A fatal cash crash? Conditions were ripe for it after the pandemic hit, but it didn’t happen

Credit card use rose as cash use fell, but experts say cash may have found its 'floor'

PavelIvanov/ iStock

{kind=link}

In the early days of the pandemic, it looked like cash might be headed for a fatal crash.

Cash use had already been in decline in the years leading up to March 2020 start of the pandemic. Then, once COVID-19 hit, reasons for people to stop using cash kept piling up.

Lockdowns kept people inside and buying things online. When they did make in-person purchases, many avoided the personal contact that comes with exchanging bills. And there was also a widespread but unfounded worry that the notes somehow carried the virus.

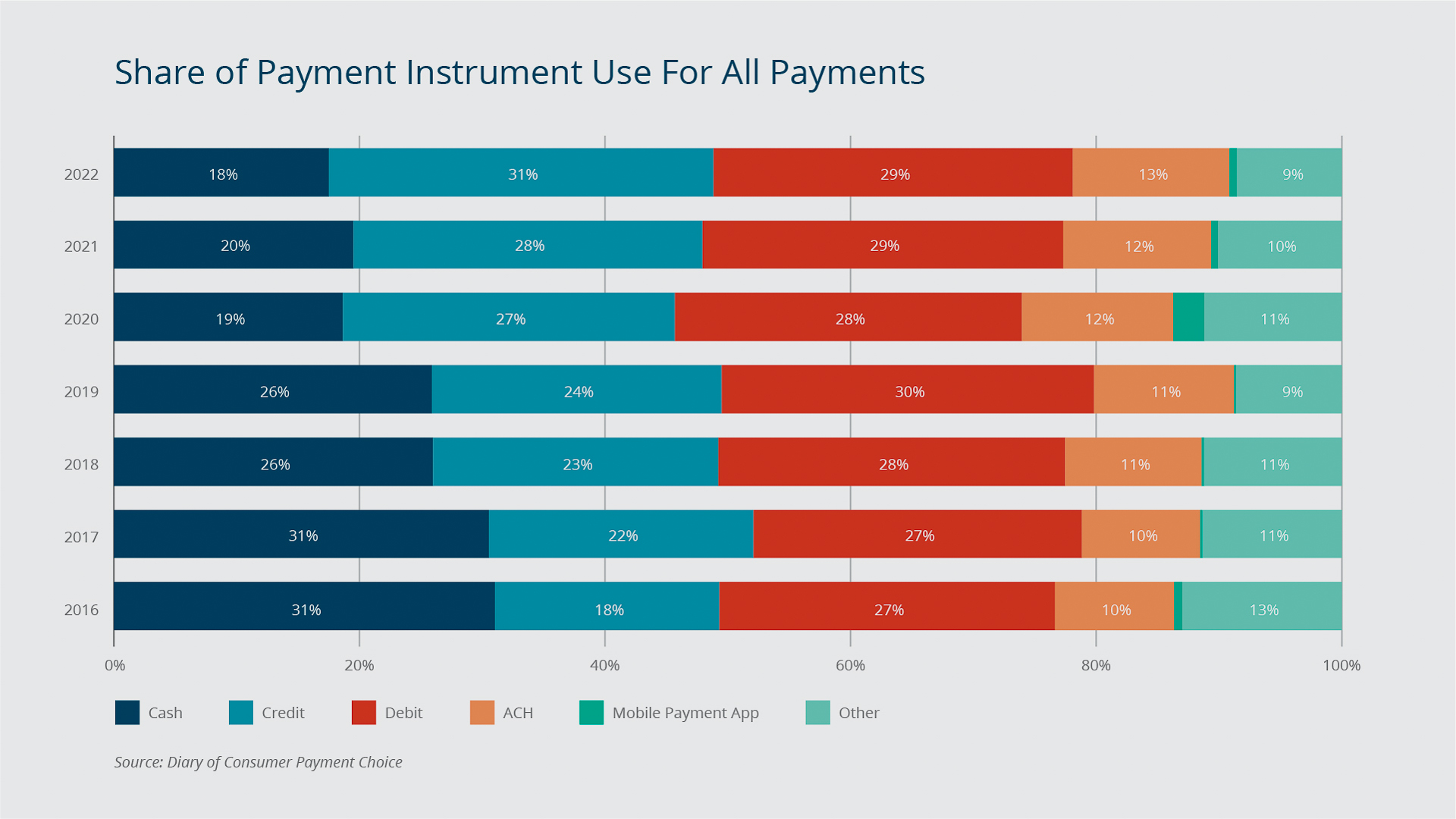

Cash use did, in fact, fall that first year. It accounted for 19% of all payments in 2020, a steep drop from 26% the year before, according to the Federal Reserve’s 2023 Diary of Consumer Payment Choice. But then, the drop stopped.

In 2021, cash use accounted for about 20% of all payments, and then about 18% in 2022, making it the third-most used payment method in the U.S. That leveling off after 2020 has experts thinking cash use may have found a “floor” it won’t fall below for a while.

Shaun O’Brien, co-author of a report on the diary's findings, said the pandemic could hardly have created better conditions for the oft-predicted disappearance of cash. Instead, he said, it might have demonstrated that cash use – though far lower than it once was – has significant staying power.

“The environmental factors were almost completely there for cash to go away, and it didn't,” said O’Brien, lead analyst in the Federal Reserve's FedCash Service. “Our conclusion was that people who are using cash just really want to use it, or they really need to use it.”

As cash declined, credit cards took top payments spot

The diary was developed at the Federal Reserve Bank of Boston, and it’s now managed at the Atlanta Fed. Years of data from the diaries show people change their payment habits slowly. But an event as disruptive as the pandemic can accelerate existing trends, and O’Brien said that appears to be what happened here – both with declining cash use and increasing credit card use.

The diary indicates credit card use rose from 18% of all payments in 2016 to 24% in 2019, just before the pandemic began. That placed it behind debit cards and cash, in that order. But by 2022, credit cards had grabbed a 31% share and become the top payments choice.

{kind=link}

Federal Reserve Bank of Boston

O’Brien said the pandemic-era shift toward credit cards is tied to the move towards online payments, because people generally prefer credit cards over debit cards for online purchases. A major reason is they feel credit cards better protect them from theft, O’Brien said.

“I think people view the risk of losing their actual funds if a debit card is compromised – versus putting their credit line at risk – very, very differently,” he said.

O’Brien said as credit card use rose during the pandemic, he expected an even greater drop in cash use. But when cash use leveled off, O’Brien and diary report co-author Emily Cubides – an analyst based at the Los Angeles branch – found their question changing from, “Why are people abandoning cash?” to “Why are they still using it?”

Fed experts: Speed, anonymity among many reasons people choose cash

Lisa Perlini, head of Cash Services at the Boston Fed, says the speed at which transactions are made – money changes hands and it’s over – is one of several reasons cash will always be in demand. Plus, the transactions are private and anonymous.

“People are going to want that when they’re 17 and when they’re 70,“ Perlini said.

O’Brien noted cash use is a necessity for many “unbanked” – a generally lower-income group that does not have checking, savings, or other bank accounts. He added cash is seen as safe during a crisis, when people are worried financial institutions or payment infrastructures will go offline or won’t be available to facilitate transactions.

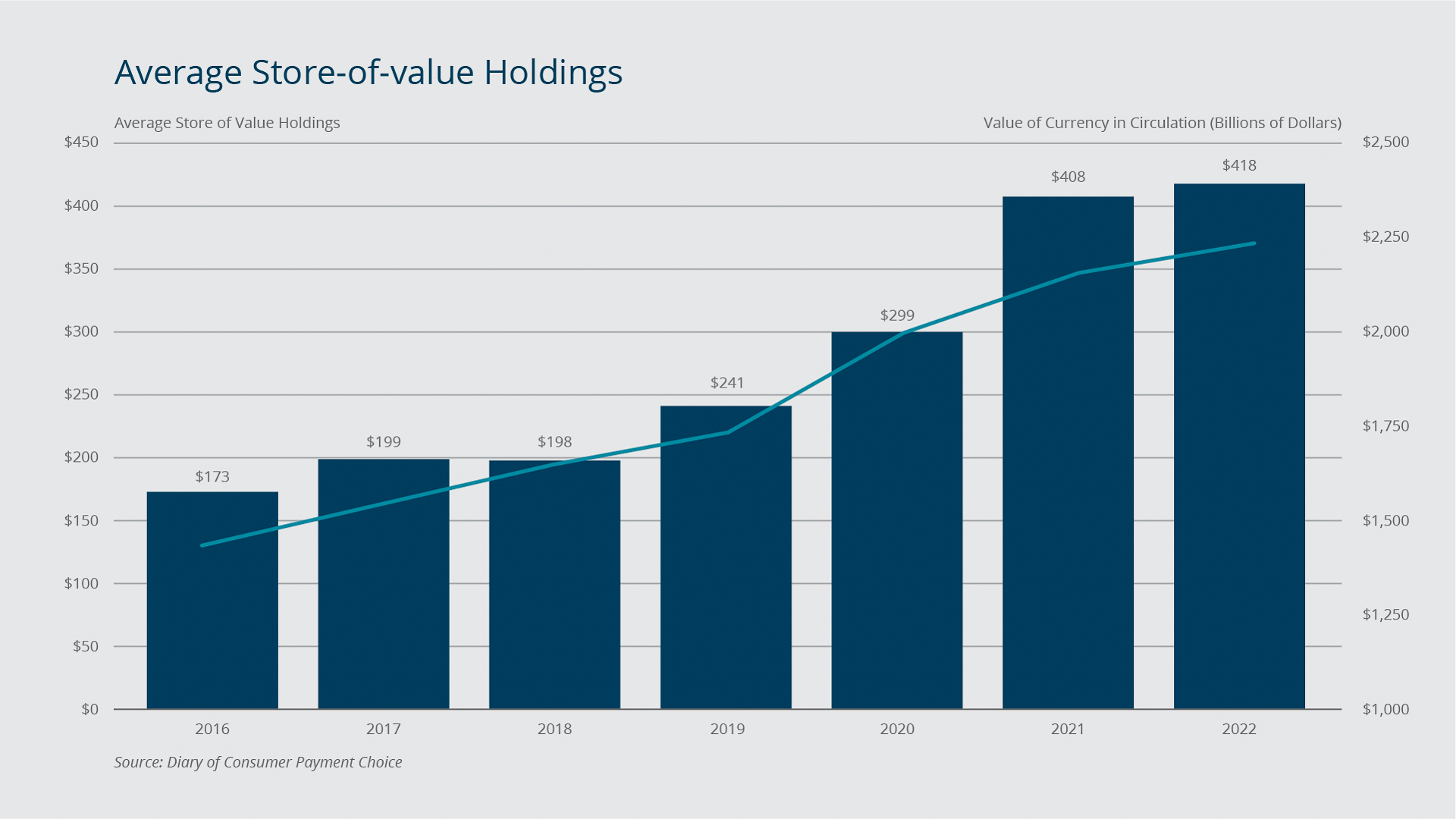

During the pandemic, average cash holdings per consumer soared from $241 in 2019 to $418 in 2022. This is cash people have on hand, just in case.

The diary also says that most people still carry cash, as roughly 80% held cash at least one of the diary’s three survey days. That, combined with elevated holdings since the pandemic, “indicate that cash remains in demand, even if some individuals hold cash only for contingency purposes and as a backup payment option,” the diary says.

{kind=link}

Federal Reserve Bank of Boston

The diary results also make it clear that even though people are using cash less, they intend to keep using it. When asked, “Do you currently have any plans to stop using cash in the future?”, 93% of respondents answered, “No.”

Perlini said it’s clear that cash is always going to be the preferred choice for some.

“There's this core of people who continued to use it during the pandemic,” she said. “And unless something shifts in their world, I don't see why they would stop.”

Media Inquiries?

Contact our media relations team. We connect journalists with Boston Fed economists, researchers, and leadership and a variety of other resources.

About the Authors

About the Authors

Jay Lindsay is a member of the communications team at the Federal Reserve Bank of Boston.

Email: jay.lindsay@bos.frb.org

Site Topics

Keywords

- cash ,

- cash demand ,

- consumer credit ,

- consumer payments ,

- payments