2014 Series • No. 2014–1

Current Policy Perspectives

Let's Talk About It: What Policy Tools Should the Fed "Normally" Use?

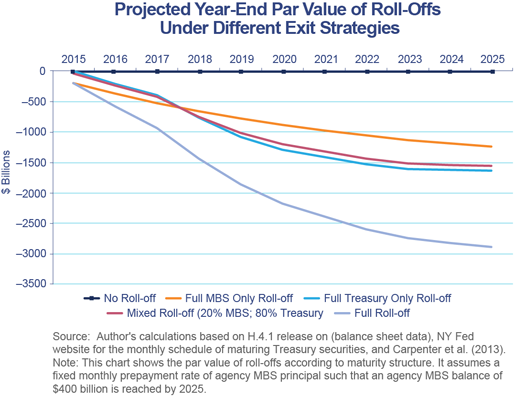

During the onset of a very severe financial and economic crisis in 2008, the federal funds rate reached the zero lower bound (ZLB). With this primary monetary policy tool therefore rendered ineffective, in November 2008 the Federal Reserve started to use its balance sheet as an alternative policy tool when it began the large-scale asset purchases. Now attention is turning to how the Fed should transition back to a more conventional monetary policy stance. Largely missing from these discussions about the Fed's "exit strategy" is a consideration that perhaps it should retain, not discard, the balance sheet tools. Since the Dodd-Frank Act (DFA) has added maintaining financial stability to the Fed's existing dual mandate to achieve maximum sustainable employment in the context of price stability, it might be beneficial to have several tools to achieve multiple policy objectives. An additional consideration is that some of these tools may be needed to stem future crises as a result of the DFA's new limitations on how the Fed can provide liquidity under such adverse circumstances. In an effort to spur a broader debate, this brief discusses what is known and knowable regarding the effectiveness of balance sheet tools and examines four primary arguments for keeping these as part of the Fed's toolkit.

Key Findings

Key Findings

- The relative costs and benefits of conventional versus unconventional policy are difficult to know, so appeals to these types of arguments in favor of one type of policy tool are hard to support. In terms of the absolute costs of balance sheet tools, there was a fear that using such tools would engender high inflation or unanchored inflation expectations. Yet after six years, neither result has occurred.

- Having more than just one primary policy tool confers greater flexibility and may allow the Fed to better fulfill what are now its three policy goals. Moreover, using balance sheet tools to specifically target the sector(s) that are in disequilibrium would let the Fed better focus its policy efforts on the sectors it wants to affect and would diminish some of the potential policy tradeoffs that arise when just one policy instrument is available. Such arguments become even more powerful when the simultaneous objective of ensuring financial stability must be met.

- In a low inflation environment, the probable frequency and duration of hitting the ZLB may actually be much greater than previously appreciated, and hence the need for having alternative policy instruments may be more critical than before.

- With the ability to operate more directly on the asset classes and interest rates it would like to see changed, the Fed may be able to better communicate its policy intentions to market participants.

Exhibits

Implications

While more research is needed to study the relative costs and benefits of conventional versus unconventional monetary policy tools, including the credit allocation effects that result from using the federal funds rate versus more precisely targeted balance sheet tools, there are benefits from using balance sheet tools that are not available from using the federal funds rate alone. Policymakers should seriously consider the gains that could result from keeping balance sheet tools in the Fed's arsenal.

Abstract

The use of a wide variety of monetary and credit policy instruments during the most recent crisis offers a singular opportunity to reconsider the tools the Fed could and should employ when pursuing its goals of supporting the dual mandate and ensuring financial stability. This paper discusses the conventional and unconventional tools that the Fed uses to implement its policies, reviewing what is and is not known about the relative costs and benefits of the different instruments used to achieve its monetary policy mandate and its possibly interdependent and newly enhanced responsibilities for financial stability. A broader reconsideration of these tools may result in a decision to alter the Fed's choice of the policy instruments it uses to support the dual mandate and financial stability. Once decisions are made about which tools are desired for use in the long run, transitioning to that long-run state, or "exit," becomes a more mechanical and technical discussion.