Could the Growth of Private Credit Pose a Risk to Financial System Stability?

Default Title

Default Title

{kind=link}

Federal Reserve Bank of Boston

The views expressed herein are solely those of the authors and should not be reported as representing the views of the Federal Reserve Bank of Boston, the principals of the Board of Governors, or the Federal Reserve System.

The private credit (PC) market has grown rapidly in recent years, approaching the lending volume of some traditional sources of business credit, including commercial and industrial (C&I) loans from banks, broadly syndicated loans (BSLs), and high-yield bonds. The term “private credit” refers to lending by nonbanks—such as business development companies (BDCs) and other investment vehicles—that, our analysis shows, is typically indirectly funded by bank credit; banks are not involved in underwriting or issuing PC loans. Private credit ranges from direct lending, which is similar to bank lending, to purchasing businesses’ distressed debt and other practices that do not directly compete with banks.1

Sign up for Research Department Updates.

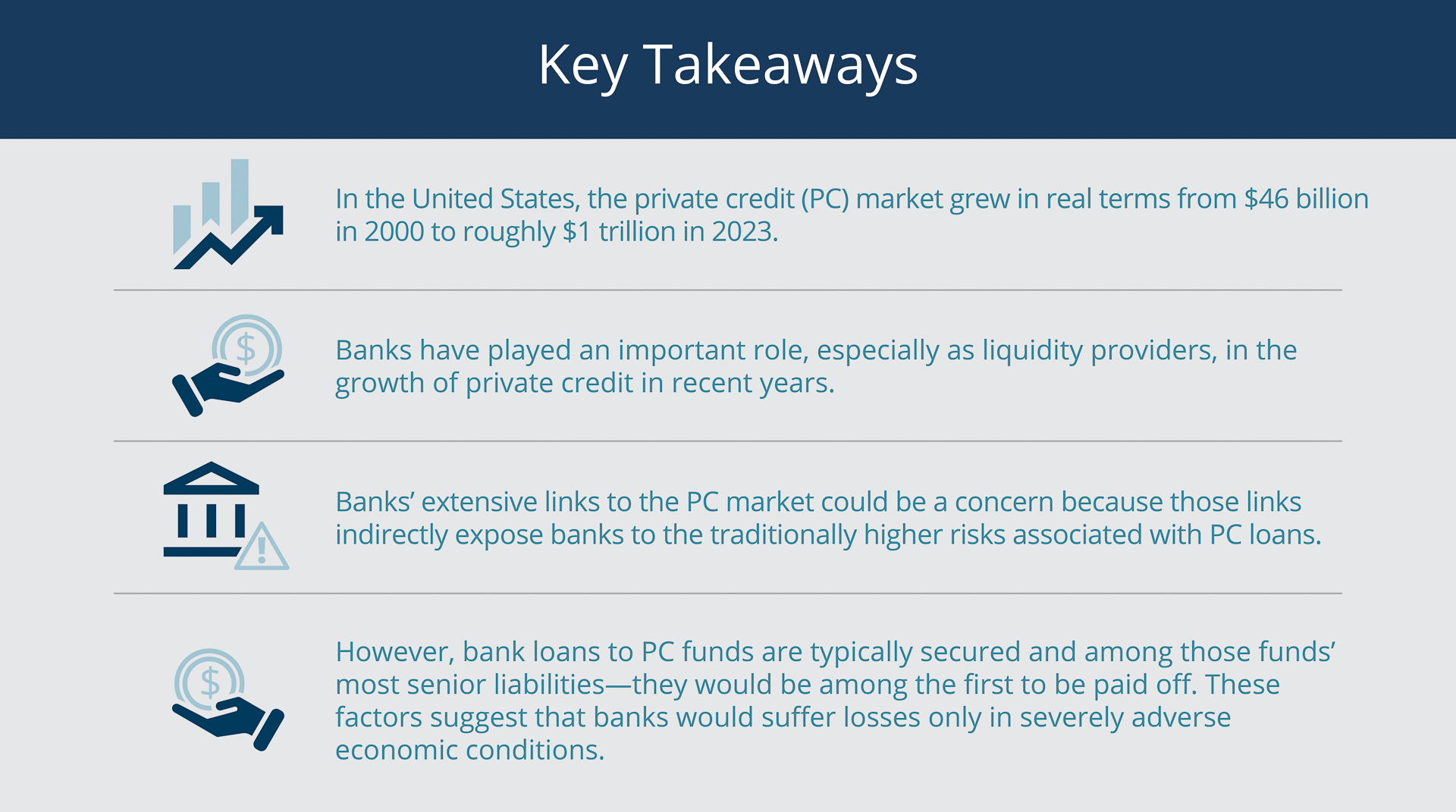

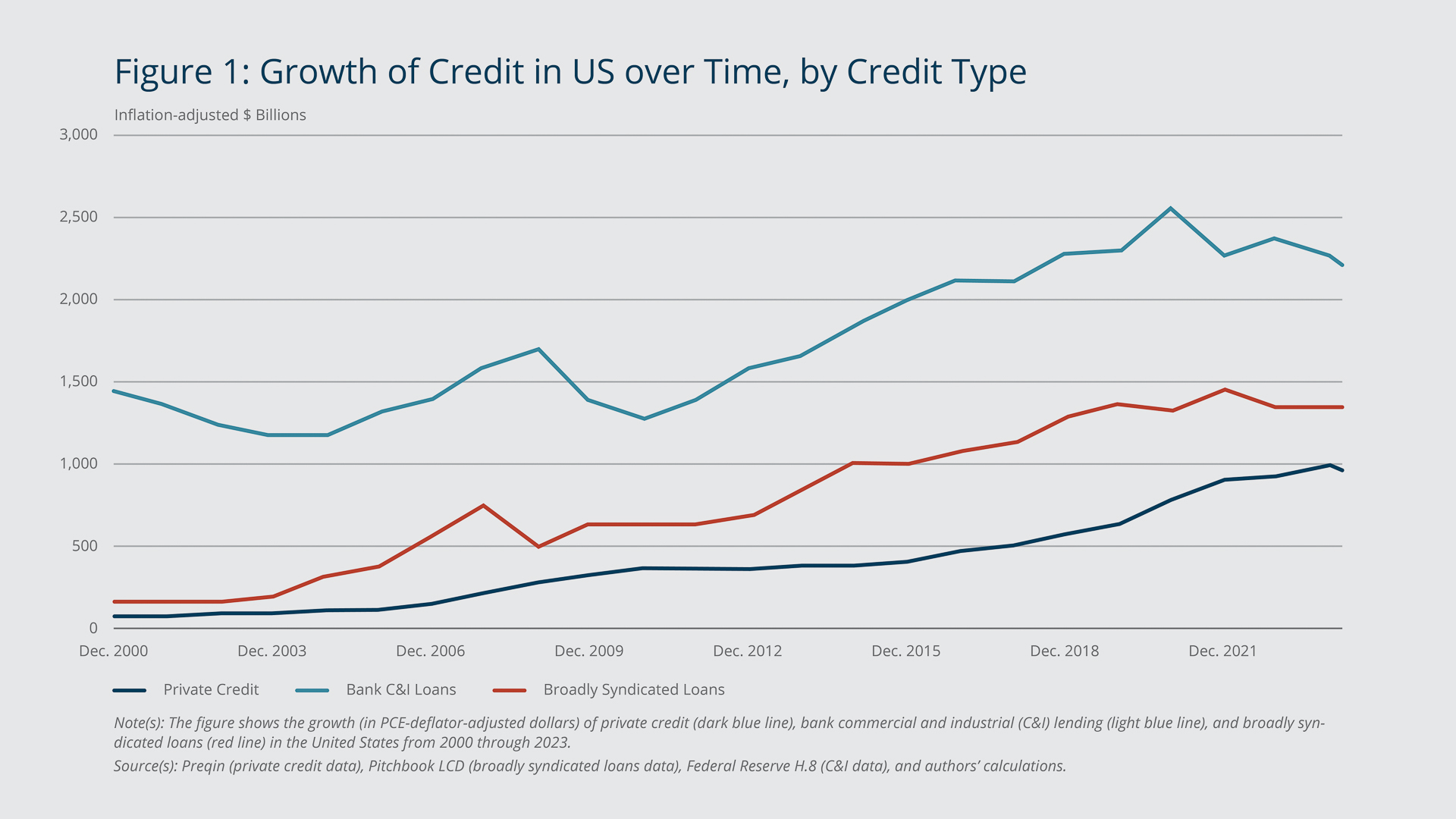

In the United States, the private credit market grew in real terms from $46 billion in 2000 to roughly $1 trillion in 2023, with the growth accelerating notably after 2019 (Figure 1) due mostly to direct lending.2 Broadly syndicated loans (large loans originated by banks and distributed to a group of investors, typically other banks and institutional investors) and high-yield bonds (corporate bonds issued by lower-rated corporations that offer higher interest rates due to the higher credit risk) are the two prominent forms of business credit with which PC lending competes. According to the commercial data provider Pitchbook LCD (formerly Leveraged Commentary and Data), broadly syndicated lending represented $1.3 trillion of debt as of the last quarter of 2023, while high-yield bonds represented $1.6 trillion, according to the International Monetary Fund’s Global Financial Stability Report (IMF 2024).

{kind=link}

Federal Reserve Bank of Boston

The volume of commercial and industrial loans, which are issued by individual banks to businesses and are the largest form of non-traded business credit, reached $2.8 trillion in 2023, up from $1.3 trillion (adjusted for inflation) in 2000.

The meteoric rise of private credit presents important questions about the role of banks going forward and the implications for stability in the US financial system. How likely is direct PC lending to replace banks as a key source of business credit? If that happens, will it raise or lower the level of systemic risk? If, instead, banks and private credit continue to coexist, will banks eventually lend mostly to PC funds rather than directly to businesses?

Our analysis of Federal Reserve and proprietary loan-level data indicates that the growth of private credit has been funded largely by bank loans and that banks have become a key source of liquidity, in the form of credit lines, for PC lenders. Banks’ extensive links to the PC market could be a concern because those links indirectly expose banks to the traditionally higher risks associated with PC loans. Such concerns would be mitigated if PC lending is growing by capturing a share of the business credit market from banks rather than by expanding the market through riskier loans that banks are not willing to make.3

Private Credit Loans Look Increasingly Similar to Bank Loans

Private credit loans, although diverse, share similarities with C&I loans and broadly syndicated loans, but they also exhibit distinct features. Banks originate both BSLs and C&I loans. After origination, BSLs are generally traded in secondary markets, while C&I and PC loans remain on lenders’ balance sheets. C&I borrowers come in all sizes, but the vast majority are smaller businesses that have not been assessed by a credit rating agency. Conversely, PC loans and BSLs tend to be targeted to midsize and large businesses, respectively. BSL borrowers are typically risky; that is, they are below investment grade or do not have a credit rating. In addition, BSLs and PC loans are both often issued to finance leveraged buyouts by private equity funds.

As private credit funds have grown in scale, PC loans have become larger, and their terms and borrower characteristics have come to look more like those of BSLs.4 Similarly, PC loan spreads—the difference between the interest rate that PC lenders charge borrowers and the reference risk-free interest rate—have historically been wider than either BSL or C&I loan spreads, but they have contracted in recent years. Our examination of the data shows that the spreads of loans held in business development company portfolios have narrowed by about 1 percentage point in the last decade, to about 6 percentage points.

We derive our findings on loan spreads from granular Pitchbook LCD data on BDCs, which constitute a relatively transparent subset of the PC sector. Even though BDCs account for only a slice of the broader PC market, the patterns gleaned from BDC portfolios should be generally applicable to non-BDC PC funds, according to our discussions with industry participants and to findings by, for example, Suhonen (2023). To the best of our knowledge, our analysis is the first to quantify bank lending to BDCs using loan-level data.

Implications of Growth due to Substitution versus Expansion

These developments in which PC credit increasingly resembles bank-issued credit suggest that a growing number of PC loans are being made to borrowers that might otherwise seek bank loans. (We provide evidence of this convergence of PC and bank lending in detail in the appendix accompanying this brief.) The extent to which the increase in PC lending represents credit substitution (lending to borrowers that might otherwise seek BSLs or other bank loans) versus credit expansion (issuing loans that banks would not issue) has implications for the potential risks that PC growth poses to financial-system stability.5

If PC funds are capturing credit market share from banks rather than expanding the market through risky loans, it would be because they offer more favorable terms than banks or more desirable loan features. However, because spreads on BDC loans (as indicated earlier, a proxy for PC credit) typically are much wider than bank loan spreads, it is highly unlikely that PC credit offers more attractive pricing. Therefore, other, non-price terms for PC loans would have to be more attractive than those of bank loans. These terms could include greater flexibility or better management expertise. Absent these more favorable non-price terms, the difference between PC and bank loan rates would indicate that PC loans require a higher return due solely to lenders’ greater credit risk exposure. Understanding what drives the differences in price and non-price terms between PC loans and bank loans is necessary for assessing the broader financial stability implications of private credit growth.

If the growth of PC lending represents mostly a shift in credit provision from banks to PC funds, it could reduce overall financial stability risk because PC funds tend to employ lower leverage than banks (that is, they have lower debt-to-equity ratios), and they pose less run risk than banks, as described in a recent Federal Reserve Board “Financial Stability Report” (BOG 2023). PC funds are less vulnerable to runs because their limited partners are locked up contractually for multiple years, whereas three-quarters of bank funding consists of run-prone demand deposits, almost half of which are uninsured (according to Federal Deposit Insurance Corporation data on Assets and Liabilities of Commercial Banks in the US; see FDIC 2024).

On the other hand, if PC lending has grown because lenders have been making riskier loans that banks would not make, then aggregate credit risk in the financial system likely would rise. In fact, not only would the financial sector be effectively more leveraged, but the added leverage would be on the balance sheets of riskier borrowers, weakening these businesses’ resilience to shocks and, as a result, rendering the financial system less stable.

Banks Are First in Line among Private Credit Funds’ Creditors

Our finding that bank lending to business development companies has been growing, both as a share of banks’ total loan balances and as a share of BDCs’ balance sheets, is consistent with recent research that finds banks have increased their lending to private equity and private credit funds broadly (Levin and Malfroy-Camine 2025). This finding suggests that banks retain indirect exposure to the credit risk of private credit loans even though they do not directly originate or hold those loans.

To the extent that BDCs and other PC funds’ shareholder equity and other liabilities (for example, subordinated long-term debt) are subordinate to bank loans, banks’ secured credit lines represent the seniormost debt instruments issued by PC lenders, meaning that PC lenders have to pay off their bank loans before any other debt. In that respect, even though loans made by BDCs and other PC funds are not explicitly securitized (pooled and sold as securities), the capital structure of BDCs and other PC funds resembles that of a collateralized loan obligation (CLO)—a securitization with various risk slices, or tranches—in which banks hold the highest rated (lowest risk) tranche.

Extending that analogy to some of the risks identified from past experiences with CLOs could inform the assessment of financial stability risks posed by PC funds. For example, the systematic component of the credit risk embedded in the AAA-rated tranche tended to be underpriced in the years leading up to the 2008 financial crisis, meaning that the risk was higher than the returns indicated (Coval et al. 2009).

The Role of Bank Loans in Private Credit Growth

Federal Reserve Y-14 data provide evidence that banks represent a nontrivial portion of private lenders’ liabilities. Here, we explore the role of banks, in particular those with more than $100 billion in total consolidated assets, in funding private credit firms as proxied by business development companies.6

The Y-14 data filed by these bank holding companies (which we refer to as “Y-14 banks”) contain loan and borrower characteristics for all commercial loans with a balance of more than $1 million. We find that each publicly traded BDC had a loan or loans at some point from at least one of the banks that filed Y-14 data during the 2013:Q1–2023:Q4 period. Using Compustat data on BDC balance sheets to complement the Y-14 data, we find that borrowing from banks represented a large portion of the funding that fueled BDC asset growth after 2000.

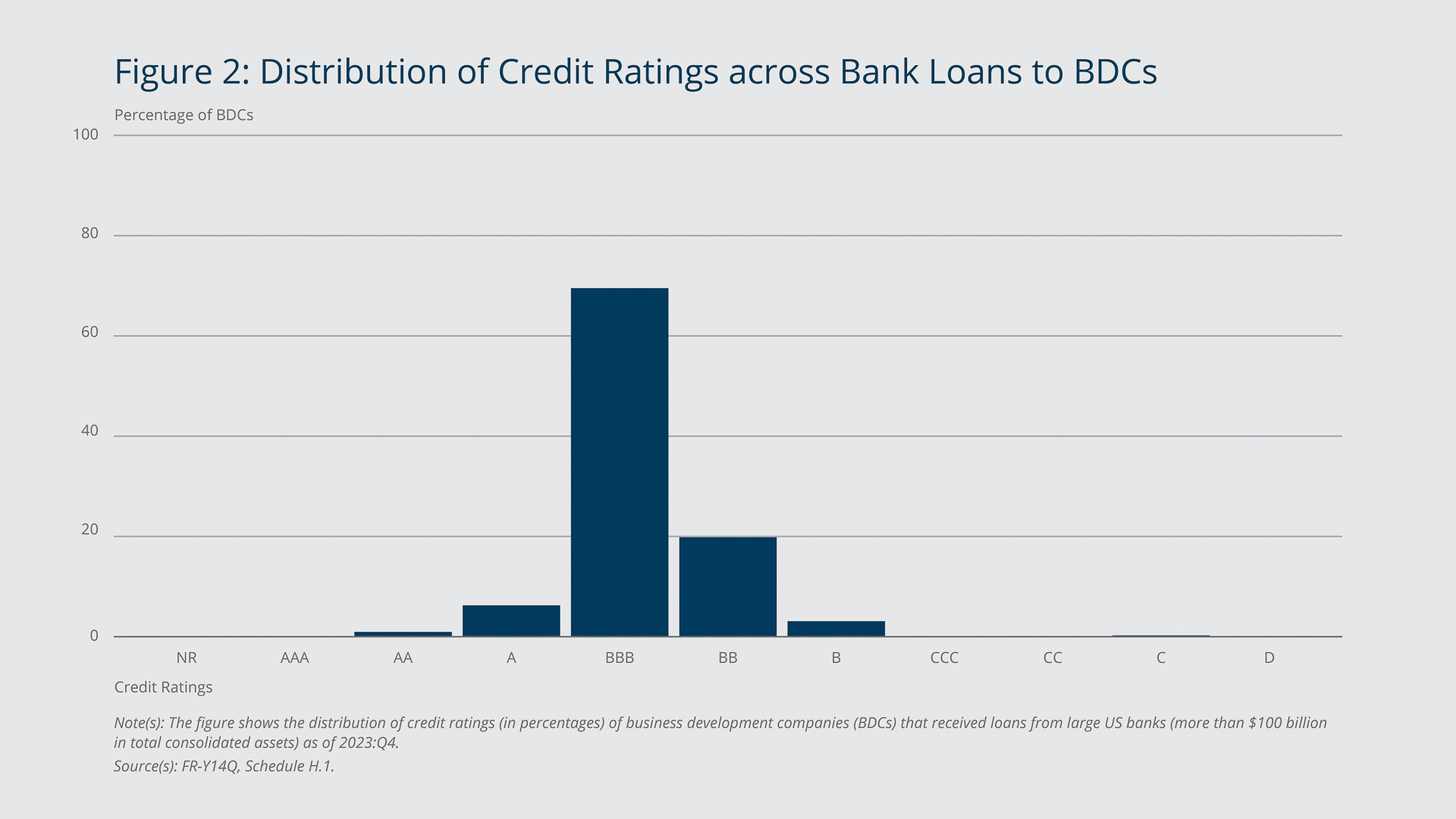

In contrast to the spreads that BDCs charge their borrowers—now, as noted, about 6 percentage points—the spreads that BDCs pay on the loans they obtain from banks lie between 2.0 and 2.1 percentage points. This is consistent with the fact that nearly 80 percent of the BDCs that obtain loans from the largest US banks are rated BBB or higher (Figure 2).

{kind=link}

Federal Reserve Bank of Boston

Figure 3 plots the time series of the amount (adjusted for inflation) of credit that Y-14 banks extended to BDCs from the start of 2013 through the end of 2023. The figure also depicts the relevance of this credit relative to BDCs’ assets. We estimate that approximately $1 billion in loans was committed. Broadly speaking, the volume of Y-14 credit rose noticeably after 2020. At the same time, the amount of Y-14 credit remained relatively stable as a share of BDCs’ assets, with the notable exception of the COVID-19 period, when bank lending declined significantly.

{kind=link}

Federal Reserve Bank of Boston

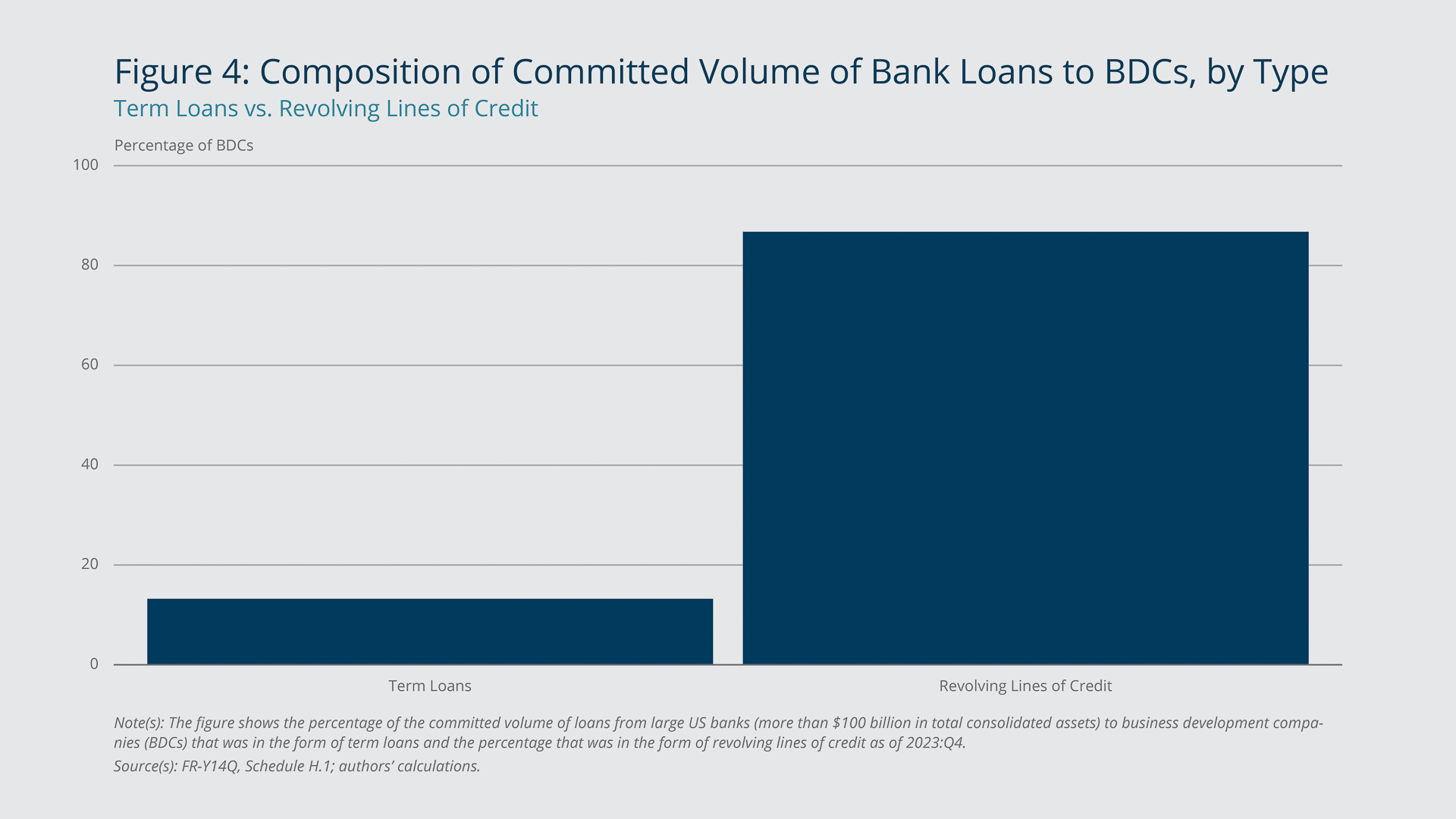

Enhanced Creditor Control and ‘Dry Powder’ May Mitigate Risk Transmission

Banks’ primary role in the liability structure of business development companies is to provide liquidity. Most bank loans to BDCs are revolving lines of credit, as opposed to term loans (Figure 4). In addition, a large share of these lines of credit (about 30 percent) remained undrawn as of 2023:Q4, while about 18 percent were fully drawn (Figure 2A in the appendix), reinforcing the notion that liquidity is the main role of bank loans to PC lenders. Moreover, the BDCs in our sample kept a significant portion of that liquidity on standby. PC lenders could use those undrawn credit lines, in addition to committed equity, to support troubled borrowers.

{kind=link}

Federal Reserve Bank of Boston

Such liquidity could be a double-edged sword. On one hand, it would improve credit availability during difficult economic times. On the other hand, it could enable over-leveraging by highly risky borrowers during an economically buoyant period. However, the heightened potential for excessive credit expansion during boom times is mitigated by enhanced creditor control over PC loans, relative to broadly syndicated loans, and potentially also by the availability of “dry powder”—capital already committed by investors but not yet invested.

Furthermore, as indicated earlier, most of the Y-14 bank exposure to BDCs is in the form of first-lien senior secured loans—97 percent of the total dollar volume—giving banks priority among creditors in the event of default (Figure 5).

{kind=link}

Federal Reserve Bank of Boston

PC lenders’ reliance on banks for liquidity could pose systemic liquidity risk to the banking sector if a sufficient number of PC lenders (BDCs and other PC funds) draw down on their bank credit lines simultaneously in response to adverse aggregate shocks. However, because bank loans to PC funds are typically secured and among those funds’ most senior liabilities, banks would suffer losses only in severely adverse economic conditions, such as a deep and protracted recession. But losses could also occur in a less adverse scenario if the default correlation among the loans in PC portfolios turned out to be higher than anticipated—that is, if a larger-than-expected number of PC borrowers defaulted at the same time. Such tail risk may be underappreciated.

Endnotes

- Throughout the paper we refer to bank holding companies (BHCs) as banks, for simplicity. Our analysis relies on data at the BHC level.

- We obtained those totals from the investment data company Preqin. Total market size includes the unrealized value of private credit funds, excluding committed but uninvested capital, or “dry powder.” All the dollar figures are reported in constant 2023 dollars.

- The importance of this distinction is highlighted in, for example, Stein (2013).

- The average private credit loan and deal size has grown in recent years (Cai and Haque 2024). The number and size of jumbo deals also have risen, from five reported deals in 2019 with an average size of $1.71 billion (adjusted for inflation) to 42 reported deals in 2023 with an average size of $2.39 billion, as reported by Kroll Bond Rating Agency (KBRA), a rating agency that specializes in private credit.

- For evidence of direct competition, see, for example, Abhinav Ramnarayan and Kat Hidalgo, “Wall Street Reclaims $16 Billion of Deals Lost to Private Credit,” Bloomberg, April 11, 2024. https://www.bloomberg.com/news/articles/2024-04-11/wall-street-reclaims-16-billion-of-deals-lost-to-private-credit

- Y-14 data are collected for capital assessments and stress-testing purposes and therefore only banks subject to stress tests disclose this information.

References

Board of Governors of the Federal Reserve System (BOG). 2023. “Financial Stability Report May: 2023.” https://www.federalreserve.gov/publications/2023-may-financial-stability-report-purpose-and-framework.htm

Cai, Fang, and Sharjil Haque. 2024. “Private Credit: Characteristics and Risks.” Board of Governors of the Federal Reserve System FEDS Notes. February 23. https://www.federalreserve.gov/econres/notes/feds-notes/private-credit-characteristics-and-risks-20240223.html

Coval, Joshua D., Jakub W. Jurek, and Erik Stafford. 2009. “Economic Catastrophe Bonds.” American Economic Review 99(3): 628–66. https://doi.org/10.1257/aer.99.3.628

Federal Deposit Insurance Corporation (FDIC). 2024. “FDIC Statistics at a Glance: December 2024 Statistics.” FCIC Quarterly Banking Profile. https://www.fdic.gov/quarterly-banking-profile/fdic-statistics-glance

International Monetary Fund (IMF). 2024. “The Last Mile: Financial Vulnerabilities and Risks.” Global Financial Stability Report. April. https://www.imf.org/en/Publications/GFSR/Issues/2024/04/16/global-financial-stability-report-april-2024

Levin, John, and Antoine Malfroy-Camine. 2025. “Bank Lending to Private Equity and Private Credit Funds: Insights from Regulatory Data.” Federal Reserve Bank of Boston Supervisory Research and Analysis Notes. February. https://www.bostonfed.org/publications/supervisory-research-and-analysis-notes/2025/bank-lending-to-private-equity-and-private-credit-funds.aspx

Stein, Jeremy C. 2013. “Overheating in Credit Markets: Origins, Measurement, and Policy Responses.” Speech at the “Restoring Household Financial Stability after the Great Recession: Why Household Balance Sheets Matter” research symposium. Federal Reserve Bank of St. Louis, St. Louis, Missouri. https://www.federalreserve.gov/newsevents/speech/stein20130207a.htm

Suhonen, Antti. 2023. “Direct Lending Returns.” Financial Analysts Journal 80(1): 57–76. https://doi.org/10.1080/0015198X.2023.2254199

About the Authors

About the Authors

José L. Fillat,

Federal Reserve Bank of Boston

José L. Fillat is a principal economist and policy advisor in the Federal Reserve Bank of Boston Research Department.

Email: Jose.Fillat@bos.frb.org

Mattia Landoni,

Federal Reserve Bank of Boston

Mattia Landoni is a senior financial economist in the Federal Reserve Bank of Boston Supervision, Regulation & Credit Department.

Email: Mattia.Landoni@bos.frb.org

John D. Levin,

Federal Reserve Bank of Boston

John D. Levin is a senior markets specialist in the Federal Reserve Bank of Boston Supervision, Regulation & Credit Department.

Email: john.levin@bos.frb.org

J. Christina Wang,

Federal Reserve Bank of Boston

J. Christina Wang is a principal economist and policy advisor in the Federal Reserve Bank of Boston Research Department.

Email: Christina.Wang@bos.frb.org

Acknowledgments

The authors thank Kenechukwu Anadu and Falk Bräuning for helpful guidance and Sean Baker, Kelly Jackson, and Stephen Shannon for support with data.

Resources

Site Topics

Keywords

- private credit ,

- banking linkages ,

- liquidity provision

JEL Codes

- G2 ,

- G23 ,

- G32

Citation

Fillat, José L., Mattia Landoni, John D. Levin, and J. Christina Wang. 2025. “Could the Growth of Private Credit Pose a Risk to Financial System Stability?” Federal Reserve Bank of Boston Current Policy Perspectives 25-8.