What are the unseen risks to banks – and the financial system – of asset fire sales by nonbanks?

Boston Fed paper looks at potential financial stability implications of nonbanks’ growing influence

ilbusca/iStock

{kind=link}

Asset fire sales are by nature unplanned, quick, and often sparked by crisis. And when non-bank financial institutions are forced into fire sales, the potential spillover to banks – and the broader financial system – could be underappreciated, according to a paper co-authored by the Federal Reserve Banks of Boston and New York.

The paper, titled “Non-Bank Financial Institutions and Banks’ Fire-Sale Vulnerabilities,” looks beyond the more easily seen direct effects of these fire sales. Instead, it focuses on the indirect impacts that are largely uncharted but can pose problems.

Non-bank financial institutions, or NBFIs, include entities like insurance companies, mutual funds, and mortgage lenders. All deal in money, risk, and time. For instance, a mortgage lender takes on credit risk to give a buyer money now, and that money is repaid with interest over time.

The paper says NBFIs now account for about $60 trillion in global “credit intermediation activities,” which includes things like arranging or granting credit.

“The overall size of these non-bank financial institutions has been growing significantly over the last 20 years, and interconnections among them has been increasing,” said Lina Lu, a paper co-author and economist in the Boston Fed’s Supervision, Regulation & Credit department.

Nonbanks have become so large and interwoven into the financial system that their asset fire sales can spill over into seemingly unrelated banking operations. Paper co-author Mattia Landoni, also an SRC economist, said it’s critical to understand the potential impacts, and the paper gives regulators a methodology to do it.

“If you don't get this fuller picture, then you don't understand the possible cascades that could happen, where they start and where they end,” Landoni said.

Fire sales’ indirect impacts can be tough to trace

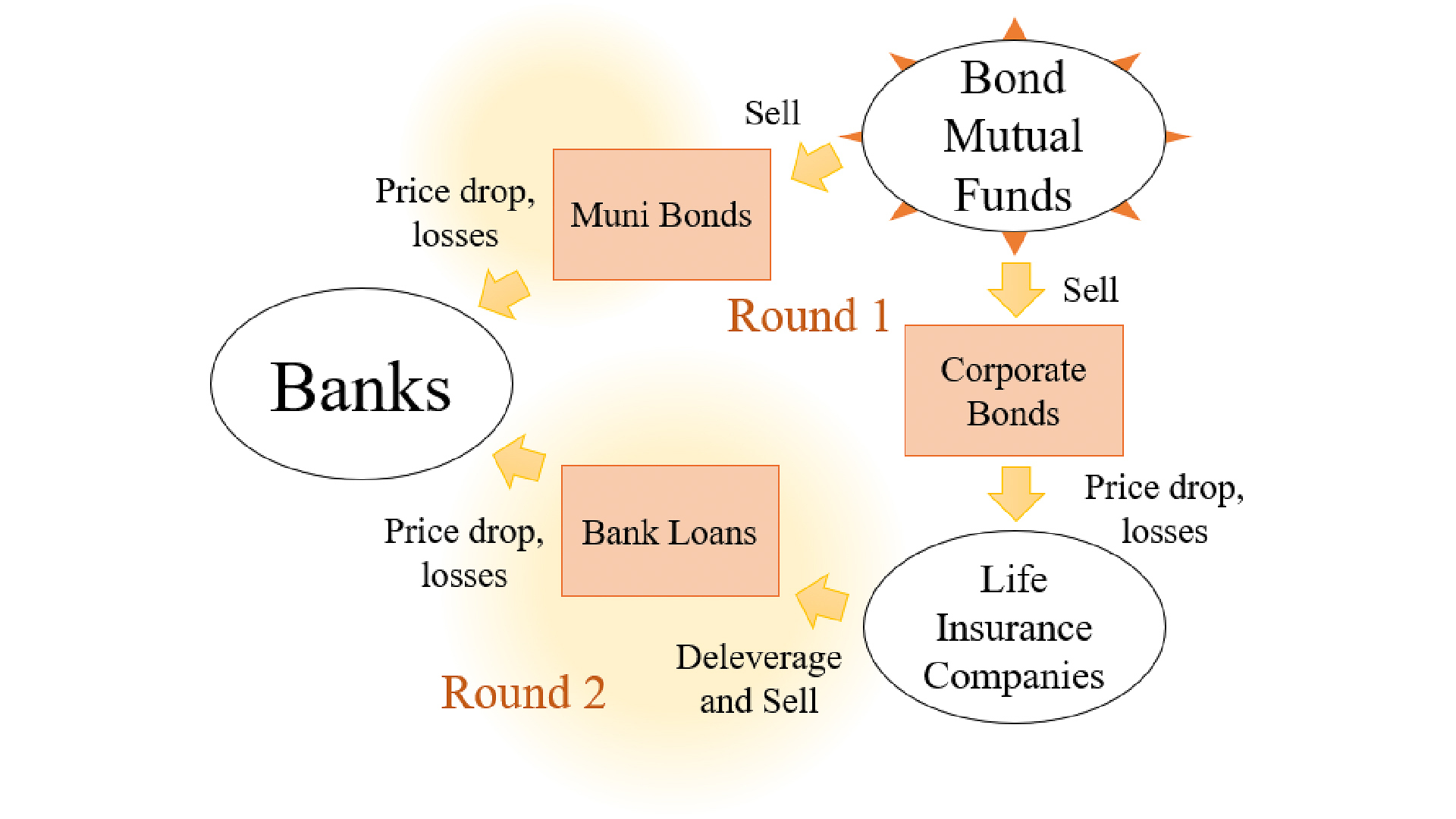

The paper explores direct and indirect fire-sale impacts from 12 non-bank segments. The direct impacts are relatively straightforward. Say the NBFI segment “bond mutual funds” has a fire sale of a portion of its municipal and corporate bonds holdings. Banks with only municipal bond holdings would be clearly and directly affected by their dropping value.

But these banks could also be affected by the corporate bonds fire sale, even though they don’t hold them. That’s because life insurance companies do. The insurers might respond to the bonds’ dropping value by selling off their own assets, including their bank loan holdings. That causes the loan values to drop, hurting banks through what the paper calls indirect “second round” impacts.

The paper says this web of asset interconnection between bank and non-banks “can contribute to very large multiples of an original fire sale, thus suggesting that conventional assessments of fire-sale vulnerabilities can be grossly understated.”

{kind=link}

Federal Reserve Bank of Boston

Paper’s authors rank the risks of non-bank asset fire sales

In the paper, Lu, Landoni, and co-author Nicola Cetorelli of the New York Fed provide a methodology for ranking the risks posed by the 12 nonbank segments.

They first rank the segments by their ability to impose direct losses on banks. Finance companies and life insurers top that list, because they are large and hold many of the same assets as banks.

Then, they rank each segment’s ability to impose the indirect, second round effects. Bond, equity, and pension funds are first here because they can impose direct losses on NBFI segments that, in turn, have heavy and direct impacts on banks.

Finally, they rank the segments according to their ability to act as “vectors” to spread the economic shock of fire sales around the banking system. Life and property-casualty insurance companies rank highest here. Their heavily diversified portfolios make them vulnerable to direct losses from a cross-section of other segments. These portfolios also tie them to banks, making them a possible hub of “shock propagation” through various complex, indirect channels.

The paper recommends, “While nonbanks are made up of a set of very separate, distinct segments, operating according to distinct business models, they should be considered as a more homogeneous whole in analyzing and understanding the transmission and the amplification of stress scenarios in the financial ecosystem.”

Find the paper on its publication page.

Stay up-to-date on SRC research by subscribing to the Supervision, Regulation & Credit email list.

Media Inquiries?

Contact our media relations team. We connect journalists with Boston Fed economists, researchers, and leadership and a variety of other resources.

About the Authors

About the Authors

Jay Lindsay is a member of the communications team at the Federal Reserve Bank of Boston.

Email: jay.lindsay@bos.frb.org

Site Topics

Keywords

- network externalities ,

- financial stability ,

- monitoring ,

- nonbanks ,

- fire sales