Geographic Mobility Trends: New Englanders Still Aren’t Moving as Much as They Did before the Pandemic

{kind=link}

Federal Reserve Bank of Boston

The views expressed herein are solely those of the author and should not be reported as representing the views of the Federal Reserve Bank of Boston, the principals of the Board of Governors, or the Federal Reserve System.

Changes in remote/hybrid workplace options and housing market conditions in New England and throughout the United States since the onset of the COVID-19 pandemic have significantly affected people’s ability and willingness to relocate within a state, from one state to another, or from one region of the country to a different region. Businesses’ adoption of remote and hybrid work has weakened the traditional link between residence and workplace, affecting individuals’ choice of where to live. At the same time, persistently rapid growth in rent and house prices, along with fluctuations in mortgage rates, has made a substantial impact on the costs associated with relocating. These changes could have a profound effect in New England, which, over the past few decades, has experienced chronic housing shortages and has seen more US residents move out of the region than into it.1

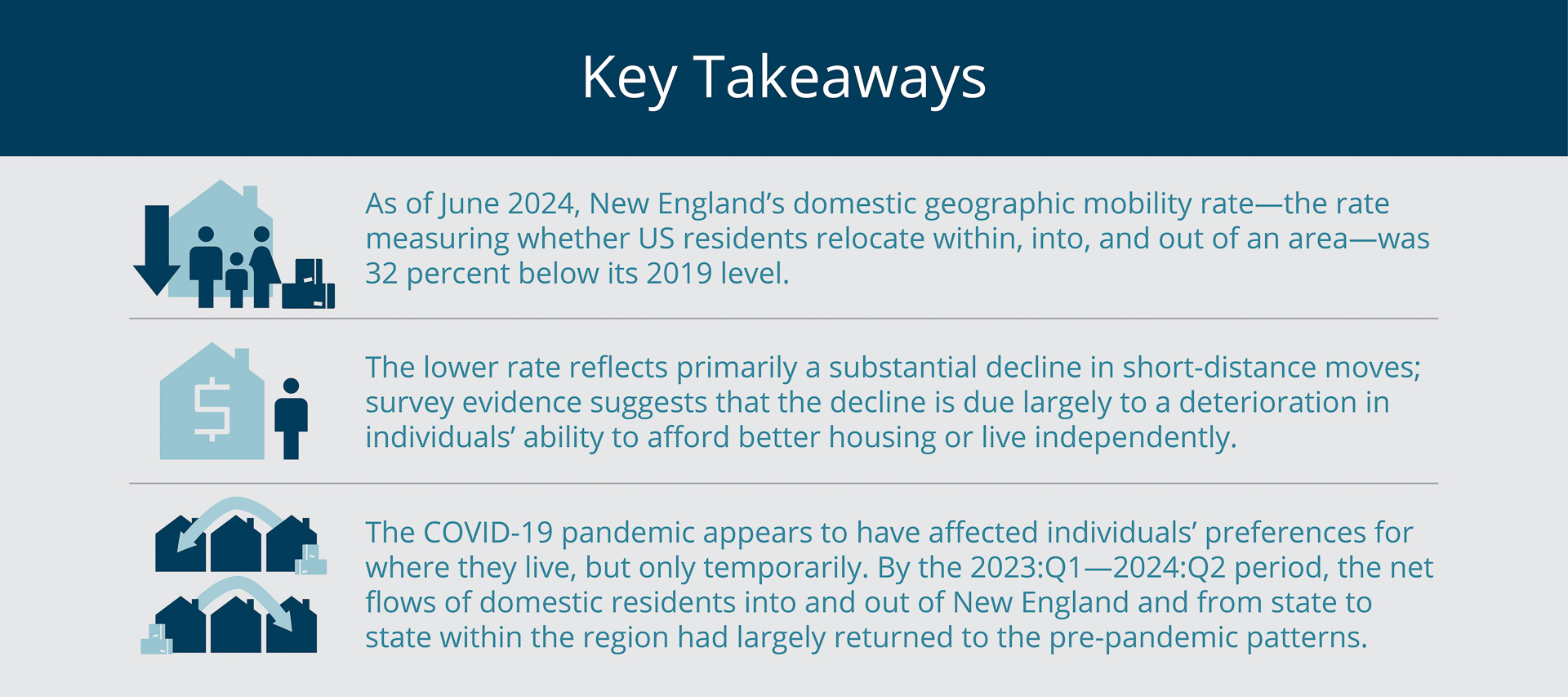

In studying the domestic migration patterns in New England from 2017 through early 2024 for this Regional Brief, I find that that nearly one-third fewer New Englanders changed residences in 2024 relative to five years earlier, before the onset of the pandemic. I also find that this decrease in the region’s domestic mobility rate was driven primarily by a decline in short-distance moves, and evidence suggests the decline is due to people’s growing inability to afford better housing or live on their own.

Sign up for new research and data on the New England economy.

In addition, the excess gains and losses in population that the New England states experienced during the pandemic due to residents leaving or new ones arriving appear to have been just temporary. However, Connecticut continues to see substantially smaller population losses from domestic migration relative to the period just before the pandemic.

I focus on two measures of migration: the quarterly domestic geographic mobility rate and the quarterly net domestic migration rate. The former is defined as the total number of people who move between census tracts in a quarter expressed as a percentage of the base population of a given geographic area at the beginning of that quarter.2 The measure captures the crude migration intensity of a population irrespective of people’s location preferences.

The quarterly net domestic migration rate is defined as the number of US residents who move into an area (in-migrants) minus the number who move from that area (out-migrants) divided by the base population of the area. It is expressed as the number per 1,000 residents. A positive net migration rate indicates that a geographic area has more people moving in than moving out, which results in a population gain. Conversely, a negative net migration rate reflects a population loss due to excess out-migration.3

For my analysis, I use consumer address records from the Federal Reserve Bank of New York/Equifax Consumer Credit Panel (CCP) to construct the measures of domestic migration. The CCP is a nationally representative anonymous 5 percent random sample of all US consumers who have a valid Social Security number and a credit file with Equifax, one of the three main credit-reporting agencies in the United States. Because younger consumers are less likely to have a credit file, and therefore the CCP may not accurately reflect their migration patterns, I restrict the sample to consumers aged 25 and older in all analyses.4

Short-distance Moves in Particular Have Plummeted

Domestic geographic mobility in the United States and in New England has gradually declined over the past 40 years as a result of changing demographics, labor market dynamics, and individuals’ willingness to exploit geographic price differences (See, for example, Karahan and Rhee 2014; Molloy, Smith, and Wozniak 2017; and Olney and Thompson 2024). This decline temporarily halted in the decade before the pandemic, 2011 through 2019, when mobility, as measured by changes of address, remained largely stable except for a modest decline near the end of this period.5 However, the pandemic disrupted this stability.

{kind=link}

Federal Reserve Bank of Boston

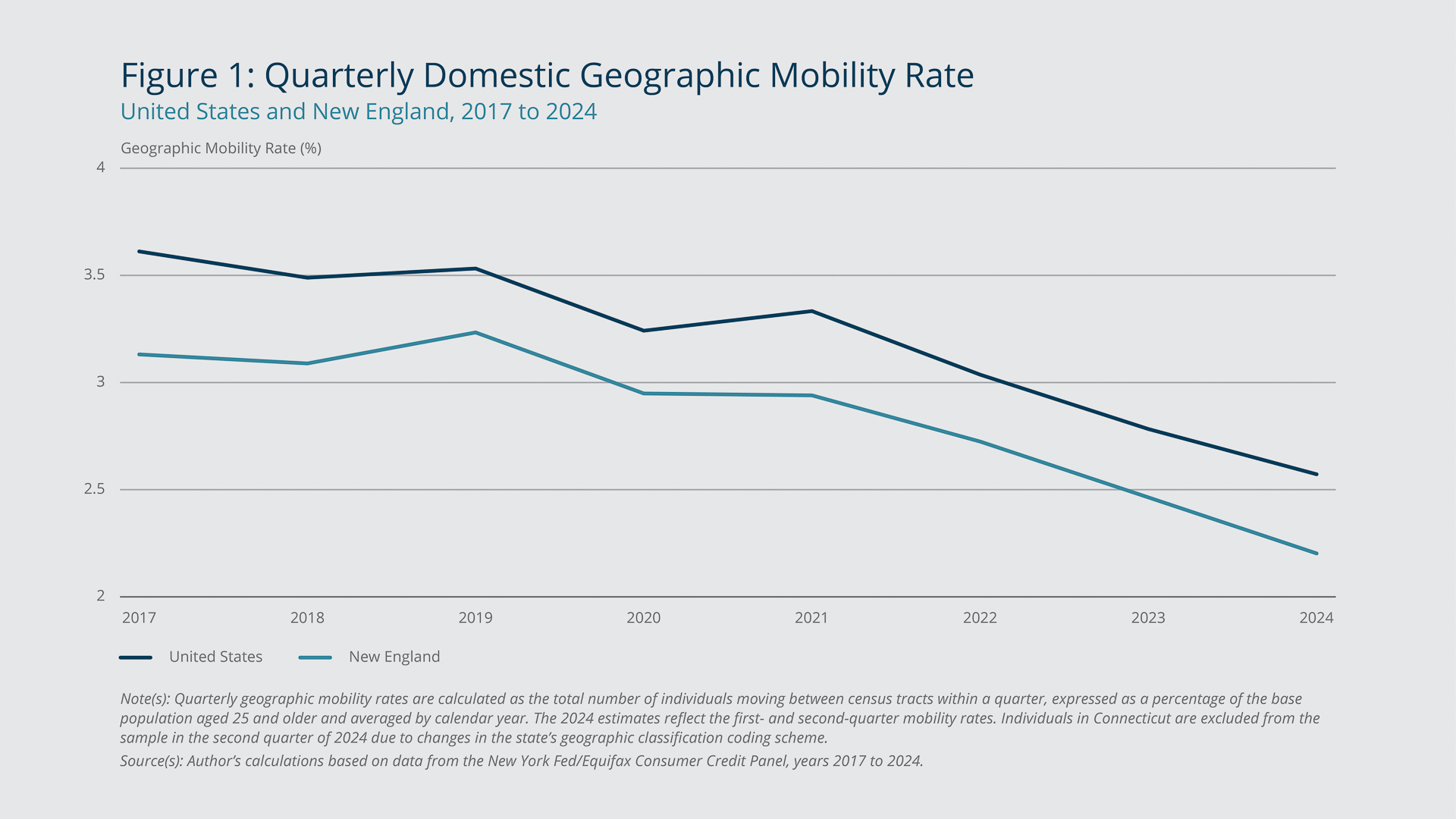

Figure 1 shows the average quarterly geographic mobility rates from 2017 to 2024 for New England and the United States. Compared with the national average, geographic mobility in New England started from a lower baseline level, 3.2 percent versus 3.5 percent. Nevertheless, the country and region experienced parallel steep downward trends in mobility following the onset of the pandemic: New England’s rate dropped 32 percent from 2019 to 2024, and the US rate fell 27 percent. The decline appears to have been tied only partially to pandemic-related restrictions, because the downward trends accelerated after 2021, when most of the government-mandated restrictions had been lifted.

A closer look at the decline in New England’s geographic mobility after 2019 reveals that it was driven primarily by a decrease in short-distance moves. The pattern is broad-based and generally holds for people of different ages, credit ratings, and mortgage-ownership status (see Appendix Figures A3 through A5 for more details), suggesting that people’s ability to move locally and accommodate changes in their housing needs or preferences has deteriorated significantly across consumer demographics and characteristics.

{kind=link}

Federal Reserve Bank of Boston

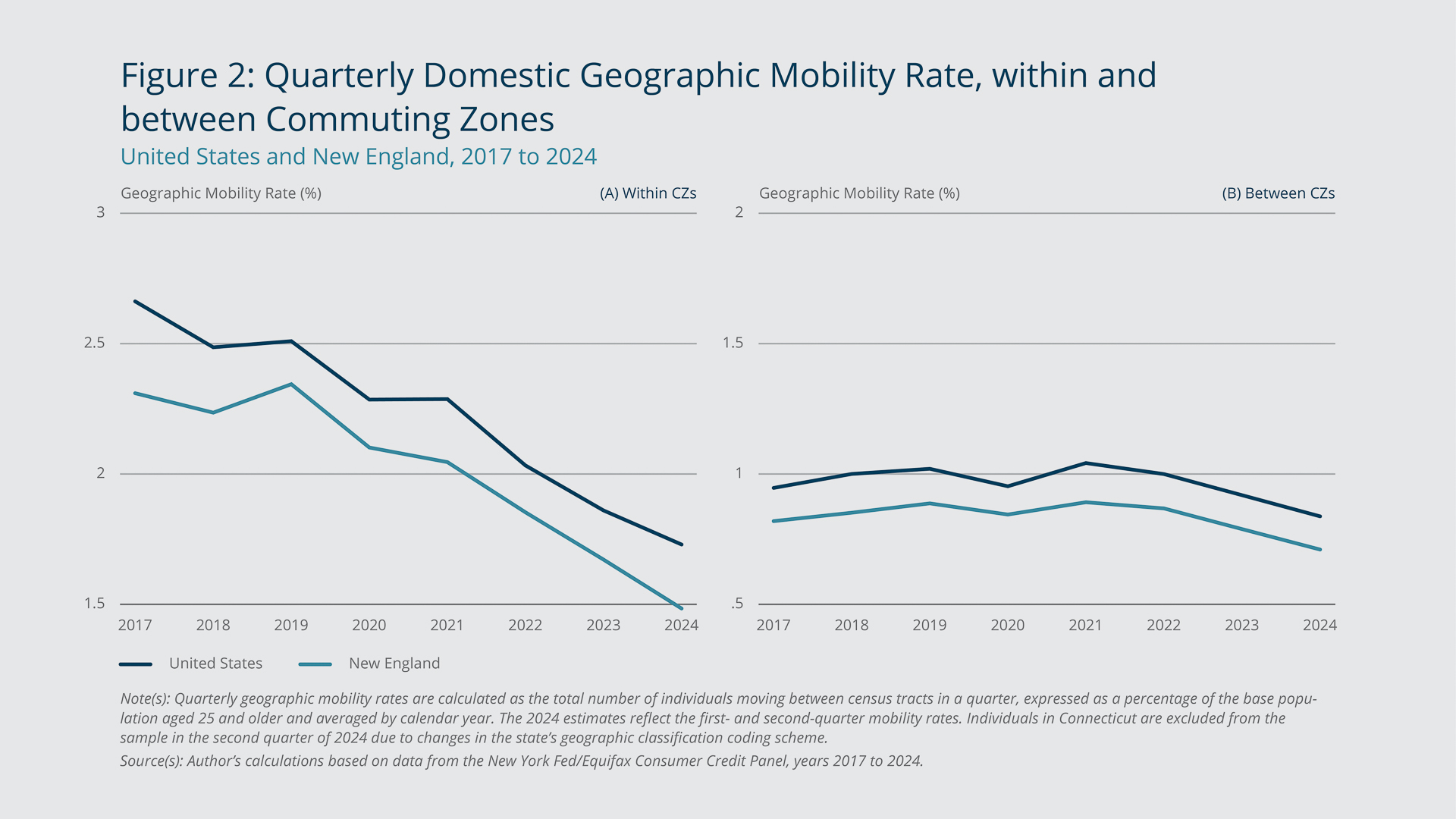

Figure 2 illustrates this point about the decline being driven by fewer short-distance moves by breaking down New England’s geographic mobility into two types: moves within a commuting zone (Panel A) and moves between commuting zones (Panel B). A commuting zone (CZ) comprises one or more counties that share commuting ties and form a common labor market. For a worker, a move within a CZ typically represents a residential relocation that does not necessarily involve a job change. A move between CZs is likely associated with a job change, assuming the new job requires in-person attendance, or it does not, and the switch to remote work enables the move.

Due to the relationship between job changes and between-CZ moves, a decline in between-CZ moves is associated with less efficient geographic allocation of workers and, consequently, a lower level of economic integration across labor markets. By contrast, barring structural changes in relocation demand, a decline in within-CZ moves is possibly related to less efficient housing allocation among the existing residents of a local labor market.

As Figure 2 shows, short-distance moves (within CZs) fell 37 percent in New England and 31 percent nationwide from the start of 2019 to June 2024. As noted, the significant drop in local moves suggests that New Englanders increasingly have chosen to remain at their current addresses instead of moving locally for changes in housing-related amenities such as house size or neighborhood characteristics. In comparison, the trend line for long-distance moves (between CZs) was mostly flat from 2017 to 2022 and did not start declining until 2023. The contrast suggests that the recent drop in geographic mobility, while reflecting a decrease in housing turnover within local markets, has had a more limited impact on the gross flow of workers across local labor markets, particularly before 2023.

{kind=link}

Federal Reserve Bank of Boston

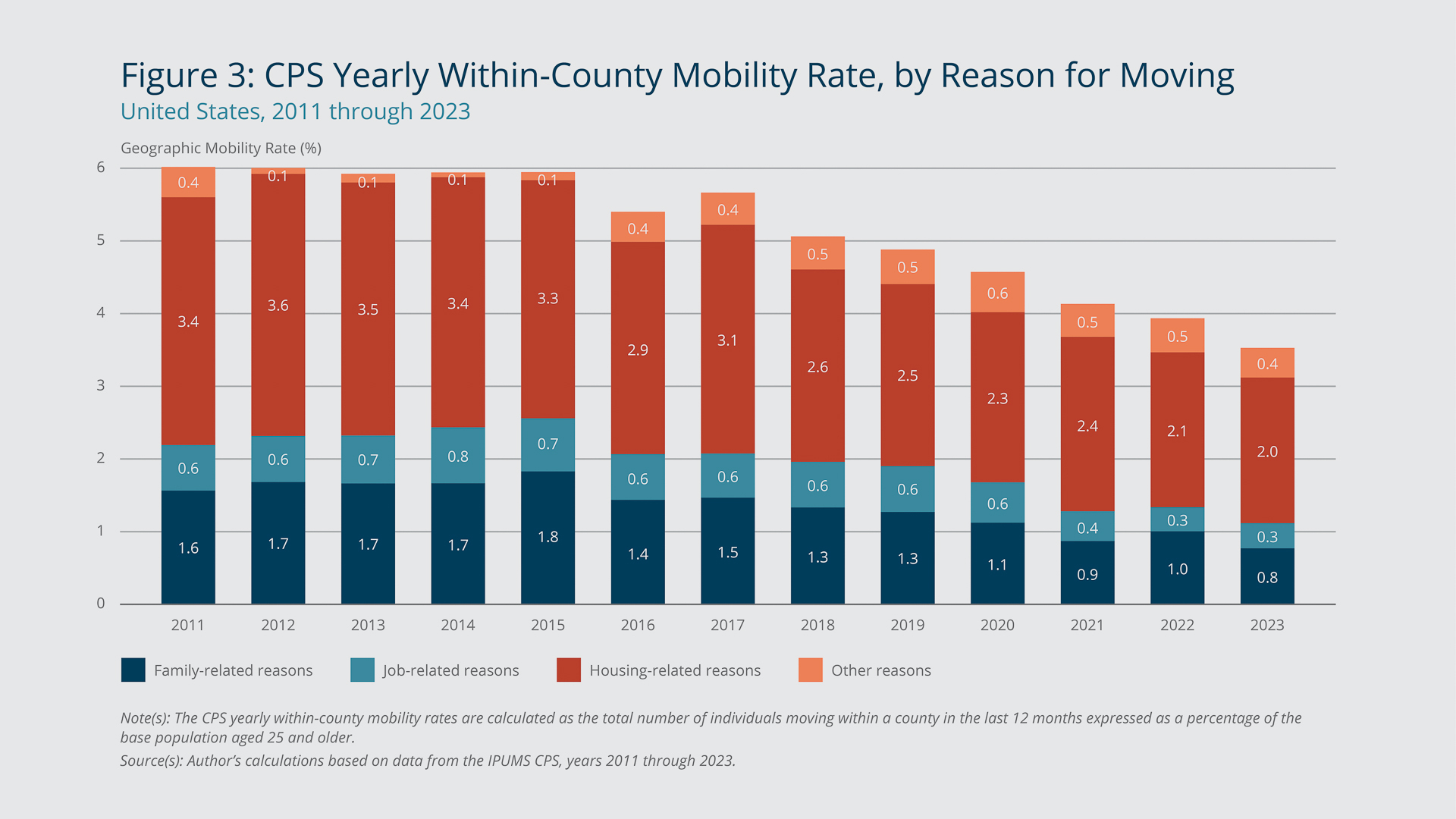

Using information from the Current Population Survey, Figure 3 breaks down the US within-county geographic mobility rate for 2011 through 2023 by people’s reasons for moving.6 The findings align with the inferences from the findings presented in Figure 2 and offer potential explanations for the decline in short-distance moves. From 2019 to 2023, the rate fell 1.35 percentage points across the United States. Decreases in housing- and family-related moves each accounted for 37 percent of the total decline, job-related moves for 21 percent, and other reasons for the remaining 4 percent.

The decline is particularly striking for moves to obtain new or better housing (accounting for 32 percent of the total decline) and moves to establish one’s own household (accounting for 17 percent of the total decline). These findings suggest that people’s ability to afford better housing or live independently has deteriorated considerably, thus limiting their local mobility over this period. Additionally, the need to move for commuting purposes has decreased with the rise in hybrid or remote work arrangements, as indicated by the decline in moves for an easier commute (accounting for 10 percent of the total decline), but to a lesser extent compared with the two housing- and family-related reasons.

Upheavals in Net Domestic Migration Trends Have Mostly Subsided

The dynamics of net domestic migration (in-migration minus out-migration) in New England underwent significant changes after the onset of the COVID-19 pandemic, leading to population gains in some of the region’s states and losses in others. However, after the early years of the pandemic, population changes related to the pandemic moderated, and by the 2023:Q1—2024:Q2 period, net domestic migration rates in most of the states had largely returned to their pre-pandemic levels.

{kind=link}

Federal Reserve Bank of Boston

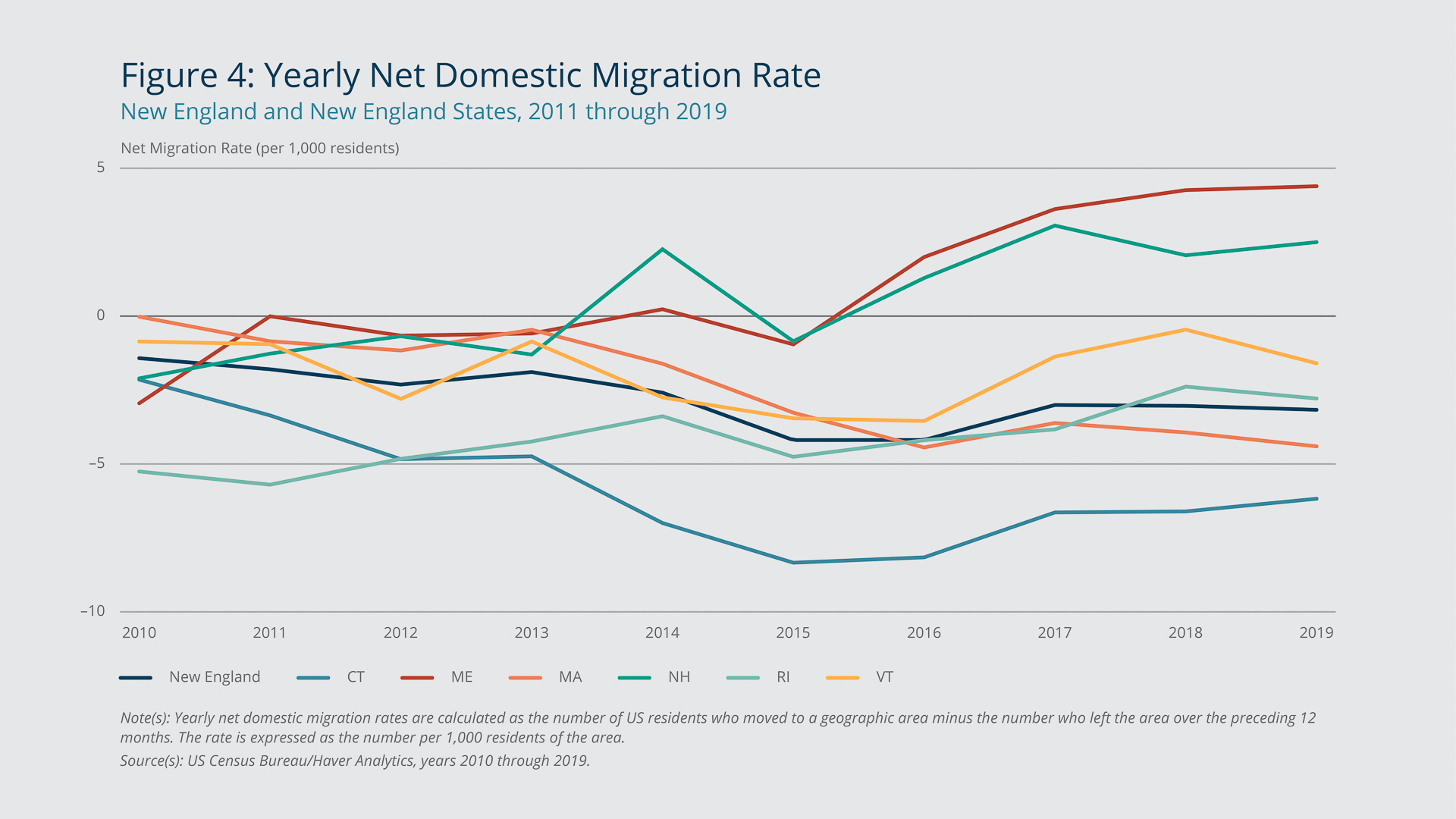

In the decade after the Great Recession, New England as a whole consistently experienced more domestic out-migration than in-migration, resulting in negative net domestic migration rates for the region. However, the trends varied across the six states. Figure 4 plots the net domestic migration rate for each New England state and the region overall from 2010 through 2019. Compared with the southern New England states (Connecticut, Massachusetts, and Rhode Island), the northern New England states (Maine, New Hampshire, and Vermont) exhibited higher levels of net domestic migration and an upward trend in net domestic migration in the five years leading up to the pandemic. By contrast, the southern New England states experienced largely flat or only modestly positive trends during that five-year period.

{kind=link}

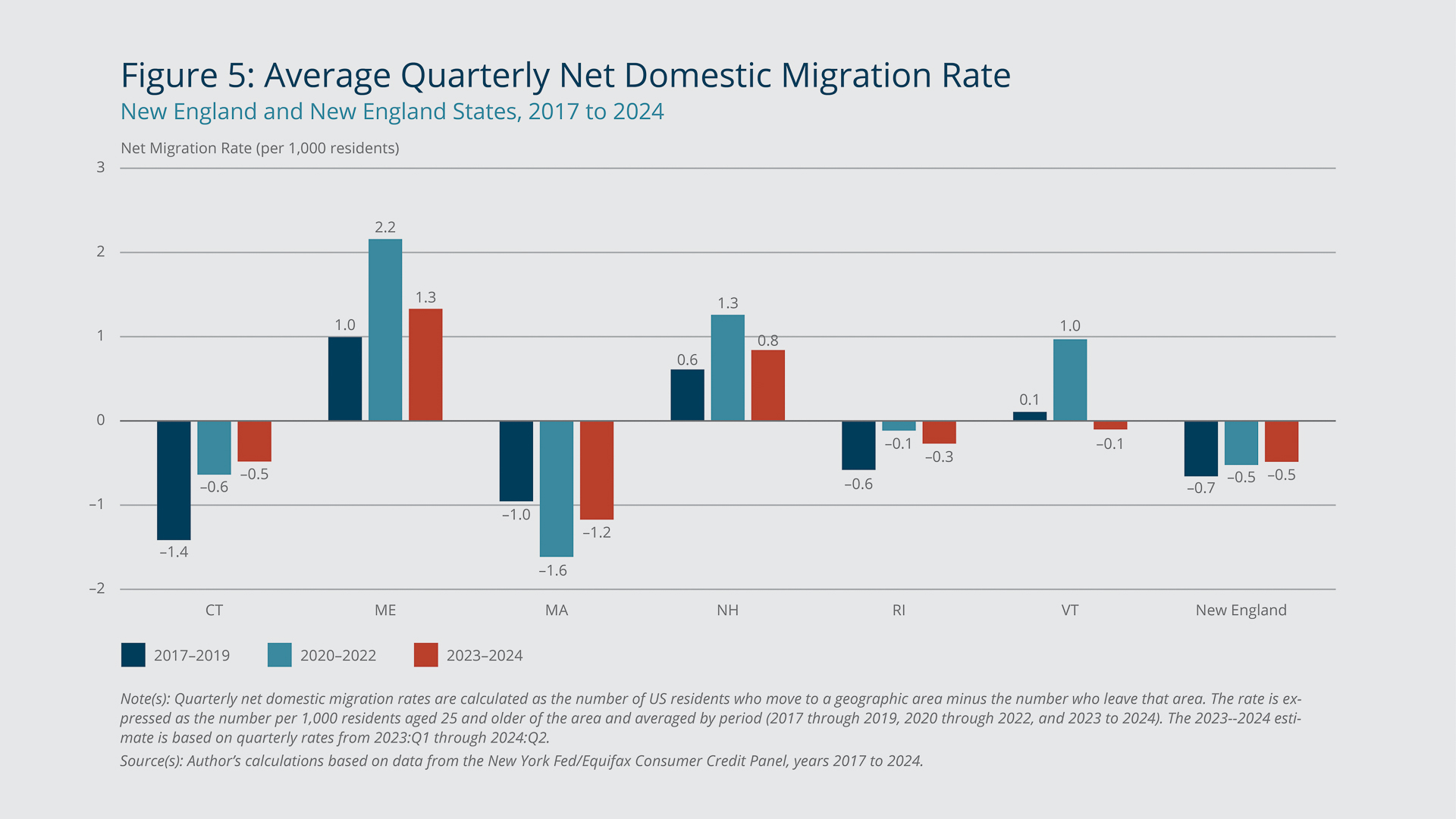

Figure 5: Average Quarterly Net Domestic Migration Rate. Federal Reserve Bank of Boston

From 2020 to 2022, following the onset of the pandemic, the northern New England states experienced substantial population gains from domestic migration as the net migration rates doubled compared with the pre-pandemic levels (Figure 5). Connecticut and Rhode Island saw lower negative net domestic migration, which reduced their population losses. By contrast, Massachusetts experienced higher negative net migration due to a rise in out-migration and sustained a substantial population loss.

{kind=link}

Federal Reserve Bank of Boston

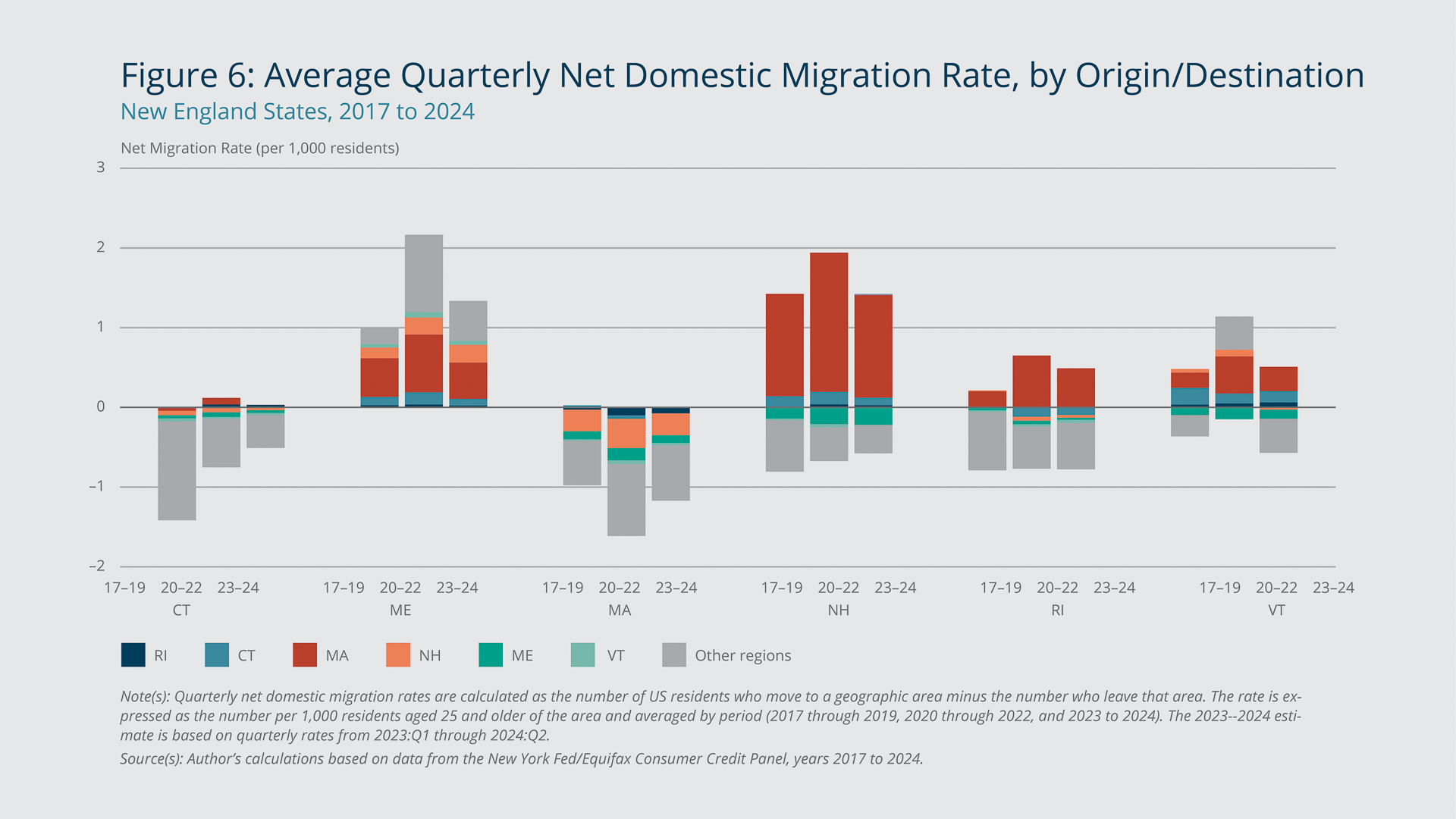

Figure 6 illustrates the effect that the pandemic may have had on individuals’ geographic preferences by breaking down the net migration rates by the origins and destinations of people who moved into, out of, or within New England. For each state, the bar areas above zero indicate net inflows of people from the indicated locations to that state, whereas the bar areas below zero show net outflows of people from that state to the indicated locations. The sums of the bar areas equal the net migration rates shown in Figure 5.

In the pre-pandemic period from 2017 through 2019, in-migration from within the region contributed to the domestic migration gains in the northern New England states. Meanwhile, an exodus to other regions of the country accounted for much of the domestic migration losses in the southern New England states. This pattern shifted after 2019. During the pandemic (2020 through 2022), people relocating from outside New England drove the net migration gains in Maine, Vermont, and Connecticut, whereas net inflows of people from Massachusetts led the migration growth in New Hampshire and Rhode Island. In Massachusetts, the accelerated population loss during this period was due to equally sized increases in out-migration to other New England states and to other regions. In the post-pandemic period (2023 through mid-2024), net migration flows between states largely returned to the pre-pandemic patterns. The exception was Connecticut, which continued to see higher net migration rates due to less net outflows of the state’s population to other regions.

The recent higher net domestic migration rates in Connecticut suggest the possibility of structural shifts in regional commuting patterns, such as new commuting ties between New York City and its peripheral areas enabled by hybrid work arrangements. Some of these structural shifts may not be apparent until geographic mobility in the region returns to a higher level, and it will take time to fully distinguish any long-term changes.

Long-term Implications of Reduced Geographic Mobility

While the excess population gains and losses observed in the New England states following the onset of pandemic have largely faded, New Englanders overall have continued to show substantially lower geographic mobility compared with the pre-pandemic level. It is premature to ascertain whether this downward trend will reverse soon. If housing affordability is the primary factor driving the decline, the continuation of the trend will depend on future trajectories of rent, house prices, and mortgage rates.

Regardless of the causes, a low geographic mobility rate is indicative of other societal changes, such as shifts in family formation, childbearing, and job preferences. It is advisable for policymakers to continue monitoring the progression of this trend, because the current path, if it persists, could lead to wider long-term implications for New England’s families and labor markets.

Endnotes

- See Chiumenti (2021) for a description of the early impact of COVID-19 on household relocation patterns in New England.

- A census tract is a small statistical subdivision of a county delineated by the US Census Bureau for statistical purposes. For more information, see https://www.census.gov/programs-surveys/geography/about/glossary.html#par_textimage_13.

- Over the study period, international migration to New England also went through substantial changes due largely to changes in immigration policies. This brief focuses on domestic migration measures exclusively to highlight the impact of the domestic economic environment on US residents’ residential choices.

- Each quarter, the CCP reports credit information for its 12 million primary sample members, along with their birth year and address. The panel nature of the data allows researchers to construct domestic migration measures based on the quarter-to-quarter address changes reported to the credit bureau.

Migration estimates derived from the CCP are comparable to those from the Internal Revenue Service (IRS) and the American Community Survey (ACS), but less so to estimates based on the Current Population Survey (CPS) due to the CPS’s smaller sample size and different survey methodologies (DeWaard, Johnson, and Whitaker 2018; Koerber 2007). The main advantage of the CCP over the IRS and ACS is its currentness. The CCP data have a process time of less than three months, compared with one to two years of the ACS or the publicly available IRS data. The contemporaneity of the data offers crucial insights into how domestic migration responds to current economic conditions, allowing policymakers to assess changes in migration trends in a timely manner. However, because the CCP was designed for credit monitoring purposes, it is less representative of the younger, low-income, immigrant, or other underbanked populations, who are more likely to have no credit history or Social Security number and therefore excluded from the sample. Hence, the estimates derived from the CCP are less reflective of the migration behavior of these demographic groups. - See Figures A1 and A2 in the Appendix for trends in US geographic mobility based on estimates from the Current Population Survey (IPUMS CPS) and the American Community Survey (IPUMS USA).

- The CPS within-county mobility rate presented in Figure 3 is defined as the share of the US population aged 25 or older that moved within a county in the last 12 months. While the definition and recall period are different from those of the within-CZ geographic mobility rate shown in panel A of Figure 2, the two figures exhibit similar downward trends in local geographic mobility.

References

Chiumenti, Nicholas. 2021. “How the COVID-19 Pandemic Changed Household Migration in New England.” Federal Reserve Bank of Boston New England Public Policy Center Regional Briefs 21–3. https://www.bostonfed.org/publications/new-england-public-policy-center-regional-briefs/2021/how-the-covid-19-pandemic-changed-household-migration-in-new-england.aspx.

DeWaard, Jack, Janna E. Johnson, and Stephan D. Whitaker. 2018. “Internal Migration in the United States: A Comparative Assessment of the Utility of the Consumer Credit Panel.” Federal Reserve Bank of Cleveland Working Paper 18-04. https://doi.org/10.26509/frbc-wp-201804r

IPUMS CPS. 2024. University of Minnesota. https://doi.org/10.18128/D030.V11.0

IPUMS USA. 2024. University of Minnesota. https://doi.org/10.18128/D014.V4.0

Karahan, Fatih, and Serena Rhee. 2014. “Population Aging, Migration Spillovers, and the Decline in Interstate Migration.” Federal Reserve Bank of New York Staff Report No. 699. https://www.newyorkfed.org/research/staff_reports/sr699.html

Koerber, Kin. 2007. “Comparison of ACS and ASEC Data on Geographic Mobility: 2004.” US Census Bureau Working Paper. https://www.census.gov/library/working-papers/2007/acs/2007_Koerber_01.html

Molloy, Raven, Christopher L. Smith, and Abigail Wozniak. 2017. “Job Changing and the Decline in Long-distance Migration in the United States.” Demography 54(2): 631–653. https://link.springer.com/article/10.1007/s13524-017-0551-9

Olney, William W., and Owen Thompson. 2024. “The Determinants of Declining Internal Migration.” National Bureau of Economic Research Working Paper 32123. https://doi.org/10.3386/w32123

About the Authors

About the Authors

Pinghui Wu,

Federal Reserve Bank of Boston

Pinghui Wu is a senior economist with the New England Public Policy Center at the Federal Reserve Bank of Boston.

Email: Pinghui.Wu@bos.frb.org

Resources

Keywords

- New England ,

- NEPPC Regional Brief ,

- Geographic mobility ,

- COVID-19 pandemic