How much will the commercial real estate market’s decline hurt the banking industry?

New Boston Fed study finds smaller banks likely will feel less pain than larger lenders

Denis Tangney, Jr/iStock

{kind=link}

Concerns about a pandemic-induced weakening of the commercial real estate market are warranted, according to a recently released working paper coauthored by Federal Reserve Bank of Boston senior economist J. Christina Wang. However, the paper finds that the commercial real estate (or CRE) market’s decline will have a greater effect on certain types of commercial properties and therefore may not hurt smaller banks as much as bigger banks and nonbank lenders specializing in large loans.

In “Lease Expirations and CRE Property Performance,” Wang and her coauthor, Federal Reserve Board of Governors principal economist David Glancy, find that as their leases expire, office buildings in central business districts – areas where onsite work has declined substantially – will likely have more trouble than other CRE properties retaining tenants or attracting new ones at current or higher rents. Vacancies and lower rents will cause a decline in the income that these properties produce for their owners.

The market’s slide will hurt the banking industry through banks’ CRE lending. Property owners that lose income when their office leases expire could default or, due partly to higher interest rates, fail to refinance when their loans mature and the loan principal becomes due. (CRE lending typically involves balloon-type loans, where the bulk of the principal is due at maturity.)

“While the CRE market as a whole has remained relatively resilient since the COVID-19 outbreak, there are segments for which the outcomes of lease expirations point toward serious stresses that are likely to contribute to loan losses in coming years,” Wang and Glancy write.

They note, however, a larger share of smaller banks’ CRE lending involves properties outside central business districts, where the market for office space has remained relatively stable, likely because there has been less of a shift to remote work.

“Office CRE loans make up a small share of (small) banks’ portfolios, and the properties securing these loans tend to be in less adversely affected office markets, which mitigates the risk of bank CRE losses prompting a broad-based credit crunch,” the authors write. “However, some banks’ loan holdings are more concentrated in office loans in troubled markets, which may constrain credit availability for some bank borrowers going forward.”

Effects of lease expirations vary across local CRE markets

Using data from 2009 through 2018, the authors find that before the pandemic, on average, expirations of office leases tended to have little effect on occupancy rates and growth in net operating income, which is the property owner’s rental income minus their costs of operating the property. This suggests that tenants typically renewed their leases or that property owners quickly found new tenants willing to pay rents similar to those that previous tenants paid.

Ultimately, conditions in the local market determine the effects of lease expirations. Wang and Glancy note that in markets with low vacancies, expirations don’t change occupancy rates and even lead to modest increases in income from properties. However, when market vacancies are high, expirations result in greater declines in income and occupancy rates.

“Intuitively, when local demand is weak, expiring leases are less likely to be renewed or replaced at a comparable rent,” the authors write. “Even when the landlord does manage to lease the space again, costlier concessions may be needed to do so, resulting in weaker cash flows after the expiration.”

Office properties in central business districts have been hit hardest

The authors find that since the start of the pandemic, CRE lease expirations overall have had only modestly larger effects on occupancy or income compared with the period before the COVID-19 outbreak. However, for office properties, the estimated effect of lease expirations on occupancy increased by about one-half during the pandemic, and the estimated effect on net operating income rose by about one-third.

The increases in the magnitude of these adverse effects since the start of the pandemic has been greatest in central business districts. The impact of lease expirations on occupancy and on income has roughly doubled for office buildings in central business districts. The authors also find that the effects of lease expirations have been much greater in counties where there has been a large and persistent decline in time spent at workplaces relative to before the pandemic.

Regarding those areas, the authors write, “This corroborates the narrative that demand for office space in those markets has fundamentally weakened, causing property performance to deteriorate as leases roll over and property financial data become more reflective of the true underlying current market conditions.”

{kind=link}

Federal Reserve Bank of Boston

Small banks may be less affected by office lease expirations

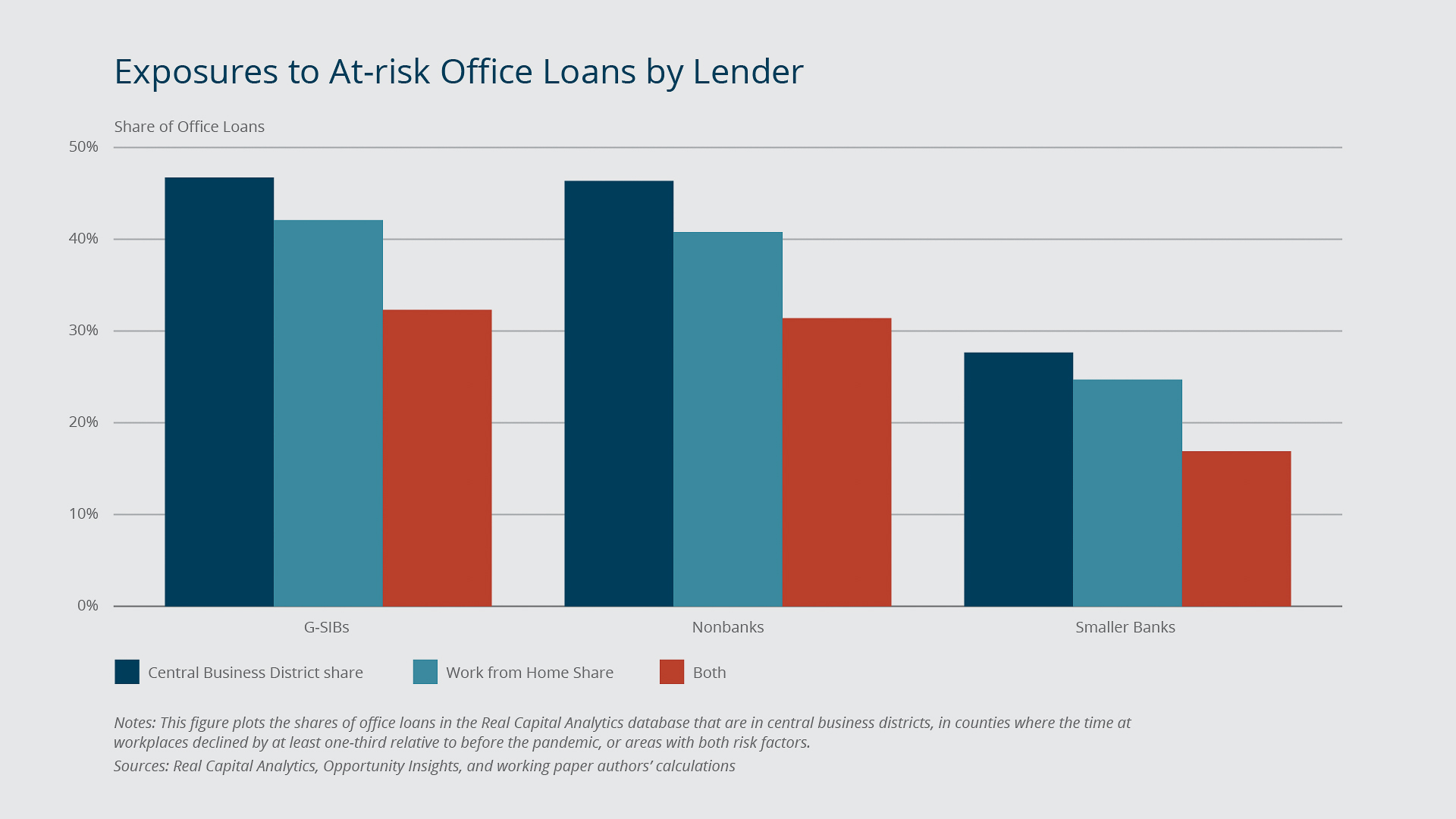

The paper’s findings indicate that smaller banks are less exposed to the risk associated with a weakened office CRE market. This is because, unlike larger banks (which the authors refer to as global systemically important banks, or G-SIBs) and nonbank lenders, they tend to make smaller loans. And those loans typically fund properties located outside central business districts.

The authors estimate that roughly 45% of G-SIBs’ and nonbanks’ office building loans involve central business district properties, and slightly more than 40% are in counties with a high work-from-home share. (See graph above.) By contrast, less than 30% of the office building loans of smaller banks involve properties in either of those areas. In terms of loan volume, the share involving office buildings in central business districts is 32% for G-SIBs and nonbanks and 17%f or small banks.

“While there remains some concern about small and regional banks facing headwinds from high concentrations of CRE loans in addition to funding pressures in the aftermath of recent bank runs,” Wang and Glancy write, “these banks appear to be at least partially protected from loan losses by having most of their office loans in less-affected CRE markets.”

Media Inquiries?

Contact our media relations team. We connect journalists with Boston Fed economists, researchers, and leadership and a variety of other resources.

About the Authors

About the Authors

Larry Bean is the executive editor in the Research department at the Federal Reserve Bank of Boston.

Email: Lawrence.Bean@bos.frb.org

Site Topics

Keywords

- Commercial real estate ,

- COVID-19 ,

- bank loan exposure ,

- office loans ,

- lease expirations