New England Economic Conditions through May 28, 2024

Key Takeaways

- Employment growth in New England has slowed so far this year compared with 2023 and 2022, and as of April, the total number of nonfarm payroll jobs in the region had surpassed its February 2020 level by less than half of a percentage point. Furthermore, the region’s employment recovery from the COVID-19 pandemic was in fact weaker than previously estimated, according to recent data revisions released by the US Bureau of Labor Statistics.

- The region’s unemployment rate was slightly higher in April 2024 than it was one year earlier, but at least some (and possibly all) of the increase in unemployment can be explained by increased labor force participation. Furthermore, layoff rates also declined in the region in March 2024 compared with the previous year.

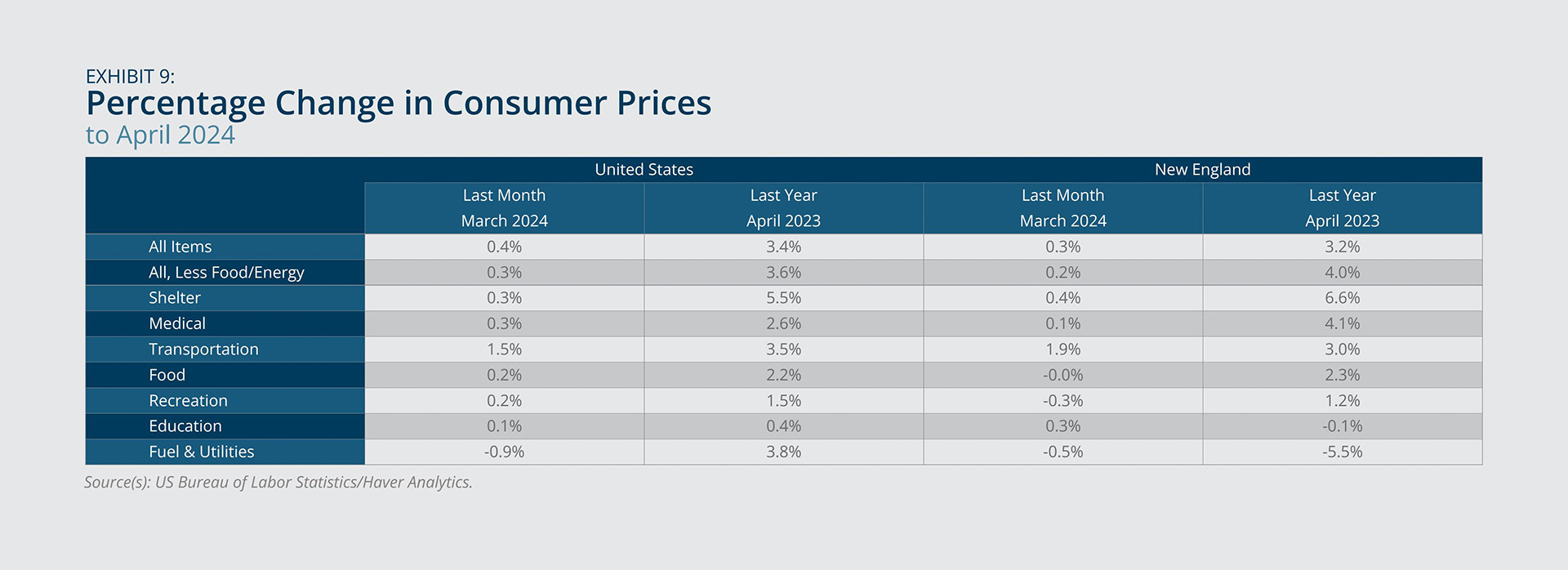

- New England’s inflation rate increased sharply in March 2024 from the previous month and increased slightly further in April, narrowing the gap with the US rate. Contributing to that development, New England experienced faster growth in shelter and medical care prices than the United States for the 12 months ending in April 2024.

- Real (inflation-adjusted) wages and salaries of private-industry workers in New England increased on a year-over-year basis in the first quarter of 2024. Although the rate of increase, at 0.6 percent, was modest, it marks a significant improvement from the negative real wage and salary growth observed for New England workers in the first quarter of 2023.

Sign up for new research and data on the New England economy.

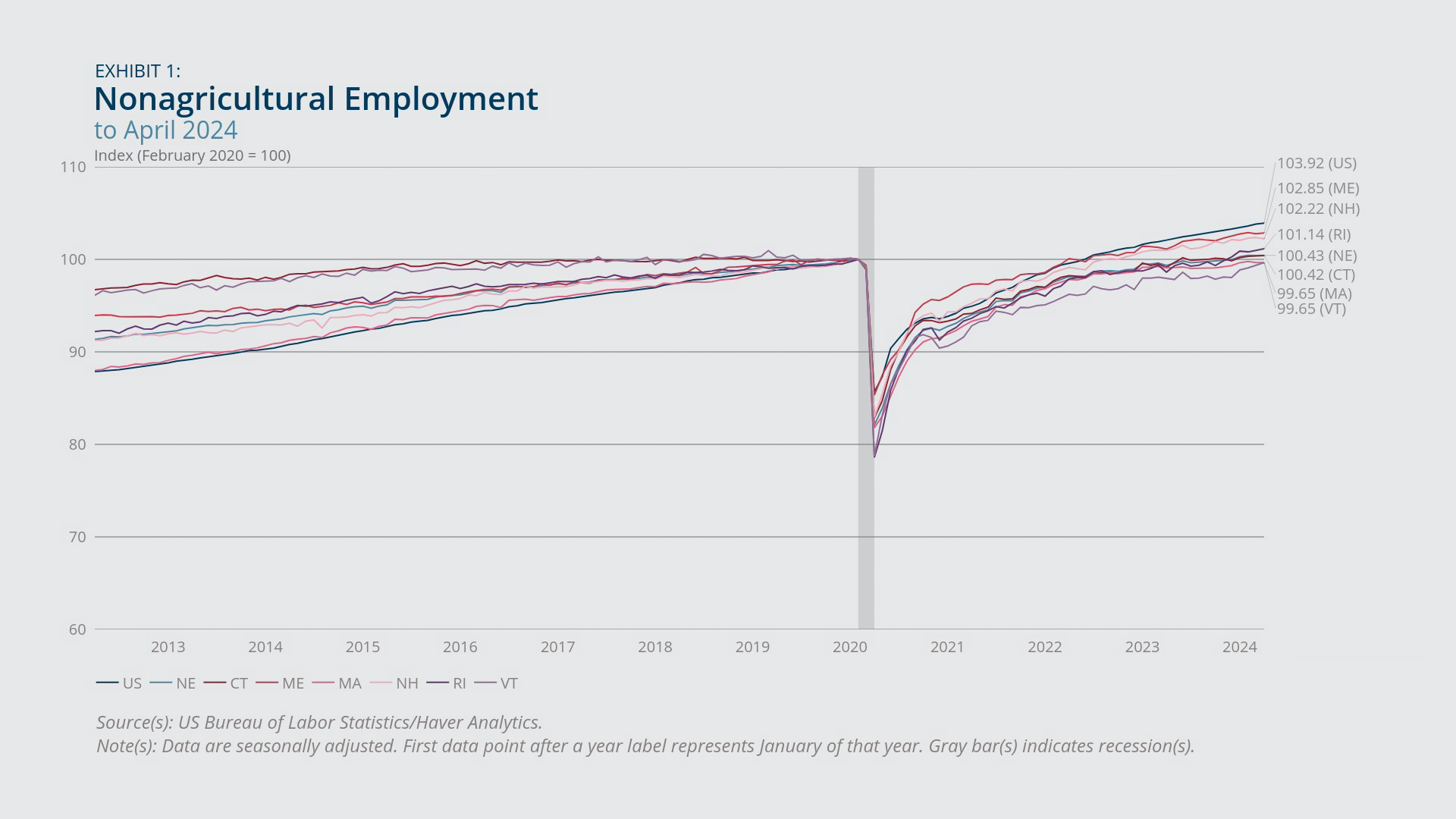

Payroll Employment

- Payroll employment has been roughly flat in New England in the past few months and remains just barely above its February 2020 level. Employment growth (on a year-over-year basis) has slowed in 2024 in both New England and the United States.1

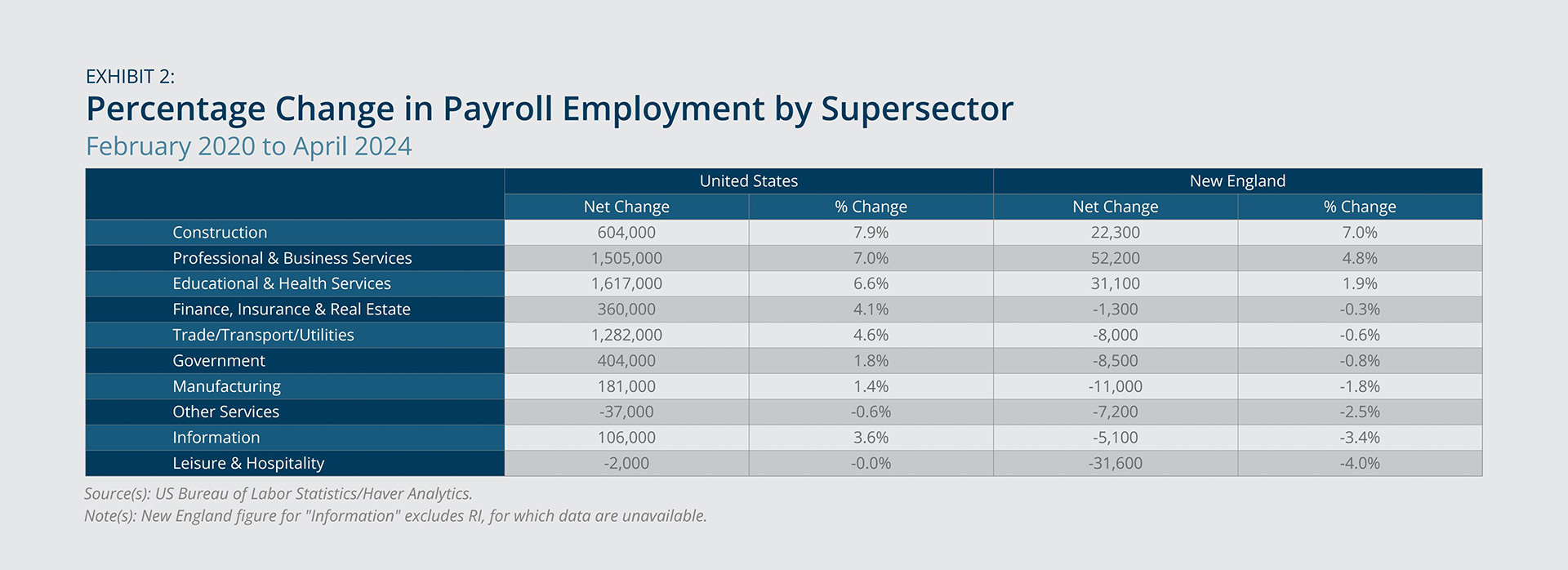

- The sectoral composition of the New England economy has shifted since February 2020, as three sectors have more than fully recovered their pandemic-associated job losses and other sectors have lost jobs on net.

Through April 2024, the region as a whole had experienced effectively zero net change in payroll jobs since February 2024 (Exhibit 1). Despite the lack of progress on employment for the region as a whole in recent months, jobs have surged in Vermont so far in 2024 and increased modestly in Rhode Island as well. The region’s employment growth pace (year-over-year) has been relatively steady at about 1 percent since mid-2023 but is down considerably from the rates observed in 2022 and the first half of 2023. Employment growth in the United States, while still stronger than in New England in the latest data, has also slowed since mid-2023.

When we look at payroll employment by supersector in New England relative to February 2020 (Exhibit 2), a picture emerges of a very lopsided recovery from the pandemic. Only three sectors have experienced net job growth since February 2020—construction, professional and business services, and education and health services. All of New England’s remaining sectors had fewer jobs as of April 2024 than before the pandemic, suggesting that the composition of jobs has shifted significantly in that time period. For the United States, the data suggest a more broadly based recovery.

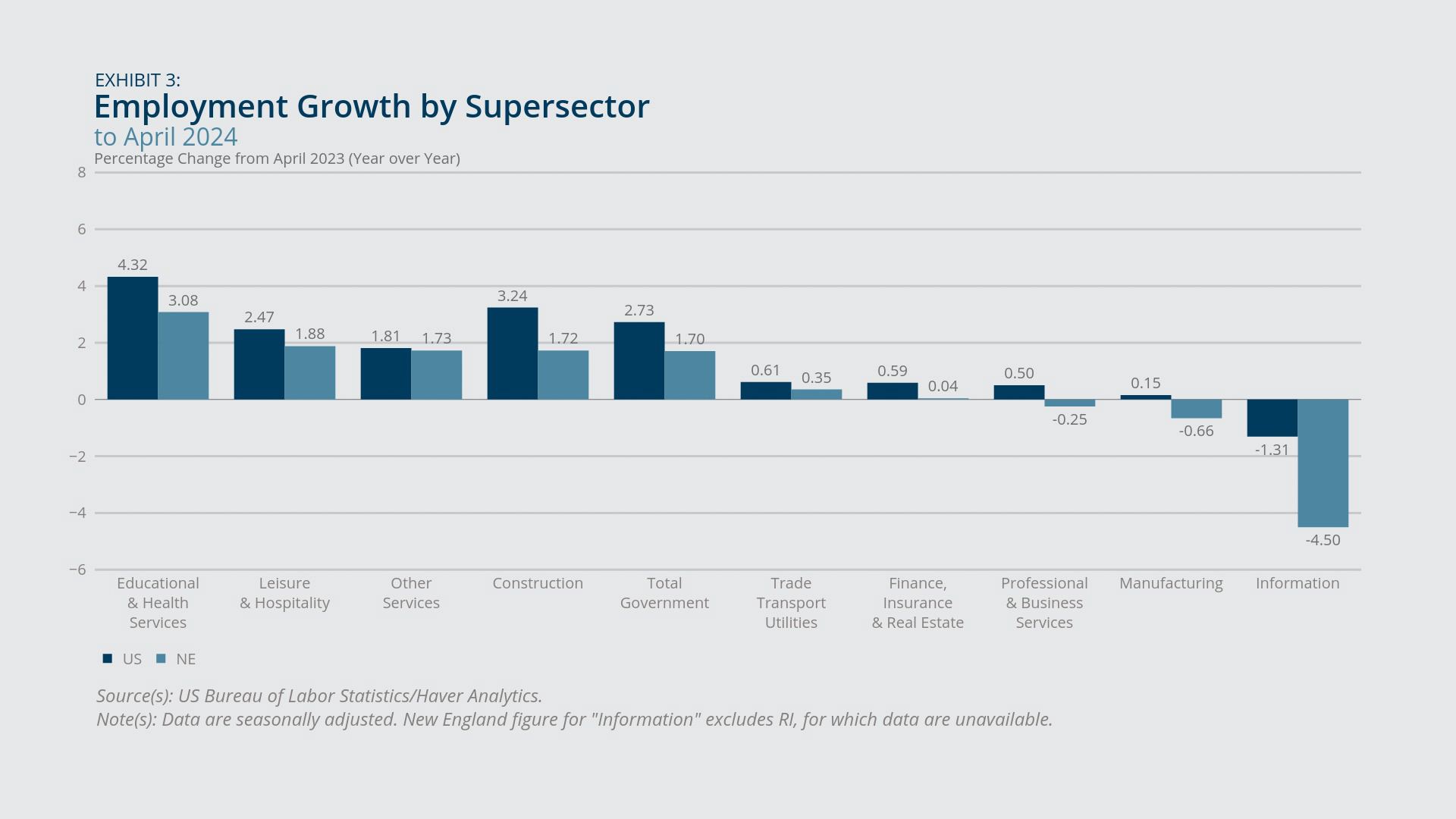

Other disparities emerge when we look at job growth by supersector from April 2023 to April 2024 (Exhibit 3). Education and health services experienced above-average job growth for the region, and within that sector (data not shown), employment growth was stronger in the health care and social assistance industry (3.3 percent) than in education services (1.1 percent). The information sector stands out with a 4.5 percent decline in jobs over the year. If recent job cuts at public broadcasters GBH and WBUR in Boston are indicative, information sector job losses reflect ongoing structural changes both in how people consume information and in how it is produced.2

{kind=link}

Federal Reserve Bank of Boston

{kind=link}

Federal Reserve Bank of Boston

{kind=link}

Federal Reserve Bank of Boston

Unemployment and Labor Force Participation

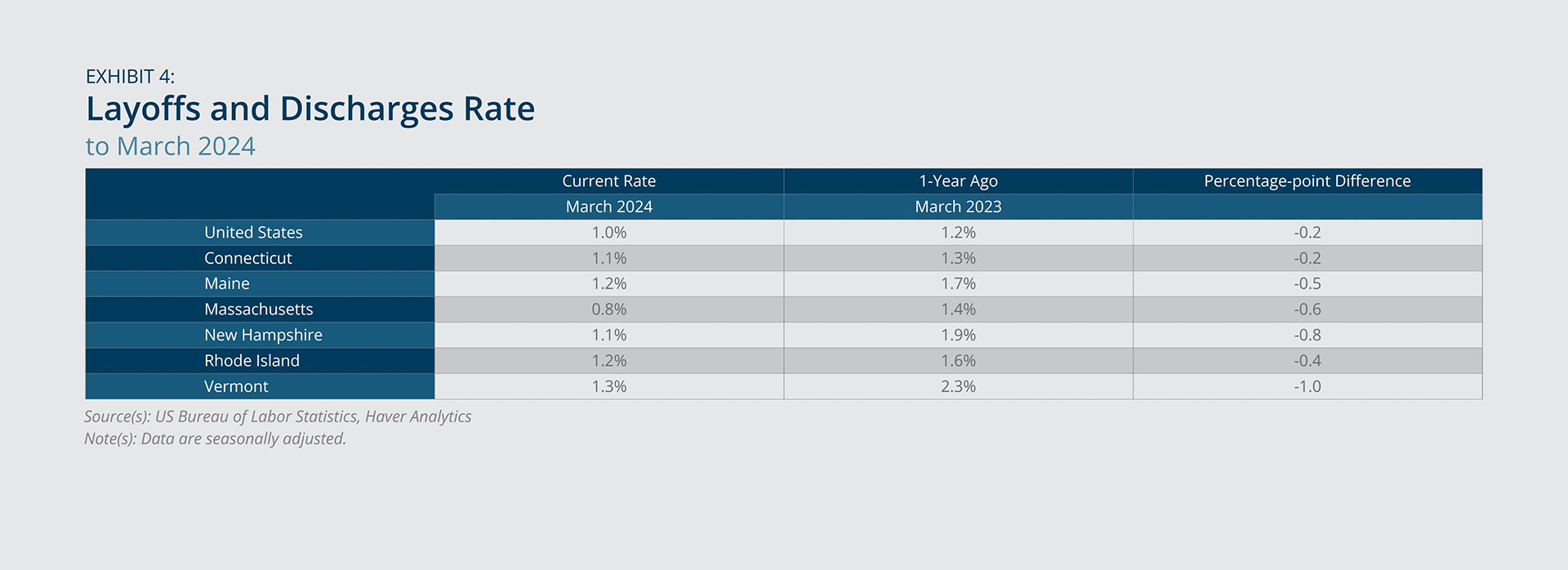

- Layoffs and discharge rates declined in all New England states and for the United States as a whole on a year-over-year basis to March 2024, and each New England state except Connecticut experienced steeper declines in layoffs and discharges than the US averages (Exhibit 4).

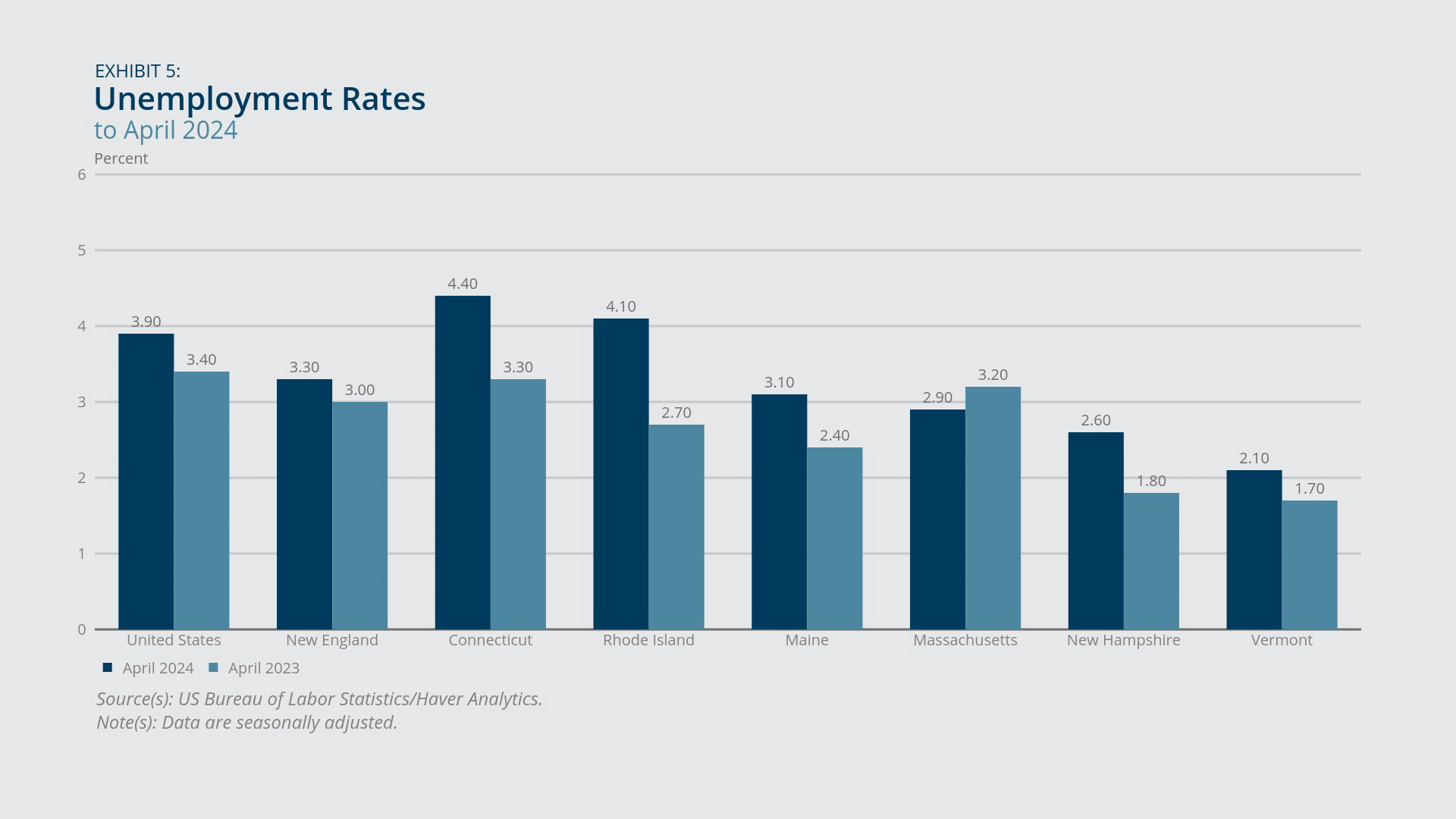

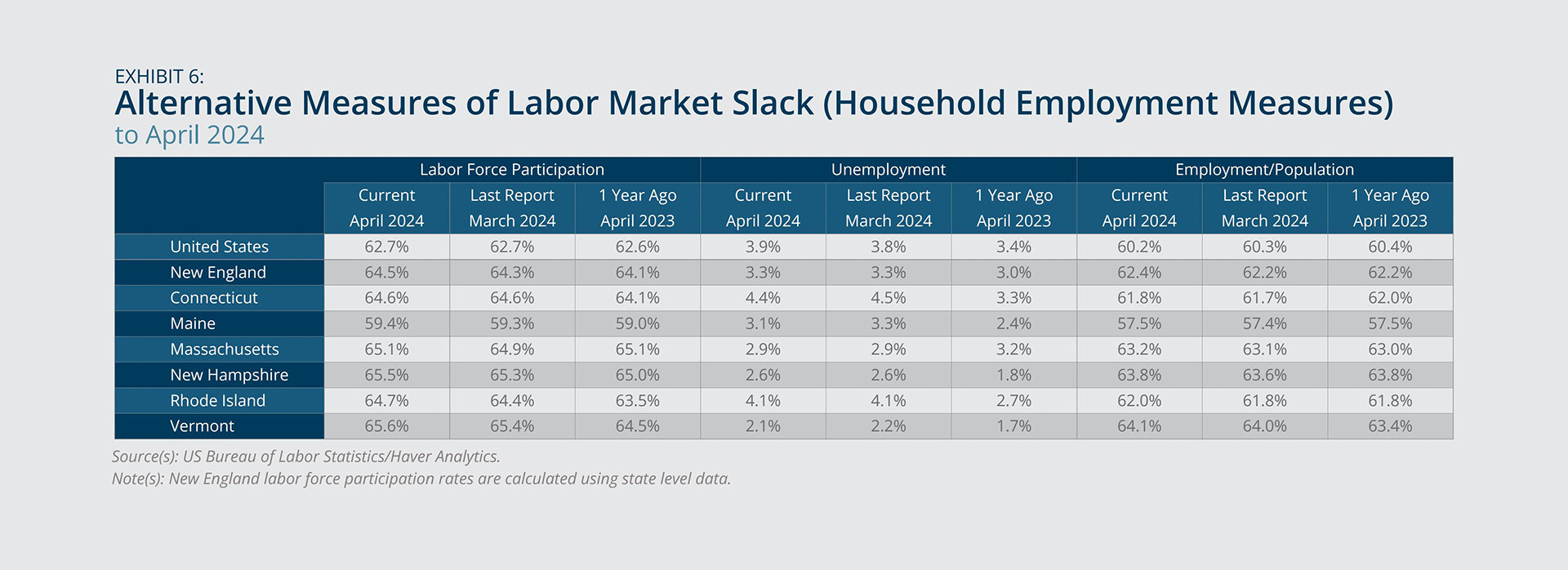

- Despite the declines in layoffs, the unemployment rate in April 2024 was higher than in April 2023 in five of the six New England states and in the region (and the United States) as a whole (Exhibit 5). Massachusetts saw a modest decline in its unemployment rate for the same time period, mitigating the overall increase in New England.

The higher unemployment rates in the five New England states appear to have been driven in part by increased labor force participation, as participation rates increased in the same five states that experienced increased unemployment (Exhibit 6). The declines in layoffs (Exhibit 4) reinforce the story that unemployment rates increased primarily because more people joined the labor force. Furthermore, for the region as a whole, the raw number of labor force participants increased by more than did the number of unemployed individuals over the period in question, suggesting that increased participation could more than explain the rise in the unemployment rate.3 However, the combination of lower layoff rates and higher unemployment rates might also imply that laid off individuals spent more time finding new jobs.

Massachusetts’ unemployment rate decline occurred in the context of a stable labor force participation rate. Furthermore, only in Connecticut did the higher unemployment rate (relative to April 2023) imply a lower employment-to-population ratio, as elsewhere in the region employment-to-population ratios were stable or up slightly in the past year (Exhibit 6). Compared with New England, the United States experienced a relatively large increase in its unemployment rate, a relatively small increase in its labor force participation rate, and a small decline (rather than an increase) in the employment-to-population ratio in April 2024 compared with one year earlier.

{kind=link}

Federal Reserve Bank of Boston

{kind=link}

Federal Reserve Bank of Boston

{kind=link}

Federal Reserve Bank of Boston

Wages and Prices

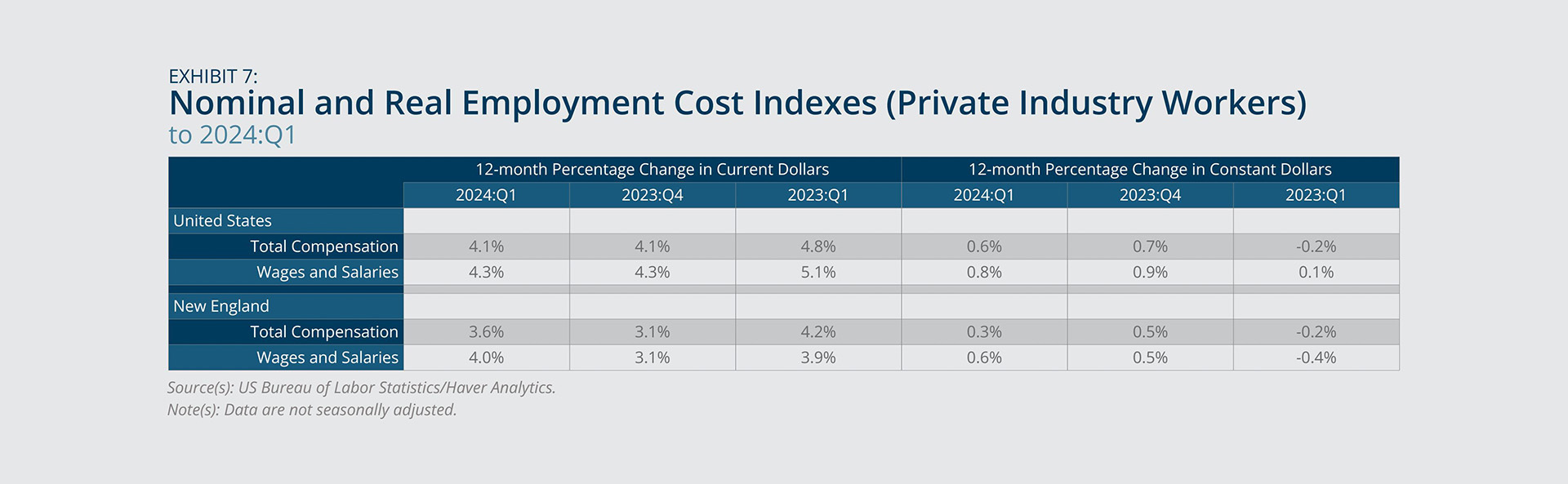

- Growth in real pay (either total compensation or wages and salaries) shifted from negative to positive territory in the first quarter of 2024 compared with one year earlier, according to the inflation-adjusted Employment Cost Indexes (Exhibit 7).

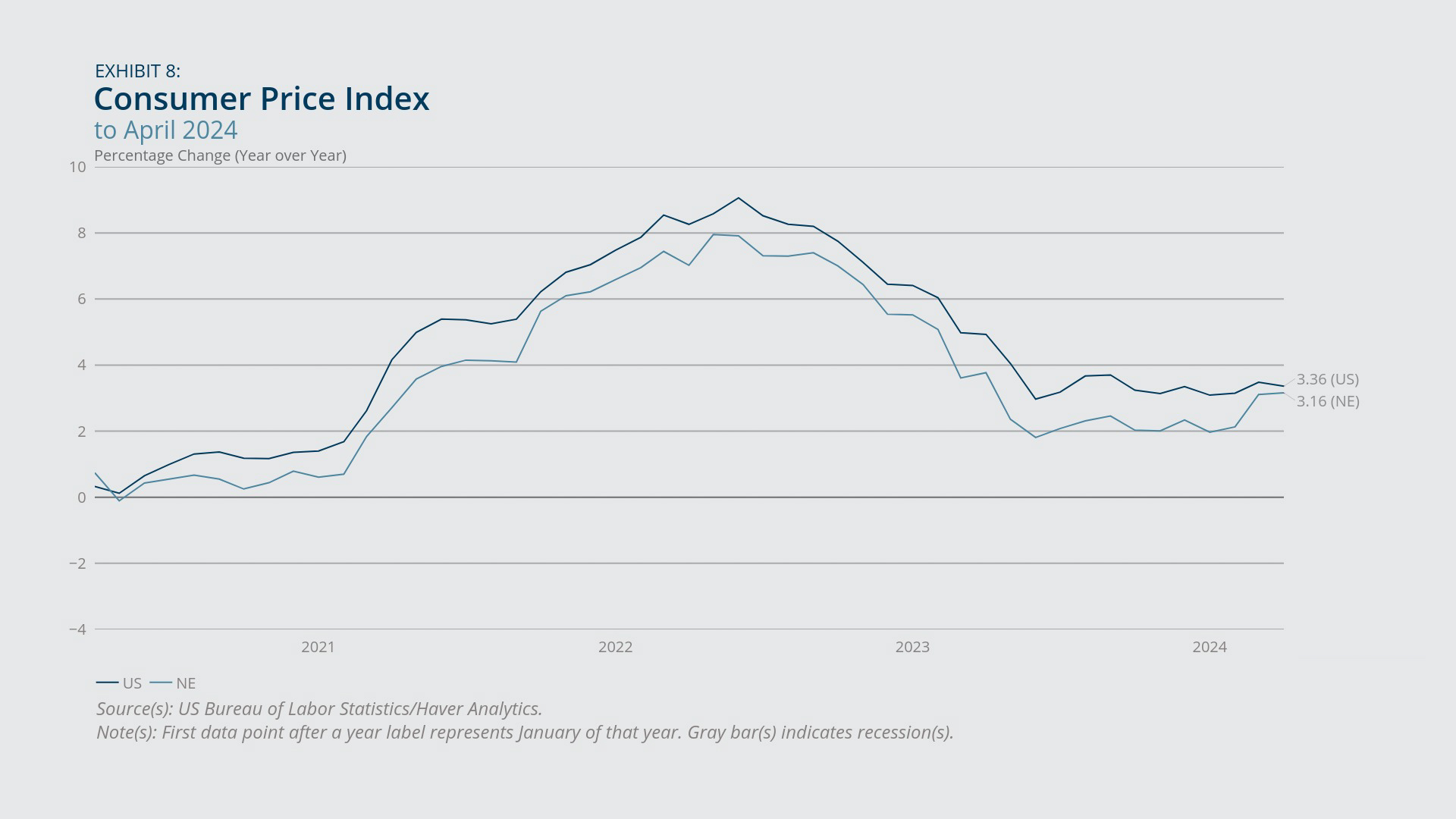

- The downward trend in Consumer Price Index (CPI) inflation has stalled since the second quarter of 2023 in both New England and the United States (Exhibit 8).

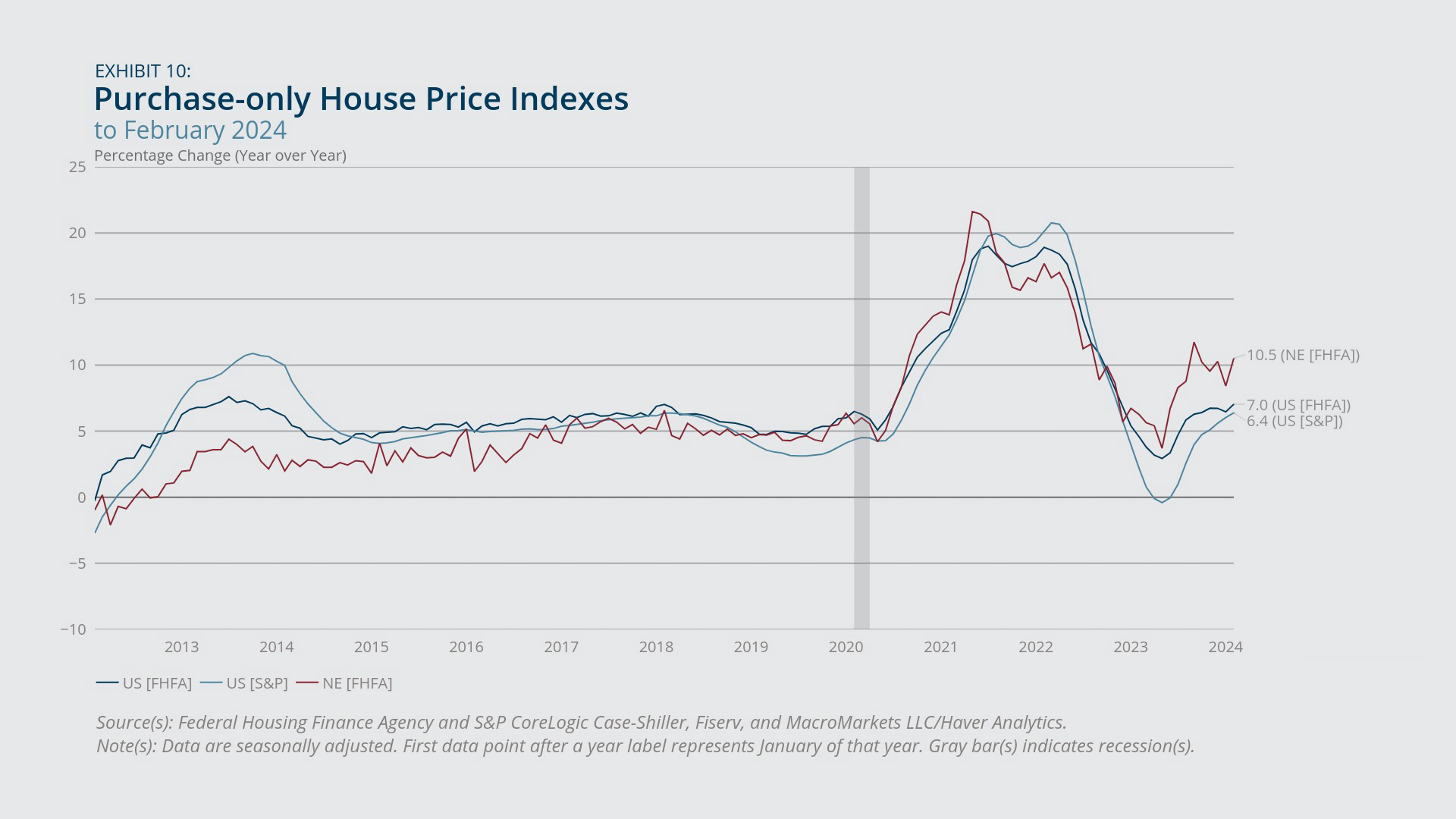

- House price growth in New England has recently surged ahead of the US average, contributing to a narrowing of the inflation gap between the region and the nation.

According to the Employment Cost Indexes (ECI) for New England, the growth rate (on a year-over-year basis) in nominal (current dollar) wages and salaries for private-sector workers was slightly higher in the first quarter of 2024 compared with one year earlier (4.0 percent versus 3.9 percent) and was up considerably from the 3.1 percent growth pace seen in the fourth quarter of 2023 (Exhibit 7). The growth rate in nominal total compensation in the region also picked up in 2024:Q1 from the previous quarter but was nonetheless lower by 0.6 percentage point compared with the first quarter of last year. For the United States, growth rates in nominal pay (either wages and salaries or total compensation) as of 2024:Q1 were unchanged compared with 2024:Q3 but were down from their year-earlier levels by at least 0.7 percentage point. For New England as well as for the United States, growth rates of real pay increased in 2024:Q1 compared with one year earlier, rising from small negative values to modest positive ones, although real pay growth was generally slightly slower in the latest data compared with the previous quarter. The sign reversals for real pay growth reflect declining price inflation over the relevant time period. For nominal and real measures alike, ECI growth rates remained lower for New England than for the United States.

Following steep declines from mid-2022 through mid-2023 in both the United States and New England, all-items Consumer Price Index (CPI) inflation moved roughly sideways but with some fluctuations. From June 2023 through February 2024, that measure stayed in the range of 1.8 to 2.5 percent in New England and between 3 and 3.7 percent for the United States. However, New England’s inflation rate increased sharply in March 2024 from the previous month and increased slightly further in April, narrowing the gap with the US rate, which nonetheless was also up somewhat in March and in April compared with February (Exhibit 8). That recent development reflects the fact that New England experienced faster growth in shelter and medical care prices than the United States for the 12 months ending in April 2024 (Exhibit 9). The transportation component stands out for its very high one-month growth rates, at 1.9 percent in New England and 1.5 percent in United States, and more detailed data (not shown) reveal that increases in gasoline prices were mostly to blame.4

Consistent with the CPI data on shelter prices, the Federal Housing Finance Agency (FHFA) house price indexes show that house price growth in New England has accelerated since May 2023, reaching a 10.5 percent year-over-year pace as of February 2024 (Exhibit 10). House price appreciation also picked up in the United States since May, albeit less dramatically, landing at 7 percent according to the FHFA index and slightly lower based on the S&P index. In Beige Book reports from the Federal Reserve First District over the past year, residential real estate contacts have consistently pointed to the severe shortage of homes for sale as a key driver of house price growth, although in the most recent reports, contacts in some New England states reported at least halting progress on inventories.5

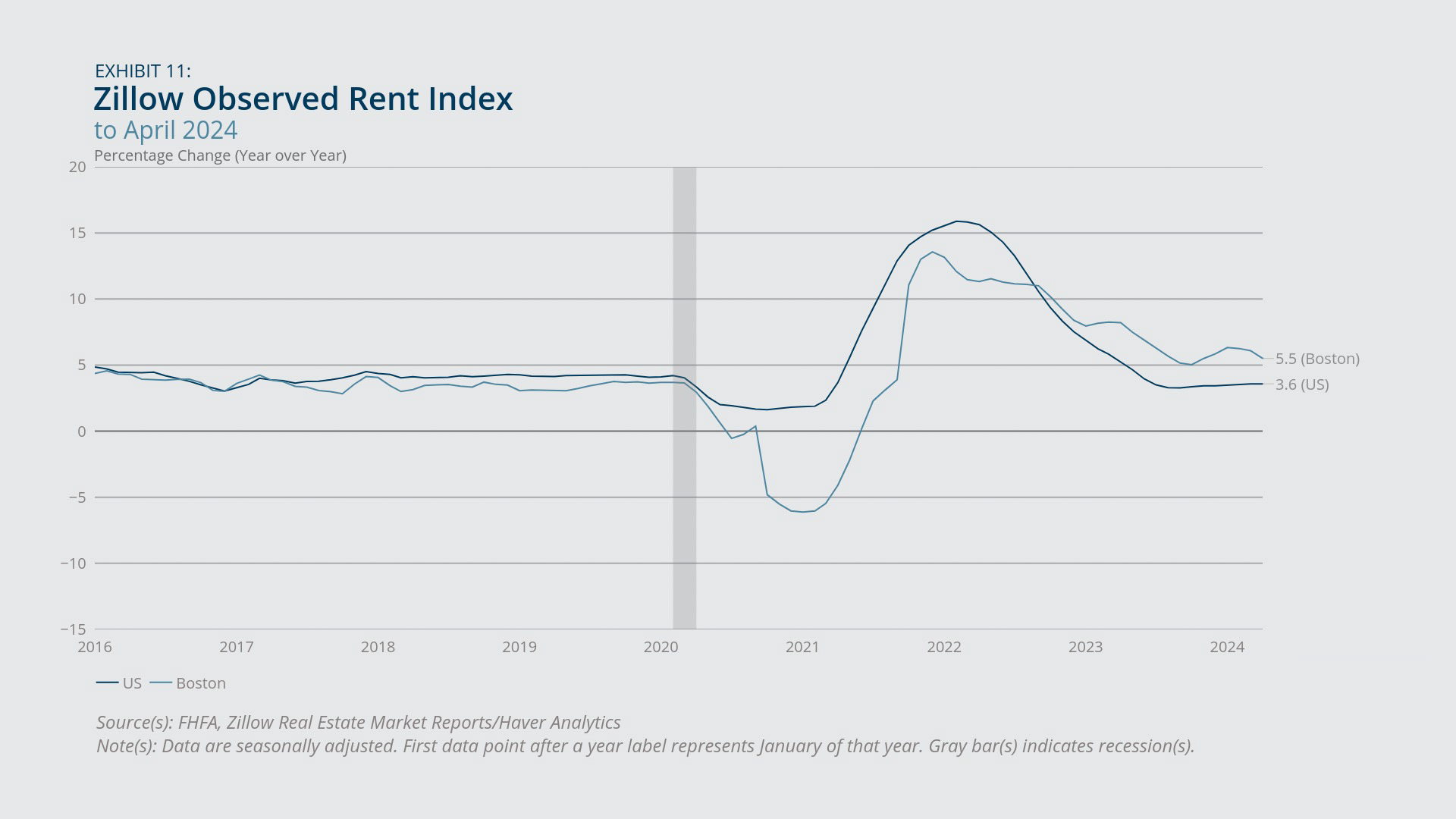

The Zillow Observed Rent Index has been flat in the United States and variable in Boston in recent months, following earlier declines from pandemic-era highs (Exhibit 11). Nonetheless, Boston’s rent growth rate has been higher than the US average since late 2022 and has oscillated in recent months, ending April 2024 at 5.5 percent, slightly above its late-2023 low of 5 percent.

{kind=link}

Federal Reserve Bank of Boston

{kind=link}

Federal Reserve Bank of Boston

{kind=link}

Federal Reserve Bank of Boston

{kind=link}

Federal Reserve Bank of Boston

{kind=link}

Federal Reserve Bank of Boston

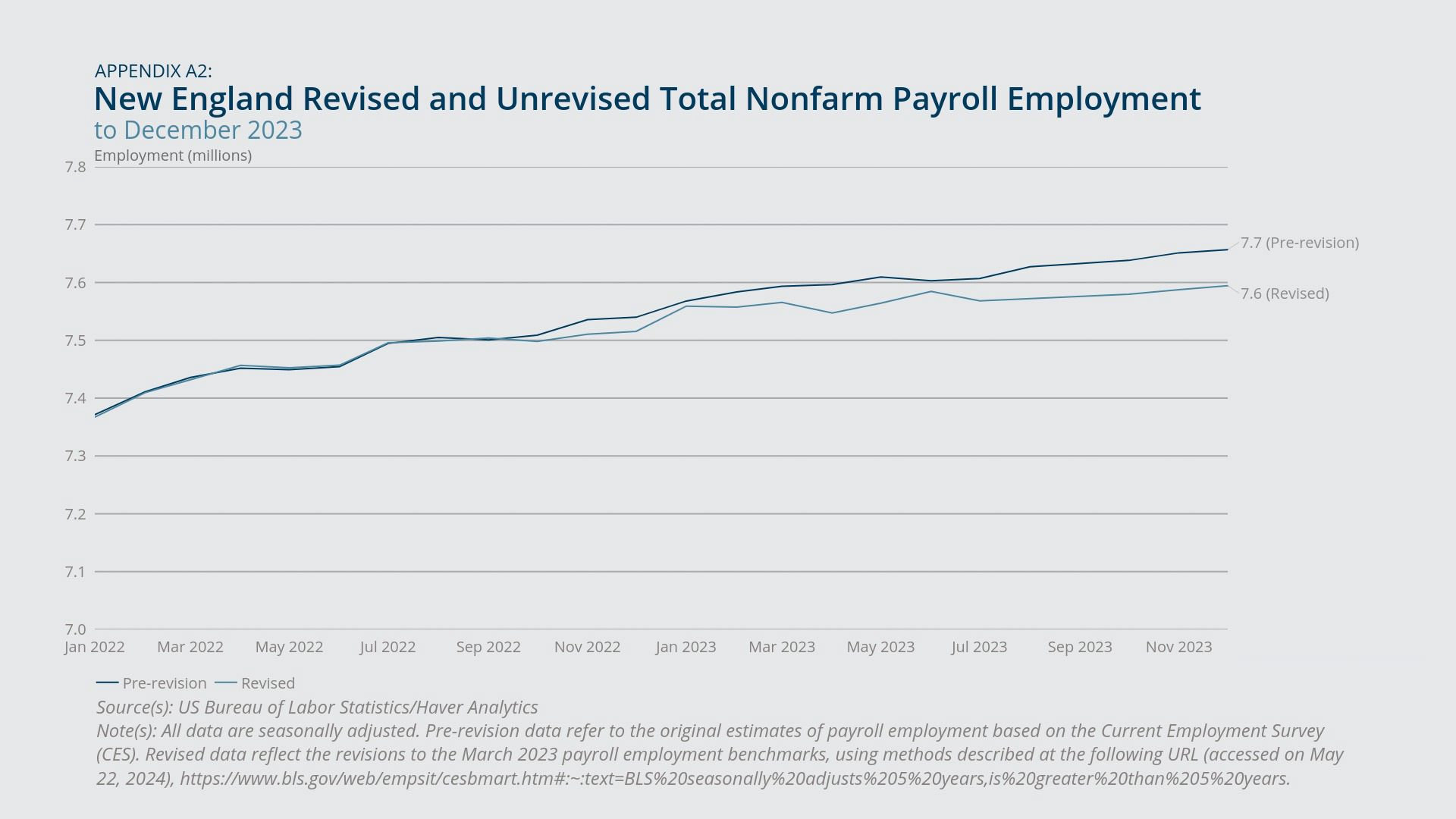

Benchmark Revisions to Payroll Employment Data from the BLS

- Recent revisions to the Bureau of Labor Statistics’ benchmark employment levels (for March 2023) imply that the employment recovery since the pandemic, in both the region and the United States, was in fact slightly weaker than suggested in the original estimates.

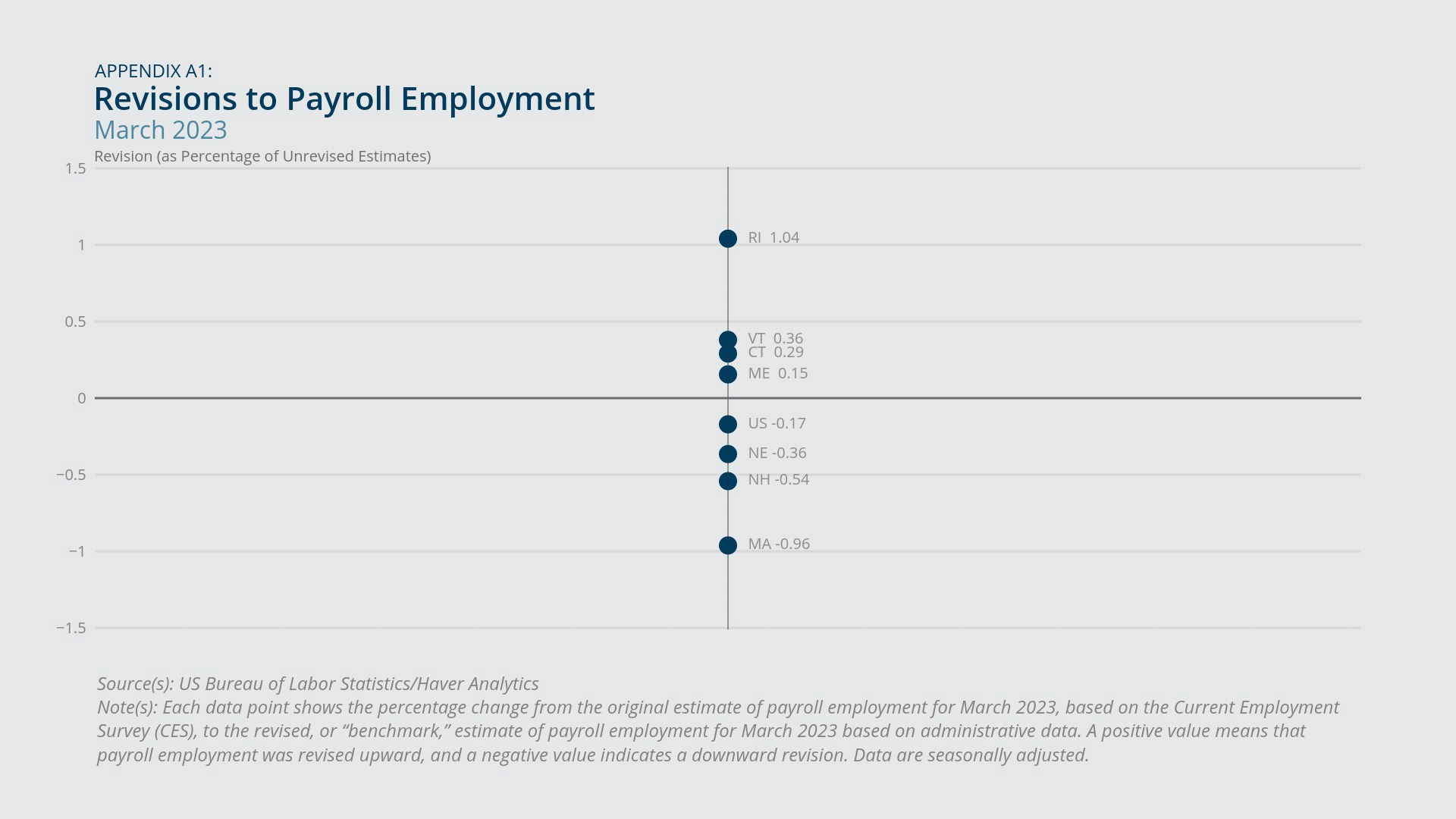

- The downward revision in the payroll employment benchmark for New England as a whole was driven largely by the –1.0 percent revision in Massachusetts (Exhibit A1).

Perhaps the most noteworthy implication of the benchmark revisions, within the region at least, is that employment in Massachusetts, previously thought to have surpassed its February 2020 level, instead remains slightly below that reference point. Comparing the revised data for December 2023 with the original estimates for the same month shows that Massachusetts had 72,600 fewer jobs, and the region as a whole had roughly 100,000 fewer jobs (Exhibit A2). By contrast, Rhode Island experienced an upward revision of 1 percent (comparing the revised March 2023 estimate with the original, March 2023 estimate); see Exhibit A1. The US employment benchmark was also revised downward, but the magnitude of the revision was smaller than that of New England.

National data (not shown) can provide potential insights into which sectors might have contributed most to the revisions in overall employment in the region. For the United States and among industries, the largest downward revision (as a percentage of the original, survey-based estimate) applied to the transportation and warehousing industry, at –2.5 percent, followed by information (–1.2 percent), other services (–0.7 percent), and professional and business services (–0.6 percent). Some industries experienced upward revisions, including utilities (3.0 percent), wholesale trade (0.8 percent), construction (0.6 percent), and financial activities (0.6 percent).

{kind=link}

Federal Reserve Bank of Boston

{kind=link}

Federal Reserve Bank of Boston

Endnotes

- All employment data in this memo (except in Exhibits A1 and A2, discussed below) reflect the annual benchmark revisions, which were released by the US Bureau of Labor Statistics in February 2024 for the United States and in March 2024 for the individual states. The revised data were also reflected in the New England Economic Conditions memo dated April 2, 2024, and (for the United States only) in the memo dated March 5, 2024. For more information on the methods used in the revisions, see Rokeya Khan and Thomas Woolley, “CES National Benchmark Article,” US Bureau of Labor Statistics. https://www.bls.gov/web/empsit/cesbmart.pdf

- See Liz Neisloss, “GBH Cuts Staff and Programming,” GBH, May 22, 2024. https://www.wgbh.org/news/local/2024-05-22/gbh-cuts-staff-and-programming

- Without directly observing the various flows into and out of unemployment, employment, and labor force participation, we cannot calculate with the certainty the portion of the increase in the unemployment rate that can be attributed to flows from nonparticipation into unemployment.

- See, for example, “Consumer Price Index, Boston-Cambridge-Newton — March 2024,” US Bureau of Labor Statistics news release, April 10, 2024. https://www.bls.gov/regions/northeast/news-release/2024/consumerpriceindex_boston_20240410.htm

- The most recent (April 2024) Beige Book report for the First District can be found at: https://www.bostonfed.org/news-and-events/news/2024/04/beige-book-first-district-boston-fed-april-2024-home-sales-turnaround-activity-up-modestly.aspx. The penultimate report (March 2024) can be found here: https://www.minneapolisfed.org/beige-book-reports/2024/2024-03-bo.

About the Authors

About the Authors

Mary A. Burke,

Federal Reserve Bank of Boston

Mary A. Burke is a principal economist and policy advisor with the New England Public Policy Center in the Federal Reserve Bank of Boston Research Department.

Email: Mary.Burke@bos.frb.org

Acknowledgments

Kelly Jackson, Federal Reserve Bank of Boston

Riley Sullivan, New England Public Policy Center at the Federal Reserve Bank of Boston

Tanner Thering, New England Public Policy Center at the Federal Reserve Bank of Boston

Resources

Keywords

- Regional economy ,

- Economic Conditions ,

- New England