A snapshot of consumer payment choices

Survey of Consumer Payment Choice examines preferences and behaviors

{kind=link}

The 2013 Survey of Consumer Payment Choice—the sixth such survey conducted by the Boston Fed—provides a snapshot of U.S. consumer payment choices that reflects widespread diversity and the influence of new payment innovations but also a persistent reliance on cash.

Each fall, the Federal Reserve Bank of Boston conducts the survey to gain a comprehensive understanding of how U.S. consumers use cash, other paper methods, payment cards, and electronic ways to pay. The survey asks about nine common payment instruments: cash, checks, money orders, traveler’s checks, debit cards, credit cards (including charge cards), prepaid cards, online banking bill payments (OBBP), and bank account number payments (BANP)—plus payments made directly from consumers’ sources of income.

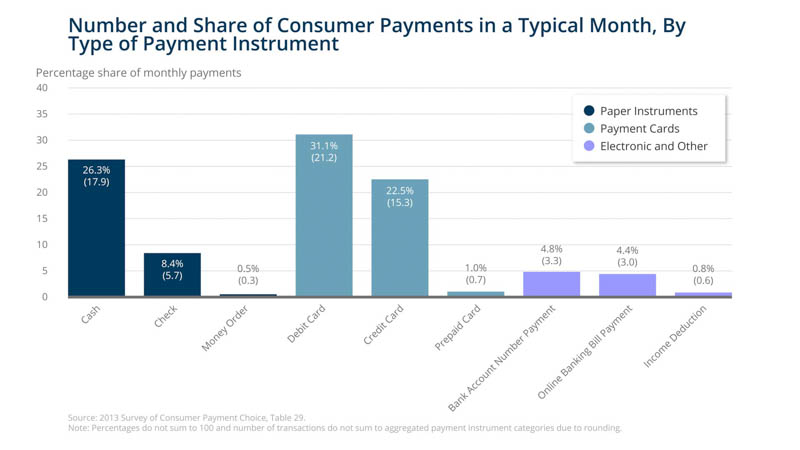

Since the survey’s inception in 2008, there has been a trend toward electronic payments and away from paper checks. The 2013 survey revealed debit cards and cash continue to account for the two largest shares of consumer payments (approximately 31 and 26 percent, respectively), and the credit card share reached about 23 percent. One-hundred percent of consumers either have some cash or have used cash at least once in the past year.

{kind=link}

Christian A Miranda/Federal Reserve Bank of Boston

In 2013, consumers made about 40 payments for retail goods and services in a typical month. The survey also reports the payment choices consumers make in other situations: for bills paid automatically, for online purchases or when repaying a friend, for example. Additionally, the survey reveals consumers’ cash management preferences: how often they get cash and how (from the ATM, a friend, as cash back at the grocery store, among other behaviors).

In almost every annual survey, consumers have selected security as the most important aspect of payments—above cost, convenience, and other attributes. Consumers also rate payment instruments on the ease of acquiring (or setting up) the payment instrument, how likely merchants and other payees are to accept the instrument, and the quality of recordkeeping associated with the instrument.

Data about consumer behavior and preferences can assist policymakers and industry to develop payment methods that satisfy consumers. Survey data brings the voice of the consumer into consumer protection, financial education, and innovations affecting how we pay.

A full report, including 20 figures and 57 tables, is available here.