in 2020 and 2021 has provided a cushion and, thus far in the current tightening cycle, has enabled firms to invest, grow, and distribute money to their shareholders with limited reliance on additional debt financing, which has become significantly more costly due to the large interest rate increases since 2022.

Conclusion

This brief highlights that firms accumulated an unprecedented level of cash and cash equivalents in 2020 and 2021. Historically, firms with higher cash levels have shown a muted investment response to monetary policy, whereas firms with lower cash levels have exhibited a significant decrease in investment. This brief shows that in the current hiking cycle, firms have relied on the cash they accumulated in 2020 and 2021 to finance operations, growth, and payouts. Due to this depletion of the accumulated-cash buffer, the effects of interest rate increases to date on corporate investment will likely gain traction in the coming quarters.

The views expressed herein are those of the authors and do not indicate concurrence by the Federal Reserve Bank of Boston, the principals of the Board of Governors, or the Federal Reserve System.

Endnotes

- In this brief, we refer to cash in the broad sense. From the Financial Accounts of the United States Z.1 released by the Federal Reserve Board, we use the total volume of liquid assets for nonfinancial corporate businesses, which comprises foreign deposits, checkable deposits and currency, time and savings deposits, money market fund shares, security repurchase agreements, debt securities, corporate equities, and mutual fund shares. Our results are qualitatively similar if we use alternative definitions. From Compustat data, we use a measure of cash and short-term investments that represents cash and all securities readily transferable to cash—often referred to as "cash equivalents."

- See, for instance, Aladangady, Cho, Feiveson, and Pinto (2022) and Abdelrahman and Oliveira (2023).

- As is common practice, our analysis of financial statements excludes firms in the following sectors: utilities, finance and insurance, public administration and government, gasoline stations, and postal services.

- We assign firms to the high-cash or low-cash group based on the median cash-to-assets ratio of all firms in a given industry in the same quarter. (Industries are identified by their two-digit North American Industry Classification System, or NAICS, code) Note that the results are robust to computing high-cash firms after controlling for size effects (sales, assets, etc.). Therefore, the documented differential effect depending on cash is not driven by size differences.

- Since both monetary policy and firms' investment depend on current and future economic conditions, we use unexpected monetary shocks for identification. These monetary shocks are computed from high-frequency changes of asset prices around Federal Open Market Committee meetings (see Swanson 2021).

References

Abdelrahman, H., and L.E. Oliveira. 2023. "The Rise and Fall of Pandemic Excess Savings." FRBSF Economic Letter. May 8.

Aladangady, A., D. Cho, L. Feiveson, and E. Pinto. 2022. "Excess Savings during the COVID-19 Pandemic." FEDS Notes. October 21.

Bräuning, F., G. Joaquim, and H. Stein. 2023. "Interest Expenses, Coverage Ratio, and Firm Distress." Federal Reserve Bank of Boston Current Policy Perspectives. August 29.

Jordà, O. 2005. "Estimation and Inference of Impulse Responses by Local Projections." American Economic Review 95(1): 161–182.

Montiel Olea, J. L., and M. Plagborg-Møller. 2021. "Local Projection Inference Is Simpler and More Robust than You Think." Econometrica 89(4): 1789–1823.

Swanson, E. T. 2021. "Measuring the Effects of Federal Reserve Forward Guidance and Asset Purchases on Financial Markets." Journal of Monetary Economics 118: 32–53.

About the Authors

About the Authors

Falk Bräuning,

Federal Reserve Bank of Boston

Falk Bräuning is a vice president and economist in the Federal Reserve Bank of Boston Research Department.

Email: falk.braeuning@bos.frb.org

José L. Fillat,

Federal Reserve Bank of Boston

José L. Fillat is a principal economist and policy advisor in the Federal Reserve Bank of Boston Research Department.

Email: Jose.Fillat@bos.frb.org

Gustavo Joaquim

Acknowledgments

The authors thank Philippe Andrade, Daniel Cooper, Giovanni Olivei, Joe Peek, Jenny Tang, and Vaishali Garga for useful comments and discussions. Lucy McMillan provided excellent research assistance.

Resources

Site Topics

Keywords

- monetary policy transmission ,

- cash accumulation ,

- investment

JEL Codes

- E22 ,

- E52 ,

- G30

Citation

Stavins, Joanna. 2023. “Credit Card Spending and Borrowing since the Start of the COVID-19 Pandemic.” Federal Reserve Bank of Boston Current Policy Perspectives. October 18, 2023.