Interest Expenses, Coverage Ratio, and Firm Distress

Historically, the pass-through of federal funds rate increases into firms’ interest expenses has been incomplete and delayed, with the peak responses occurring about one year after a policy rate increase. These findings indicate that current corporate interest rate expenses will continue to increase, even absent any additional rate hikes going forward. Higher interest expenses can lead to firm distress and defaults, which have adverse effects on employment and investment. These effects can be amplified through the financial accelerator channel.

Sign up for new research and data on the New England economy.

An important channel for monetary policy transmission operates through the balance sheets of nonfinancial corporations. Specifically, when the Federal Reserve raises its policy rate—the federal funds rate—this typically increases corporate interest expenses for two main reasons. First, firms with existing floating-rate debt must pay interest on this debt at a rate that moves in line with the prevailing interest rates. Second, firms that wish to refinance existing debt or issue new debt must do so at the new, higher interest rate. (When the Federal Reserve lowers its policy rate, corporate interest expenses decline primarily for the same two reasons).

A rise in corporate interest rates will squeeze firms’ profits and ultimately may render firms less able to borrow, invest, and hire (or retain) workers. This can happen, for example, when an increase in interest expenses results in a decline in firms’ financial performance ratios, including the interest coverage ratio (income relative to interest expenses). Many debt contracts include financial covenants that require firms’ performance metrics to meet certain thresholds, so higher interest expenses can lead to firm distress and, if the covenants are violated, actual defaults. Distress or default in turn has a strong contractionary effect on firms’ demand for labor and investment. This effect can be amplified by the so-called financial accelerator channel, as banks and other lenders reduce their supply of credit in response to realized or anticipated firm defaults, further increasing corporate interest expenses through increased risk premiums.1

In this brief, we look at the effect of interest rate increases on US nonfinancial corporate interest expenses during past monetary policy tightening cycles and draw implications for firms’ risks in the current cycle. Overall, more than a year into the hiking cycle, firms have weathered the steep increases fairly well; corporate interest expenses did not start to increase until the third quarter of 2022. However, firms face continued risks based on the lagged effects of the interest rate hikes that have already occurred, regardless of future hikes.

Firms’ Interest Expenses and Monetary Policy

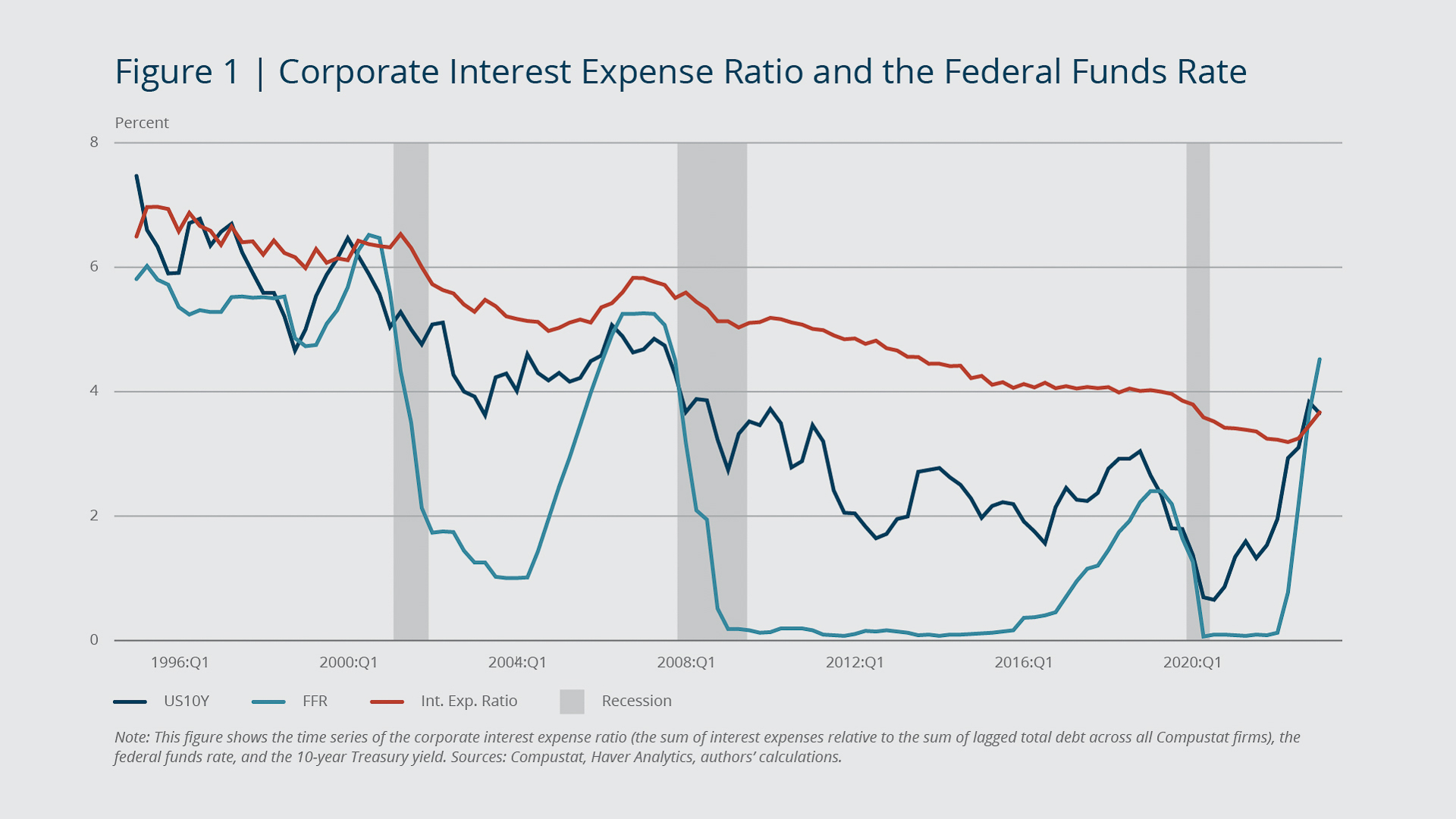

The corporate interest expense ratio, defined as interest expenses as a percentage of lagged total debt, represents the average cost of debt funding for corporations.2 Figure 1 shows the evolution of the corporate interest expense ratio since the mid-1990s, using quarterly data on public firms’ financial statements retrieved from Compustat. For comparison, the figure also depicts the federal funds rate (FFR) and the 10-year Treasury yield (US10Y), which represents the cost of risk-free debt issuance at the 10-year maturity (that is, the marginal risk-free borrowing rate). In general, two key observations stand out. First, all interest rates exhibit a general decline over our sample period, which is consistent with the secular decline in interest rates. Second, the cyclical connection between the FFR and the marginal risk-free borrowing rate is relatively loose, and the same is true for the FFR and the corporate interest expense ratio. The pass-through of FFR changes into the corporate interest expense ratio is incomplete. It’s incomplete because the share of debt that is floating-rate debt (for which the interest rate would adjust more or less in line with the FFR) is relatively small, and due to patterns of staggered refinancing, changes in the marginal cost of funding only gradually affect corporations’ average cost of debt.

{kind=link}

Federal Reserve Bank

Regarding the small floating-rate share of debt, during the COVID-19 pandemic and recovery, firms issued a large volume of bonds, which increased the share of debt that was fixed-rate and extended its average maturity, and thus it has contributed to the delayed and incomplete pass-through during this hiking cycle.

Even though the corporate interest expense ratio is at historically low levels, it did start to increase in the second half of 2023, a potential sign that the steep increase in the federal funds rate since 2021 is beginning to feed through into firms’ cost of borrowing. The significant and sudden change in the monetary policy stance has raised questions about the historical effects of FFR changes on the corporate interest expense ratio.

{kind=link}

Federal Reserve Bank

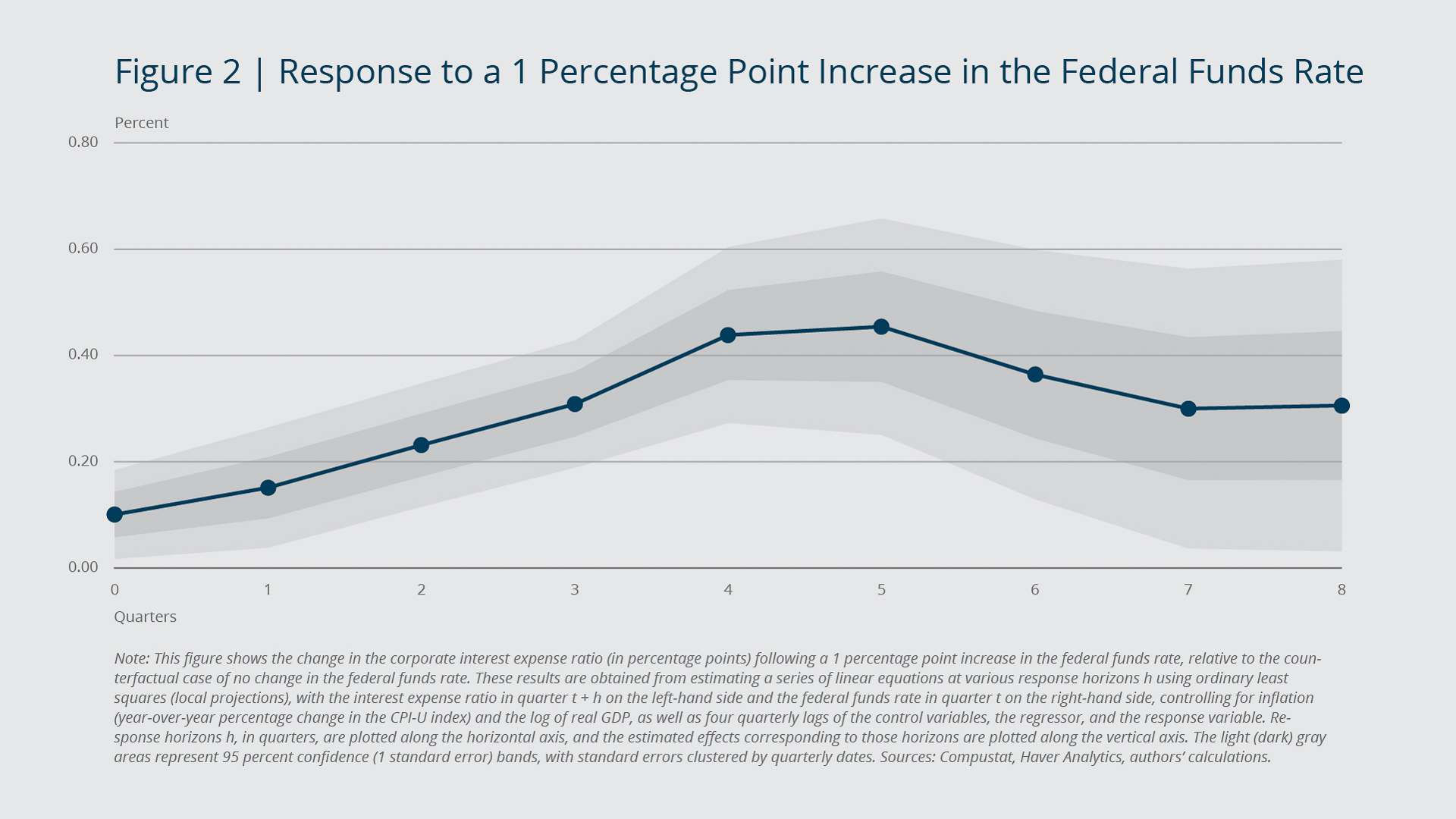

Using the full sample of nonfinancial firms in the Compustat database from 1995 through 2019, we estimate the average response of the corporate sector’s interest expense ratio to changes in the FFR. Our estimate accounts for other macroeconomic factors, including the past dynamics in interest rates and economic activity. We use lag-augmented local projections (Jordà 2005; Montiel Olea and Plagborg-Møller 2021), a method widely employed in the empirical macroeconomics literature. Figure 2 shows how a 1 percentage point increase in the FFR has affected the corporate interest expense ratio historically. The figure shows that the ratio has not responded 1-for-1 to changes in the FFR; rather, there is partial pass-through of about 50 percent. In other words, a 1 percentage point increase in the FFR raises the average corporate interest expense ratio by about 0.5 percentage point.

Furthermore, and perhaps most strikingly, the pass-through is gradual and peaks five quarters after the initial 1 percentage point FFR increase. With respect to the current cycle, this finding suggests that most of the interest rate increases still have not fully fed into firms’ interest expenses. The initial rate increase of 0.25 percentage point in March 2022 may have fully passed through into the corporate interest expense ratio, but firms have yet to see the full impact of the subsequent 5 percentage points of rate increases.

Current Interest Expenses and Firm Risk

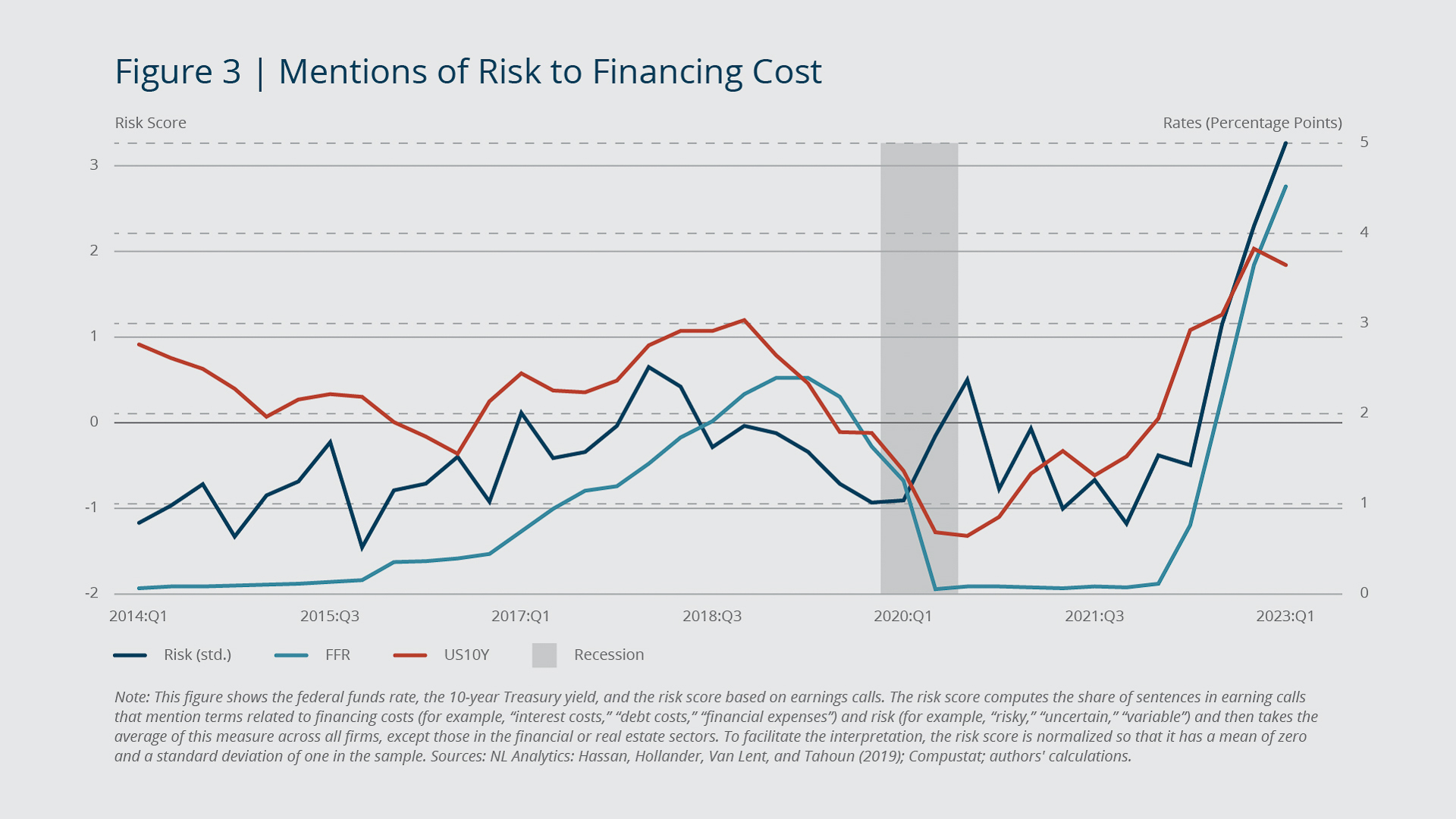

While corporate interest expenses have only recently started to rise, firms are increasingly worried about this issue, as evidenced by their earnings call statements. We quantify their level of concern using a risk score based on the number of times an earnings call includes phrases such as “interest expense” paired with the word “risk” or “uncertainty” or a synonym, divided by the total number of sentences in the call.

{kind=link}

Federal Reserve Bank

Figure 3 presents this risk score for public firms outside the financial and real estate sectors along with the federal funds rate and the 10-year Treasury yield for comparison.3 The findings, as depicted in the figure, indicate that these firms have become more concerned with their interest expenses than they had been over the last decade, and this concern has increased with the recent hiking cycle. Insofar as the risk score is forward looking, the findings also indicate that firms believe the recent increases in interest rates may continue to put pressure on them, even after the hiking cycle has ended.

Current Cycle and Debt at Risk of Default

We next turn to the implications of the current monetary policy tightening cycle for firms’ interest coverage ratio (ICR), an important financial performance measure with implications for real outcomes such as firm investment and employment. The ICR is typically defined as the ratio of earnings before interest, taxes, depreciation and amortization (EBITDA) to interest expenses (both measured as four-quarter rolling sums). The ICR is a crucial metric for debt and equity investors and is prevalent in debt contracts, particularly in financial covenants.

Financial covenants are provisions included in the vast majority of commercial loan contracts. They can limit the set of actions a borrower can take or specify thresholds for key financial indicators. For instance, a covenant can specify that the firm’s ICR cannot be less than 4 at the end of any fiscal quarter. An increase in interest expenses thus can cause a violation of these covenants.4 A covenant violation is considered a technical default and gives the lender the right to accelerate the repayment of the loan, to obtain better terms through a renegotiation (for instance, higher interest rates), or to take control of the firm. Chodorow-Reich and Falato (2022) show that the reduction in credit to borrowers that violate a covenant was an important factor in the 2008–2009 financial crisis. The finance literature highlights that a covenant violation (or simply approaching a violation) can lead to a contraction in investment and employment because firms will make adjustments to stay above their contractual ICR limit (see, for instance, Chava and Roberts 2008, and Bräuning, Ivashina, and Ozdagli 2022). Beyond this direct effect, firms’ distress can be amplified through a financial accelerator whereby lenders’ credit supply contracts as defaults erode their net worth.

{kind=link}

Federal Reserve Bank

We conduct an exercise in which we take the recent monetary policy tightening, coupled with various future corporate income scenarios, and compute the share of debt outstanding in firms that could have an ICR of less than 4 at the end of this year, that is, firms that could be in violation of their financial covenants and thus at risk of default. Because the ICR depends on total interest expenses (and not the interest rate), we first redo the analysis from Figure 2 for the cumulative growth of interest expenses and then compute the expected growth of firms’ interest expenses from the second to fourth quarters of 2023. We find that firms’ interest expenses are expected to grow approximately 23 percent by the end of 2023. Finally, we compute the share of debt at risk of default for various income scenarios relative to 2022: no change in income or an increase or decrease by 5, 10, or 20 percent. As a reference point, note that firms’ EBITDA fell roughly 24 percent in our sample during the Great Financial Crisis. The results, shown in Figure 4, point to a significant increase in the shares of debt at risk during this cycle of monetary tightening. The shares are roughly equivalent to those at the onset of the COVID-19 pandemic.

The views expressed herein are those of the authors and do not indicate concurrence by the Federal Reserve Bank of Boston, the principals of the Board of Governors, or the Federal Reserve System.

Endnotes

- The financial accelerator channel is the process through which adverse shocks to the economy are amplified as credit market conditions worsen. See Bernanke, Gertler, and Gilchrist (1996).

- Using quarterly data, we compute the interest expense ratio as interest expenses during a given quarter over the stock of total debt at the end of the preceding quarter.

- For more detail on the textual analysis, see Hassan et al. (2019).

- Greenwald (2019) estimates that 80 to 90 percent of loans have ICR-based financial covenants. Typically, an ICR covenant threshold is about 3, and when a firm’s ICR falls below 4, the firm may be deemed in distress.

References

Bernanke, B., M. Gertler, and S. Gilchrist. 1996. “The Financial Accelerator and the Flight to Quality.” The Review of Economics and Statistics 78(1): 1–15.

Bräuning, F., V. Ivashina, and A. Ozdagli. 2022. “High-yield Debt Covenants and Their Real Effects.” National Bureau of Economic Research Working Paper No. 29888

Chava, S. and M. R. Roberts. 2008. “How Does Financing Impact Investment? The Role of Debt Covenants.” The Journal of Finance 63(5): 2085–2121.

Chodorow-Reich, G. and A. Falato. 2022. “The Loan Covenant Channel: How Bank Health Transmits to the Real Economy.” The Journal of Finance 77(1): 85–128.

Greenwald, D. 2019. “Firm Debt Covenants and the Macroeconomy: The Interest Coverage Channel.” MIT Sloan Research Paper No. 5909-19.

Hassan, T. A., S. Hollander, L. Van Lent, and A. Tahoun. 2019. “Firm-level Political Risk: Measurement and Effects.” The Quarterly Journal of Economics 134(4): 2135–2202.

Jordà, O. 2005. “Estimation and Inference of Impulse Responses by Local Projections.” American Economic Review 95(1): 161–182.

Montiel Olea, J. L. and M. Plagborg-Møller. 2021. “Local Projection Inference Is Simpler and More Robust Than You Think.” Econometrica 89(4): 1789–1823.

About the Authors

About the Authors

Falk Bräuning,

Federal Reserve Bank of Boston

Falk Bräuning is a vice president and economist in the Federal Reserve Bank of Boston Research Department.

Email: falk.braeuning@bos.frb.org

Gustavo Joaquim

Hillary Stein,

Federal Reserve Bank of Boston

Email: hillary.stein@bos.frb.org

Acknowledgments

The authors thank Lucy McMillan for providing outstanding research assistance.

Resources

Site Topics

Keywords

- monetary policy ,

- interest expenses ,

- firm distress

JEL Codes

- E32 ,

- E52 ,

- G32

Citation

Bräuning, Falk, Gustavo Joaquim, and Hillary Stein. 2023. “Interest Expenses, Coverage Ratio, and Firm Distress.” Federal Reserve Bank of Boston Current Policy Perspectives, August 29, 2023.