The Historical Effects of Banking Distress on Economic Activity

The failures of several U.S. regional banks have stimulated discussions about the macroeconomic effects of a likely credit contraction triggered by the recent banking turmoil. Drawing on historical evidence from advanced economies, this study documents a sizable and persistent decline in output and rise in unemployment following non-systemic financial distress. The effects of a systemic banking crisis are two to four times as large. High corporate leverage exacerbates banking turmoil, whereas high bank capitalization and a relatively large share of market financing in corporate debt mitigate it. These channels approximately offset one another so that the estimates tailored to the current U.S. economy are in line with the average effect.

Sign up for new research and data on the New England economy.

The recent failures of Silicon Valley Bank, Silvergate Bank, and First Republic Bank in the United States and of Credit Suisse in Europe have spurred renewed interest in the effects of banking distress on economic activity. Following these bank failures, policymakers promptly pointed to the contractionary effects of tightening credit conditions as a reason to reassess the monetary policy stance consistent with price stability and full employment. But how large are the contractionary effects of banking crises, how fast do they materialize, and how long do they last?

To contribute to this ongoing debate, this study evaluates the macroeconomic effects of banking distress by examining historical episodes that took place in advanced economies, including the United States, during the modern period.1 These episodes include not only systemic crises but also milder banking distress, which is a useful benchmark since the current turmoil may not be systemic. Although there are differences across the countries analyzed in this brief, all are highly developed and share many important characteristics, such as a developed financial market and banking system. Thus, such international evidence can provide useful context for our understanding of contemporary events.2

The key result presented in this brief shows that even non-systemic financial distress is typically followed by a sizable and persistent economic contraction. A systemic banking crisis has two to four times larger contractionary effects on output and employment compared with an episode of non-systemic financial distress. The degree of corporate leverage, market-based financing, and bank capitalization can generate some heterogeneity in the output effects: The effects of financial distress are amplified by a highly leveraged business sector but dampened if corporate debt is financed by bonds rather than bank loans and if the banking system is well capitalized.

Historical Episodes of Financial Distress

This analysis uses data from two sources. One is a compilation of crisis indicators by Reinhart and Rogoff (2009), who differentiate across types of crises such as financial distress, systemic banking crises, currency crises, and other types in a global setting.3 The other is the Macrohistory Database (see Jordà, Schularick, and Taylor 2017; Jordà et al. 2021), which provides long time series on financial conditions as well as economic activity and labor market characteristics for a variety of advanced economies.4 Note that this database also contains an indicator for a financial crisis, but unlike Reinhart and Rogoff's data, it does not differentiate across types of crises. Such a differentiation, however, is key for the analysis presented in this brief, which focuses primarily on the effects of non-systemic financial distress.5

The estimation sample covers 16 advanced economies during the 1960–2014 period, with the output and unemployment effects analyzed through 2019.6 Of the 27 financial distress episodes occurring in this sample, 10 correspond to a systemic banking crisis. These episodes include the post-Franco crisis of the late 1970s in Spain; the banking crises of the early 1990s in Finland, Norway, and Sweden; Japan's banking crisis of the 1990s; and the 2007–2008 Global Financial Crisis in some countries.7

The non-systemic financial distress episodes are distributed more evenly than the systemic crises. Such episodes include those that occurred in the United Kingdom in the mid-1970s, mid-1980s, and early 1990s; in Germany in the late 1970s; in Canada in the mid-1980s; in the United States in the late 1980s (the savings and loan crisis); in Australia and Italy in the early 1990s; in France in the mid-1990s; and others. For six countries, the Global Financial Crisis was also an episode of non-systemic distress. Thus, history provides substantial variation in the geography, time, and severity of financial distress to identify its impact on the economy.

{kind=link}

Federal Reserve Bank of Boston

Effects on Output and Unemployment

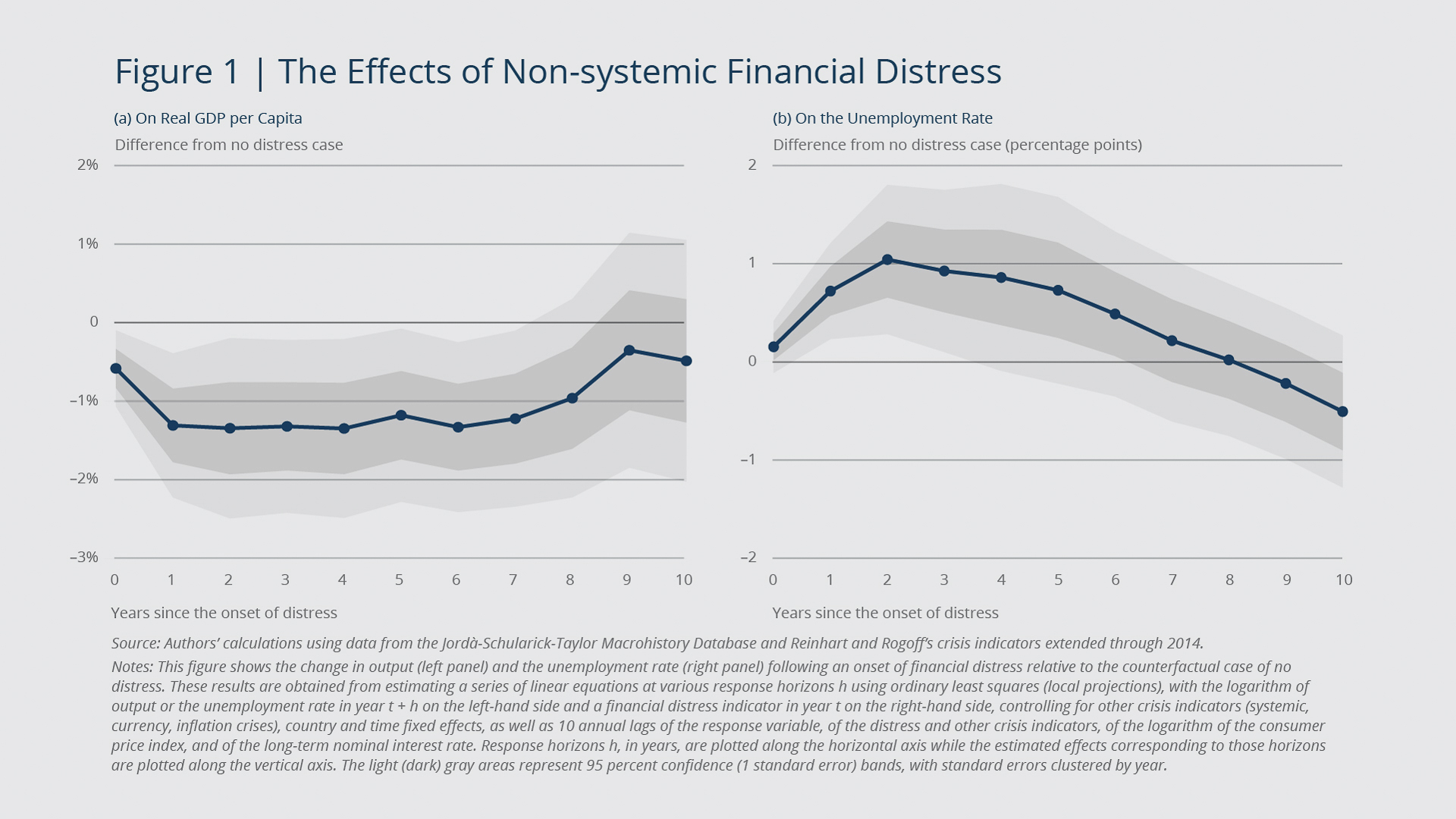

Figure 1 shows that non-systemic financial distress in the banking system has sizable and persistent contractionary effects on real GDP per capita and the unemployment rate. These effects are estimated using lag-augmented local projections (Jordà 2005; Montiel Olea and Plagborg-Møller 2021), a method widely used in the empirical macroeconomic literature. The estimates show that banking distress, on average, leads to a reduction in output of 1.3 percent one year after its onset and a peak increase in the unemployment rate of 1.0 percentage point two years after the onset.

Real consumption per capita and real investment per capita both decline persistently following an episode of financial distress.8 Real consumption declines 2.7 percent and real investment 7.6 percent after three years. The large estimated decline in investment confirms that this component of output is particularly sensitive to financial conditions. The estimated effect on inflation is not as clear and appears to be statistically insignificant.

While the Global Financial Crisis features prominently during the sample period, the estimated effects on output and unemployment remain large when we exclude this episode from the sample. In the sample ending in 2002 (and the economic effects measured through 2006), the effects on output are approximately the same as those in the baseline sample, whereas the effects on unemployment, at their peak, are about half the magnitude of the baseline value.

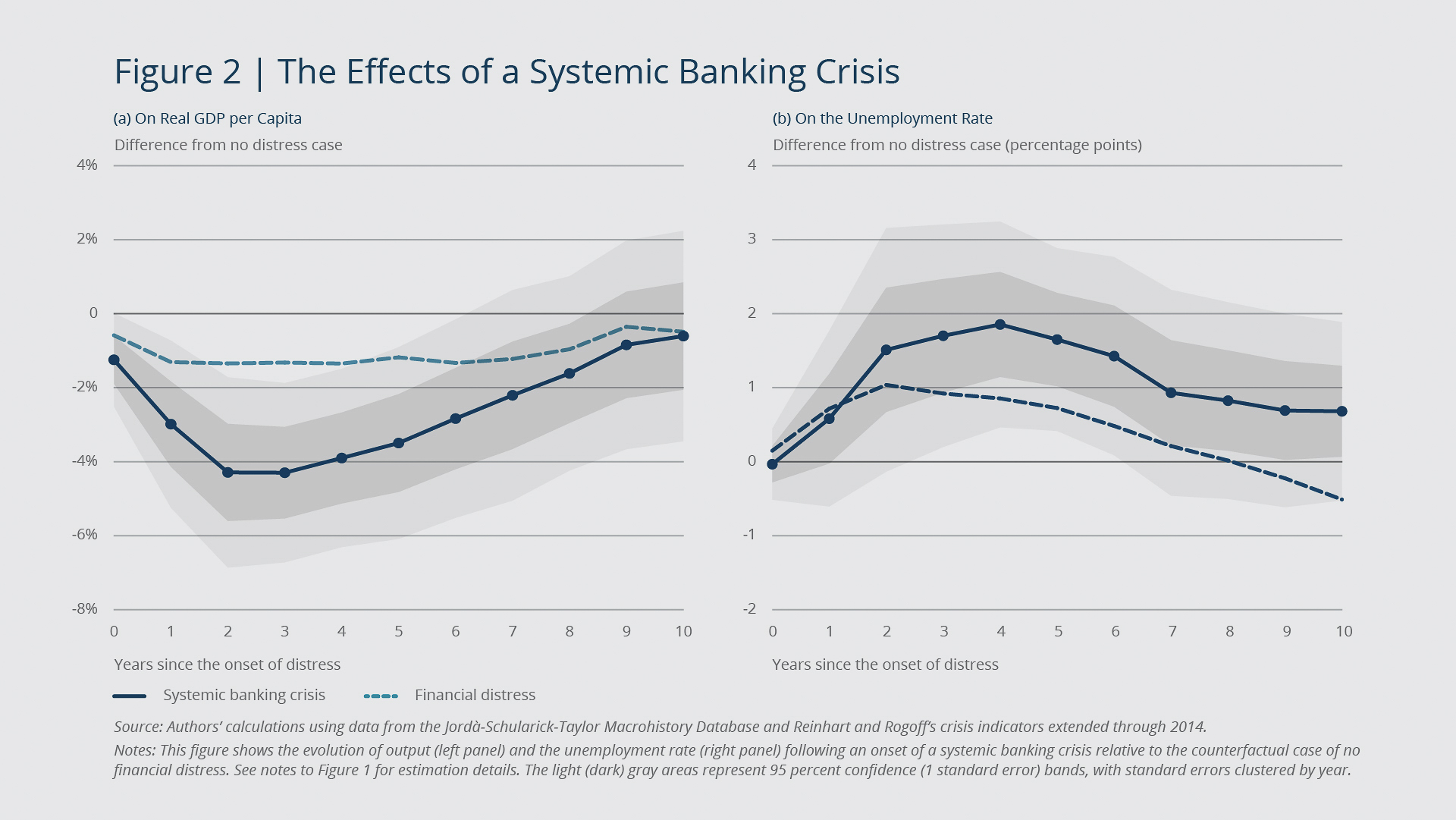

The baseline estimates of the banking distress effects documented in Figure 1 are moderate, in part because those episodes exclude systemic banking crises.9 Figure 2 shows that a systemic banking crisis has an effect on output that is as much as four times greater compared with financial distress and a peak effect on unemployment that is two times greater. For comparison, the blue dashed lines in the figure show the previously discussed effects of non-systemic banking distress. The remainder of this brief focuses on non-systemic financial distress episodes, since systemic crises are relatively rare and have received significant attention in previous studies. Nevertheless, they may provide a useful benchmark as an upper bound of the effects of problems in the banking system.

{kind=link}

Federal Reserve Bank of Boston

Amplification Factors

The effects discussed so far correspond to the average financial distress period during our sample period. The output decline due to financial distress likely depends on the amount of credit in the economy, the role that depository institutions play in credit intermediation, and the resilience of the financial sector to adverse shocks, among other factors. The wide variety of international financial distress episodes analyzed in this brief can be used to assess the relative contribution of these factors to heterogeneity in the real effects of financial distress.

This study finds that non-systemic banking distress leads to a larger output decline when the non-financial business sector is highly leveraged, as measured by debt to income. Specifically, an increase in non-financial business debt of 10 percent of GDP amplifies output declines one year after the onset of the financial shock by 0.42 percentage point, which is about one-third of the average decline. This and the related estimates discussed below are obtained by interacting the financial distress indicator with the annual lag of the corresponding measure—business debt as a share of GDP, in this case.10

Next, a higher share of market-based financing (for example, through issuance of corporate bonds) relative to bank financing (that is, bank loans) in total business debt helps mitigate banking distress. This study estimates that a 5 percentage point increase in the share of business debt financed by bond issuance reduces the output decline due to financial distress by 0.55 percentage point after one year. To illustrate the scale of this effect, note that the average observation in the sample is characterized by a roughly 50-50 split between bank loans and market funding.

The effects of banking distress on the economy are less pronounced in better-capitalized banking systems. A 1 percentage point increase in the bank capital ratio (bank equity divided by assets) leads to a 0.27 percentage point reduction in the output decline one year after the shock and a 0.66 percentage point reduction in the output decline after two years. Hence, while increased bank capitalization has a relatively modest effect at the peak of financial distress, it can shorten the crisis substantially.

Overall, these results are intuitive: Higher leverage makes businesses more vulnerable to a tightening in bank lending standards and a credit contraction, while higher bank equity stimulates credit supply and enhances banks' capacity to absorb shocks.

Implications for the Current Banking Issues

The factors amplifying or dampening the effects of financial distress are not only important for cross-country differences but highly relevant for the ongoing domestic policy discussions. The U.S. economy, on the one hand, is characterized by historically high corporate leverage. On the other hand, the U.S. banking system is likely better positioned to withstand an adverse financial shock than it was during the 2007–2008 financial crisis, due in part to improved regulation following that episode. Moreover, the domestic economy is supported by deep financial markets, which could mitigate the credit distress stemming from a specific segment of the banking sector such as regional banks.

In lieu of concluding remarks, this study performs back-of-the-envelope calculations of the effect of non-systemic financial distress, similar in size to the typical episode in the sample, on domestic output. These calculations combine the latest observations of debt over GDP, bank loans over business debt, and the bank capital ratio for the United States with the estimates discussed above. The negative effect of relatively high corporate leverage in the United States is almost entirely offset by the positive effects of relatively high bank capitalization and a relatively small share of bank loans in business debt. The resulting estimate of output decline one year after the onset of non-systemic financial distress equals 1.4 percent, which is statistically indistinguishable from the 1.3 percent estimated in the full sample without accounting for heterogeneity.

While the historical evidence presented in this brief provides a useful benchmark of the quantitative effects of banking distress, it is still early to assess the size of the financial shock. The current banking turmoil also differs from past stress episodes in various ways that deserve separate coverage. Thus, it remains to be seen whether this time is going to be different.

The views expressed herein are those of the authors and do not indicate concurrence by the Federal Reserve Bank of Boston, the principals of the Board of Governors, or the Federal Reserve System.

Endnotes

- This study builds on vast academic research studying financial crises. For influential empirical studies, see Bernanke (1983), Peek and Rosengren (2000), and Khwaja and Mian (2008), among many others. For examples of theoretical contributions, see Bernanke and Gertler (1989), Kiyotaki and Moore (1997), Gertler and Kiyotaki (2010, 2015), and Gertler, Kiyotaki, and Prestipino (2020).

- Examples of influential studies that employ cross-country data to quantify the macroeconomic effects of financial distress include Bordo et al. (2001), Reinhart and Rogoff (2009, 2013), Jordà, Schularick, and Taylor (2013, 2016), and Jordà et al. (2022). Sufi and Taylor (2022) provide a comprehensive survey of this literature and estimates.

- These data, updated through at least 2014, are available from Harvard Business School's Behavioral and Financial Stability Project at https://www.hbs.edu/behavioral-finance-and-financial-stability/data/Pages/global.aspx.

- We use Release 6 (July 2022) of this database, which can be accessed at https://www.macrohistory.net/database/.

- Another difference between these sources is that the Macrohistory Database indicates the onset but not the duration of a crisis. This difference, however, plays a lesser role in the analysis here because we control for the lags of the financial distress indicator as well as other observable variables, thereby extracting the unforeseen component of a crisis.

- The country coverage follows that in the Macrohistory Database, except for Ireland and Switzerland, for which the financial distress indicator is not available from the other source. While the original sample is selected starting in 1950, the 1950–1959 period is not in the estimation sample because it is used for lag controls. We omit the period prior to 1950 because the global financial system was likely too different from the modern one to be informative for contemporary policy issues.

- The year 2008 is associated with a systemic banking crisis in six countries in the sample, with financial distress in another six countries, and with neither a systemic crisis nor financial distress in four countries.

- In the interest of space, the figures showing the responses of GDP components and other variables are not shown but described briefly in the text.

- During systemic crises, as defined in the literature, the financial system experiences significant bank runs that result in the closure or takeover by the public sector of important financial institutions.

- The estimated model includes lags of leverage and other variables discussed in this section as control variables. All such variables as well as the corresponding interaction terms are included simultaneously to account for cross- correlations. Secular trends in leverage and other continuous financial variables are removed by using deviations from five-year, backward moving averages.

References

Bernanke, Ben S. 1983. "Nonmonetary Effects of the Financial Crisis in Propagation of the Great Depression." American Economic Review 73(3): 257–276.

Bernanke, Ben S., and Mark Gertler. 1989. "Agency Costs, Net Worth, and Business Fluctuations." American Economic Review 79(1): 14–31.

Bordo, Michael, Barry Eichengreen, Daniela Klingebiel, and Maria Soledad Martinez-Peria. 2001. "Is the Crisis Problem Growing More Severe?" Economic Policy 16(32): 52–82.

Gertler, Mark, and Nobuhiro Kiyotaki. 2010. "Financial Intermediation and Credit Policy in Business Cycle Analysis." In Handbook of Monetary Economics, vol. 3, edited by Benjamin M. Friedman and Michael Woodford, 547–599. San Diego, Calif.: Elsevier.

———. 2015. "Banking, Liquidity, and Bank Runs in an Infinite-Horizon Economy." American Economic Review 105(7): 2011–2043.

Gertler, Mark, Nobuhiro Kiyotaki, and Andrea Prestipino. 2020. "A Macroeconomic Model with Financial Panics." Review of Economic Studies 87(1): 240–288.

Jordà, Òscar. 2005. "Estimation and Inference of Impulse Responses by Local Projections." American Economic Review 95(1): 161–182.

Jordà, Òscar, Martin Kornejew, Moritz Schularick, and Alan M. Taylor. 2022. "Zombies at Large? Corporate Debt Overhang and the Macroeconomy." Review of Financial Studies 35(10): 4561–4586.

Jordà, Òscar, Björn Richter, Moritz Schularick, and Alan M. Taylor. 2021. "Bank Capital Redux: Solvency, Liquidity, and Crisis." Review of Economic Studies 88(1): 260–286.

Jordà, Òscar, Moritz Schularick, and Alan M. Taylor. 2013. "When Credit Bites Back." Journal of Money, Credit and Banking 45(s2): 3–28.

———. 2016. "Sovereigns versus Banks: Credit, Crises, and Consequences." Journal of the European Economic Association 14(1): 45–79.

———. 2017. "Macrofinancial History and the New Business Cycle Facts." NBER Macroeconomics Annual 31(1): 213–263.

Khwaja, Asim Ijaz, and Atif Mian. 2008. "Tracing the Impact of Bank Liquidity Shocks: Evidence from an Emerging Market." American Economic Review 98(4): 1413–1442.

Kiyotaki, Nobuhiro, and John Moore. 1997. "Credit Cycles." Journal of Political Economy 105(2): 211–248.

Montiel Olea, José Luis, and Mikkel Plagborg-Møller. 2021. "Local Projection Inference Is Simpler and More Robust Than You Think." Econometrica 89(4): 1789–1823.

Peek, Joe, and Eric S. Rosengren. 2000. "Collateral Damage: Effects of the Japanese Bank Crisis on Real Activity in the United States." American Economic Review 90(1): 30–45.

Reinhart, Carmen M., and Kenneth S. Rogoff. 2009. This Time Is Different: Eight Centuries of Financial Folly. Princeton, N.J.: Princeton University Press.

———. 2013. "Banking Crises: An Equal Opportunity Menace." Journal of Banking & Finance 37 (11): 4557–4573.

Sufi, Amir, and Alan M. Taylor. 2022. "Financial Crises: A Survey." In Handbook of International Economics, vol. 6, edited by Gita Gopinath, Elhanan Helpman, and Kenneth Rogoff, 291–340. Amsterdam: Elsevier.

About the Authors

About the Authors

Falk Bräuning,

Federal Reserve Bank of Boston

Falk Bräuning is a vice president and economist in the Federal Reserve Bank of Boston Research Department.

Email: falk.braeuning@bos.frb.org

Viacheslav Sheremirov,

Federal Reserve Bank of Boston

Viacheslav Sheremirov is a principal economist in the Federal Reserve Bank of Boston Research Department.

Email: Viacheslav.Sheremirov@bos.frb.org

Acknowledgments

The authors thank Philippe Andrade, Susan M. Collins, Chris Foote, Maria Luengo-Prado, Giovanni Olivei, Joe Peek, and Jenny Tang for very helpful comments and suggestions. Noah Flater provided excellent research assistance.

Resources

Site Topics

Keywords

- banking distress ,

- Real Economy ,

- financial crises

JEL Codes

- E44 ,

- F30 ,

- G01 ,

- G21

Citation

Bräuning, Falk, and Viacheslav Sheremirov. 2023. “The Historical Effects of Banking Distress on Economic Activity.” Federal Reserve Bank of Boston Current Policy Perspectives. May 25, 2023.